Reserve Bank (RBNZ) Governor Adrian Orr says Wednesday’s 25 basis points Official Cash Rate (OCR) rise will cost the average mortgage holder an extra $825 a year, or $16 a week.

Orr mentioned the figures when he appeared before Parliament’s Finance and Expenditure Committee on Thursday to talk about the Bank’s latest Monetary Policy Statement.

“Many things are hidden among the average,” he noted.

“There will be people who have significant equity in their homes, because they’ve been there for a very long time, so their wealth has gone up considerably. There will be people who are very recent buyers and will have a very high level of debt relative to their income and they will find that additional cost harder. So there are unders and overs.”

The other point worth noting is that the OCR has already gone up 75 points since the RBNZ started tightening monetary policy, and is expected to continue on a steady path up.

Financial markets have also priced in hikes ahead of the RBNZ lifting the OCR.

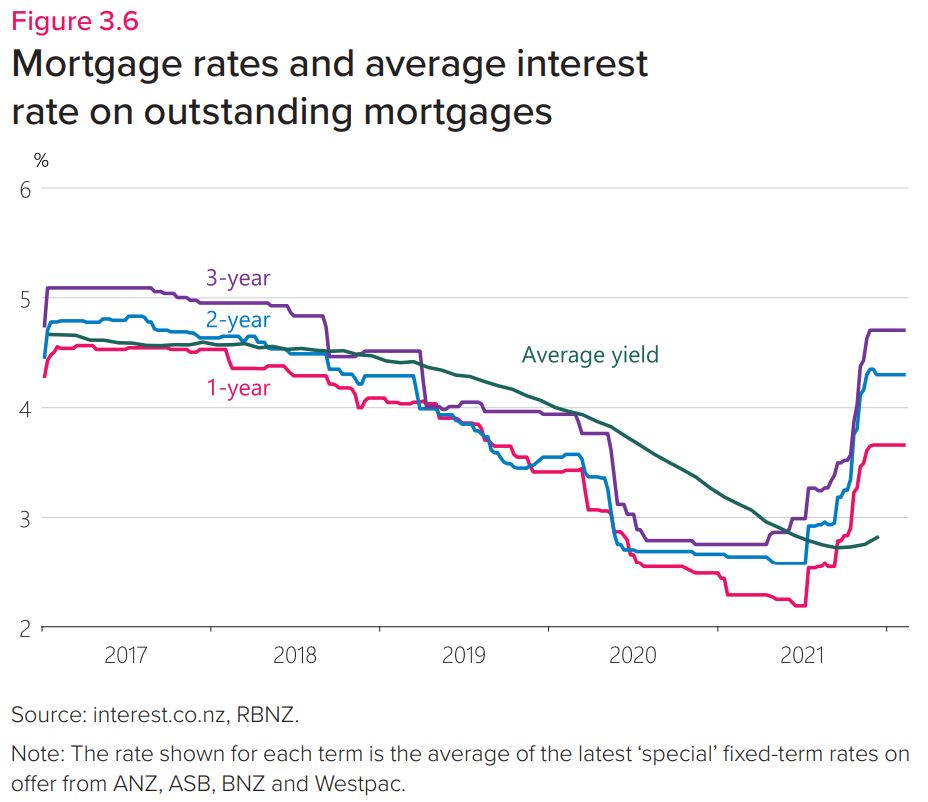

Someone with a $200,000 mortgage, paying the average two-year fixed rate a year ago (2.53%), would’ve had monthly repayments of $793. Meanwhile someone paying the average two-year fixed rate today (4.20%), will be paying $978 a month. That’s $2,200 more a year.

Meanwhile someone with a $600,000 mortgage would’ve had monthly repayments of $2,380 a year ago, versus $2,934 today. That’s $6,648 more a year.

The RBNZ, in its Monetary Policy Statement, further discussed the impact rising interest rates are having on mortgage holders.

“Relatively small upward movements in mortgage rates since November 2021 suggest most of the pass-through of higher wholesale rates happened before the November Statement,” it said.

“The two-year interest rate swap rate increased nearly 100 basis points between the October Review and the November Statement, and this move was reflected in mortgage rates before the November announcement.

“Increases in the OCR will be passed through to the economy further as more fixed-term mortgages come due to reprice, and will do so at higher rates.

“Over half of total mortgage debt is due for repricing during 2022.

