The Reserve Bank (RBNZ) says new bank regulatory capital requirements will reduce the highest quality and most expensive capital New Zealand's big four banks must hold by $3.4 billion, reducing their funding costs and boosting their lending capacity resulting in lower interest rates for borrowers.

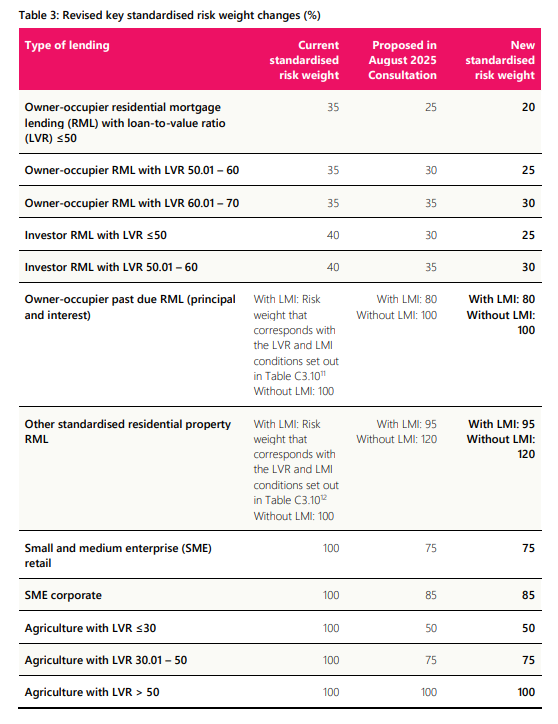

At the same time the RBNZ says "based on strong evidence provided by stakeholders," it'll align standardised risk weights for housing lending with loan-to-value ratios (LVRs) below 70% with Australia's set by the Australian Prudential Regulation Authority (APRA). Risk weights for loans with higher LVRs will remain unchanged.

Bank capital is funding that's first in line to absorb any losses banks may incur. Risk weights are used to work out the minimum amount of regulatory capital a bank must hold. The capital requirement is based on a risk assessment for each type of bank asset or loan. (The RBNZ's decisions paper is here).

RBNZ Chairman Rodger Finlay says completion of the review commissioned in March means "modernised capital rules" supporting an efficient and resilient financial system. The new capital requirements will take effect between 2026 and 2029.

"We recalibrated our risk appetite to have regard to our new Financial Policy Remit, and to reflect important developments since 2019, including the introduction of the Depositor Compensation Scheme, and more intensive supervision, enforcement, and resolution approaches. This led us to ease common equity requirements across the system by around $5 billion compared to current levels, while still remaining confident in our system resilience," says Finlay.

Changes also include more granular risk weights, simplification of capital instruments, and greater alignment of instruments for the big four banks with Australian settings.

"Our approach is simple, strong, proportionate, and efficient. These new settings will reduce the overall cost of deposit takers’ funding, which we expect to see passed on as benefits to New Zealanders through increased lending and reduced rates, which we will monitor closely," new Reserve Bank Governor Anna Breman says.

“Small and mid-sized deposit takers should see a proportionately larger reduction than the four large banks, which should allow them to grow and compete more effectively.”

"We will be monitoring closely the impact of our new settings, including on lending rates, and we will be publishing our findings every two years," Breman says, adding this will help the RBNZ assess how the changes affect market dynamics, including from a competition perspective.

The RBNZ says the changes will reduce banks' average funding costs by six basis points compared to current capital levels, and by 12 basis points compared to the 2028 settings under 2019 review decisions. It's expecting an eight basis points decrease in lending interest rates.

The RBNZ decided to review capital requirements after government MPs urged the prudential regulator to stop further increases, suggesting they were raising borrowing costs and suppressing competition. In August the RBNZ proposed changes citing a higher risk appetite to explain lower settings than were set at the end of its last capital review in 2019, which was seeing increases phased in through to 2028.

Breman says despite the political pressure, the decision to review banks' regulatory capital settings was made by the RBNZ board.

