By Gareth Vaughan

The Reserve Bank has watered down the final decisions in its broadest ever review of banks' regulatory capital requirements a little and given banks seven years, instead of the previously proposed five years, to adopt them.

The upshot is that instead of needing $20 billion of new capital sourced solely from equity, banks now need to find $11 billion of equity and can stump up the remaining $9 billion through issuing preference shares.

The Reserve Bank has confirmed that the big four Australian-owned banks - ANZ, ASB, BNZ and Westpac - will be designated as systemically important banks requiring them to hold more capital than their smaller rivals. Despite the increased capital requirements banks will remain highly leveraged. The Reserve Bank says it's increasing the amount owners contribute from $8 of every $100 of lending to $12 as it moves to reduce the probability of a banking crisis in New Zealand to a one-in-200-year event from about one-in-100 years now.

"Capital requirements are the most important component of the Reserve Bank’s regulatory framework for banks. We have decided to raise the bar for New Zealand’s banks in this area, not only to strengthen the banks themselves, but to better protect all New Zealanders from the damaging consequences of banking crises that will inevitably be on the horizon,"the Reserve Bank says.

It says the new capital requirements could lead to about a 20 basis points increase in the average lending rates banks charge, once changes are fully implemented.

"Äs an example, $5 would be the fortnightly increase in a $100,000 mortgage over 30 years at the current 3.45% two-year rate, based on a 20 basis point increase," the Reserve Bank says. "Banks make profits from lending. The competitive market will continue and if one bank pulls back in a particular segment of lending, we expect another will step up."

"With seven years to transition to the new requirements, banks will be able to maintain their lending growth, reach higher capital ratios, and continue to pay dividends." (See more here on the impact the Reserve Bank expects from its new capital requirements).