“Additionally, in the past few months more borrowers have been fixing at terms longer than one year. This means they will face even higher interest rates than if they re-fixed at the same term, as the two-year and three-year rates have increased by around 20-30 basis points more than other shorter-term rates since October 2021.

“Although mortgage rates are rising, they are still low relative to their longer-term history.”

Mortgage holders had a good run…

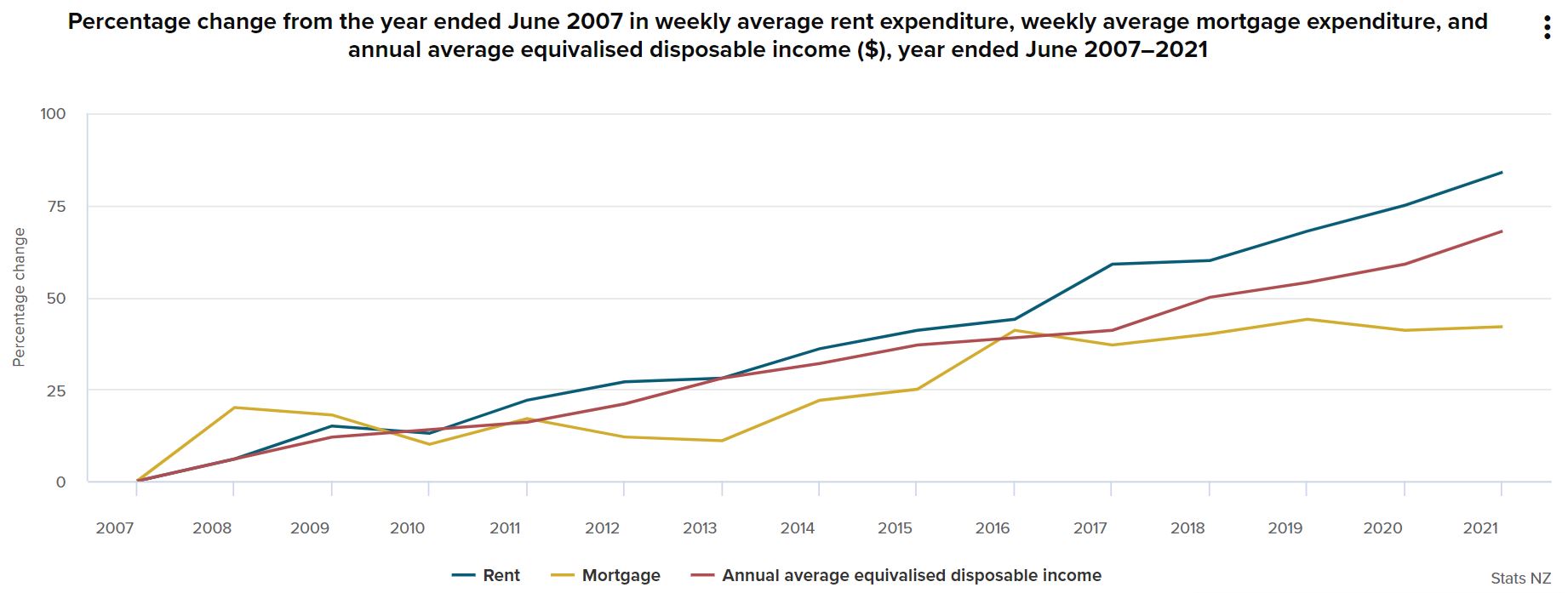

Figures released by Statistics New Zealand on Thursday illustrate how low rates mean mortgage holders have been in a much better position than renters (on aggregate) in recent years.

It noted that between June 2007 and June 2021, the average weekly rental cost rose 84%.

This increased faster than household disposable income, which increased 68% over the same period.

Stats NZ said households that had mortgages during the same period would have experienced, on average, a 43% increase.

"Mortgage payments have been relatively unchanged since year ended June 2016 (up 0.9%)," it said.

"This is due to lowering interest rates and principal expenditure increasing, through the purchase of additional mortgages or borrowing more due to rising house prices. Lowering interest rate payments offset increasing principal payments, resulting in a flat trend."

Stats NZ also said that in the year ended June 2021, 17% of New Zealand households spent more than 40% of their disposable income (not equivalised) on housing costs.

Renters were over-represented in these figures, with over one in four renters compared to one in nine homeowners spending more than 40% of their disposable income on housing costs.