$3.4b reduction

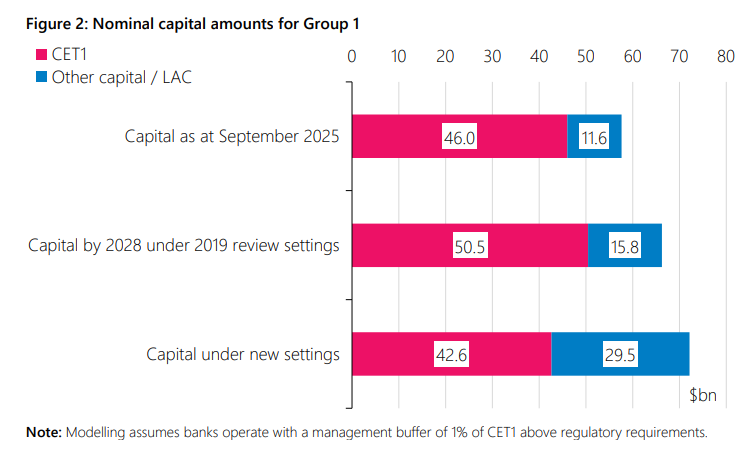

The changes will see ANZ NZ, ASB, BNZ and Westpac NZ's common equity tier one (CET1) capital reduced by about $3.4 billion, or 7%, from the $46 billion it was at in September this year. CET1 "going concern" capital consists of the likes of ordinary shares, retained earnings and reserves.

CET1 capital requirements will also be reduced for smaller banks and non-bank deposit takers. For banks/deposit takers with total assets of $2 billion or more, but less than $100 billion (group 2) such as Kiwibank, Rabobank and TSB, it'll be reduced by up to $1.9 billion, for deposit takers with total assets of less than $2 billion, (group 3) such as building societies, credit unions and deposit taking finance companies, by up to $70 million.

"CET1 capital is the highest quality and most expensive form of capital, and therefore these changes will reduce the weighted average cost of deposit takers’ funding. Lower CET 1 levels increase the risk of financial crises occurring, but the LAC [loss absorbing capacity] requirements improve the ability to mitigate the cost of these crises if, and when, they occur," the RBNZ says.

"This will deliver substantial capital reductions compared to the 2028 settings under 2019 review decisions, in line with our assessment that risk weights should be reduced to reflect actual risk as established by available data."

LAC can be a cushion of equity and debt instruments that allows a bank to absorb unexpected losses without failing or needing a bailout.

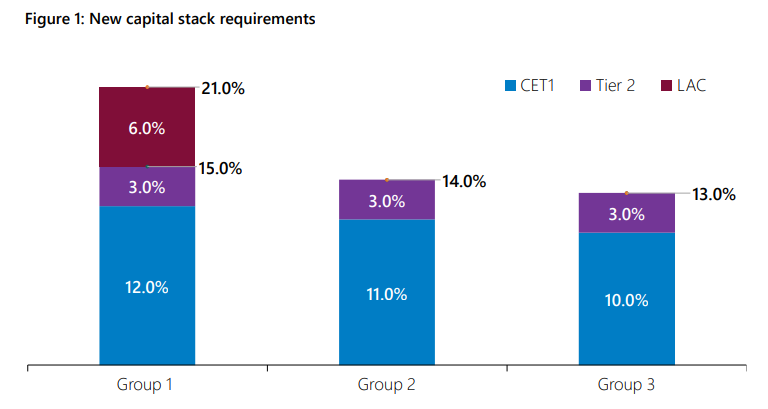

"We estimate group 2’s total capital will be up to 21% lower than the current levels, taking into account expected management buffers above the regulatory minimum. For group 3, the expected reduction in capital is up to 20%. We analysed options that considered further lowering of the capital ratio requirements for group 2 and 3 deposit takers, but consider that further reductions would undermine financial stability. Group 2 and 3 deposit takers only have a small buffer for recovery when distressed and additional reductions in capital ratio requirements for these groups would further increase failure risk for deposit takers."

Funding costs down 12 basis points, more debt access

Despite the reduction in CET1 requirements, the introduction of LAC will increase regulatory capital required by the big four banks by 25% to $72.2 billion from $57.6 billion, the RBNZ says. LAC debt instruments could see the outstanding balance written down or converted into equity if a bank is in distress. The big four banks will be required to issue their LAC instruments to their Australian parent banks. This is cheaper funding than CET1.

"Overall, total CET1 in New Zealand’s deposit takers is expected to reduce by 10% or approximately $5 billion from current levels, while total regulatory capital is expected to increase by 18%. We expect that replacing higher cost CET1 with LAC will reduce deposit taker’s average funding costs by around 0.06%, 6 basis points, compared to current capital levels, and by 0.12%, basis points, compared to the 2028 settings under 2019 review decisions," the RBNZ says.

