New Zealand banks saw a bounce back in profitability in the June quarter after a fall in impaired asset expense and a rise in non-interest income due to greater gains on trading and hedging products.

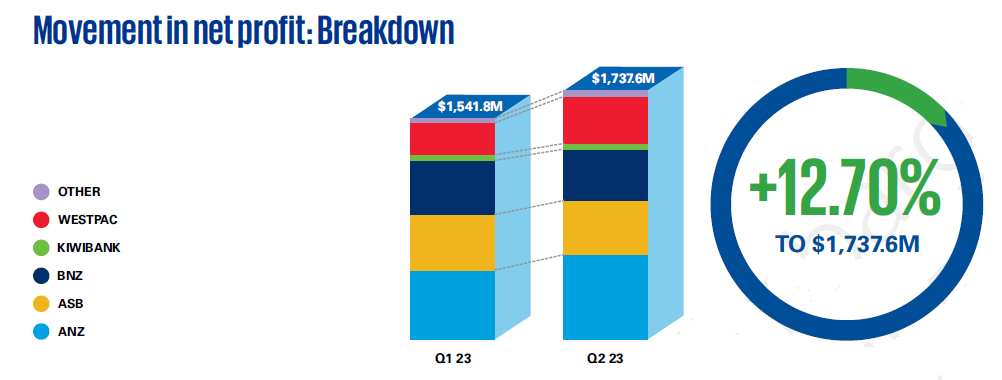

The latest Financial Institutions Performance Survey (FIPS) quarterly update from auditing and financial advisory firm KPMG shows that the banking sector net profits after tax (NPAT) bounced back 12.7%, rising from $1.54 billion in the quarter ended March 2023 to $1.74 billion in the quarter ended June 2023. This followed a 13% drop in the March quarter.

Compared with the June quarter a year ago, the NPAT for the banks was up - just - by 0.55%. (The graphs in this article are from the latest FIPS publication)

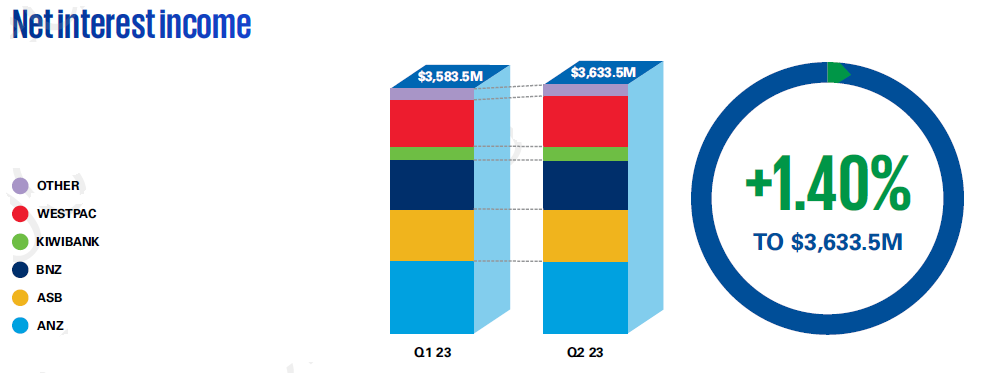

However, the latest resurgence in profits was not particularly due to net interest income, as this remained in KPMG's words, "somewhat flat this quarter", increasing by 1.4% to $3.63 billion. That is, however, up 12.8% on the net interest income in the same quarter of 2022.

But the "usually volatile" non-interest income saw a 30.4% June quarter 2023 rise compared with the March quarter - up from $443.8 million to $578.7 million. KPMG said this figure has risen this quarter due to greater gains on trading and hedging products.

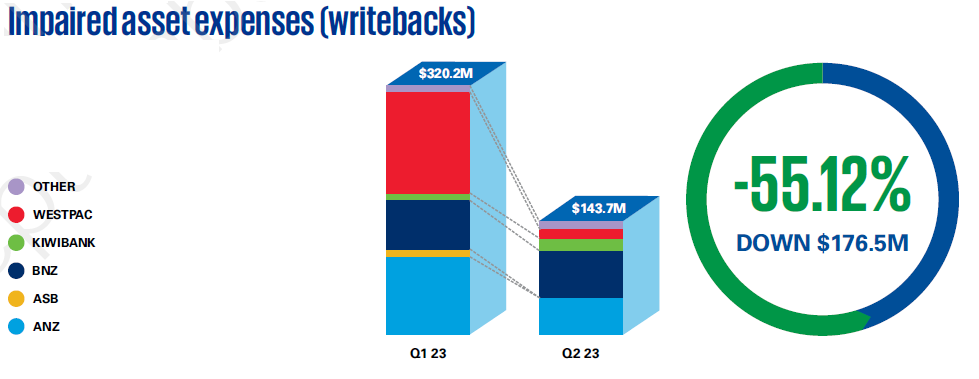

In the March quarter NZ banks' impaired asset expenses as a percentage of their total operating expenses had risen to their highest level, excluding the height of the Covid-19 period, since 2011. That was according to KPMG's March FIPS. Impaired asset expense rose 192% in the March quarter from the December quarter to $320.2 million, with both individual and collective provisions rising.

That's fallen in the June quarter, as explained by KPMG partner John Kensington.

"...There has been a fall in impaired asset expense. It is important to note that although the impaired asset expense has decreased, it’s still the second largest impaired asset expense since the start of the pandemic and has driven a 2% increase in provisions on lending," he said.