52 Comments

It doesn't sound like it'll be mortgage repayments, but general inflation, that'll cripple families budgets if CPI is allowed to run wild by keeping the OCR low.

Huge assumption that increasing the OCR will make any difference to the prices of things that families buy. Increasing the OCR will reduce disposable incomes whilst international factors continue to push prices up. It is that combination that will cripple family budgets.

As household budgets tighten, homeowners will prove resourceful enough to hold onto their abodes.

Many homeowners have fought hard to get a home - and they’ll fight even harder to keep it. A tight labour market will provide support.

Despite COVID, Ukraine, inflation and so forth, the NZ housing market will remain resilient - more so than the doom goblins here dare contemplate.

TTP

I challenge TinkerThePrice to put hard numbers on what "resilient" actually means. Max price drop of what?

“DOOM GOBLIN”?

😆

Oh TTP, how you make me chuckle. What are doom goblins? Do they lurk in tree roots or caves? Do they clean houses while you sleep? Or are they just people who are worried about high debt levels?

You know goblincore is a thing now right? Doom Goblin could be the next iteration, or maybe a metal band?

Welcome back, Gingerninja, always good to hear from you.

Trust all's well in Wellington....... Not so many doom goblins lurking there, I hear.

Salutations,

TTP

P.S. You can think of doom goblins as being the inner-circle of the DGM.

Doom Goblin Movement

Doom Goblin Movement? Where do I sign up Nzdan?

TTP. Welcome back? I’ve been here the whole time good sir! I just haven’t commented. I have to be disciplined about time spent online because whilst it’s all highly amusing still it’s also a massive time suck.

I still absolutely love Wellington, yes! We’ve more or less completed the first stage of our massive reno but decided to postpone the next major phase. We spent a fortune getting Resource Consent (major neighbour nimby issue) and then the government just announced the new legislation meaning we don’t even need the Resource Consent for what we originally wanted. So we decided to wait. Plus hopefully, as the housing market slows a little, there will be less craziness with tradie schedules and supplies. I’d rather be patient and have less stresses. My builder has been flat out on other projects and he knows I’m not in a huge hurry. I’m happy for him to make hay while the sun shines and then commit to my project once things slow down a bit.

The human excrement being flushed down the storm water by “protestors” and other “protest” shenanigans has tarnished the usual chilled vibes of Wellington somewhat recently.

I had come to believe that Kiwi’s were a rather sensible, pragmatic and rational bunch, immune to the hysteria and delusional movements of other countries, so it’s been disheartening to see the rot set in here. We see/hear or smell the protest regularly in our day to day lives. There was a woman (an ex nurse no less) ranting about how the vaccine turned blood black and how spiked proteins in her husbands vaccine had somehow poisoned her sheep. So she killed her sheep. She was rabidly delusional. One of our office colleagues was assaulted and pushed to the ground in the street (just walking to work) for wearing masks and told they were doing it for their “freedom”. It’s not something I expected to see here.

I read Jenèe’s excellent article recently about her experience of the protest, and I did empathise.

What have you been up to? Still trolling the property bears i see?

There isn't going to be a tight labour market for much longer.

Higher OCR -> stronger currency -> cheaper imports.

WAY too simplistic when global events - now including war - have a much bigger influence on our inflation than us tinkering with the OCR

The OCR will still have the same influence, even if it is lost in the noise of larger powers. For sure if we don't raise it appropriately, inflation will get even higher than otherwise.

If we increase the OCR so our currency gets ~1% stronger, oil and other internationally priced commodities get ~1% cheaper. Not enough to counteract the recent price rises, but no reason to give up all hope and surrender.

Maybe mfd? Although, a lot of other countries look to be tightening too, so that effect may be nullified. And with global supply chain disruption extant, imports are likely to continue to carry the additional expense of us being so far away and expensive to ship to, with resulting delays and shortages driving up locals prices.

I think we have to keep hiking just to stay in line. For FX traders, $NZ is an optimistic, risk-off trade. With markets tanking, global inflation and geopolitical threats, the natural move for the $NZ is plummeting downwards.

And like you say, we have structural vulnerability to inflation. We're utterly petrol-dependent without producing any of our own, for a start.

I’m hedging across a few currencies. I wish I could say I had any clue what will happen and it’s an overused phrase, but this shit is unprecedented.

