As we head into winter, financial markets are signaling that interest rates will be rising further.

Inflation's threat from the expected long-term fallout from Donald Trump's Gulf War is driving the upward expectation.

Markets have come to accept that the monetary authorities will have little alternative than to hike rates to keep inflation in check.

That is especially true in New Zealand where the current Government removed the dual mandate that required the Reserve Bank (RBNZ) to consider the effect on the labour market. Now their sole mandate is inflation control. And RBNZ Governor Anna Breman committed to being "laser-focused on inflation" when she was appointed by the Minister of Finance.

But this rising interest rate trend isn't just related to New Zealand. It is global. Oddly however, equity markets don't seem to care. They know the world is in a rising rates cycle, but equity indexes are generally at near record highs. (However, that may only be because such indexes are now dominated by big tech.)

Historically, the rising cost of money hurt corporate profits. And it restrained households and those sectors that rely on household willingness to spend, especially on leveraged spending like house-buying.

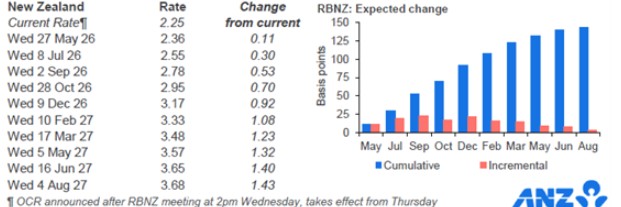

How far will interest rates rise?

Market signals currently suggest the RBNZ's Official Cash Rate is going to rise from its current 2.25% to 3.75% over the next year. At least, that is what financial markets are pricing.

NZ Government bond yields have been rising too. From its recent low point in October 2025, the one year NZGB yield has gone from 2.45% to just under 3.1% now (+65 bps). The two year NZGB has gone from 2.5% to 3.7% (+120 bps).

Of course, the primary influence on these isn't local, rather it is the big international benchmarks. The US Treasury 10 year hasn't moved a lot even if it is now back up to year-ago levels. But the Japanese 10 year is up at an almost 30 year high. And the Australian 10 year is back to levels last seen in 2011.

Wholesale money markets are pricing in two more +25 bps hikes in Australia over the next year, three by the ECB, three by the Canadians, one by the Americans, and three by the Bank of England.

So the six +25 hikes priced in for New Zealand looks excessive on the face of it, but we are starting eight such hikes behind Australia, six behind England, and five behind the Americans. Our Consumers Price Index levels are not so different to explain those discrepancies. So, we have some catching up to do, and that will involve pain that has so far been deferred.

Adding another +1.5% to our OCR will not help our property market. But much of our borrowing is on fixed rates. Those fixed rates will be more influenced by the international cost of money. It seems unlikely this will be less than the signaled OCR hikes.

The average home loan (RBNZ C31) is currently $321,000 for current owner-occupiers, and remember half will be borrowing less than this, half more. It is $588,000 for first home buyers (FHBs). The average two year fixed home loan rate is currently 5.29%, and most borrowers will be on lower earlier fixed rates. These two data points make the current reference 30 year mortgage payment $1065 per week.

If the priced +150 bps rise does flow through over the next year, that weekly mortgage payment will rise to $1115 and a +5% addition to household budgets for this item. (Let's not talk about rates or insurance.) For FHBs the payments go from $1951/week to $2048/week.

For the average owner-occupier, that eats into their income by -$2727 of take-home pay over a year, for FHBs by -$5033 over a year. While bank lending criteria will show that almost all households could absorb these increases, they will have an outsized impact on retail sales and other discretionary spending.

And that is only part of it. Low migration and still-strong house building suggests we will arrive at an over-built situation soon. Some urban areas are already at that point (Auckland? Wellington?) with others (Christchurch?) are rapidly approaching it. Excess housing supply drives down house prices and rents. As good as that may sound, it also undermines the "wealth effect", something that encourages homeowners to spend.