The nuts and bolts

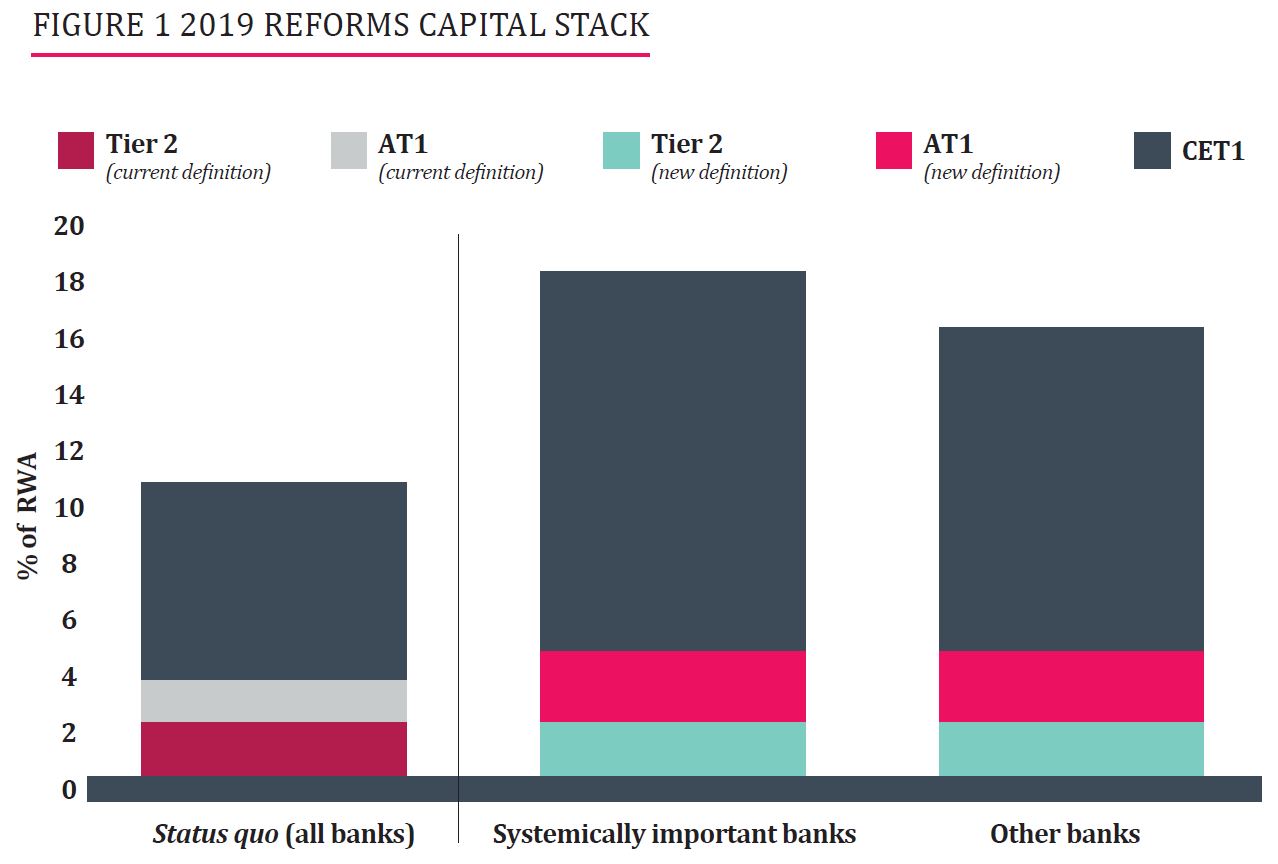

The four big banks will require total capital equivalent to 18% of risk weighted assets (RWA). RWA are used to determine the minimum amount of capital that must be held by banks to reduce the risk of insolvency.

Other banks will be required to have total capital equivalent to 16% of RWA, meaning the previously proposed 1% systemically important bank capital buffer will now be 2%.

For the big four the Reserve Bank says long-term subordinated debt, or Tier 2 capital, can contribute up to 2% of their requirement, Tier 1 capital will need to be 16%. Of Tier 1 capital, redeemable preference shares, or Additional Tier 1 capital (AT1), can contribute up to 2.5% meaning 13.5% must be met by Common Equity Tier 1 capital or CET1.

The Reserve Bank says it will accept redeemable perpetual preference shares, with suitable protections ensuring they don't get redeemed if the bank is under stress in their contract terms, as AT1 capital. And it will accept long-term subordinated debt as Tier 2 capital.

Banks other than the big four will require total capital equal to 16% of RWA. Again Tier 2 capital can contribute up to 2%, Tier 1 capital will need to be 14% with redeemable preference shares contributing up to 2.5%, leaving 11.5% of RWA to be met with CET1 capital. Currently all banks are required to have minimum capital equivalent to 10.5% of RWA with 2% of this Tier 2 capital, up to 1.5% AT1 and a minimum of 7% CET1 including a 2.5% buffer.

The average level of capital currently held by banks is 14.1%. The Reserve Bank has confirmed that contingent debt, or CoCos, will have no place in its new regulatory capital requirements. This is debt that writes-off or converts to ordinary shares when a pre-specified event, relating to the issuing bank's financial condition, occurs. Additionally there's no requirement for a leverage ratio.

"The 2019 reforms include adjustments to the 2018 proposal in five main areas: the instrument accepted as AT1 capital, the contribution AT1 capital can make to Tier 1 capital, the capital required of non-systemic banks, the leverage ratio, and the transition period.

The 2019 reforms also confirm a continued role for Tier 2 in the capital framework,"the Reserve Bank says.

"These adjustments maintain the financial system resilience provided by the 2018 proposal, while reducing the estimated average interest rate impact of higher capital.

As a consequence, the estimated annual net benefit of reform is higher than it would otherwise be. As a result of the adjustments, banks will also have more time to comply with the new requirements, lessening the near term transitional impacts."

As previously proposed, the big four banks will still be able to set their own models for measuring credit risk exposure which they must get approved by the Reserve Bank using the so-called Internal Ratings Based, or IRB, approach.

However their RWA outcomes will have to be equivalent to approximately 90% of the standardised approach used by other banks which are set by the Reserve Bank, up from about 76% now. The big four banks will also have to report their regulatory capital requirements using the standardised approach to make comparisons easier.