The interconnectedness of the global supply chain, plus social media has impacted economic behaviour in a way that we just don’t have good long term data on.

Even little factors like the giant pension obligation are relatively new in human economic history. Let alone the shadow banking or asset bubbles.

I most often lean towards Ray Dalio being roughly correct about the Long Term Debt cycle. We will see a lot of currencies cease to exist over the next decade or so. My guess is that with the constant sophistication of online scams and theft, governments will eventually all introduce their own crypto currencies (for secure online banking purposes and to make tax oversight easier), and they will use that opportunity to reset currencies. It might even be similar to when they ditched the gold standard, where we are forced to exchange our existing currencies at a shitty exchange rate. It seems likely to me that the global currency system will require some form of big overhaul at some point. The sheer level of outstanding debt doesn’t seem repayable.

'This shit is unprecedented'.

Haha, love it. Welcome back from your self imposed commenting exile, that was a lot longer than mine, haha.

The will intro their own digital currency, but for control reasons. Ability to freeze, deduct, direct, control spending type and limit how you use you 'bank account'. Social credit scores and the like.

That doesn't nullify the effect. It may mean that we're just holding the line on inflation rather than actually bringing it down, but rising the OCR will mean that inflation in the future will be lower than if we fail to raise the OCR.

I agree that it's unlikely to be sufficient to bring inflation in line, but it is necessary. We will also have to wait for commodities and supply chains to settle down to finish the job.

Well, it’s a flippin complex set of factors. FX is only one. It’s been a powerful one for NZD over the last 15 years or so whilst NZ has had a relatively higher OCR to other countries (and all the post-GFC deflationary factors effecting other currencies and making NZD a sexier FX trade) but there are other powerful forces at work now.

For instance, the money supply is still increasing, if that money isn’t going into asset bubbles (particularly housing in NZ) then it’s going to continue to be inflationary for everything else surely?

I'm not saying the OCR is the cause of high inflation, but our exchange rate (controlled by the OCR) is one of the few levers we can pull to actually impact inflation, and we should be pulling it right now. This may also have the happy outcome of making our house prices more sensible.

Agreed.

Would have marginal effect if house prices half the price of where they currently are. Higher house prices less wiggle room anywhere else

Slowest moving train wreck there is... But a train wreck nonetheless.

Sorry, Sendatsu, there's no such thing as a slow wreck or crash.

What you contribute here today suggests that your cognitive processes have become corrupted. ☹️

You need to carry out a salvage operation on yourself.

TTP

Presumably the learned members of the finance and expenditure committee realise that RBNZ raise the interest rate precisely because they want to reduce disposable income, to reduce demand in the economy, and increase unemployment... solemnly hoping that the resultant reduction in economic activity in NZ will bring prices down?

Nevermind that the drivers of inflation are on the supply side. Donkeys.

I agree Jfoe. Seems we are very much in the minority.

Why are you so confident that the inflation is supply-side driven?

We have a housing bubble that has pumped billions of borrowed money into the economy. A lot of that is chasing the same things- building materials and builders, yachts, SUVs, outdoor pizza ovens... it's "the wealth effect", you know. If you believe it's real, then you surely believe it's inflationary too. Or else it isn't real, and lowering rates does nothing to stimulate.

I agree, demand side has certainly been critical. But I think with all the actions taken, including the CCCFA and OCR increases, those demand side pressures have been subsiding for some months.

My view is that the demand side has been nearly dealt to- another 50 BPs of OCR hikes and it would have been dealt to for sure.

Then we are mainly left with supply side inflation, which OCR raises will have minimal impact on.

I agree that the local demand-side inflation can and will be dealt to pretty quickly this year, in the form of a rapidly cooling housing market. Another 50bp to mortgage rates probably would do it; 1% certainly would.

My thesis is that the role of supply chains in global inflation is overstated too, and more of the inflation has come from the same 'wealth effect' bubble. In the case of the US, it's both real estate and even more so, a massively pumped equities market, as well as the the fiscal stimulus which caused a large, irregular demand bump. So we'll continue to see imported inflation until they have an equities and real estate bust of their own. On top of which, energy inflation is a secular trend which will only be exacerbated by the Ukraine invasion; and it's one we're particularly vulnerable to.

