Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE RATE CHANGES

None to report again today.

TERM DEPOSIT/SAVINGS RATE CHANGES

In case you missed it late yesterday, ANZ raised most term deposit rates for terms to 1 year, nothing longer. That makes their new six month rate 5.00% and their new one year rate 5.50%. ASB made similar moves today. SBS Bank raised its 6 & 9 month offers, and ended its 6% one year offer. A review of the TD market is here.

FONTERRA IMPRESSES

Fonterra reported profits up +50% in their half-year review, ROE was up to 8.6%, and they declared a 10c interim dividend. They say earnings are strong despite lower NZ milk volumes and ongoing market volatility. They note success is coming from scale and their ability to shift milk to higher earning segments and products.

BROAD-BASED ECONOMIC WEAKNESS

Economic activity declined more quickly than expected in Q4-2022. Household consumption was flat, government consumption fell, investment spending fell, exports fell, imports rose. Less upbeat spending and investment highlight that demand is weakening, which is a necessary evil to get inflation back under control, notes Infometrics. If there is a 'positive' is is that nominal GDP exceeded $101 bln in Q4, the first time any quarter has breached the $100 bln level. Inflation pushed that.

A SUCCESSFUL BOND TENDER

Fifty out of 105 bids won something at the latest Treasury bond tenders. The May 2028 $200 mln attracted $680 mln in bids and went for a 4.35% yield, well below the 4.61% at the equivalent event two weeks ago. The April 2033 $150 mln got $538 mln in bids, also going for a yield of 4.35% and also down from 4.60% two weeks ago. The Mau 2051 $50 mln went for 4.60% yield, little-changed from the 4.63% two weeks ago even though it attracted $103 mln in bids. Overall $920 mln of demand went unsatisfied today.

A FAILED CARBON TENDER

Yesterday we noted the failed carbon tender where no units were allocated because no bidder fronted up with a price above the Government's [secret] reserve level. We have more on this story here. Today, secondary market trading has the price at $67.35/NZU which is probably still below yesterday's reserve.

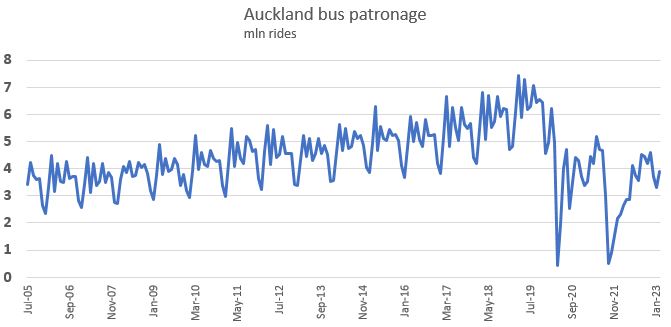

RIDERS GIVE UP ON AT

Auckland bus patronage continues to languish, undermined by WFH, cancellations, and poor service. Half fares have not rejuvenated it. You can see a long-run chart of bus ridership here, through to the end of February 2023. Auckland Transport is struggling to win back riders. Depending on the month they have lost between -2 and -5 mln rides per month from the pre-pandemic peak.

{kind=link}

AUSSIE JOBS MARKET STRENGTHENS

In Australia, their labour market came in stronger in February than expected with +64,600 extra jobs or which +75,000 were full-time positions, and part-time roles fell more than -10,000. Their jobless rate fell to 3.5% while their participation rate was unchanged at 66.6%. (NZ is 3.4% and 71.7% respectoively.)

SWAP RATES TURN BACK DOWN

Wholesale swap rates are probably slightly lower today. However, the real action in swap rates comes near the close. Our chart will record the final positions. The 90 day bank bill rate is down -8 bps at 5.01% and now only +26 bps above the current OCR. The Australian 10 year bond yield is now at 3.37% and down -9 bps from this tiem yesterday. The China 10 year bond rate is little-changed at 2.89%. And the NZ Government 10 year bond rate is now at 4.40% and down -2 bps from this this time yesterday and still well above the earlier RBNZ fix at 4.28% which was down -8 bps from yesterday. The UST 10 year is down further today at 3.49 with a -19 bps drop from this time yesterday. Any sense of calm yesterday disappeared today with the European banking wobbles.

EQUITIES LEAK VALUE

Wall Street ended its Wednesday session down -0.7% and that was a lot less of a fall than the earlier session suggested. At one point it was down a full -2.0%. Year to date it is up +1.8%. From its peak at the end of 2021 it is down -18.3%. The NZX50 is down -0.1% in late trade. This is nothing like the -1.8% mid afternoon fall on the ASX200. Tokyo has opened down 0.9%. Hong Kong has opened down -1.9%. Shanghai has opened down -0.4%.

GOLD FIRM

In early Asian trade, gold is up +US$7 from this time yesterday at US$1910/oz, although it was higher intra-day earlier.

