BNZ's half-year profit dropped 5% as income and its net interest margin fell, and expenses rose 11%.

The bank reported net profit after tax for the six months to March 31 of $762 million, down $43 million, or 5%, from $805 million in the same period of its previous financial year.

BNZ's total operating income fell $5 million to $1.770 billion, with net interest income down $2 million to $1.462 million.

CEO Dan Huggins says BNZ's annual net interest margin, the difference between what the bank borrows money at through the likes of deposits and what it lends it out at, dropped eight basis points year-on-year to 2.37%.

Operating expenses increased $64 million, or 11%, to $641 million with increased spending on staff salaries and higher technology spend factors in the rise. BNZ's cost-to-income ratio rose 370 basis points to 36.2%.

The bank's annual credit impairment charge fell $8 million to $71 million.

"High interest rates and cost of living pressures continue to impact business and household finances," Huggins says.

"While easing inflation is encouraging, it is expected to remain outside of the Reserve Bank's target band until the end of the year. Economic conditions are likely to remain challenging until there is a material reduction in interest rates."

"Supporting our customers through these challenging times remains our top priority," Huggins says.

BNZ says its lending grew $2.4 billion, or 2.4% in the March half-year to $104.2 billion, with home lending rising $1.1 billion, or 1.9%, to $58.8 billion, and business lending up $1.3 billion, or 3%, to $45.2 billion. Customer deposits increased $1.5 billion, or 1.9%, to $80 billion.

Mortgage test rate now 9%

Figures from BNZ's parent, National Australia Bank (NAB), show the NZ subsidiary's loans at least 90 days past due plus gross impaired assets to gross loans at 0.61% at March 31, down from 0.78% at September 30 last year. They also show BNZ's home loan loss rate running at 0.00%.

Huggins told interest.co.nz BNZ's now testing mortgage applicants at 9% to check their ability to maintain payments if interest rates rise further. That's up from 8.75% when the bank reported annual results last November.

"We've been careful about how we construct the [loan] book to make sure that it is a book that is robust to these types of cycles. And we've worked with customers to make sure the balance sheets are in good shape. And so you're seeing that flow through now," Huggins says.

Nonetheless, he expects to see "some increase in [loan] arrears from here" until interest rates start reducing.

BNZ's total loan provisioning increased by about $39 million to $971 million.

'A bit of a quiet achiever for NAB'

Meanwhile, NAB posted a 13% drop in interim cash earnings to A$3.548 billion. NAB's net interest margin fell five basis points to 1.72%, and its cash return on equity was 200 basis points lower at 11.7%.

NAB's common equity tier one capital ratio slipped six basis points to 12.15%, and it's paying an interim dividend of A84 cents per share, down A1c.

NAB also announced an A$1.5 billion increase to its on-market share buy-back programme.

Andrew Irvine, NAB's CEO, described BNZ as "a bit of a quiet achiever for NAB."

NAB figures also show BNZ's branch numbers down seven year-on-year to 127.

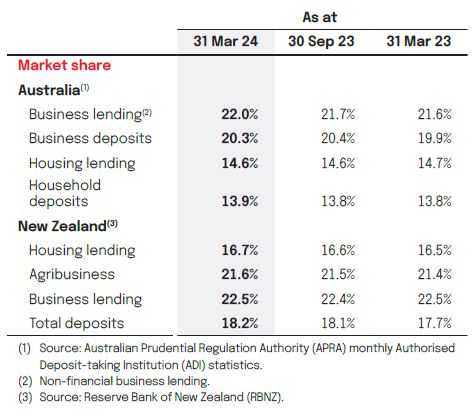

*The chart below comes from NAB.

And the results summary from BNZ's parent National Australia Bank is here.

5 Comments

That's interesting. Home lending increased 1.1 billion 1.9%, whilst business lending increased 1.3 billion 3.0%.

Wonder what is behind that interesting stat?

Borrow an umbrella today and pray for sunshine tomorrow?

Good

Like all bankers in NZ they are greedy and uncommercial.

Be the start of their international home loan book falling apart.

BNZ where big players in the launder money from 2011 to 2018 it all comes out in the wash.

I would expect there to be too many provisions and too much noise in the numbers to draw any conclusion.

It's nice to see the bank's business loan book still up there. Other banks could take notice.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.