By Gareth Vaughan

ANZ New Zealand has posted a 12% rise in annual net profit after tax to a shade under $2 billion, a fresh record high for the country's biggest bank.

ANZ NZ says September year profit after tax rose thanks to the strong NZ economy, improved credit quality and the bank's focus on digital innovation and customer service.

Higher net interest margins, the difference between the interest income generated from the bank's loans and the amount of interest paid for funding such as deposits, also helped profit. The ANZ Group results show the NZ operations' first half-year net interest margin up eight basis points year-on-year to 2.38%, and its second half-year net interest margin up four basis points year-on-year to 2.37%.

Additionally ANZ NZ's bottom line benefited from a $117 million positive turnaround in its hedging used to manage interest rate and foreign exchange risk, plus a $40 million revaluation of insurance policies.

September year profit surged $206 million, or 12%, to $1.986 billion from $1.780 billion last year. ANZ NZ says it has a financial relationship with about one in two New Zealanders, being people who have or use at least one of its products. That's about 2.45 million people, meaning the bank made the equivalent of about $809 per customer.

Both revenue, or operating income, and expenses rose 3%. Revenue was up $106 million to $4.183 billion, with net interest income also up 3, or $99 million, to $3.177 billion. ANZ NZ's operating expenses rose $48 million to $1.494 billion. The bank's credit impairment charge dropped $6 million, or 10%, to $53 million.

ANZ NZ's cost to income ratio fell 110 basis points to 36.1%.

Customer deposits increased 7.5% to $104.1 billion, and gross lending rose 3% to $128.7 billion. This left a funding gap of $24.6 billion, down from $28.1 billion the previous year.

UDC Finance off the block as CEO highlights benefits from economy

Meanwhile, ANZ says any sale of UDC Finance is off the table for now. (See more on this here). And ANZ NZ CEO David Hisco highlights benefits to the bank from a robust economy.

"The continued strength of the economy - strong exports and tourism sector aided by a lower dollar, continued demand for houses and growth in household incomes - has been good for our business," Hisco says.

"The Government's investment in major infrastructure across the country and trade achievements are providing jobs and fuelling consumer spending and saving. We also have had a significant reduction in provision charges - funds set aside for bad debts - due to credit quality improvements across our retail, commercial and agri businesses," Hisco says.

Against the backdrop of the Australian Royal Commission and Financial Markets Authority and Reserve Bank review of NZ banks' conduct and culture, Hisco says ANZ NZ is "committed to doing what is best for our customers and the community, being transparent and putting things right quickly. This will continue to be a strong focus for us in the future."

ANZ NZ's share of the home loan market was put at 31.0% at August, down 10 basis points year-on-year. As of September 30, ANZ NZ's home loan book stood at $81 billion, up $4 billion, or 4.9%, year-on-year. In KiwiSaver ANZ NZ now has 24.2% market share, down 40 basis points year-on-year. It has $12.9 billion under management, and 745,000 KiwiSaver customers. Over the September year the bank's household deposit market share fell 20 basis points to 33.8%, and its business lending market share dropped 130 basis points to 26.9%.

ANZ NZ's annual cash profit was up $49 million, or 3%, to $1.904 billion.

Dividends equivalent to 84% of annual cash profit

As previously reported by interest.co.nz ANZ NZ paid an $800 million ordinary dividend in September. This followed ordinary dividends of $3.8 billion for the nine months to June, which included April's issuing of $3 billion worth of shares to immediate shareholder ANZ Holdings (New Zealand) Limited, and the paying of $3 billion worth of dividends to the same entity. ANZ NZ said this was done to pass retained earnings to the bank’s parent, without impacting total equity, with no tax benefits generated.

Thus effectively the bank paid $1.6 billion in annual dividends, a similar level to its September year last year when they weighed in at $1.635 billion. This year's dividends are equivalent to about 84% of annual cash profit, down slightly from 88% last year.