In a year, most of us will look back on current interest rates as 'low'.

Daily swap rates

Select chart tabs

21 Comments

Retail Banks have already priced in 150 basis points of tightening over the next 18 months. So I'd say the cheapest 1 year rate you could get in late 2027 will be 6% or thereabouts.

The market tailed into 5% US30Y yesterday, the pressure everywhere is up

That said I think consumers everywhere are very weak, and

it's like trying to fly a heavy jet, at just above stall speed, close to the ground.....

I wonder if they will head the other way later in the year. The market had priced in the RBNZ raising the OCR, first of all because they thought the economy would start growing, and now because fuel prices have caused inflation. My guess is by the end of the year 91 fuel prices will be back around $2.50l, the economy will still be in a rut, and the OCR will be at a similar level to now. That is a total guess of course, but a scenario I haven't heard anyone else hypothesise.

I don't know where the OCR will go. If forced, I would suggest 1 or 2 small hikes at most this year. then pause.

But I really don't think there will be 5 or 6 hikes.

Why?

By the 4th hike, our economy would be in a deep recession. The futility of raising the OCR further to quell a primarily supply-side inflation issue will be apparent.

We'd have unemplyment above 7%. Financial stability, a key objective of the RBNZ, would be under threat.

In response to your guesses, my guess for year end would be:

- 91 at circa $3

- OCR at 2.5%

- Economy in a slightly worse state than now

I don't think there is any reason at the moment to think that fuel prices will spiral unless the war escalates. Hopefully it will be a one off hit to fuel prices that will then cause a one off hit to other prices. In theory the RBNZ may look through that. So yes your scenario is quite plausible.

We also heard this view a few years ago when people said the world would end if the OCR went above 5%. Claimed that this was an impossible outcome because the housing market would tank and a depression would happen.

Well guess what? The OCR went above 5% and we all survived (mostly...although I'm sure there were a few that didn't...but they were probably the ones telling people on here to 'be quick' and by a house at the time...ie the greedy and overleveraged).

But the starting point is far, far different. Don't you think?

ie. the economic was very hot before the hiking started in 2021.

this time it is very weak

this is a critical difference

The economic was very hot before the hiking started in 2021.

Yes both record GOVT stimulus ie our per per capita debt went up 108% and crazy OCR setting and almost free money for banks to lend off RBNZ. After all this stimulation it was not just very hot it was BUZZING. ie time to sell certain "assets", they really sold themselves.

This time it is very weak.

It is very weak, the GOVT is now saddled with the debt from above. No stimulation happening, no willingness to and painting Labour is the only party of Lolly scramble elections. No fiscal stim here....

So with a GOVT not willing to spend you need consumers to spent to get you out of a rut. They not only feel not too flash, they are feeling poorer as well, In most cases (almost anyone owning a home) you are. Houses are 15% off peak in latest HPI, many are much worse than this, and in the middle/top end of town.

Normally at this point the pretty low OCR would have produced a wave of real estate purchases, but interestingly , it has not even with these 15% falls, buyers want lower prices and seem on strike as listings grow. Can't say RBNZ did not try to relight the Ponzi, but now they have a very nasty non-white blackish looking Swan Not seen or planned for by anyone (you know) certain war in the middle east. Black swan = Confidence is very weak, caution seems the most prudent act.

Even with this background, financial markets say two hikes fully priced in.

The OCR will be 1.75% or lower by mid 2028

Where does that predict HPI average house prices are?

- another 15-25%? that's a very low OCR at 1.75%, NZ would need to be bleeding out economically, ?

if thats our future perhaps ocr is even lower, i suggest if we fall below 2 we going 0 to negative here.

Markets have come to accept that the monetary authorities will have little alternative than to hike rates to keep inflation in check.

That is especially true in New Zealand where the current Government removed the dual mandate that required the Reserve Bank (RBNZ) to consider the effect on the labour market. Now their sole mandate is inflation control. And RBNZ Governor Anna Breman committed to being "laser-focused on inflation" when she was appointed by the Minister of Finance.