'We've listened'

The next step in the process will be consultation on an ‘exposure draft’ of the detailed regulatory requirements during the first half of 2020. The new capital regime will then take effect from 1 July 2020 and banks will be given up to seven years to comply.

The Reserve Bank also explains why the big four - ANZ, ASB, BNZ and Westpac - are deemed to be systemically important requiring them to hold more capital than smaller banks.

"Systemically-important banks are banks that are large relative to the economy as a whole and on a variety of other metrics, and whose failure would have significant adverse consequences beyond their immediate customers and other counterparties, affecting the economy as a whole. For example, their failure may cause the failure of otherwise sound banks and businesses," the Reserve Bank says.

"We've listened to feedback and reviewed all the data, and are confident the decisions are the right ones for New Zealand," Reserve Bank Deputy Governor and General Manager of Financial Stability Geoff Bascand says.

'Á modest 'win' for the banks'

In a note on the Reserve Bank's capital decisions, Australian-based UBS banking analysts note the key elements from last year's proposals remain intact, including increasing New Zealand bank capital ratios materially, towards the strongest in the world.

"However, there is some moderation to what we considered more excessive proposals. This provides a modest 'win' for the banks in a very challenging environment," UBS says.

"While the RBNZ retained its 16% Tier 1 requirement, we believe there are three main changes: (1) The transition period was extended from five to seven years. The first phase (increase RWA scalar) will begin in July 2020, rather than January 2020; (2) Increase in the proportion of Additional Tier 1 (AT1) that may contribute to Total Tier 1 capital to 2.5% of RWA, from 1.5% in the 2018 proposal; (3) Further, the definition of AT1 has been widened to include Redeemable, Perpetual Preference-Shares (RPPS), rather than just Non-Redeemable Preference Shares in the 2018 proposal."

"Importantly, this increases the attractiveness of ATI as marketable securities, with the RBNZ stating that the original AT1 proposals 'would not appeal to either equity or debt investors and… would not be issued by banks'. In effect, this implies that the amount of CET1 the banks will need to hold falls to >13.5% compared to >16% in the 2018 proposal," UBS says.

"Calculating the exact capital shortfall for both the New Zealand business and the Australian (Level 1) operations is complex, and some inputs are not publicly available. We expect each of the major banks to make announcements today regarding their initial estimates of their capital shortfalls and the potential for issuing AT1 securities. However, we expect the NZ CET1 requirements to be substantially lower than their original estimates (ANZ NZ$6-8bn; CBA NZ$3bn; NAB NZ$4-5bn; WBC NZ$3.5-4.0bn)."

34 Comments

A pioneering move. Once again NZ punches above its weight and shows the world how it is done. Well done, Mr Orr. Merry Christmas to you all at RBNZ.

Pioneering it is not, when other economies already have equivalent and better requirements.

Its a start. Just a shame this wasnt introduced ten years ago. NZ wouldn't be $250 billion poorer, which Jon Key facilitated during his tenure. Has anyone asked him what commission rate he was on?

I think the agreed upon commission was him double-dipping into ANZ's global honorarium fund as chairman at ANZ NZ while also serving as a director on its Aussie parent's board.

The dude hasn't been PM for three years. Do you seriously think he stole more than entire year worth of the country's GDP? Let it go or get help.

Pioneering it is not, when other economies already have equivalent and better requirements

Any particular examples you want to highlight?

Reproducing my question to Gareth on a previous article and his reply :

Quote :

by SmoKey | 3rd Dec 19, 7:31am

How do these proposals compare with the provisions for large banks in other western countries ?

Is RBNZ trying to catch up with others or is it trying to be a pioneer in introducing better measures to meet future adversities ?

EDIT REPLY REPORT COMMENT

by Gareth Vaughan | 3rd Dec 19, 9:23am

The RBNZ is proposing both higher capital requirements than are in place in comparable countries, and higher quality capital too.

Unquote :

Pioineering much, alright.

