The Reserve Bank (RBNZ) expects new requirements for banks to hold a “material” amount of additional capital will have a net impact of increasing economic growth in the long-term.

On average, it sees the changes increasing interest rates for borrowers by 20.5 basis points.

RBNZ Governor Adrian Orr says this could easily get "lost in the wash" when combined with all the other economic factors that affect interest rates.

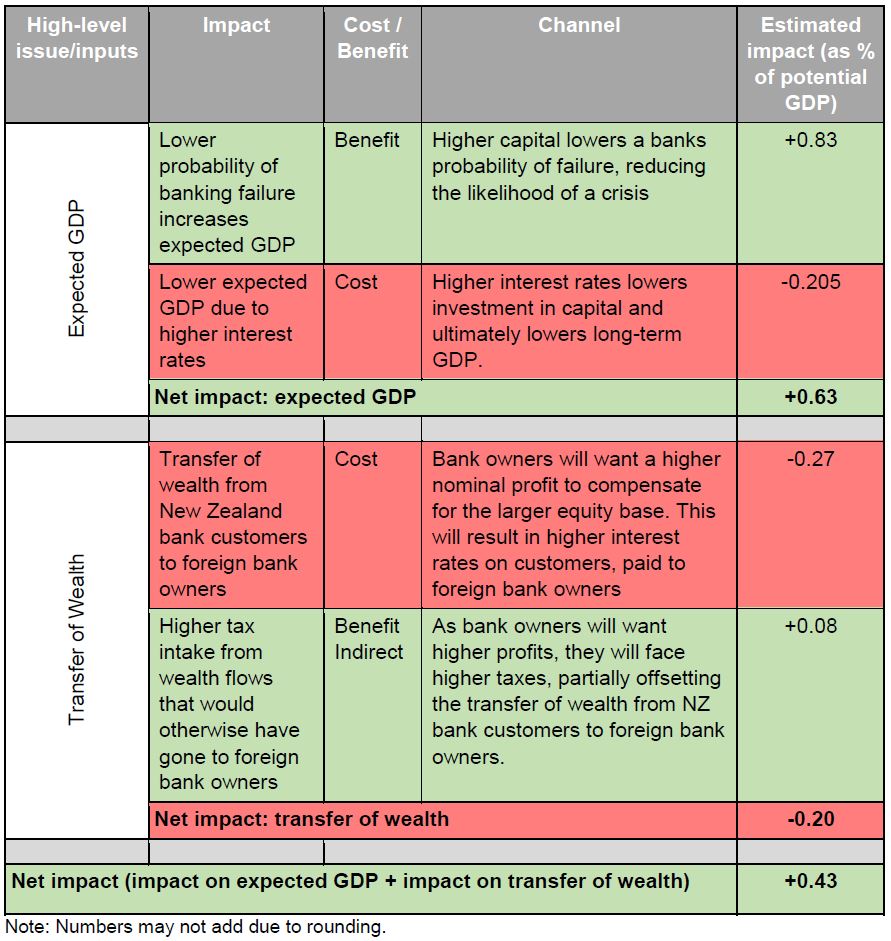

Weighing up the costs and benefits of the changes, the RBNZ expects gross domestic product (GDP) to increase by 43 basis points or 0.43% on average over the long-term.

