The Government is proposing to regulate interchange fees, typically the largest component of merchant service fees charged by banks to business customers for accepting card payments, through "hard caps" priced for a range of different types of merchants.

Additionally the Government is mulling a range of other options to force down merchant service fees. These include price regulation of the entire merchant service fee, of card fees for consumers, and of buy now pay later merchant fees. These prices could be regulated directly or be subject to principles based tests.

These are some of the key proposals and options aired in a Ministry of Business, Innovation & Employment (MBIE) issues paper released on Thursday. (There's also a merchant service fees summary from the Government here).

Commerce and Consumer Affairs Minister David Clark and Small Business Minister Stuart Nash say the Government is pushing ahead with regulation of merchant service fees on debit and credit cards to make them fairer and less of a burden for Kiwis and businesses. Doing so was a Labour Party election promise.

For small and medium sized businesses (SMEs) card acceptance fees can be the third highest cost of doing business after wages and rent. The idea is that reducing these fees should flow through to consumers, thus providing some stimulation to a COVID-19 hit economy with small businesses said to generate 28% of New Zealand’s Gross Domestic Product and employ more than 600,000 people.

"Interchange fees for open party credit and debit schemes (Mastercard and Visa) will be regulated with hard caps. The hard caps for each transaction type will be set applying principles linked to the objectives outlined in chapter 5 [see below] and may be targeted for different classes of merchants," the issues paper proposes.