Impaired asset expenses fell by 55.1% to $143.7 million following the March 2023 quarter’s expense of $320.2 million.

Provisions, however, continue to increase due to increasing arrears.

"Provisions have been steadily increasing since the start of 2022 as borrowers face challenging economic conditions with rising interest rates and the cost of living," Kensington said.

"The June 2023 quarter is the second consecutive quarter in which each of the five major banks have reported an increase in the percentage of loans which are past due, indicating more customers are struggling to meet their repayments. With inflation and interested rates high, if we see this trend continue through the second half of the year, it is likely that we could see further increases in provisions."

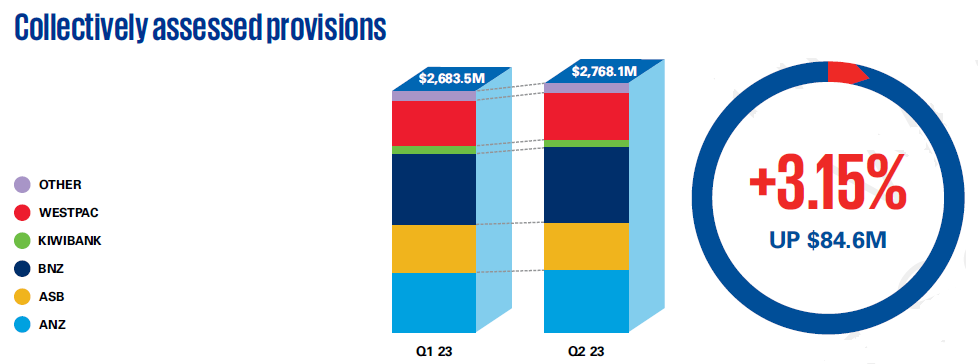

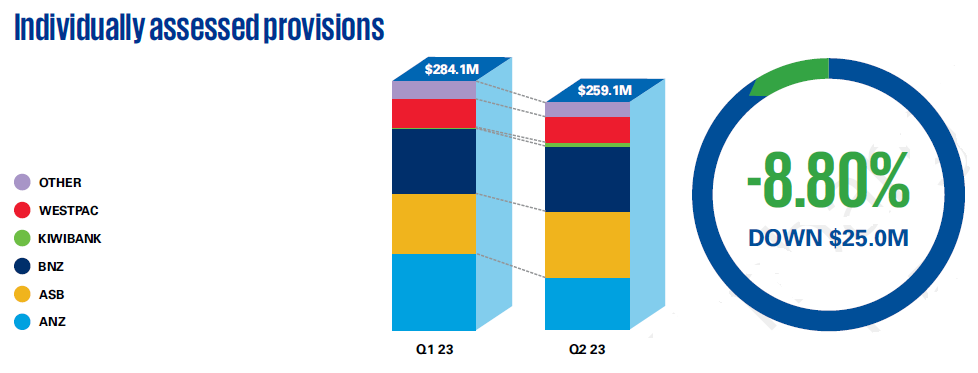

The results for the quarter showed collective provisioning continued to increase for the sixth consecutive quarter. The increase has slowed this quarter with growth of 3.15% to a total of $2.768 billion after the March 2023 quarter’s 10.7% increase. Individual assessed provisioning saw a decrease of 8.8% this quarter to $259.1 million. Overall, total provisioning increased by 2.0% to $3.03 billion, building on last quarter’s 10.4% increase.

In the latest FIPS, Centrix Credit Bureau managing director Keith McLaughlin has a close look at where arrears are coming from.

He said there had been an upward trend across all age groups since 2020.

"However, it’s clear the younger generations in Aotearoa New Zealand are the ones doing it toughest.

"Zeroing in on the under 25-year-old segment, some interesting credit behaviour has emerged. There are over 260,000 credit active consumers in this age group, of which 57% use Buy Now, Pay Later (BNPL) products while only 12% are credit card users."

He said BNPL products are now the most common first credit product for this age group, accounting for 47% of first credit events (or earliest credit account on file). This is followed by telco accounts (28%), auto loans (9%) and utilities (7%).

"However, this age group is also experiencing climbing arrears and debt stress, up significantly since 2020 and driven by overdue telco, personal loan and BNPL repayments. There are several factors likely to contribute to this. In this group, most will be living from pay day to pay day, having just entered the workforce or studying and working part- time. They tend to have less savings to draw upon and are often inexperienced in managing finances."

McLaughlin said in contrast, older generations are likely to have established savings and higher incomes to help weather the day-to-day impacts of the economic climate. Those aged 50 and over, for example, saw an uptick in arrears near the beginning of 2022, but have managed to weather the current climate.

Looking at the mortgage market, he said "after the highs of 2021", demand for new mortgage lending has slowed throughout 2022 and 2023.

"However, as we get through 2023, this cooling appears to be slowing and suggests a shift in tide for the housing market."

He said the 39–41 years age group currently holds the largest average outstanding mortgage amount at $627,000, followed by 36–38 years ($614,000) and 33–35 years ($607,000).

Home loan delinquencies have risen steadily since 2022, "but are currently in a state of relative stability".

On the whole, 30+ days’ delinquencies have risen across all age groups "with a notable acceleration for those aged under 30 years old".

"However, it is important to remember this arrears growth is coming off record low arrears recorded throughout 2022 and overall remains below long-term averages."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.