Impact during transition

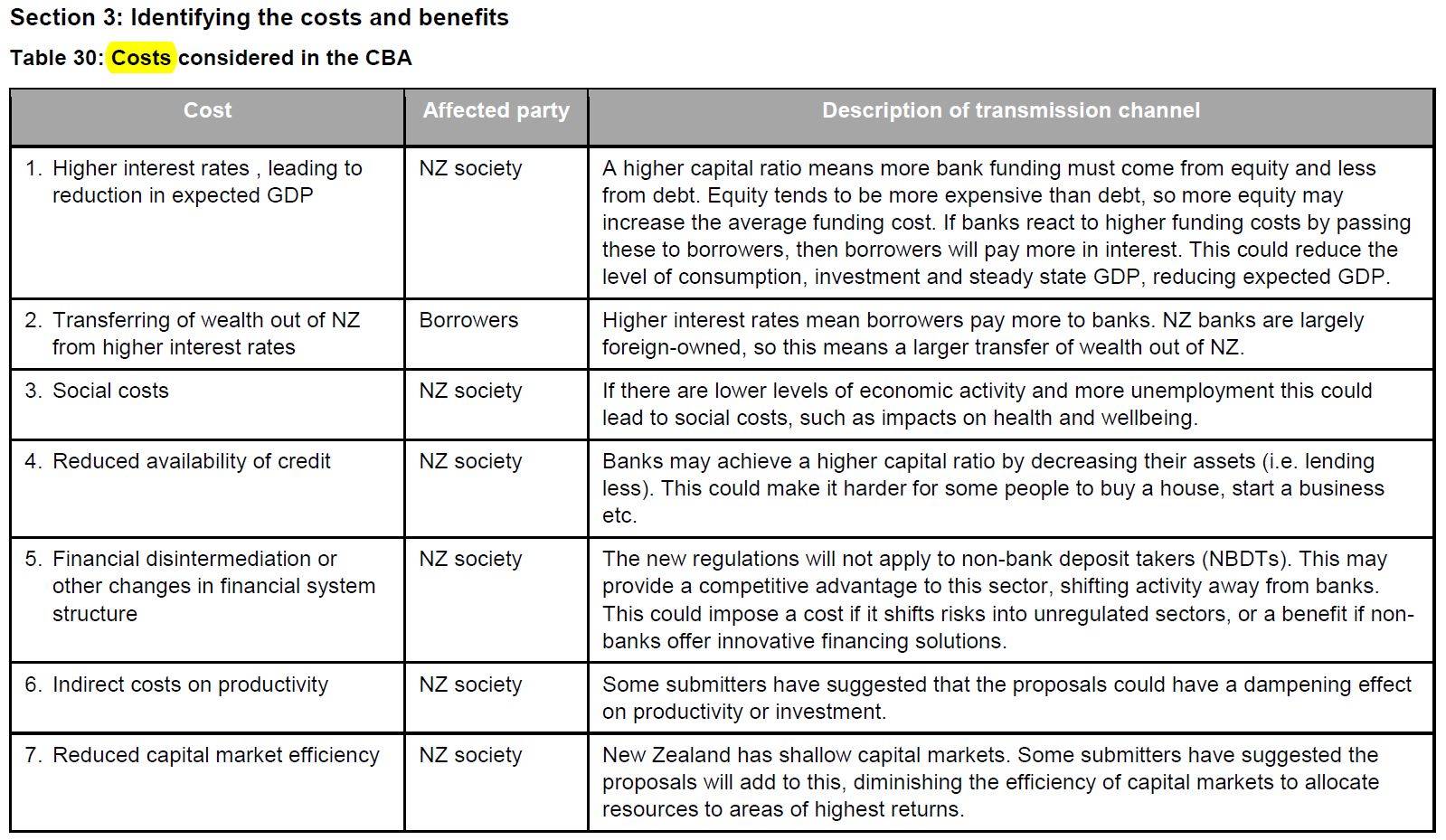

The RBNZ recognises that during the seven-year transition period it has given banks to implement the changes, they are likely to restrict their lending by 2.2 basis points.

It has assumed that without the changes, banks would have had annual credit growth of 5.10%. However with the changes, this will fall to 5.08% during the transition period.

It expects the impact to be much lower with a seven-year transition period, versus a five-year one as initially proposed.

The RBNZ says: “Increasing capital requirements can creates costs in the transition period that are independent of the steady-state costs. This is driven by banks restricting credit growth, rather than by restricting dividend payouts to investors, in order to meet capital requirements.”

Long-term impact

Coming back to the long-term impacts, the RBNZ recognises this will vary across banks.