There was some noise about $30k in your bank account being guaranteed. Who was driving that and is it current?

It's not worth worrying about.

If you ever need to claim on your $30k, it will buy you about what $1k will today. ie: For that to happen our banking system will have collapsed, and so will the purchasing power of our currency. Any small bank that 'goes down' will be married to a larger one to protect savings; any large one will be rescued by its parent in Australia; Holland etc - as the reputation damage of not doing so would be too big and so affect the parent.

Bloody hell, everytime I start to get my head wrapped arround this it's bigger and more intertwined than I imagined.

Cheers for the explanation bw.

So if you're worried about this sort of thing it's better to have some PM's to cover your behind for a bit incase the big ones drop as well.

"any large one will be rescued by its parent in Australia"

There are recently introduced reduced exposure limits that have been imposed on the Australian banks by their regulator APRA. Depending upon the amount of capital required by their NZ subsidiaries, there is a constraint imposed on the parent bank to recapitalise a NZ bank subsidiary.

The announcement follows the confirmation of plans by the Australian Prudential Regulation Authority (APRA) to lower the level of exposure that the country’s banks can have to offshore units to 25% of core capital from 50%, ANZ said on Tuesday.

https://www.reuters.com/article/anz-bank-regulator-new-zealand/update-3…

This is a far more pragmatic outcome than the original proposal, the banks will be very, very happy. Seven years to get CET1 to 13.5% is not at all onerous.

Business as usual, let the good times roll.

Well Done.

Even at 18% of the risk weighted assets I do not feel comfortable. As we saw in the GFC these risk weighting processes can go horribly wrong. They assume that only a small % of debts will go bad. As we saw in the GFC, when things really hit the fan, a few debts going bad can collapse a large part of the economy and risk a large % of debts going bad and the whole house of cards collapses. As I have noted some years ago, that even after what should have been the salutatory experience to the GFC and resultant Basel 3 provisions, it was not long before banks were again fudging their risk weighting formulas. It seems that our RB found that this was also happening here.

These Banks cannot be trusted for 5 minutes and Mr Orr will have to keep on their back continuously.

I still think that there are some very major flaws in the structure of our economic management model and the banks place within it. Major deep long term thinking and change is still required. This is just a patch.

You're right.

Reading the fine print of your mortgage documentation will tell the bank can call in your mortgage anytime they like; regardless of your equity position. Forcing you to refinance under a new set of rules, which could mean you may be forced to sell; likely in a market where there are few purchasers.

We may have to wait another 7 years for the next installment of banking regulations; if banks still exist then.

"Reading the fine print of your mortgage documentation will tell the bank can call in your mortgage anytime they like; regardless of your equity position."

True, but politically, mass foreclosures would be pretty unpalatable I would think.

It would - and should - be the trigger for nationalisation.

"It would - and should - be the trigger for nationalisation."

It depends on who the major shareholders of the bank are.

1) publicly listed bank

2) majority owned subsidiary which is unlisted (situation in NZ banks)

An example of a publicly listed bank that experienced funding difficulties was Northern Rock in the UK, which was nationalised by the UK government. Also look at the US publicly listed banks that issued new equity (either a rights issue to existing shareholders, or issue new preference shares or new equity to new shareholders). Some examples in the US were Citigroup and the issue of the convertible preference shares. Also in Iceland, the Icelandic shareholders were unable to recapitalise the publicly listed Icelandic banks and were nationalised by the Icelandic government. Depending upon circumstances, sometimes nationalisation can be a solution. BNZ in the 1990's required capital injections by the shareholders (of which the NZ government was a major shareholder at the time). Also note publicly listed ANZ Group (parent of NZ bank) undertook a rights issue in 2015, and Westpac in Australia has recently undertaken rights issue

In NZ, the big 4 banks are owned by Australian parent banks. If their NZ subsidiary bank need additional capital urgently, then the first call is likely to be from the existing shareholders. If the amount of capital required exceeds the constraints by APRA regulations, then alternative solutions may be required. E.g preference shares? additional equity from other sources?