Tough year for parent with pay cuts

Parent the ANZ Banking Group posted a 5% fall in annual cash profit to A$6.487 billion. Its return on equity was down 67 basis points to 11.0%, first half net interest margin was 1.93% and second half 1.82%. The bank is paying unchanged annual dividends of A$1.60 per share.

Group CEO Shayne Elliott says ANZ has taken action to "fast track fundamental changes" resulting from "our failures" highlighted by the Royal Commission.

"We expect the tough revenue growth environment in retail banking in Australia to continue for the foreseeable future, however we are well positioned to take advantage of growth opportunities in institutional [banking], Asia and New Zealand," Elliott says.

"While there was much to be pleased about this year, we accept the significant community concern as a result of our failures highlighted by the Royal Commission has impacted our standing in the community," Elliott adds.

"This was a factor in the decision to reduce variable remuneration [from the ANZ incentive plan] paid to staff this year across the bank by $124 million. We are also undertaking the urgent work required to fix the failures that have been highlighted by the Commission and further increased our focus on conduct issues."

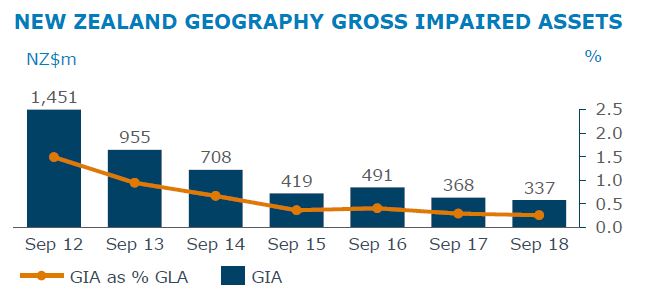

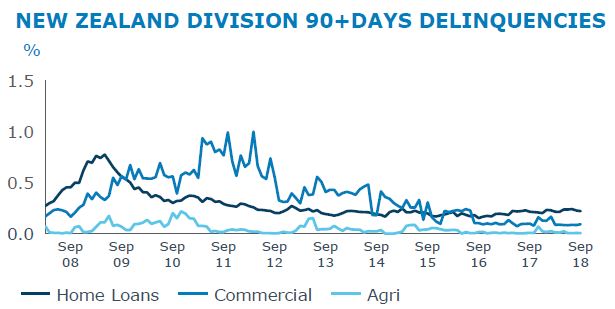

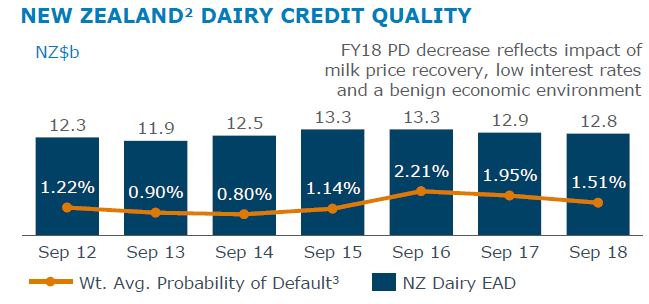

The charts below come from the ANZ Group presentation.

ANZ NZ's press release is here, the ANZ Group press release is here, and the ANZ Group presentation here.

There's also the transcript of an interview with ANZ Group CEO Shayne Elliott by ANZ's own BlueNotes website here.

63 Comments

Institutional Division down 27% on last year.

That has brought many an aspiring CEO of The Group down......

The Markets unit had a shocker... In fairness to ANZ though, the NZ operation is producing class leading numbers, it's a great business for them.

Sounds to me like the NZ banks are not in too much trouble and that they have room to withstand a downturn

But will the NZ offshoot matter if the parent hits the wall? The same results reflected in Aussie:

"ANZ profit goes backwards as costs bite"......"...we sacrificed short-term revenue growth and higher margins ... particularly in the investor and interest-only segments". But "it was the right thing to do" "

bw, that means the ANZ in OZ has made less profit but nonetheless still a profit. I'm a multiple business owner and I would not expect my businesses to make record profits every single year.