"This is expected to support improved access to credit."

Antonia Watson, CEO of ANZ NZ, says the RBNZ changes will result in less upward pressure on interest rates. She says the old capital settings would've "resulted in an extra cost on providing loans" of more than 40 basis points, on average.

"The RBNZ says its new capital settings will mean this extra cost on providing lending will be seven to 19 basis points less. We estimated in our recent submission that it would only be six basis points less. Regardless, that’s still an uplift and it comes at a cost to banks and, therefore, consumers," Watson says.

The RBNZ says more detailed information and supporting analysis to the decision will be published in February, with consultation on the detailed design of tier two "gone concern" capital, which mainly consists of long-dated subordinated debt, and LAC requirements for the big four banks in June 2026.

Additional tier one (AT1) capital instruments, such as preferred shares that are continuous given there's no fixed maturity date, are to be phased out.

An RBNZ capital review finalised in 2019 resulted in retail banks being required to lift their total regulatory capital from about 10.5% of risk weighted assets to 18% for the big banks and 16% for others by 2028. The implementation of the 2019 capital requirements were delayed by the Covid-19 pandemic.

The RBNZ's 2019 review made the explicit assumption that New Zealanders aren't prepared to tolerate a system-wide banking crisis, and its adverse economic and social impacts, more than once every 200 years. This is now gone. Breman notes the RBNZ is not running a zero failure regime.

"We've now moved away from this ‘one-in-X-many years’ framing, and our board has decided to focus on options with a higher risk appetite. This means options that reduce the cost of regulation compared to the 2019 decisions," the RBNZ says.

Willis cheers

Finance Minister Nicola Willis welcomed the RBNZ changes.

"Higher costs for banks translate to higher lending costs for New Zealanders and, potentially, less lending to the agricultural and other important sectors."

"Therefore, when I issued the new Financial Policy Remit to the Reserve Bank last year I outlined the Government’s expectation that it should ensure that prudential regulation of the banking sector did not impede competition," Willis says.

"The new requirements announced today remain prudent and strike a better, more graduated balance between risk and competition. In particular, the adjustments to risk weights are expected to enable smaller deposit takers to compete more effectively against the big four banks. They also open the door to more lending to the agriculture sector," says Willis.

The RBNZ says it'll align the risk weight settings for community housing providers with owner-occupied residential mortgage lending using the same LVR categories, in a shift from alignment with property investment mortgage lending.

"We have also added a maximum risk weight of 30%, regardless of LVR, for community housing providers with long-term funding contracts with government agencies. This reflects the secure income that these providers have."

There'll be more granularity for small business (SME) lending, with the RBNZ to review risk weight thresholds for this lending in 2026. These are currently 100%, but could be reduced to 75% for retail SME lending and 85% for corporate SME lending. For agriculture lending the RBNZ says it'll create three new LVR-based categories to ensure more accurate and risk-sensitive weightings. This could reduce risk weights on some lending from 100% to 75% or 50%, based on LVRs.

Breman says the changes mean banks and non-bank deposit takers from the RBNZ's groups 2 and 3, which are capital constrained today, will have more ability to lend to small and medium sized businesses.

The RBNZ will also review capital requirements for reverse mortgages, commercial property, infrastructure and securitisations next year.

What is capital?

Kicking off the Reserve Bank's biggest ever review of bank capital requirements in March 2017, which culminated in the 2019 decisions, the then RBNZ Deputy Governor and Head of Financial Stability Grant Spencer described bank capital as an important cushion for the financial system.

"It is the form of funding that stands first in line to absorb any losses that banks may incur. Having sufficient capital promotes financial stability by reducing the likelihood of bank insolvency and moderating the effect of credit cycles," Spencer said.

Bank capital includes ordinary shares, retained earnings, capital instruments issued by a bank that are continuous given there's no fixed maturity date such as preferred shares, and long-dated subordinated debt, such as bonds, issued by a bank.

The RBNZ has also decided to reduce the minimum amount of capital for deposit takers from the $30 million currently required for a registered bank to $5 million from 2028.

Victoria University's Martien Lubberink argued an Oliver Wyman report commissioned by the RBNZ this year to support its proposed changes used "two iffy methodological choices that systematically bias the comparison in favour of finding New Zealand banks overcapitalised," which these being "a peculiar selection of comparator countries and a size-adjustment technique that obscures the fundamental relationship between bank size and capital ratios."