Hopefully, the likes of KiwiSaver funds, ACC Investments and NZSF manage to snap up a decent chunk of the $9 billion in preference shares, so we could keep some of those tidy bank profits circulating within our economy.

Wishful thinking.

Most will go to related parties, through the internationally franchised local merchant banksters. Why would they not look after their biggest customers first.

Goldman Sucks and Morgan Stealy are licking their lips..

Is this likely to hurt banks share price,and if it does will it have a flow on effect to investment companies on the NZX eg AFI,MLN etc.

If an Australasian had spare cash to invest, with say ANZ, would they now plonk it down in Australia or New Zealand? That's where the new funds might come from to keep our interest rates falling....

NSD/AUD cross continuing to do well....!

In an environment where there is concern over the banking system, those with a large cash balances may choose to put in Australia over NZ due to the size differentials in the deposit guarantees.

Also wholesale funding may pull out of NZ banks and put into a Australian bank for those same reasons.

Okay , so a 7 YEAR lead-in period should be manageable .............. unless of course the wheels come off before then ?

Will depend on the year by year step up stipulated. Any word on that ?

Relax, they said a 1/200 year event! Don't worry about about the current system fragility, or how overdue we are for a crisis. There's 96.6% chance we'll make it 7 years, apparently.

The NZ herald quoted an additional $5 for each $100k of mortgage lending. Are we in for some mortgage rate hikes? Or was this already priced in?

an extra $5? of what?

"The Reserve Bank estimates the changes could increase borrowing rates by around 20 basis points (the difference between a 4 per cent interest rate and 4.2 per cent interest rate).

According to Reserve Bank documents, this could add around $5 a fortnight to the repayment costs of a $100,000 loan.

However, the bank's estimated of the impact on customers on its earlier proposals was questioned.

It suggested the impact of its December proposals could be 20-40 basis points, but some market analysts said the impact could be double that."

https://www.nzherald.co.nz/personal-finance/news/article.cfm?c_id=12&ob…

"We have decided to raise the bar for New Zealand’s banks in this area, not only to strengthen the banks themselves, but to better protect all New Zealanders from the damaging consequences of banking crises that will inevitably be on the horizon"

Ominous statement… so does the RBNZ expect this banking crisis NOT to happen for the next 7 years?

Ominous indeed. And to answer your question - No one knows, not even the RBNZ. That's why banking crises etc happen.(NB: Note the use of the plural of the noun, crisis. There could be several in those 7 years) ....( I know. You know all that already. We all do!)

Bank failures happen, when and where depends. But mass bank failures or potential failures as happened during GFC 2008 woke up the Central Bankers to the greed and bad practices that Banks follow and since then they have been struggling to make sure it doesn't happen again or to reduce to the barest minimum the chances of it happening again. There is no unanimity in this. Each country for its own. Now the focus is on Australasian Banks and their bad behaviour is being exposed, there is more urgency here. RBNZ should be congratulated for catching the bull by its horns and trying to tame it.

Hugh Hendry has the answer at the end of the video

https://www.youtube.com/watch?time_continue=501&v=3oZtPK6hqLU&feature=e…

The challenge is to implement the regulations when the risk is rising as a prevention to a banking crisis. If implemented, & enforced, and a banking crisis is averted, then the general public is generally unaware. Look at the government actions in 2009 during the GFC to ensure NZ banks were able to continue accessing international capital markets for funding, and guarantee of bank deposits in NZ - many property investors are unaware that this action by the government to ensure the safety of the banking system led to an entirely different economic outcome for the country than if the government had let the banks be subject to free market forces like Northern Rock in the UK, where the Bank of England wanted to avoid moral hazard.

Politicians are unwilling to act to implement regulations as a preventative measure, as it constrains growth in the economy and a booming economy increases their probability of getting re-elected into office. Politicians typically act after the crisis has occurred as a repair measure, and the general public are able to see the results of their efforts.

Well done Mr Orr, I think we have a good governor in charge

Not a word from banks yet

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.