Governor Adrian Orr says the Reserve Bank plans to impose capital standards on banks that match the public’s risk tolerance.

"We have been reassessing the capital level in the banking sector that minimises the cost to society of a bank failure, while ensuring the banking system remains profitable," Orr told a Business NZ CEO Forum in Auckland on Friday.

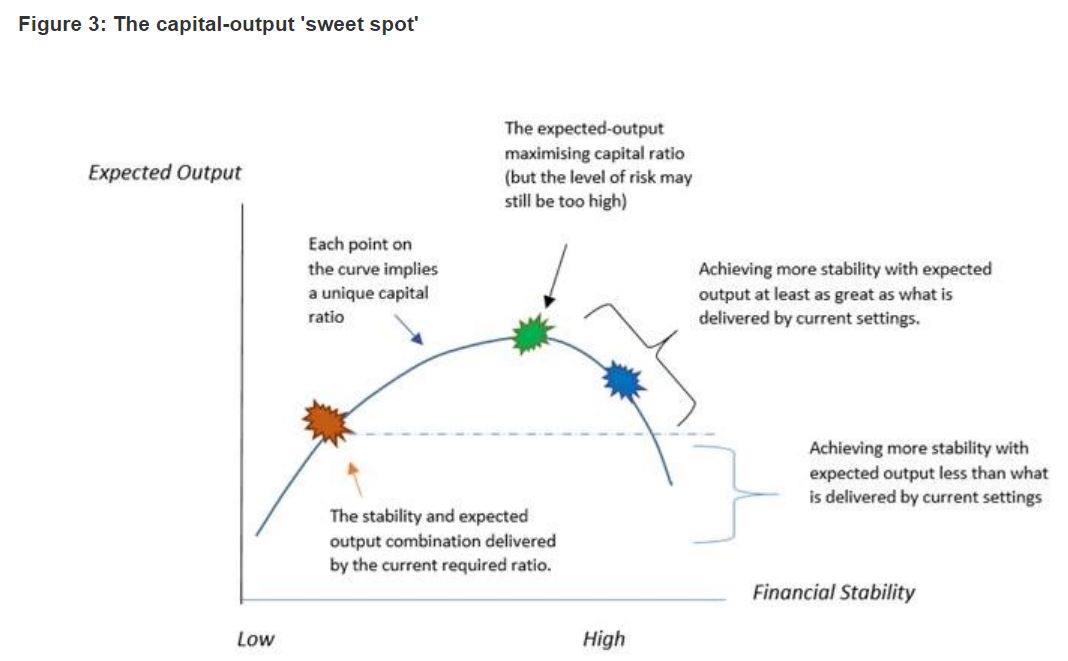

"The stylised diagram in Figure 3 [below] highlights where we have got to. Our assessment is that we can improve the soundness of the New Zealand banking system with additional capital with no trade-off to efficiency," said Orr.

"In making this assessment, our recent work makes the explicit assumption that New Zealand is not prepared to tolerate a system-wide banking crisis more than once every 200 years. We have calibrated our ‘sweet spot’ thinking about economic ‘output’ and financial stability benefits."

'We need to hear a broader perspective'

Orr went on to say that the Reserve Bank is tasked with ensuring the banking system is sound and efficient. The most important tool to do this is ensuring banks hold sufficient capital, or equity, to be able to absorb unanticipated events. The level of capital reflects the bank owners’ commitment, or skin in the game, to ensure they can operate in all business conditions, bringing public confidence, said Orr.

"Given its importance, we have been undertaking a review of the optimal level of capital for the New Zealand system. We conclude that more capital is better. We are sharing our work with the banking sector and public, and expect to hear one side of the story loud and clear, that capital costs banks. We need to hear a broader perspective than that, to best reflect New Zealand’s risk appetite."

"The Reserve Bank needs to ensure there is sufficient capital in the banking 'system' to match the public’s 'risk tolerance.' This is because it is the New Zealand public - both current and future citizens - who would bear the social brunt of a banking mess," added Orr.

"We know one thing for sure, the public’s risk tolerance will be less than bank owners’ risk tolerance. How do we know this? Surely the more capital a bank has the safer it is and the more it can lend. Why don’t banks hold as much capital as they can?"

"First, there is cost associated with holding capital, being what the capital could earn if it was invested elsewhere. Second, bank owners can earn a greater return on their investment by using less of their own money and borrowing more - leverage. And, the most a bank owner can lose is their capital. The wider public loses a lot more."

