By Gareth Vaughan

They have a business model to die for. They're the ultimate ticket clippers and, in New Zealand, are largely unregulated and pay almost no tax.

Who am I talking about? Visa and Mastercard.

Since Mastercard and Visa listed on the New York Stock Exchange in 2006 and 2008, respectively, they've been investor darlings. And even though the coronavirus pandemic sweeping the globe may reduce the volume of transactions they're able to clip the ticket on and is hitting their share prices, Visa and Mastercard operate an extraordinarily profitable business model. A recent Mauldin Economics article by Stephen McBride summarises this nicely.

"Visa and Mastercard have effectively created a universally accepted money - a 'global currency.' $13 trillion flowed through their networks last year. They make money by taking a small cut of each transaction, like a tollbooth on a highway," writes McBride.

"It hardly matters what bank you use. At the end of the day, your card likely needs Visa or Mastercard’s payment network to function."

Keep in mind that Visa and Mastercard aren't financial institutions. They don't issue credit or debit cards, lend money, or set the interest rates and fees users of their products pay. That's what their bank/financial institution partners do. In NZ bank card issuers push their contactless credit and debit cards at the expense of EFTPOS, and do very well out of Visa and Mastercard, thank you very much. There's more on this to come.

According to Statistics NZ, Kiwis made 1.881 billion electronic card transactions in 2019. And in January this year we made 158 million transactions with an average value of $50 per transaction, spending $8 billion using electronic cards.

Total credit card billings in NZ during 2019 were $48.333 billion. In January outstanding credit card balances stood at $7.321 billion, according to Reserve Bank of New Zealand data. And as of December, the weighted average interest rate on personal interest bearing loans was 17.8%.

Massive scale

Want an idea of Visa and Mastercard's scale? Then get a load of this.

Visa chairman and CEO Alfred F. Kelly, Jr, speaking at the company's recent annual general meeting, said in 2019 Visa made significant strides in advancing its goal to be in the middle of any transaction in the movement of money, both on the Visa network and beyond. In 2019 total Visa payments and cash volume topped US$11.6 trillion, driven by 202 billion Visa transactions, equating to an average of 553 million Visa transactions every day, with more than 3.4 billion cards available worldwide to be used at more than 61 million merchant locations. Of the 202 billion total transactions, 138 billion were processed by Visa, Kelly said.

Established in 1958 and incorporated in the tax haven US state of Delaware but with its headquarters in San Francisco, Visa has 19,500 employees. And it'd be fair to say it's a pretty profitable enterprise. Net revenue for 2019 rose 11.5% year-on-year to US$22.977 billion, and net income climbed 17% to US$12.080 billion, with Visa splashing out US$10.9 billion on dividends and share buybacks, a 19% increase.

Visa says net revenues consist of service revenues, data processing revenues, international transaction revenues, and other revenues minus costs incurred under client incentive arrangements. More on a key client incentive arrangement later. Visa's revenue is detailed in the diagram below.

Mastercard's also a profit machine. It's 2019 net revenue rose 13% to US$16.9 billion, with net income up 37% to US$8.1 billion. Mastercard's operating margin, derived by dividing its operating income by its net revenue, weighs in at 57%. (Visa's 2019 operating margin was even higher at 65%). Mastercard spent US$6.5 billion on share buybacks and paid US$1.3 billion in dividends. Gross dollar volume across its network rose 13% to US$6.5 trillion, and switched transactions increased 19% to 87.3 billion.

Established in 1966, Mastercard has its headquarters in Purchase, New York but is also incorporated in Delaware. It has 14,800 staff.

Embracing threats

Visa and Mastercard are adept at embracing new threats to their businesses, enabling them to clip the ticket when new payments technologies and services emerge. Visa calls this its "open partnership model."

"For more than 60 years, mutually beneficial partnerships have been fundamental to Visa’s business model. We traditionally have operated in a four-party model, facilitating transactions between issuers, acquirers, merchants and account holders. As the payment ecosystem grows, so too does Visa’s partnership model. Today, our partnerships extend to technology companies, fintechs, governments and non-governmental organizations," says Visa.

Witness the growth of buy now pay later services and moves into payments by technology behemoths such as Apple and Google. In December Latitude Financial Group, parent of GEM Finance, and Mastercard announced a strategic partnership saying customers of Latitude's buy now pay later service would be able to "buy now pay later anywhere Mastercard is accepted globally."

Laybuy, another local buy now pay later service, has done a similar deal with Mastercard. And guess whose cards the likes of Laybuy and AfterPay accept? You got it, Mastercard and Visa debit and credit cards. And remember when Apple Pay first launched in NZ? It was via ANZ-issued Visa credit and debit cards. And Google Pay? Yep, users also require a Visa card.

Cryptocurrencies are another area Visa and Mastercard are keeping tabs on, Mastercard with its own cryptocurrency team. And both were involved early with Facebook's Libra project before deciding they didn't like the cut of its jib and pulling out.