NZD SOFTER

The Kiwi dollar is -½c lower than where we were this time yesterday, now at 61.7 USc as the greenback rises on safe-haven flows. Against the Aussie we are a little softer at 93 AUc. And against the euro we are up slightly at 58.2 euro cents. That means the TWI-5 is down to 70.2 and a -40 bps slip from yesterday.

BITCOIN LESS VOLATILE

The bitcoin price has moved little today, a second day with only a minor change, now at US$24,374 and down -1.6% from this time yesterday. Volatility has been moderate today at +/-2.8%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

65 Comments

If only God would give me a clear sign, like making some large deposit for me in a Swiss bank account!

Woody Allen

Hmm. A sign of substance...

For me it would be a meteor hitting the RBNZ building, at night when nobody was there, of course. Only a sign. For now.

Gold being at an all time high in NZD terms is worth a mention. Or should that be the NZD has been devalued to all time lows against gold? Anyway...

Yes. Powered past previous ATH last night. And something interesting happened with the Perth Mint Gold Token (tracks the market price)- the price soared by 13% at one point last night. I received an alert on my phone. Didn't stay there long.

Something else interesting with the Perth mint... couple of Chinese guys with missing fingers wanting to talk about the quality of that last shipment....

Bit of karma maybe.

https://decrypt.co/34033/chinese-firm-dumps-83-tonnes-of-fake-gold-on-t…

Less upbeat spending and investment highlight that demand is weakening, which is a necessary evil to get inflation back under control.

Nonsense. Price increases have next to nothing to do with levels of domestic demand, and crushing demand will not cause prices to come down. All we're doing is putting the economy in a tailspin because we don't have economists in Govt or the central bank with the knowledge, creativity or influence to suggest alternatives to hiking rates.

"Price increases have next to nothing to do with levels of domestic demand"

Theoretically I don't agree with this statement, then again in real life, we raised our prices by 10-20% last November, I paid close attention to sales, as I was worried these would drop… We have more sales now than back then ! Go figure ?

Exactly. Companies across the world adopted a 'price over volume' approach during 2021 and 2022 - willing to lose a bit of market share in uncertain times by increasing prices. Pepsi offset all their losses from pulling out of Russia by inching their prices up, keeping a close eye on Coca Cola market share. What did Coca Cola do? Put their prices up to match. Oil companies did the same with spectacular results. Kerching.

I would wager good money that well over 80% of our price rises in NZ are the result of higher input costs (oil and fertiliser) and increases to company margins.

So, what happens as consumer demand falls in NZ? Simple, companies will reduce their costs and supply in proportion to the reduction they see in demand. They will then hold (or even increase) prices in real terms depending on their market power.

Our central bank has no idea what is actually going on - although the recent monetary policy statement at least started to explore some of these issues (is non-tradable inflation actually domestically determined at all? what is going on with margins?)

"what happens as consumer demand falls in NZ? Simple, companies will reduce their costs and supply in proportion to the reduction they see in demand. They will then hold (or even increase) prices in real terms"

Jfoe, this sounds good but, reducing costs is a lot easier said than done, why would companies be able to reduce cost over what they're paying now? Also holding (OK) or increasing prices, is extremely difficult to do when consumer demand falls, unless the company has a monopoly like service or product.

Costs will be forced down... as per usual the businesses that offer the best produxt or service for the lowest price will win.. especially in the new world where people have less to spend .. suppliers/retailers will need to fight for business. Couple of examples...

If someone pays less for a house they can afford to take a lower salary (think new home buyers or renters after a crash) at the same time If there is higher unemployment the employer can choose to offer the unemployed or graduate person who has a cheaper house and less costs (no fam yet)... less than the mid aged leveraged equivalent. Cuts his/her costs.

In nz we have one of the worst levels of productivity in the oecd. There is a ton of scope to use tech or different processes to deskill or eliminate roles and thus reduce costs via headcount or hourly rate.

As we destroy wealth.. the employers that are smartest .. and evolve and cut costs without damaging quality will thrive and survive.. its darwinism. And lots of scope for nz to shift.

Sorry, maybe should have said reducing productive capacity rather than costs. Crude example: If you have 10 staff and three delivery vans and consumer demand drops by 20%, you can lose a van and two members of staff, right?

Right, now I get you!

Exactly, no inflation in China:

China's very weak FAI in Jan/Feb demonstrates two concerning factors: private cos aren't investing at all (private FAI up just 0.8% y/y). Also, the govt isn't doing any more this year than last year when last year it didn't near enough. Link

So much for China's highest manu PMI in a decade. Industrial Prod managed all of 2.4% y/y Jan/Feb. Actually, that low # was consistent with what the PMI really said, not what everyone said it said. Link

Central banks are trying to tame inflation by disinflation and disinflation is slowing of price growth. Now to bring prices down is a separate story in itself and is called deflation.

