By Simon Geldenhuys*

The Reserve Bank's (RBNZ’s) 2025 capital review signals a clear shift in how bank resilience will be delivered. Rather than relying on even higher equity buffers, the revised framework places greater emphasis on a thicker layer of Tier 2 capital designed to absorb losses at--not before--the point of failure. This redesign brings New Zealand’s framework closer to international norms and reflects a growing regulatory focus on resolvability alongside resilience.

Investors have asked us a simple question: Does lower equity mean weaker banks and lower ratings?

Our answer is equally simple: No. Our ratings are unlikely to change.

Specifically, we don’t expect any impact on our standalone credit profiles or ‘AA-’ issuer credit ratings on the four major banks we rate--ANZ Bank New Zealand, ASB Bank, Bank of New Zealand, and Westpac New Zealand. We think their capitalisation will remain strong, supported by disciplined capital management and the banks’ close ties with their Australian parent groups.

A framework reset, not a retreat

The December 2025 capital review revisits reforms introduced in 2019, when the RBNZ substantially increased equity capital requirements to strengthen system resilience in the wake of the Global Financial Crisis.

Six years on, the landscape has changed. Basel III is now well-embedded globally and New Zealand’s Deposit Takers Act 2023 has overhauled key aspects of bank regulation. There were also lingering industry concerns that New Zealand’s capital settings were excessively conservative.

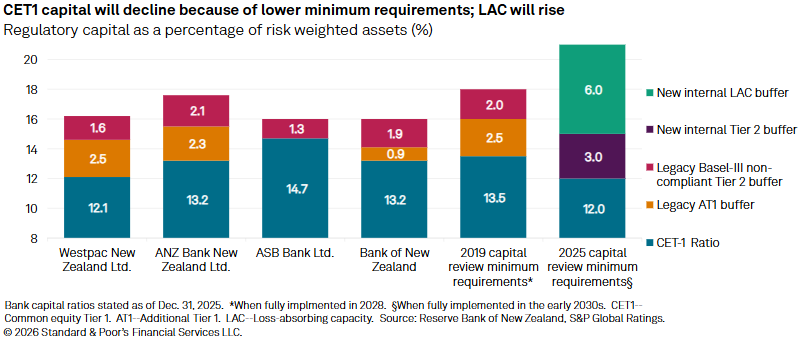

Against this backdrop, the revised framework introduces four key changes in our view: a modest reduction in minimum common equity Tier 1 (CET1) requirements; the phase out of additional Tier 1 (AT1) instruments; the introduction of a substantial layer of internal loss absorbing capacity (LAC) and Tier 2 instruments; and more granular standardised risk weights, easing the impact of the RBNZ’s high output floor.

CET1 will fall

Under the new framework, minimum CET1 requirements will fall to 12% of risk weighted assets (RWAs) by December 2028, down from the 13.5% level envisaged under the fully implemented 2019 rules. AT1 instruments, currently about 10% to 15% of Tier 1 capital for some banks, will be removed entirely.

Strong CET1 buffers remain very important. Banks are inherently confidence sensitive, and equity capital provides insurance against unexpected losses. However, holding capital well in excess of underlying risk can dilute returns and constrain lending.

In our view, the recalibration improves efficiency without undermining resilience. We assume the major banks will continue to operate with sound buffers above regulatory minimums, consistent with their history of prudent balance sheet management.

Ratings capital will also fall--but remain strong

The shift away from CET1 and AT1 will reduce capital captured in our risk adjusted capital (RAC) ratio, which measures going concern LAC.

Once fully implemented, the four majors’ RAC ratios will fall but remain firmly above 10%. This is our cutoff for a bank to be considered ‘strongly capitalized’.

While regulatory capital structures are evolving, we think underlying capitalisation will remain robust.

A clearer, simpler capital stack

One of the most significant changes is the removal of AT1 instruments. We think this simplifies the capital stack and aligns more clearly with the RBNZ’s preferred single point of entry resolution strategy. This reflects the inherent complexity of AT1 instruments and the fact that, in New Zealand’s small, highly concentrated banking system, it’s not totally clear to us how AT1s would behave in a crisis scenario.

In their place, the RBNZ will require a much thicker layer of internal Tier 2 and LAC instruments, lifting total LAC to a minimum of 21% of RWAs, once fully implemented. These instruments will include nonviability conversion clauses and will be issued internally to Australian parents, ensuring 100% of LAC is group sourced.

While these instruments are not a substitute for equity, they materially enhance resolvability and reduce the likelihood of losses being imposed on senior creditors or depositors.

Australian parents: more skin in the game

The revised settings further strengthen alignment between New Zealand subsidiaries and their Australian parents. New Zealand operations are integral to group strategies, typically contributing 10% to 30% of earnings and common equity.

The introduction of fully internalised LAC reinforces expectations of strong parental support in any foreseeable circumstances.

Looking ahead

Some uncertainty remains. The RBNZ is expected to provide further clarity in mid-2026 on transition timelines, legacy instruments, and resolution strategies. Over time, this could pave the way for a statutory bail-in regime.

For now, the direction is clear: New Zealand’s capital framework is becoming more efficient, more resolvable, and more aligned with global standards--without weakening bank resilience.

*Simon Geldenhuys is a Melbourne-based banking analyst at S&P Global Ratings.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.