When you have Visa and Mastercard's scale, there are many willing partners and many ways to partner. For example, last July Visa said it was launching a service through which Visa card issuers such as banks, and merchants can offer customers an instalment payment option - buy now pay later - using a Visa card. Visa noted instalment payment volumes were growing twice as fast as credit card volumes.

China is proving a tough nut to crack for the two US companies. However even there some progress is being made. In early February Mastercard announced it had received in-principle approval from the People’s Bank of China to start formal preparations to set up a domestic bankcard clearing institution through a joint venture with NetsUnion Clearing Corporation. Within a year, the joint venture company will be able to apply to the People’s Bank of China for formal approval to begin domestic bankcard clearing activity, Mastercard said.

China's UnionPay International, with the scale of the Chinese market and major investment capacity behind it, has the potential to take on Visa and Mastercard globally. However, UnionPay's challenge may be suspicions in the West of Chinese technology, and what the Chinese company may do with people's data. Such fears could play into Visa and Mastercard's hands.

Interchange & 'a drug'

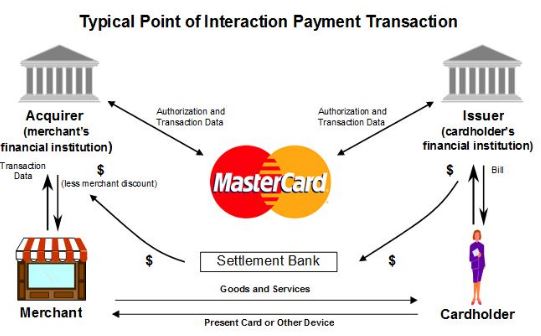

An interchange fee is a fee charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. A typical card transaction involves four parties the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

Visa and Mastercard point out interchange doesn't generate revenue for them. However it underpins and grows their networks. And it drives up costs for merchants, or retailers, and ultimately consumers too.

"Consumers get benefits from using cards - convenience, interest-free periods, rewards points - but do not face the full costs. Instead, the cost of a consumer's choice of payment is, in part or in full, borne by merchants, who pay interchange fees each time a consumer pays them using a card. In some cases these fees are used to fund reward points that are, in effect, a payment to the consumer for using the card. These fees are usually recouped through higher prices paid by all consumers. This means that financial institutions and card schemes have the opportunity and incentive to grow their networks by competing to subsidise the benefits to cardholders - at merchant's expense," the Australian Productivity Commission said in a 2018 report.

"Rewards and other benefits may be useful to expand card networks in their infancy, and thereby enhance the value of the network for all, by increasing the incentive for individuals to use cards. With mature card scheme networks and ubiquitous use in Australia and worldwide, it reflects significant market power to suggest, as the major card schemes have, that in order for them to survive, merchants should be required to pay higher fees to cross-subsidise consumer reward programs. The case for interchange fees to fund reward programs or to redistribute benefits on a transactions basis from the merchant’s bank to the customer’s bank is feeble," the Productivity Commission added.

A senior NZ banking figure, who didn't want to be named, used even blunter language. They described interchange to interest.co.nz as an outdated model to share the benefits of credit card functionality that hasn't adapted to the modern world. And the reason it hasn't adapted is because of the self interest of banks from the "sugar rush" of rewards schemes, with Visa and Mastercard the biggest ultimate winners, they said.

This source argues interchange was introduced to reflect the value created by the global payments system so the card issuer could share some of the value received from the card being used at a merchant in NZ or overseas. But this was in the days of paper when today transactions are electronic and instantaneous.

"Yet interchange levels that were maybe 120 basis points [of the transaction value] when it was all paper are now in NZ still on average 80 or 90 basis points when it's literally almost costless," they say.

A Visa NZ spokesman told interest.co.nz interchange fees play an integral part of a secure, frictionless and reliable electronic payments system that connects financial institutions to merchants and cardholders around the world.

"These fees balance incentives between financial institutions to both support and issue payment credentials to consumers and to enrol and process transactions for merchants. They also enable the benefits that all cardholders and merchants enjoy and expect - including speed, security, innovation and convenience. By balancing the economics among all participants, interchange encourages more merchants to accept electronic payments and consumers to use them," the Visa spokesman said.

Interchange is regulated in dozens of other countries, including Australia and the European Union, but not in NZ. There will be more on this, and interchange fee levels, to come.

Banks earn money through customers using Visa and Mastercard credit and debit cards at the expense of EFTPOS and are incentivised to grow this business. The domestic EFTPOS system, however, doesn't charge per-transaction fees to merchants. Rewards programmes, whilst popular with many customers, are actually a problem for NZ Inc, the senior banking source argues.

"We're all on this drug, all the providers of credit cards are on this drug called rewards which is fed by interchange. It drives transactional activity and the interchange is generally big enough to pay for the rewards cost. And then if some of those customers don't pay their [credit card] balance off they make money not just on the interchange versus rewards margin, they also make money on the credit card balance at 18% on average."