I think 2022 will be our 2008; the year we realise we've been living in an economic dream and ignoring every gathering storm cloud. I'm quite, quite confident that there will be no 'labour shortage' by the end of the year.

Good post. Agree.

I actually think the demand-side pressures are close to dead now. Especially now that omicron is whacking us.

Another 50 BPs and demand side should well and truly be tamed.

yup supply of money

singalong with RBNZ,dont worry,be happy.a hit in 1988!

Hmmm I wonder who's created this mess...

I don't know man, not me.

Figures released by Statistics New Zealand on Thursday illustrate how low rates mean mortgage holders have been in a much better position than renters (on aggregate) in recent years.

It's all about choice for many. Houses are always cheaper yesterday- there's a real cost behind trying to time the market and those who think they're smarter pays the price.

There is only so far OCR can rise before the economy gives- make the bet accordingly.

And if the economy gives, house prices keep going up eh?! (because I’m the past we had deflationary forces and falling interest rates…now we have the opposite)

Clown world is a bit slow on the uptake.

Houses were more expensive yesterday.

Pure real estate agent speak. You forgot to close your statement with the usual "be quick" exhortation.

I really don't get how you could possibly say that is a matter of choice.

The housing problem is just about that, the possibility of choice (for almost every non owner) has been removed.

You can't "choose" to have 200k for a deposit, man!

Also, remember, home owneship is going down. so home owners count less in election day.

You might have 10 houses or 100, and I might have 0, but in front of the electoral piece of paper your vote and my vote have the same value.

I will anticipate your thinking by only saying that I am in the top 2% earners in NZ, so yeah in my case (but I appreciate that I am an exception) is a matter of choice. But what you are saying is to be considered pretty offensive for many people.

Be quick! <= this is offensive, most people cannot be quick or late, they can or can't

Best time is yesterday! <= yesterday I was busy trying to find the money to pay my landlord

Houses go up, only up <= oh thanks, just what I needed

Do you get it?

Well people could always just choose to save $200k......Just like they could have chosen to be born a little earlier, chosen who their parents are, made the choice on behalf of the employer(s) that rejected their job application for an opportunity at starting a prosperous career. People could always choose not to take out student loans for qualifications, they could choose how much rent their landlord charges them per week for the privilege of having a place to sleep within an hour of their workplace.

It's funny how CWBW talks about choices from his Ivory Tower of success. Personally, I don't look down my nose at others from my tower.

There's nothing much to brag about in being born far earlier and receiving affordable housing supply from previous generations either.

I think that was Nzdan point exactly :)

Side note - where are you finding stats specific enough to identify top 2% income?

> 200k (govt claimed that new tax changes were to hit >180k was about 2% of population), so I guess I am in that set

Thanks, fair enough assumption. It seems that tax band is hitting 50% more people than they'd expected.

This is all media spin by RBNZ. The need of the day was go quick, go hard and fix this mess. 91 petrol will be above $3 today and inflation will come at 7% for this quarter. But RBNZ governer will still keep his job when he has failed to do his main job for last 3 quarters.

If i don't perform on my work, i loose it. If i don't perform in my business, it closes. But RBNZ not performing in their job but no one talks about it or even asks them the question on why not?

Total anarchy

I agree 100%. This lack of accountability is incredible. And now Orr is pretending that inflation happened by magic and that his own ultra-loose reckless and unsustainable monetary policies did not play a big part in this mess.

He's totally out of control, and the RBNZ is a mess.

He should have been sacked.

$825 a year is peanuts in comparison to weekly average rent $600 or capital gains made by multiple property owners median $4,20,000 as per last December property sale.

Lots of noise & expectation, zero impact.

Except it's a lot more than that for those getting new - thus larger - mortgages.

And those new mortgages are for the purchasers of property that is on the market now.

So buyers can't borrow as much (except for the small number who don't need a mortgage).

Market prices are set by the most recent transactions. What existing mortgage holders will pay is less relevant to price than what new mortgage holders will have to pay.

100% correct in my opinion.

The "new" house prices will be in function of how much will be granted to the "new" home buyers.

ocr go down => people can borrow more => assets cost more

ocr go up => people can borrow less => assets cost less

The fatigue of current debtors is always much more biased by inertial forces, it matters much less.

The new ones make the market (mostly)

If you own a home and need at as a place live you can't realize the any capital gain, it doesn't go into your bank account you can't spend it on food, its totally meaningless.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.