Making less profit ($5'800 Million = 5.8 billion to be exact) in a bad year is not bad at all and it's a lot better than making a loss

Actually, the more I think about it, the more I think NZ banks will be fine. ANZ OZ made $5.8 billion profit… that's $5.800.000.000 PROFIT !!! ….. in a difficult year!!!

How are they getting net interest margin up with dropping mortgage rates?

Is that much of their lending to low equity customers getting hit with low equity margins?

Are people carrying higher credit card balances?

The world is awash with cheap money. More to come as Trump fires up the printing presses to fund his trade war with China.

Interesting perspective seeing as the FED is on a distinct course of reducing it's balance sheet.

"reducing it's balance sheet" .. interesting idea, but you can't tapper a Ponzi scheme.

Hi Pragmatist.

The nations mortgage debt has now risen from $225 billion in 2016 to $254 billion in 2018. 12% or so more debt created and we are likely to see a fourth year of negative household savings rates (which has been growing as a negative percentage each year). The Lords will 'taketh' but they are not giving away. For a housing correction not to occur not only do we need debt to grow another 12-15 billion this year, we need it to do the same the following year etc etc..

essentially that is where all our GDP comes from, if households get to the point that they decide to de-leverage even the slightest amount, then pop!. So we have to keep expanding credit to the private sector and enslaving the next generation. Its that or bust, but the bust will come soon anyway.

The links below are worth thinking about ( take a look at the graphs on the max tab). Every-time that the household debt curves slow, ie flat-line or turn negative, there is a downturn and housing correction. Each nation has its different physical limits (as proportion of GDP) and it's not that percentage to GDP that is relevant its all about the pace of debt growth. That's why the banks are lowering rates, if the pace of debt growth slows and houses deleverage the correction becomes a spiral.

https://tradingeconomics.com/japan/households-debt-to-gdp

https://tradingeconomics.com/canada/households-debt-to-gdp

https://tradingeconomics.com/spain/households-debt-to-gdp

https://tradingeconomics.com/singapore/households-debt-to-gdp

https://tradingeconomics.com/ireland/households-debt-to-gdp

https://tradingeconomics.com/united-states/households-debt-to-gdp

https://tradingeconomics.com/united-kingdom/households-debt-to-gdp

https://tradingeconomics.com/australia/households-debt-to-gdp

https://tradingeconomics.com/new-zealand/households-debt-to-gdp

That doesn't address the question I asked. Nice rant tho.

…but it does make one look very smart when you post looooong comments with lots of links

I thought he answered in his first sentence? Net interest margin has possibly remained static, but overall lending is up 12% hence more profit? And yes then goes on to say if we don't have this growth in debt we might be in the poo

. The ANZ Group results show the NZ operations' first half-year net interest margin up eight basis points year-on-year to 2.38%, and its second half-year net interest margin up four basis points year-on-year to 2.37%.

Not a static NIM.

If the average loan asset interest rate has fallen, the only way NIM (as a percentage of assets) would have risen is because their borrowing costs must have fallen by more i.e. those miserable savings account rates and term deposit rates you get. Not sure if the definition of NIM includes a provision for bad debts, but if it does, that would also be a contributor. If you are just talking about NIM in terms of dollars, then that can rise just based on volume increases.

Deposit rates have been dropping.

"fuelling consumer spending and saving.' Saving?

I very much doubt if we'll see an improvement in the household saving rate this year... which is likely to be a 4th negative year in succession when figures are out next month.

Depends how people are saving. People might buy precious metals, crypto-currencies, use foreign savings accounts, etc. The idea people should/will save by placing their NZ dollars into a NZ bank account or term deposit is perhaps misguided. Given real inflation, such a savings regiment would be akin to setting a small portion of your NZ dollars on fire.

Buying something is spending, not saving. At a stretch you could call it investing, but definitely not saving.

I bought a car and a fridge last year, does that mean i'm saving?

If you replaced the V8 Holden with a used yaris.. probably :)

Gold = Money

Dollars = Currency

Therefore acquiring gold is a form of saving.