"Hence, we need to impose capital standards on banks that matches the public’s risk tolerance," said Orr.

'Bank failures happen more often and can be more devastating than bank owners & credit ratings agencies tend to remember'

Orr went on to say existing capital levels are based on international standards, and thus aren't optimal for any one country.

"The standards are also a minimum. There is a clear expectation that individual countries tailor the standards to their financial system’s needs. Banks also hold more capital than their regulatory minimums, to achieve a credit rating to do business. The ratings agencies are fallible however, given they operate with as much ‘art’ as ‘science’," said Orr.

"Bank failures also happen more often and can be more devastating than bank owners – and credit ratings agencies – tend to remember. The costs are spread across the public and through time."

"Many large banks are foreign owned – especially in New Zealand. Their ‘parents’ are subject to capital requirements in their home and host country. This creates continuous tension as to who gets the lion’s share of capital and failure management support. It would be naïve to expect a foreign taxpayer to bail out a domestic banking crisis," Orr added.

"Hence, New Zealand needs to assess its own risk tolerance, and decide who pays to clean up any mess and the scale of that mess."

"A word of caution. Output or GDP are glib proxies for economic wellbeing – the end goal of our economic policy purpose. When confronted with widespread unemployment, falling wages, collapsing house prices, and many other manifestations of a banking crisis, wellbeing is threatened. Much recent literature suggests a loss of confidence is one cause of societal ills such as poor mental and physical health, and a loss of social cohesion. If we believe we can tolerate bank system failures more frequently than once-every-200 years, then this must be an explicit decision made with full understanding of the consequences," said Orr.

Widest ranging review of bank capital requirements

His speech follows the release of the Reserve Bank's latest Financial Stability Report on Wednesday, where Orr said bank capital is the number one safety valve for the citizens of a country.

The Reserve Bank will release a consultation paper on minimum bank capital ratios in December. This is the final part of the widest ranging review of bank capital requirements the Reserve Bank has ever undertaken, which began early last year. (There's more information here).

In an "in principle" decision announced in July, the Reserve Bank said the big four banks will now have to calculate capital under both the internal model and standardised approaches, and publish both sets of results, rather than just use the internal models approach that allows them to set their own models for measuring risk exposure which they must then get approved by the Reserve Bank. All other banks use the standardised approach for measuring credit risk, through which their credit risk weights are prescribed by the Reserve Bank and are higher than those of the big four banks.

The big four banks - ANZ, ASB, BNZ and Westpac, using the internal models, or internal ratings based, approach means credit risk weights calculated using it account for about 86% of NZ bank lending.

Another in principle decision the Reserve Bank has made during the capital review is to ban contingent debt from qualifying as regulatory capital.

The chart below covers key NZ retail banks at September 30

| Bank | Total capital | Gross loans |

| ANZ | $11.858 billion | $127.058 billion |

| ASB | $7.882 billion | $83.983 billion |

| BNZ | $8.763 billion | $83.682 billion |

| Co-operative Bank | $216 million | $2.386 billion |

| Heartland Bank | $570 million | $4.148 billion |

| Kiwibank | $1.680 billion | $18.789 billion |

| Rabobank | $1.545 billion | $10.387 billion |

| SBS Bank | $341 million | $3.876 billion |

| TSB Bank | $626 million | $5.558 billion |

| Westpac | $8.925 billion | $80.515 billion |

The chart below comes from Wednesday's Financial Stability Report

Note, CET1 is common equity tier one capital. Tier 2 is tier two capital, tier 1 is tier one capital, and AT1 is additional tier one capital.

The video below comes from the RBNZ

23 Comments

To anyone with a bit more banking knowledge than I possess, does this mean that NZ's major banks will need to hold a larger amount of capital relative to their lending out than they have to date?

Yes, hopefully. But RBNZ consultation processes tend to start with the RBNZ taking quite a strong position that gets watered down somewhat by the end of the process.

You'd think that was the implication, but i await the transformation of Central Bank doublespeak to actual action.

Capital idea!

Interesting to note that the capital to loan ratio is in the vicinity of 10 for most. The interst they pay us for our deposits is really pitiful!

not deposits, loans,

"we" are unsecured creditors.

they don't hold the funds on our behalf, or in trust for us...

Yes, I understand that and have argued that point many times. I find it very frustrating that the authorities do not act to change that.