Price increase has everything to do with it. For simplicity lets keep it theoretical and start with there are 500 families earn $100 each day to start with and price of Apple is $20/KG and there are only 400KG of apples and every family consumes 1KG of Apples. There are a few scenarios possible

- Everyone reduces their consumption to 0.75 KG and let everyone have equal share (not going to happen due to human nature - greed, distrust etc)

- Families who want full share would either try to pay more to get 1KG.

- Seller knows that there is shortage of Apples and those who want to consume would pay more.

Now to stop the prices rise what you can do is increase Apple supply or make people pay more for other services leaving less money with family to buy Apples and thus divert the demand away by reducing spare money.

And before the skeptics jump in I know its theoretical and in practice real life is much complex but this is just a crud example.

Great example. Apples were 7% cheaper in February than a year ago. Is that because of lower domestic demand for apples? Nope - it's because the price of apples is determined primarily by import and export prices (bizarrely we import about the same number of apples as we export). If domestic demand for apples drops a bit - more apples go abroad at the market price. You can repeat this same story throughout our economy - the price of cheese, beef etc all follow international auction prices. Big input costs like oil and fertiliser are determined on global markets - but have a big impact on the cost of production here. NZ consumers are price takers of price takers.

"Big input costs like oil and fertiliser are determined on global markets" Partly true. When you take a very large player out of the market, Russia, the other fertiliser manufacturers put up their prices. In particular I wasn't aware that the EU had also banned Russian fertiliser around sep22. https://www.neweurope.eu/article/the-eus-revised-sanctions-policy-hinde… This would reduce the supply side with a commensurate increase in costs. Don't know the % world production for US fertiliser but it can't be that high if the US didn't want to screw its own farmers, not like NZ. In NZs case for fertiliser they put a 35% tariff on Russian fertiliser about six months before the EU Russian fertiliser ban, effectively banning Russian fertiliser. The US up to three months ago had no such ban. https://www.bloomberg.com/news/articles/2022-07-18/us-pulls-plug-on-fer…

bizarrely we import about the same number of apples as we export

Really?!

If you want to eat them year round you either have to store them in suspended animation or import them.

Until recently it was cheaper to ship them than store them.

They've already done enough rate hiking to slow the train enough, but they'll do another couple of hikes because they don't follow what's happening on the ground in real time, so unfortunately the train will eventually get too slow. Then what? Panic stations. Stimulus.

Yes. The economy will be in deep trouble within a few months.

That’s why I originally thought they would be cutting the OCR by year’s end.

However…. It will take time for unemployment to rise, and high inflation is likely to persist. I don’t think they can cut the OCR when inflation is high, the economy weak and unemployment still low-ish / moderate.

They will need the weak economy to realise unemployment above 5~6% and inflation to get below 4% before they can even start thinking about cutting the OCR. So that will be mid 2024 at the earliest, unless the recession gets really bad, quicker.

Apparently it'll need to go to 8% to get down there.

Fonterra up 50%. As Robert Muldoon sang out in one parliamentary interjection, “oh what a friend we have in cheeses!”

To the farmers: "Smile and Say Cheese"

How where the life boats?

Do you think you are becoming fixated and lost your sense of humour

Stay on topic

dp

I rode the Auckland busses recently when visiting for a weekend. When they ran, they were great. The other 50% of the time either the bus just did not show up, or the driver couldn't be bothered stopping.

Congratulations, you got to experience the Reality of Auckland Transport. And this was after they axed a bunch of services because they admitted they couldn't get enough drivers to run the buses. Doesn't stop them from 'improving' the roads to the point of near standstill for car traffic.

I live in Ak and don't own a hop card.

The dangers of travelling by bus is one factor in the equation.

No doubt more of this to come. Some pretty sizable losses.

https://www.oneroof.co.nz/news/crippling-losses-for-amateurs-who-gamble…

Echoes what I was saying yesterday, even spookily echoing my phrase ‘amateur developers’.

of course, OneRoof were a big part of hyping this activity up,lol….

And quoting Tony Alexander, spew….

Tony is all out of credibility, just stop listening to him, its not worth the heartbeats.

I wonder if Max key would be in the "amateur developer" class. Mind you he'd have his old man to bail him out or would the old man let his son's company fold.

Yep definitely amateur, a real wannabe

Well this is slipping under the radar of most media. It looks like "CBDC 1.0" is ready to be launched in the U.S. in July.

“With the FedNow Service, the Federal Reserve is creating a leading-edge payments system that is resilient, adaptive and accessible,” said Tom Barkin, president of the Federal Reserve Bank of Richmond and FedNow Program executive sponsor. “The launch reflects an important milestone in the journey to support financial institutions serve customer needs for instant payments to better support nearly every aspect of our economy.”