*Mastercard's "typical transaction" diagram below highlights its network supporting what's referred to as a “four-party” payments network.

Tax, or lack thereof

Given their dominance in NZ's credit and debit card markets and payments sector Visa and Mastercard must have big, profitable operations here that pay significant tax right? Wrong. Visa Worldwide (New Zealand) Ltd and Mastercard New Zealand Ltd haven't filed financial results with the Companies Office since 2014. As previously reported by interest.co.nz they no longer have to because as subsidiaries of overseas companies, they're deemed to not be big enough to be required to.

Back when the two did file annual financial results they didn't feature the sorts of numbers you'd expect. Mastercard NZ had revenue of just $4.5 million, paid tax of $71,445, and reported profit after tax of just $166,044 in 2014. Visa Worldwide (New Zealand) had revenue of $3.2 million, paid income tax of $185,664, and profit of $102,603.

Why are the two multinationals' NZ arms so small? Because the bulk of what they do here, and the subsequent revenue, is run through their respective parent companies, both domiciled in Singapore.

Visa Worldwide (New Zealand) Ltd provides "administrative, liaison and support services" in marketing and business development for Visa Worldwide Pte Ltd and Visa International Service Association's clients and business interests in NZ and the South Pacific. Its immediate parent company is Singapore's Visa Worldwide Pte Ltd. Mastercard NZ Ltd provides "liaison and marketing services" to its holding corporation and related corporations. The NZ company's immediate controlling corporation is Mastercard Asia Pacific Pte Ltd of Singapore.

Visa Worldwide Pte, described as "the company's operating hub in the Asia Pacific region," and Mastercard Asia Pacific Pte which fulfils a similar role for the Mastercard group, have eye watering revenue but pay very little tax.

The most recent financial statements available from Visa Worldwide Pte show 2018 September year revenue of US$2.9 billion, up from US$2.5 billion the previous year. Income tax expense was just US$109.291 million giving a tax rate of just 5.1% versus 5% in 2017. Profit was US$2.03 billion. Mastercard Asia/Pacific Pte's 2018 calendar year revenue weighed in at more than US$3 billion, up from US$2.5 billion in 2017. Income tax expense was a miniscule US$31.3 million, giving a tax rate of 2.2% down from 3.2% in 2017. Profit was US$1.358 billion.

The standard Singapore corporate tax rate is 17%. So why did these two global behemoths pay so little tax in Singapore? Sweetheart tax deals as Mastercard explains below.

"In connection with the expansion of the Company’s operations in the Asia Pacific, Middle East and Africa region, the Company’s subsidiary in Singapore, Mastercard Asia Pacific Pte. Ltd. (MAPPL) received an incentive grant from the Singapore Ministry of Finance in 2010. The incentive had provided MAPPL with, among other benefits, a reduced income tax rate for the 10-year period commencing January 1, 2010 on taxable income in excess of a base amount."

"The Company continued to explore business opportunities in this region, resulting in an expansion of the incentives being granted by the Ministry of Finance, including a further reduction to the income tax rate on taxable income in excess of a revised fixed base amount commencing July 1, 2011 and continuing through December 31, 2025. Without the incentive grant, MAPPL would have been subject to the statutory income tax rate on its earnings. For 2019, 2018 and 2017, the impact of the incentive grant received from the Ministry of Finance resulted in a reduction of MAPPL’s income tax liability of $300 million, or $0.29 per diluted share, $212 million, or $0.20 per diluted share, and $104 million, or $0.10 per diluted share, respectively," Mastercard says in its annual report.

The Visa NZ spokesman says the company has less than 25 staff in NZ, working in marketing and business development support roles. They work closely with Visa's global and regional teams to provide clients support on enabling innovation and security in payments, the spokesman says.

"In more than 200 countries and territories where Visa does business, including New Zealand, Visa fulfils its tax and legal obligations and complies with all applicable laws," the Visa NZ spokesman says.

Mastercard has not responded to requests for comment.

To be continued...

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

6 Comments

Through the fees they pay, retailers are effectively selling at a discount to to credit card purchasers. How about retailers giving a discount to eftpos transactions. Should be easy enough to build into the system.

Do their agreements with retailers prohibit this?

It already is for many - credit card surcharging.

from an RBNZ media release. Never knew this. "Retailers should use common-sense when it comes to cash. Businesses are not obliged to accept cash, but declining it may end up disadvantaging people who rely on its use." Suspect there'll be less use of cash right now with "infected notes" although I understand coins are worse from carrying viruses.

Nice piece Gareth, was wondering how easier for Banks, such ANZ recently to abolish their card fee. Made them $$$ the past couple of years, then suddenly not interested? - Every Bank moves in the end about profit.

Sigh, the little people pay taxes. The big corporates get away with not paying. This needs to change.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.