Unusually, there appears to be more action in the bond market than currency markets overnight.

After tracking sideways during the Asian session, US Treasury rates have shown a steady decline since the US open.

The 2-year rate is down 3bps to 0.81% and the 10-year rate is down 7bps to 1.56%. While the 2-year rate is still a few bps above the pre-Yellen, pre-Fischer weekend comments, the 10-year rate has retraced the entire sell-off.

The only data releases of note were US personal income and spending data, along with the PCE deflators. They were in line with expectations, consistent with the view that consumer spending remains solid and Q3 GDP is set to rebound, after sluggish readings over the past few quarters. While annual core PCE inflation was a touch higher than expected, the monthly figure was in line and the data show a stabilisation of inflation pressures over the past few months.

While that data likely had little impact on the market, the more likely explanation for the rates move is that the market simply over-reacted to Fischer’s comments on Friday. While he was obviously keeping alive the possibility of a September rate hike and two possible hikes this year, ultimately it comes down to the data over coming weeks and months. However, this isn’t an entirely satisfactory explanation, as the USD has managed to hold its ground, following the surge after Fischer’s comments.

The San Francisco Fed released a research paper which was consistent with the St Louis Fed’s Bullard view that the neutral policy rate had fallen. The implication is that the process of normalising the Fed Funds rate may end up being more gradual. It’s certainly consistent with the view that the low interest rate environment could be the new norm.

Yesterday local interest rates rose, following the US moves over the previous session, but the increases were fairly modest given that backdrop.

The 2-year swap rate rose by just 0.5bp to 1.97% while the 10-year rate was up 3bps to 2.42%. The bill futures strip showed implied increases in yields of 1-2bps.

The prospect of tighter US monetary policy over the near term and the weaker NZD provides the RBNZ a little breathing space – we’d emphasis the word ‘little’, as on a TWI basis the NZD remains above the level seen at the beginning of last week, despite the increased prospect of tighter US monetary policy.

Daily swap rates

Select chart tabs

Jason Wong is on the BNZ Research team. All its research is available here.

1 Comments

The only data releases of note were US personal income and spending data, along with the PCE deflators. They were in line with expectations, consistent with the view that consumer spending remains solid and Q3 GDP is set to rebound, after sluggish readings over the past few quarters.

Hmmmm -

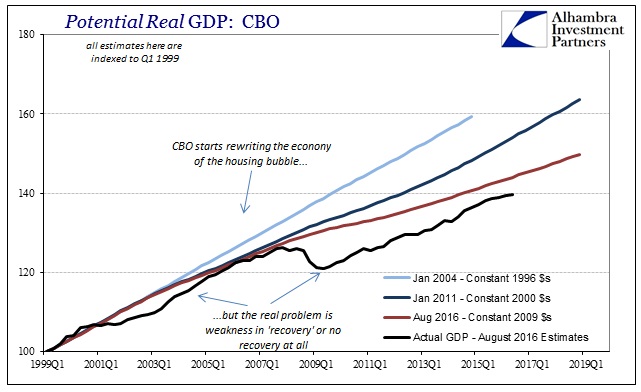

The CBO, as the Fed and any other orthodox institution, still hasn’t calculated where this will all end – because it hasn’t. In the August 2015 update to real GDP potential, the CBO actually upgraded ever so slightly its trajectory from the January 2015 set reflecting the ideas of “full employment” and final liftoff including, finally, inflation (the frame of reference for all of this in orthodox terms). Though it wasn’t anything like what potential was supposed to be especially as compared to the January 2004 math, it was at least thought an end to the almost constant downgrades to it. View graphic detail and article

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.