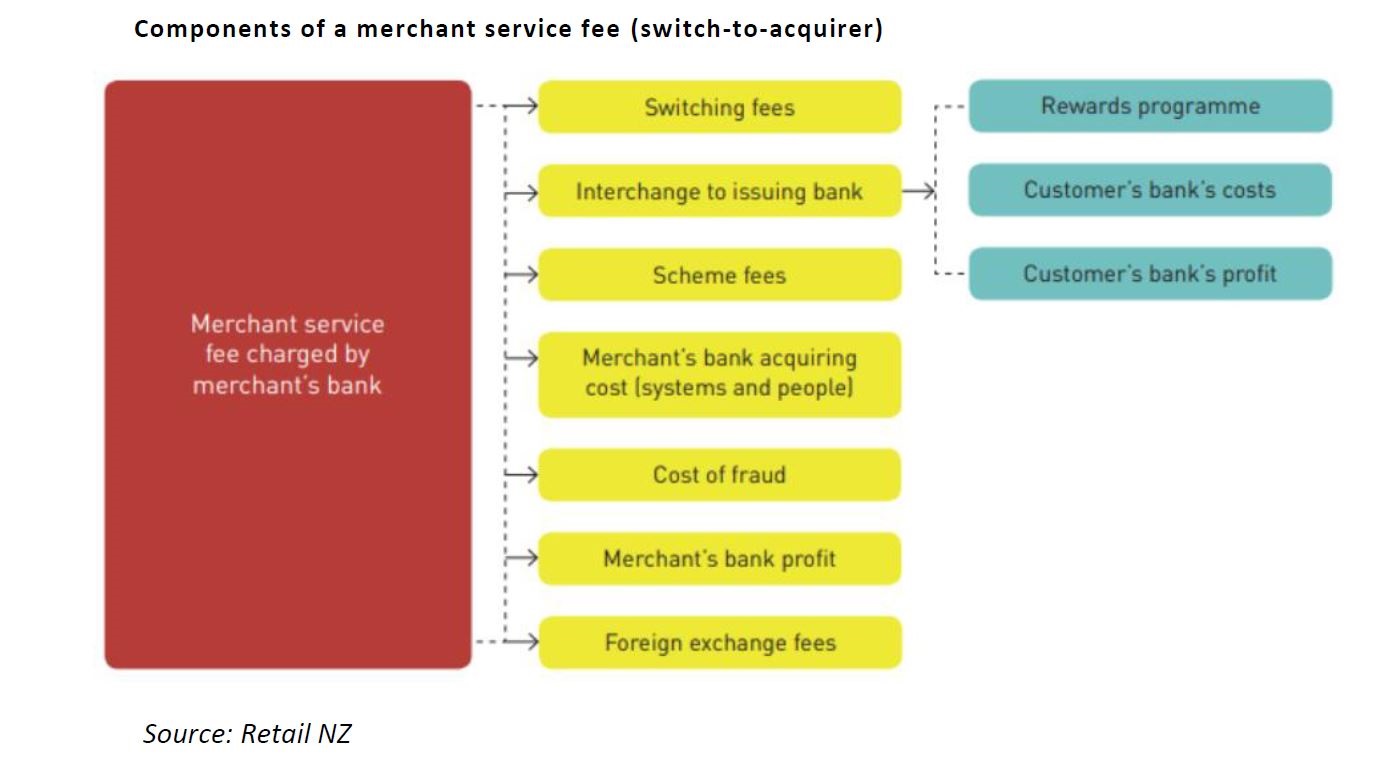

Interchange is a fee charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. Each bank sets its own rates within a cap set by Visa and Mastercard.

The interchange fee is the biggest component of the merchant service fee, especially in credit card transactions where it can be 70% to 80% of the total merchant service fee, MBIE says. It's typically set as a percentage of the transaction value. The fee is the charge payable by the merchant’s bank to the consumer’s bank to recoup the costs of processing payments, a profit margin, and in the case of credit card transactions, an additional margin to fund inducements or rewards such as Airpoints for customers and the credit supplied.

MBIE has monitored interchange fees since 2017, estimating weighted average credit and debit interchange fees have fallen since then by about 11%.

"There have been positive moves from the banks on merchant service fees for contactless debit card merchant service fees. Recently many of the banks have announced that merchants will not be charged more than 0.7% [of the purchase payment] to process contactless debit card transactions. This will be a reduction for some smaller merchants from merchant service fees that were previously close to 3%," MBIE says.

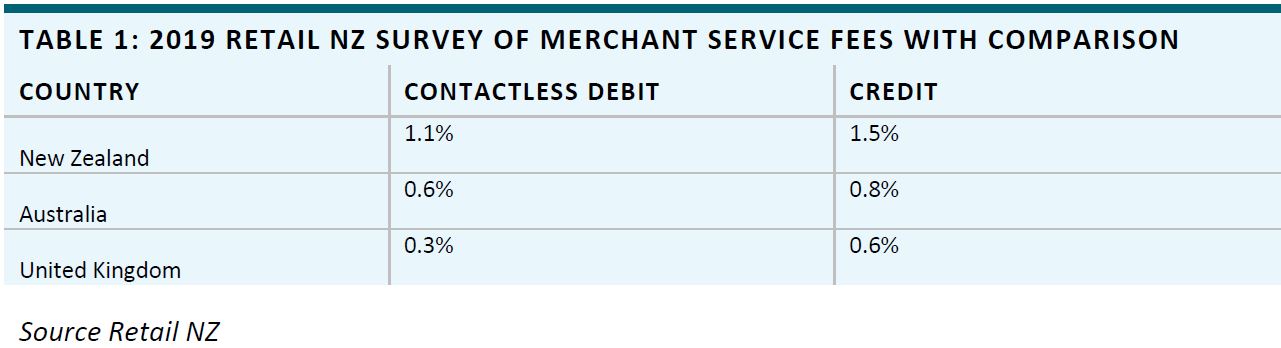

Nonetheless Nash says NZ businesses pay higher merchant service fees than their counterparts in comparable countries such as Australia.

“New Zealand retailers pay more than other countries, costing businesses on average $13,000 more per year than their Australian counterparts,” Nash says.

“Because small businesses are so heavily reliant on credit and debit card transactions, they are at the mercy of the banks when it comes to receiving payments for goods and services."

'It isn't fair'

Nash told media it isn't fair that big retail chains can negotiate with banks over their merchant service fees whilst SMEs "have no rights whatsoever" and must take the pricing they're given. Nash cited "market failure," saying NZ banks, among the world's most profitable, had the opportunity to reduce fees but hadn't.