Is acquiring Platinum a form of saving too?

the ANZ chairman will be looking for a nice bonus,

He gifts it to charity, doesn't he! (sarc off)

Bollard lowered the OCR to %3 as an emergency measure, then to %2.5 after the Christchurch earthquake.

So why is it on %1.75 today unless we are deep in the belly of a monster?

Absolutely right Andrew 1.75% interest rates?

Keeping the bubble from deflating

Hi Colin

Indeed, however even at those low rates the pace of credit growth is decelerating and that is all it takes to collapse the system. If the pace of debt growth to households was $6 billion say next year and $5 billion the year after, that would be enough to lead to a heavy housing market correction as there would not be enough buyers to prop up the existing debt and the perceived asset values - it needs more debt to keep it up and can't survive with less or even a reduced pace of increase. The only way NZ housing could keep going (that is just to stay at the current prices) would be if household debt were to be at $270 billion next year, $285 billion 2020, $301 billion by 2021. That's not going to happen because we're already well beyond that servicing ability so there is only direction for the market to go now even if there is credit growth, the change of pace of that growth means that we will see a downturn.

We're short on FHB's, reduced the number of foreigners and there is no point speculating in a flat market where rents don't cover mortgages and there is no capital growth. So the reduced demand for credit is a self fulfilling contraction.. That's why the msm, banks and real estate agents are really pushing things on the young at the moment.

They should lift the banks capital ratio so the money stays in NZ.

So for near on $2b profit what is it that ANZ and other banks offer? Being a middle man is a minuscule part of there business now so term investments and savers get next to nothing. They loan money that they create from nothing which is there main source of income. Aside from their financial services, how do they provide $2b worth of value?

Hi Withay

99.9% of the population don't understand that and probably don't have the mental capacity to ever understand.

Here is the bank of England Report from as recent ago as Q1 2014 where they finally cottoned on and recognised that the banks 'create money' when a loan is written.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/20…

Hopefully we'll get the understanding to 99.8% by the end of the next crash.

Is this same creation of money by banks happening like that in NZ and AU, the way Richard Werner suggests? If so, why do we continue to get bits, like for example in the article above, about ANZ's net interest margins? If what RW says is true for here, then shouldn't the interest margins be more like 4.5? And with this money creation thing in mind, what difference does the OCR actually make? Or is the conjuring up of new money just to cover the funding gap of $24 billion? Sorry for these noob questions, still trying to get my head around this...it feels too wrong to be true.

OnTick

https://www.youtube.com/watch?v=79Xys_2e9CY

Strong credit growth outstripping deposit growth? Go off shore and top up?

OnTick

Let's say it's unlikely that you could grow debt in the economy using deposits (by over $25 billion in 2 years) with a negative household savings rate.

https://www.stats.govt.nz/news/households-continue-to-outspend-their-in…

Hi Nic, it gives me hope that some understand though. If the profile of the issue can be raised enough then maybe we could tick off most of NZ’s biggest issues by correcting it.

Regarding the article, the majority of the profit should be going to term deposits/local savers, not overseas. Banks need to become an intermediary between savers and borrowers again, not the abomination they are now.

Richard Werner

Interest rates & GDP growth over half a century in 4 of the 5 largest economies show that interest rates follow growth & are consistently positively correlated. If policy-makers aimed at setting rates consistent with a recovery, they'd raise them.

https://www.sciencedirect.com/science/article/pii/S0921800916307510 …

Can anyone recall a bigger New Zealand corporate profit than this that wasn't inflated by asset sales and/or other one-off items?

How about the other banks Gareth? the total river of money going out of the country should be of serious concern to the Government, but they don't seem to understand or care.

I can see Ozzy parent banks aggressive leeching in any way possible to preserve capital. Where does that leave NZ credit availability then?

Why would the government care? The banks price at what they think the market can stand. From this one bank they get a 770 million dollar tax skim for the year. For doing nothing. They don't bite the hand that feeds them.