There's a an RBNZ frequently asked questions document here.

Figures 1 and 2 and table 3 below come from the RBNZ.

Note, group 1 covers ANZ NZ, ASB, BNZ and Westpac NZ, the big four "systemically important" banks that between them hold the lion's share of loans and deposits.

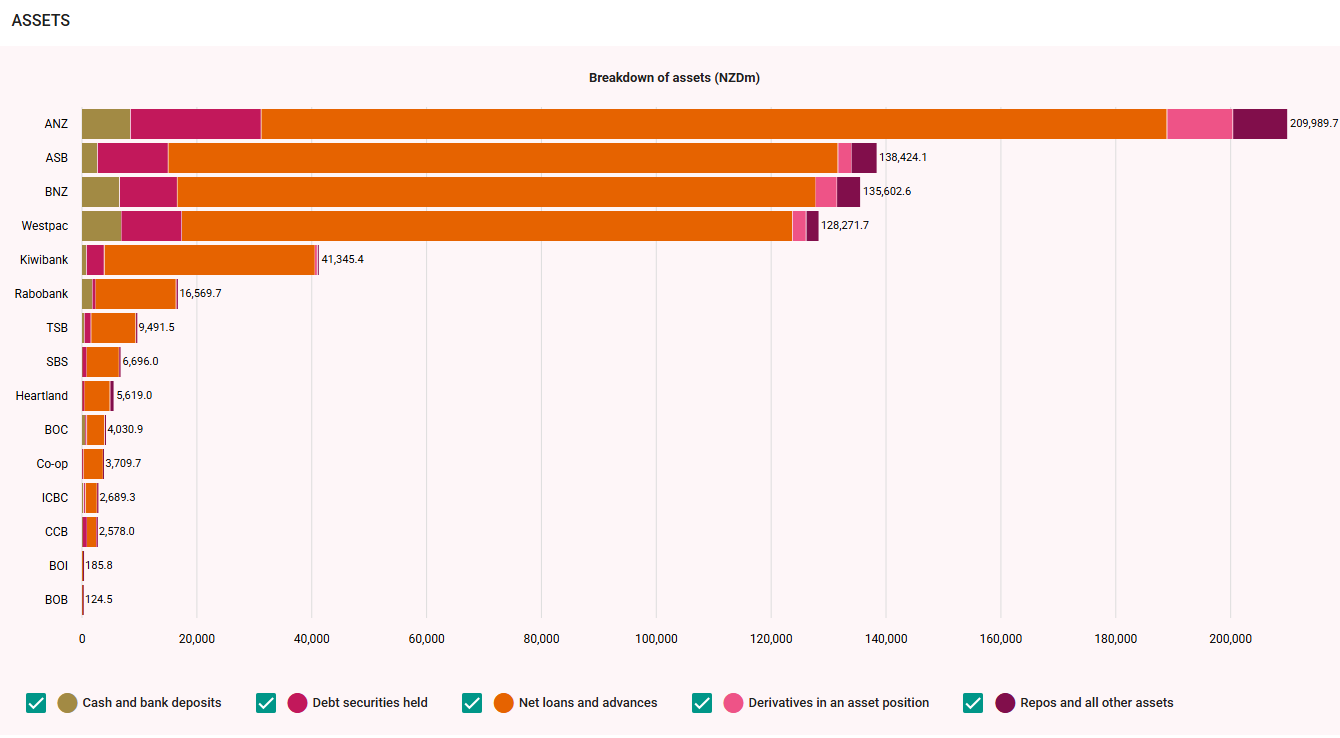

The chart below comes from the RBNZ's Bank Financial Strength Dashboard.

23 Comments

Our private debt levels relative to GDP are the problem (way above 100%) - creating more of the problem (private debt) is not the solution.

Unless you are the current government. And the previous, infact the last 40 years.

Well pretty much post GFC our private debt vs GDP has been high - only sustainable by always dropping interest rates so that we never had to face the reality of the situation (too much private debt relative to our productivity) while people say the economy was ‘booming’ or a ‘rockstar’.

In reality we were extending too much debt against the housing market - and the article above implies that if we can just extend even more (debt) then we will have growth again - not realising we currently don’t have growth because we’re drowning in the previously created debt that was supposed to stimulate growth now. It’s insane thinking. Actually highly unintelligent. Thinking more of the problem is the solution.