Let's see what it actually turns into, but on face value - good!

However, are we at year 199, Adrian? You tell us what your models say, and we'll be able to judge you on what happens from here.

"New Zealand is not prepared to tolerate a system-wide banking crisis more than once every 200 years."

I don't reckon New Zealand should have a system-wide banking crisis - at all.

Yes, it is not natural disaster planning after all.

In the interests of Adrian Orr's call for a broader perspective, here's an article from a couple of years ago; Why banks should be holding more capital against their housing loans

I applaud Adrian Orr for his work on imposing stronger capital standards on banks that match the public's risk appetite. I for one, am as at least as concerned about the risk of loss of my bank deposits as I am with losses in the value of my shareholdings, and that simply shouldn't be so, given the theoretical nature of the risk of those two asset classes. Should a banking crisis occur, I have little confidence that I won't suffer a loss, or at the very least, a substantial haircut.

What a shame. An opportunity to address a broader range of issues around bank capital levels is going begging. Mention capital levels and damn near everyone in NZ relates it solely to its impact on our housing market. We have an opportunity to broaden the public discussion ( and that is what Orr is asking for ) around where NZ's financial future lies. In simple terms the RBNZ influences where in the economy and for what length of term the trading banks lending is directed. It is clear - the RBNZ picks financial winners and decides losers. Orr has already acknowledged that the Basel rules are not specific to any one country. Now is the opportunity to review the various parts of the economy and their relative risk levels and after analysis if there is room to adjust the various bank capital levels required the RBNZ could influence the trading banks future direction of their funding..

Wilco, I'm not aware that Adrian Orr has said the capital review only relates to banks' housing exposure. In fact in what I've heard and read, he specifically hasn't said that...It's a capital review full stop. Nothing is going begging at this point.

Gareth - I didn't say Orr has said the capital review only relates to housing - I said damn near everyone is only interested in its impact on the housing market. From what I understand the focus of this ongoing RBNZ review has been on the definition of bank capital and what banks can claim as their capital contribution. They are now looking at the level of that bank capital needed to minimize bank failure and make sure the banks have enough skin in the game to ensure prudent lending behaviour by them. Great. But what an opportune time to also reconsider the RELATIVE capital ratios are right for NZ's future. As an example NZ has relied almost exclusively on the Basel rules with one of the few exceptions being a rural review which is now 7 years old. These trading bank capital adequacy ratios are a potentially powerful tool for the RBNZ to use to guide future lending and therefore future economic growth.

Dec 03, 2017 "Reserve Bank warns: 'It's not our job to protect you from the housing market'; https://www.stuff.co.nz/business/99408539/reserve-bank-warns-its-not-ou…

It's prudent the RBNZ now takes steps to protect depositors by enforcing tougher capital requirements so to keep banks open.

The RBNZ are mindful that the risks of another global crisis are growing.

Right. Let's do it then. I'll do some study & homework over the weekend & report back.

This is right up Interest.co.nz's alley. Maybe we could co-ordinate our findings and make a submission???

Can we form a committee? Do we invoice Jacinda Ardern directly for our time and refreshments?

Good on them. I criticised them for the LVR changes but I guess this goes some way to mitigating.

don't get carried away too soon. What Orr is saying is that if the banks hold more capital, then the RBNZ is prepared to lower lvr. The trade-off is that for shareholders to get the same return, bank margins will need to increase. That means higher interest rates for borrowers, and lower deposit rates for savers.

Wilco, we haven't seen the consultation paper yet. If the capital requirements for various asset classes don't get a mention we can still submit on them.

Seems strange after relaxing lvr's. Orr giveth with one hand and taketh with the other. Probably more appealing to the general public this way though.

As mervyn King made clear in his book on the GFC-The End of Alchemy,giving bank assets a risk-weighting dependent on their perceived riskiness,failed completely.

Thus,in early 2007,Northern Rock had the highest ratio of capital to risk-weighted assets of any major UK bank and was indeed,considering a return of capital to shareholders. At the same time,its leverage was extraordinarily high at over 60/1. To quote him; "In the case of Bank regulation,it is better to use a measure of leverage rather than a ratio of capital to risk-weighted assets".

Leverage is not one of the many metrics in the RBNZ Dashboard and though it can be easily calculated from the figures,I would like to see it stated explicity. In my feedback to the RB,I made this point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.