The government wouldn't necessarily make less if ANZ's profit margin was reduced. Sure, they'd make less corporate tax from ANZ, but they'd make more in GST and corporate tax from other companies as that money gets spent elsewhere. If the profit was reduced by paying NZ based staff a higher wage, the government might take in more tax as the 33% personal tax rate is higher than the 28% corporate tax rate.

So they get to keep 1/3 of the money that leaves the country, while 2/3 is no longer being taxed as it is spent in the economy (GST -> Company Tax -> Income Tax - > GST -> Company Tax - > Income Tax ->).

Murray -they don't afford to care. They could invest some ten of billions of tax payers money into Kiwibank and try to "stem the flow" but frankly they dont want to, and neither does the public if they understand what that means to other public services. They had the BNZ, but that went broke in the 80's and was pick up by a much more competent bank in NAB. NZ is extremely well & securely serviced by the Australian banks mostly, and if you're not prepared to do it yourself, the profits will flow to those shareholders who will - as a Kiwi I'm one of those where my bit doesn't offshore, I don't think there's a rule that I'm the only Kiwi allowed to do that.

ANZ's supposedly inflated profits are not translating into stellar shareholder dividends - they are good but not exceptional.

Share price down about 18% since Aug. Dividends are good with franking credits. Do they exist in NZ? I don't know.

Just a cheeky $400 profit from each man, woman and child in New Zealand, for a single bank. Nothing to see here.

My family doesn’t bank with ANZ so not sure how they made $400 of each of us?

Am I missing something?

Don't worry, others will be picking up your slack. The $400 is an average over the whole population, I'm sure once you get down to adult customers of ANZ the average profit will be in the low 4 figures.

And the government took on our behalf $150 for each of us in tax.

Yeah that's right, that $150 is gone for good.... Never to be seen again......

The government needs money to keep all the balls in the air. Allowing market-dominant companies to earn super profits and skimming off corporate tax is far easier than regulating competition and lower costs for all. Then they would just have to tax us all more individually to make up the shortfall. Taking money off the big bad corporations is more politically palatable than taking it from the workers. But the workers still pay regardless.

dp

To all the petty, envious, jealous comments above, bitching about someone else making more money doesn't help you. Spend your time minding your own business, as in "really look after your own affairs" instead.

Shame there's no thumbs down option, surely I'd break a new record with this comment

For a little context, the frequently criticised supermarket duopoly made profits of ~$800 million in the last financial year. The banks made ~$5 billion. We're not innocent bystanders watching the banks make this money, we're the customers they are making it from.

The average bank profit/NZer last year was ~$1000, from your comments regarding rental properties I would assume your contribution is significantly larger than that. I'm far from anti-business, but I find the figures interesting.

To me I don't care how much banks or anyone else is making, I care about my own business. Call me selfish but I don't mind if banks or anyone else makes a gazillion dollars profit as long as they help me make some profit of my own.

I pay the banks hundreds of thousands of $ in interest pa and I'm very happy paying it. What matters is that I can make a profit out of my borrowings, not how much the lender is making

Yvil.

You obviously have a big relationship with the bank and I'm sure they will treat you kindly. How many people do you directly employ in your business?

Nic,

What do you do for a living?

How much do you owe to the banks?

Do you have staff, if so, how many?

but banks are not 'someone else'

Yeah but you can leverage the banks money and make your own money. Have to pay to play the game though.

Ah so that's where my 200 a month in non negotiable overdraft management fees (whether I use it or not) ended up. They also charge higher rates because it is 'unsecured' - this means not secured by residential property, the 1m in unencumbered stock is worthless.

Love you ANZ .... not.

How many accounts do you have? $200 a month seems a bit steep...

Approximately 1% of the total tax take on this if I am reading the numbers right Gareth? From one bank, that is an astonishing figure. What is the total take from all the banks combined? How big a part of the economy are these banks? Where is the line between facilitating industry and commerce, being industry and commerce.

HI Scarfie, isn't the govt %38 of gdp? Take away the banks take and no wonder there are so many poor people.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.