Yes their sole mandate is inflation. But they are not compelled to hike the OCR to try and quell inflation. hiking the OCR is not a mandate.

If hiking the OCR will have little effect on quelling inflation (because it is mostly supply-driven), why hike the OCR? The OCR is a demand-side tool, demand is already sickly.

Further, their inflation mandate is focused on the medium term.

Why repeatedly hike the OCR, for limited gain and very significant cost, for an inflation issue that is potentially short term?

If hiking the OCR will have little effect on quelling inflation (because it is mostly supply-driven), why hike the OCR?

Because supply side inflation always sneaks into domestic cost push...

But surely in this environment - a weak economy with weak demand - there will be limits to how much prices can be raised. at least for discretionary spend. We aren't in the typical inflationary environment, where the economy is overheating. Quite the opposite.

Businesses will be limited in the extent to which they can raise prices. Because if they raise prices, already weak demand will fall further away.

It might be different for essential - non-discretionary - goods and services. Like groceries. Yet, hiking the OCR is hardly going to help such inflation.

But also what you are saying is that the OCR is useless for stagflation. Shouldn't the RBNZ have another tool up their sleeve?

yes exactly. Completely useless.

Many NZ business simply quote the higher price and if the client does not accept the price the work does not occur.

this factor does not limit inflation, rather it limits economic growth to get us out of a rut.....prices could go up and up as the economy goes down the crapper, and nothing gets done. As economy falls NZD falls, and local prices go up even further. At some point OCR rates have to go up to Protect NZD

I don't think people understand stagflation yet. Assume growth and inflation go hand in hand. ie not that you can have high inflation and zero or negative growth. ie they think recession/poor growth only happens when deflation occurs. (confirmation and recency bias of the past few recessionary cycles).

It might be a surprise when they see that if you let inflation go untamed, that growth keeps getting worse and worse, until you get it back under control. Just as if you let deflation get out of hand...

Hence the views of 'let just let this inflation run hot for a while and let it fix itself by doing nothing - so we can avoid a recession that will definitely occur if we raise rates' - not seeing that a ripper of a recession will also happen if we don't get inflation under control! Once it becomes embedded, its a feedback loop that is harder and harder to stop. Needs to be nipped in the bud asap to prevent future pain. As the future pain will be greater than earlier present pain, if addressed immediately.

Rather it is the disconnect between 'growth' and return....if there is no growth there is no return....or debt deflation if you prefer

As Keynes noted ....in the end we are all dead.

We just spent 3 decades dropping interest rates because we were importing cheap goods from (slave..?) labour in Asia that was recorded in our CPI.

ie we imported cheap stuff and the RBNZ's response was to drop the OCR. We didn't just do that for a few months...we've basically done that now for 2-3 decades.

But now that we import something that puts the CPI up, we ignore the OCR as a tool to keep inflation steady?

Its extremely two faced logic.

Its like we only want to use the OCR to drop interest rates (so we can create more mortgage debt and raise house prices....), but never to use it to raise rates and prevent the erosion of the value of the dollar (thus reducing purchasing power and living standards of the country as a whole...ie that is what happens when the central bank allows inflation to run hot). The bias is quite extraordinary.

The difference is that fuel price rises will hopefully be temporary. Likewise if a price went down temporarily (e.g. China dumped a shipment of cheap TVs into the market), I wouldn't expect the RBNZ to drop the OCR either. The focus is the medium term, which means they need to perform some black magic and guess work and cross their fingers.

Temporary yes, but almost certainly to average over $100 a barrel for the remainder of the year, and still elevated well above the $70 mark of recent times, for all of 2028. So a fair chunk of the high-cost fuel saveloy to go...

Central Banks around the world aren't on top of their game.

How can mortgage owners and businesses plan with rates going up and down like a Yoyo. I'm a bit over the rollercoaster

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.