Fees free EFTPOS has been losing market share to contactless debit and credit cards favoured by consumers but which charge fees to businesses. The Government says in many cases consumers are ultimately picking up the tab, as retailers pass on these costs through higher prices for goods and services.

"We just don't think the banks are playing their part, hence the reason we have stepped in to ensure that in fact our retailers and New Zealand's consumers get a fair go," Nash says.

The MBIE paper notes that interchange fee regulation is merely one aspect of retail payments system regulation. Evaluations of overseas approaches, where retail payments are already regulated, shows the importance of taking a "systems approach" to retail payments system regulation, MBIE says.

Thus regulation needs to also include some of the following types options to supplement interchange fee regulation, MBIE says.

a. Other price regulation: Other aspects of the retail payments system could be covered by price regulation, for example the whole merchant service fee, card fees for consumers, or other product types (e.g. online payment gateways, ‘Buy Now, Pay Later’ merchant fees). These charges could be regulated directly or subject to principle-based tests. For example,

i. on the merchant-side, they could be subject to a requirement that fees charged to merchants must be closely connected to the activity for which the fee is charged and not unreasonable, or the regulator could have the ability to regulate other aspects of the merchant service fee if they increase in response to interchange fee regulation.

ii. on the issuer-side, they could be subject to a test of no ‘net compensation’ from a scheme, similar to the Australian regime.

b. Information disclosure: A requirement for acquirers to disclose information to a regulator or the public on the merchant service fees they are charging merchants. This could be used to provide merchants an understanding of the levels of merchant service fees that they should be paying and/or monitor merchant service fees in more depth.

c. Collective bargaining: Options to enable collective bargaining by groups of merchants with acquirers and other payments providers may increase the power of merchants when bargaining. For example, Retail NZ has negotiated rates with one of the banks for processing card transactions, which is available for all of its participating members. However, it appears to have had limited uptake.

d. Other options could include:

i. Codifying rules and practices that would support greater transparency and incentives in the system. This could include rules around cross border acquirers, changes to surcharging and steering allowed by merchants, limiting the extent of rewards and loyalty schemes, prohibiting of bundling of certain services (e.g. acquirers not offering other services to merchants), facilitating access for competing payment methods or providers, or encouraging least-cost routing for transactions.

ii. Requiring merchants to surcharge for particular higher cost payment methods or requiring discounts for customers that transact using lower cost payment methods. This would avoid consumers paying with lower cost options subsiding customers that pay with higher cost options. However, such requirements would need to guard against excess surcharging to protect consumers.

iii. Setting requirements relating to product development and technology. This may include such things as requiring payment terminals to be able to automatically surcharge for different payment types or automatically adopt least cost routing.

The MBIE paper says the overall objective is for the retail payments system to deliver long-term benefits for end-users within New Zealand. This, MBIE says, requires that the system:

a. enables healthy competition between payment providers and payment products

b. incentivises beneficial innovation for consumers and merchants

c. is efficient in allocating resources through clear price signals, where prices are cost-reflective for the system as a whole

d. is fair in its distribution of costs, particularly in its treatment of small business and low-income consumers.

104. In addition to these objectives, it is vital that payment systems are sound, secure and subject to prudential supervision. However, we do not focus on these objectives here, as the RBNZ largely holds responsibility for these outcomes in its prudential role.

Consultation on the issues paper is open until February 19 next year, with Nash and Clark to report to Cabinet by next April.

Earlier this year interest.co.nz ran a five part series by Gareth Vaughan on retail payments fees. The headlines and links to these articles are below.

2 Comments

There is absolutely no need for a percentage based fee at all. The size of the payment has no bearing on the complexity or risk of the transaction. A flat transaction of a couple of cents should do it.

In fact, given the Govt clearly want to move away from cash entirely they should be removing all charges associated with "payment".

size counts. Contactless debit for example NZ population to Oz to UK.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.