The Federal Reserve Banks are developing the FedNow Service to facilitate nationwide reach of instant payment services by financial institutions — regardless of size or geographic location — around the clock, every day of the year. Through financial institutions participating in the FedNow Service, businesses and individuals will be able to send and receive instant payments at any time of day, and recipients will have full access to funds immediately, giving them greater flexibility to manage their money and make time-sensitive payments. Access will be provided through the Federal Reserve’s FedLine® network, which serves more than 10,000 financial institutions directly or through their agents.

https://www.frbservices.org/news/press-releases/031523-july-launch-anno…

Important Update: FedNow is basically a CBDC for institutional payments. It allows both consumers & businesses to make payments in real time, with immediate availability of funds for the receivers.

FedNow does not have the level of programmability that a CBDC system theoretically could have.

It'll be a digital crumb dispenser.

Fiat with lipstick is still a pig.

People shorting Silicon Valley Bank and Signature Bank on the Robinhood platform are not able to sell their contracts or get paid. And it has spread to other brokers such as Fidelity. This is a great example of how Wall Street gets first divs and screws over the little guy, despite the democratization of finance through technology.

The lawsuits are already in preparation and the SEC and Attorney General are going to have to step up and be accountable.

https://www.forbes.com/sites/brandonkochkodin/2023/03/14/robinhood-user…

People still use Robinhood? Are they thick?

Mental note that Robinhood is a clown show and should never be trusted.....

The only economic news story of importance is Credit Suisse. The rest is noise for now.

Warren Buffett -‘There’s never just one cockroach in the kitchen’

Given at least one French bank clamped down on some aspect of their CS relationship, it will be interesting to watch them and their compatriot banks in the days ahead.

Wait till analysts twig to the US banks exposure to the antipodean property market.

Says it all for National...

https://www.stuff.co.nz/opinion/114832273/jim-hubbard-cartoons

When people start losing their jobs because the property market falls over, then you do wonder if a party leader who owns seven rentals will be seen fondly or not.

What Luxon did was what The System encouraged him to do. All the incentives were set to buy property. I don't criticize him for that.

What I do question is his judgement, both financially and politically. It was obvious what was coming to the property market, yet he held his portfolio.

What we need from a future PM is someone who looks ahead; anticipates what's coming. Not someone stuck in a past of failed policy settings.

Does he still own the same number of properties?

But now he's in a position to influence the incentives in the system would it not be more ethical for him to sell?

Absolutely. The nats proposed policies on property investment stink of self interest, and this is enough to rule out me voting for them. He should sell his rental properties and put the proceeds in a blind trust.

A quick squizz at the old Pecuniary Interests register shows Hipkins has three houses.

And I can't recall ever hearing the name 'three houses Hipkins' once in his entire career.

It couldn't possibly be that people are setting bars for leaders they're not going to vote for anyway that no one else can apparently get over either?

Firstly, I've got no plans to vote for Labour either. Secondly, the thing that makes Luxon's position so offensive is not only does he own several houses, but he is proposing policies which will actively boost house prices. I believe these go against the interests of the majority of kiwis, and firmly in his own self-interest.

The only economic news story of importance is Credit Suisse. The rest is noise for now.

Nobody around the water cooler seems particularly concerned. I don't push the issue.

Having to sell your treasuries & take a loss for cash flow reasons exposes the whole stinking system. We've reached breaking point. My guess is the Swiss authorities won't let CS fall/fail.

QE then.

And that too will fail this time.

None of us is going to sit back and watch Inflation eat our purchasing capacity whilst new, system saving Debt is created. We'll be out buying and spending, and driving the CPI into double digits.

We may get QE and be saved, but we'll also get 30% mortgage rate along with it.

Absolutely. I'm already being utterly wreckless. I have a stockpile of 3 bags of muesli in the cupboard and no regrets. If they push me any harder with inflation there is no telling what I'll do.

Hahaha

Also with a lot of the world now forced to / wanting to decouple from our currency/banking system you would think this would incentive them.

Swiss central bank extended 54bil usd loan to CS, so consider them the proud property of the swiss population, then may be more cash required.......

...went for a 4.35% yield, well below the 4.61% at the equivalent event two weeks ago.

*Sigh* Remember when debt was like 0.5% and we could just spend money like water? I suppose it's time to take a sober look at what we have due and when.

We should probably start to run a budget surplus as well, introduce some new taxes and cut the spending.

Only David Seymour could make that sound sexy

What would expected patronage be (if they didn't have all the problems with their network) given the propensity for working from home and flexible working hours since the pandemic?

If you're not forced to travel at peak hours (where you might have considered languishing on a bus rather than in the traffic). Is a 1/3 drop unreasonable? I feel like 3 days a week in the office is pretty normal at least anecdotally.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.