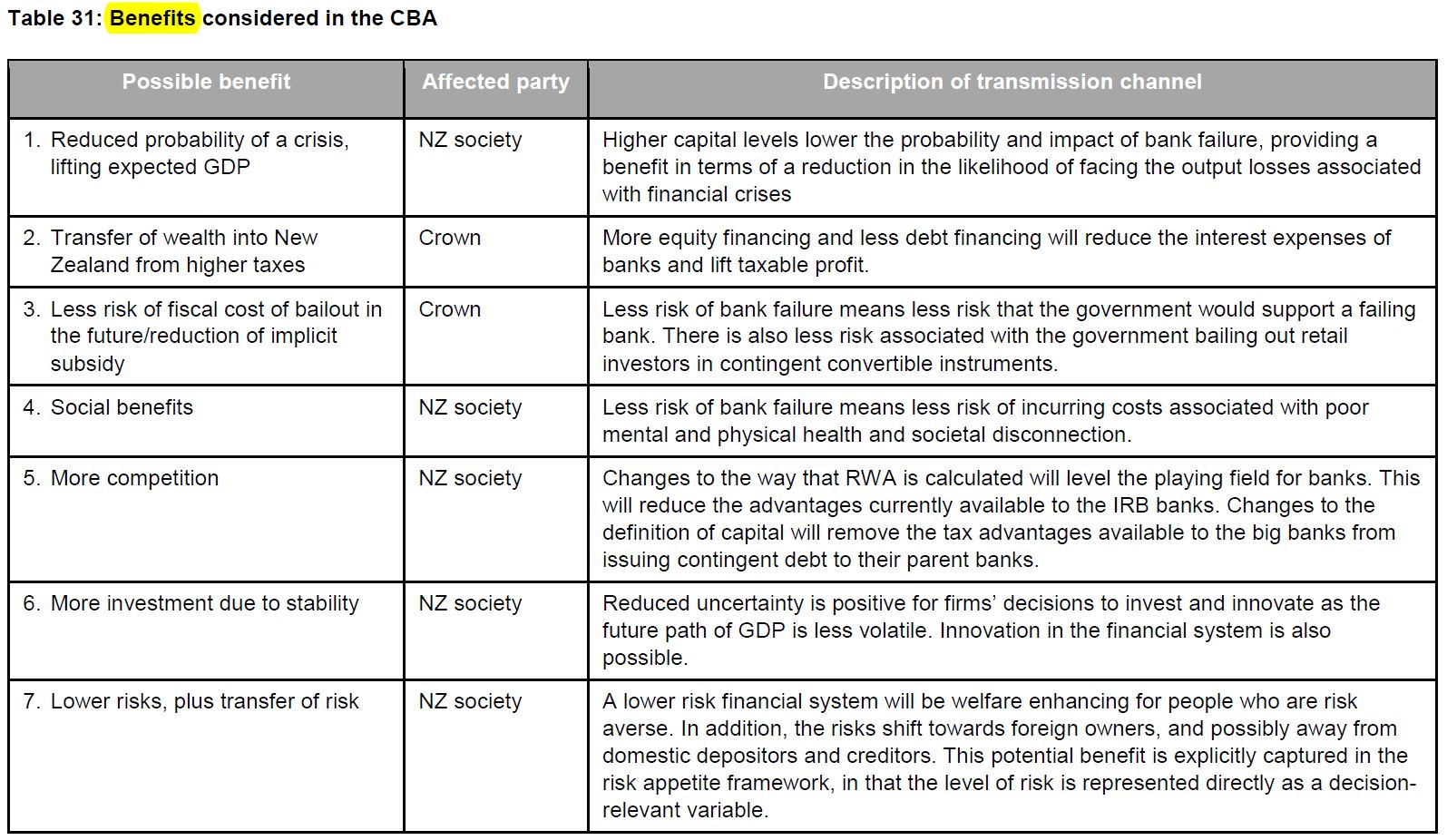

But it’s of the view that the changes, which will reduce the probability of a crisis in any given year from 1.8% to 0.5% (or deliver 1-in-200-year soundness), will be beneficial on balance.

It expects that on average, the interest rates borrowers will have to pay will increase by 20.5 basis points. So someone paying 4% interest on their mortgage, may be charged 4.205%.

This will dampen investment in capital and lower long-term GDP by 0.205%.

But offsetting this, it expects the reduced probability of a banking failure to give GDP a 0.83% boost, resulting in a net 0.63% increase.