And leads to this little gem in the Balance of payments article.

"Foreign investors earned over two and a half times higher dividends this quarter compared with the last quarter. The increase in dividends paid this quarter was due to several banks paying their parent companies."

Yep, agree that NZ private debt is pretty high but this latest move aint about creating more of it.

Its about removing a headwind that was tightening credit more than intended, esp at a time when households are already deleveraging. Structural fixes remain with the govt, not rbnz.

First para:

‘reducing their funding costs and boosting their lending capacity’

ie this is all about creating more private debt.

Yeh but capacity aint he same as demand. Banks can be able to lend more without people actually borrowing more. If households are paying debt down and incomes still limit what people can borrow then lending doesnt magically rise. This just removes an extra squeeze on top of the ocr, it doesnt fix weak demand or weak incomes.

My experience is that if people are able to take on more debt because interest rates are lower, they will - regardless of how rational it is.

Did you not see what happened in 2020-2021?

I see where you are coming from as a FHB. Anything that will further lower the cost of debt on what is probably a large mortgage - I get it. But I’m more thinking system wide risk and implications and not from the perspective of a single entity (ie your personal circumstances).

Yeh fair, Im not sayin theres no risk and Im definitely not calling for another 2021. Just that right now peoples incomes and budgets are doing most of the slowing. Cheaper funding might mean people pay debt down a bit slower, but thats pretty different from everyone piling into new debt again. Across the system as you say, the bigger issue at the moment I think is weak growth, not runaway borrowing. Btw Welly-FHB is an old handle (2010) and not a first home buyer now

We are seeing a slow economy as private debt is too high and people aren't willing to take on more. Having an economy like this clearly isn't sustainable long term and will eventually take a large hit from external price shocks such as oil shocks or a market crash (possible for the AI bubble currently). We need to build greater resilience in NZ vs going back to the ways of boom and bust property cycles and expecting to be better off by passing on more and more debt each sale to the next greater fool.

Yup, dont really disagree with that. High private debt is def part of why growth is weak and why shocks can be so ouchy. My point isnt that we should go back to boom/bust housing or keep levering people up, its that right now the slowdown is coming from stretched households, and not a lack of credit supply.

Long term I totally agree NZ needs more resileince, productivity and less reliance on property cycles, but thats more about policy, incentives and investment choices than bank funding changes\tweaks. And yeh, there’ll probably always be a “greater fool” as you put it as they've been around as long as housing has. Maybe they pause for a bit, but theyre not disappearing anytime soon... right need another coffee 👌

Where is the tightened credit? Banks have been offering good incentives for new customers, not turning them away.

Tightening doesnt mean banks stop lending altogether. It just shows up in things like higher margins, tougher service tests and shorter fixed terms. I assume you mean cashback offers? then thats just banks competing for the few borrowers who still tick all the boxes.

Excellent start from the new rbnz gov.

Would have preferred a NZer of course!

🥂

So the "laser focus on inflation" is already out the window. That didn't take long.

"Watch what they do, not what they say..."

Gotta pump that housing inflation somehow… it’s the productive economy don’t ya know ..sarc

I am absolutely sure banks will pass savings onto customers and not just increase profit for shareholders. Absolutely sure of it.

If they want lower interest rates, just decrease the OCR and keeps the banks solid.

It doesn't work like that!! If the wholesale markets think the OCR is lowered when it doesn't need to be, the swaps will start reflecting higher future inflation (due to too much money chasing the same quantity of goods and services in the economy) and then mortgage rates go up, which then limits the banks ability to issue more debt (this is why the banks started freaking out this last week and whinging to the RBNZ to talk the wholesale markets back down again because higher rates would impact their ability to create more debt -ie the herion they sell to NZ debt junkies).

You can't just lower the OCR because you want banks to create more private debt.

You lower the OCR because the financial system risks falling into deflation.

Sub-4% interest rates here we come 👍

Luxon and Willis will be loving this. More cheap credit to lever everyone up with; add the surge in immigration about to begin.

A perfect recipe for another property boom just before next year's election.

If thats the hope then the immigration floodgates will need to be opened now (or yesterday) as I doubt there is sufficient appetite for more debt in the current environment given the glut of (unaffordable) housing, dairy price declines and business opportunity.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.