Turning to the impacts on the transfer of wealth, the RBNZ accepts bank owners will want to make larger profits to compensate for the larger equity base. So they will charge borrowers higher interest rates. This money will go to banks’ foreign owners, denting GDP by 0.27%.

Countering this a little, is the fact that higher profits will require banks to pay more tax in New Zealand. This will add 0.08% to GDP. But weighed against the impact of profits going overseas, the RBNZ expects the net effect on the transfer of wealth to reduce GDP by 0.20%.

Mashing together the impact on the transfer of wealth with the impact on GDP, the RBNZ has concluded the total impact will be a 0.43% increase to GDP.

34 Comments

Okay, increases average mortgage costs by 20 bps, but what if any affect on deposit rates?

Bond and treasury yields?

.. I imagine this is just one more in a very long line of measures to protect us that we , the customer , will ultimately pay for ....

No increase for TD's !

A superb analysis, explaining the rationale, cost and benefits and how over the long term, benefits will outweigh the costs. Glad, RBNZ persevered through and brought this on.

... glad you're so happy ... cos you will be paying for this extra protection ... and me ... all of us .

.. the banks will continue on their merry way making supersized profits for their Australian owners ... regardless Orr the RBNZ ...

We are in a losing game as consumers. That is the tragedy and beauty of banks, depending on who you are.

If the Banks go under and if they are bailed out (or not), then also we are going to pay for it.

Slash dividends!?

A cap on dividend repatriation and stricter RWA for home lending could be the next steps, hopefully. The first one needs more political will and the second is a RBNZ issue. May be after the next election, depending on who comes to power ?

Conceptually flawed with no consideration of how banking regulators globally are heading nor any guidance as to how NZ banks are to adhere to these simplistic rules and the much more intensive and intrusive tests being applied by APRA.

I note in many of the submissions there was an observation that the RBNZ had not clearly defined what the objective or ideal state was or how they arrived at 1 in 200 years. A quick flick thru what has been presented doesn't seem to address those questions at all.

Whilst I acknowledge the virtue of making banks safer and increasing capital, the quality of this proposal and process from the RBNZ is extremely poor.

Its almost Jacinda-esque.... lovely idea... but dropped the ball on delivery.

Orr has stated in the past that they started from a gut figure, then began assesing how that adds up, and found it would likey be positive. Not sure why you think its conceptually flawed? Banks have a long history of privatising gains and socialising losses, should we not want such imprtant institutions to do less harm to our long term growth rates?

"Conceptually flawed with no consideration of how banking regulators globally are heading nor any guidance as to how NZ banks are to adhere to these simplistic rules and the much more intensive and intrusive tests being applied by APRA.

Yeah, its not a fashion parade, Orr doesn't have to be "on trend", he has to be effective. And the APRA tests are also not his baliwick, perhaps the Australian banks could ask the Australian regulator how they should comply?

At least they acknowledged the role of Tier 2 debt..... suggesting removing that was nothing short of stupid.

Okay Jenee .just so I understand what is the phase-in period for this , we dont want any sudden interest rate shocks ?

7 years

7 years but they need to start pricing this in now as to avoid a massive increase towards the end of the 7 year term. I believe the banks have already started pricing in these changes months ago when it was first announced, which is shown by the banks already tightening their credit criteria. It is already much harder to get a loan from the banks now and this is good. It should eventually lead to asset prices softening as sellers adjust to the new market. Less credit available always leads to lower asset prices, since most borrowers don't have funds to purchase a house outright, without a bank loan.

Isn't the demand for debt driven by its cost?

If banks want to recover the cost of holding more money for a rainy day, the conclusion I draw is an increased lending rate would mean a reduced level of lending. Customers can only afford a certain level of repayment, so will be forced to borrow less or push out the term of their loan. Correct me if I'm wrong.

This will mean reduced business for banksters, who will be forced to lend more responsibly rather than for their short term bonuses. Also reduce profit being exported from the country. How was 18% return on equity justified anyway?

Its a pity it got watered down from that initially proposed, however it was sure thing it was going to be delayed to avoid the consequences being felt prior to next years election. You'd be a fool to think the Reserve Bank is independent of the government.

Merry Christmas to the debt enslaved.

"reduce the probability of a crisis in any given year from 1.8% to 0.5% (or deliver 1-in-200-year soundness)" -- hmmmm..... wondering how Nassim Taleb's gonna name this one

A Grey Swan ?

White Swan in a coal cellar?

Golden Swan Dive !

O for orrsome,any measure to avoid the chance of OBR has to be good,let the bank shareholders carry the risk.

I agree and I am a bank shareholder. I take that risk knowingly, but a bank collapse would impact me much more than loosing a few shares.

.. the banks will pass on the extra costs to the customers ... they will not skip a heartbeat on this ... you & me , us poor smucks will end up paying....

Turning the impacts on the transfer of wealth, the RBNZ accepts bank owners will want to make larger profits to compensate for the larger equity base. So they will charge borrowers higher interest rates. This money will go to banks’ foreign owners, denting GDP by 0.27%.

This gets back to my previous comment, below, which demands to know how much risk weighted capital banks will have at risk for each dollar of mortgage debt granted. Depositors have a constant 100% at risk and banks may not be counting the mortgage assets funded by the off-balance sheet, derivative hedged (X-CCYswap) foreign funding in the on- balance disclosure of RWA percentages.

OBR exposed depositors need to see what dollar value of regulatory capital (1.6 cents?) is set aside for every dollar of bank credit applied to residential property mortgage asset creation. The depositors have 100% (100 cents) in the game for nothing in real, risk adjusted returns, and yet they remain unsecured bank creditors. What claim status do foreign bank and covered bond lenders have in comparison? If it's the World Bank etc (Kauri bond issuer) lending our local Aussie banks the foreign currency, they already have the same back in their account via the X-CCY basis swap (at the Libor basis discount) and the covered bond investors have direct claims on the mortgage asset collateral. What sort of democracy runs a racket like this? Answer, a kleptocracy. I am sure banks support all represented parliamentary parties at some level of non-public disclosure. Link

I thought the banks were making Billions a year in profits so why is it suddenly so hard to just up their capital ? 7 years to phase it in, are you kidding me ? Funny how they cut rates 50 bps overnight and then people start freaking about it going up by only 20 bps ! Something tells me that there is just still way to much money flowing out of the bank reserves and when things suddenly get tough they will all be crying "Were broke, please bail us out" after decades of totally creaming it.

Again - this is where I'm with Ray Dalio - capitalism (in its current form) is broken.

Pretty sure the banking system could be fixed if they are forced to maintain a level of capital instead of loaning it all out to the last cent. Also I think most people would agree that say another 0.5% interest rate rise to guarantee the banking system cannot fall over in a any crisis is money well spent. Much better than deposit insurance, it never covers anywhere near enough for those that have the most to loose anyway.

uNfortunately the amount of capital needed, still does not guarantee against a bank failure. Not when you realise the amount of derivatives stacked against these banks. Warren Buffet refers to Derivatives as "Financial Weapons of Mass Destruction", for a very good reason.

Well done Mr Orr, I think we have a good RB governor in charge

... the banks will fleece your pocket to pay for this protection... and mine ....all of us ....

Orrsome ?

I don't think the banks will fleece us, they need our business and yes if it makes the banks a little more solid, good on Orr

This is the best move our RBNZ has made in a very long time. We need our banks to stay strong because the consequences of a bank failure will impact all of us, not just those who borrowed more than they can afford to repay.

with a 14-17% ROE in the current environment there is ample room for a reduced shareholder return...scaremongering on a grand scale FFS

They have already reduced our dividends significantly and suddenly. You can share the costs with us. I would still rather have safer banks anyday!

GFC as Talab explained was supposed to be a 6 sigma event. The dot com implosion similar. These are models in maths. We live in real world not models. Bank equity will be wrecked in next crash or even a 5% default by mortgages. We are NOT informed by anyone this far when banks have to start raising Tier 2 capital and by how much. Since the next crisis is overdue and likely pre end of 2021, then time frame laxity given to banks will prove risky

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.