The inflation expectations of New Zealand businesses "took a step lower" this month, but are still too high, while cost and price expectations are "holding up", according to the latest monthly ANZ Business Outlook survey.

ANZ chief economist Sharon Zollner said the January survey was "a mixed bag".

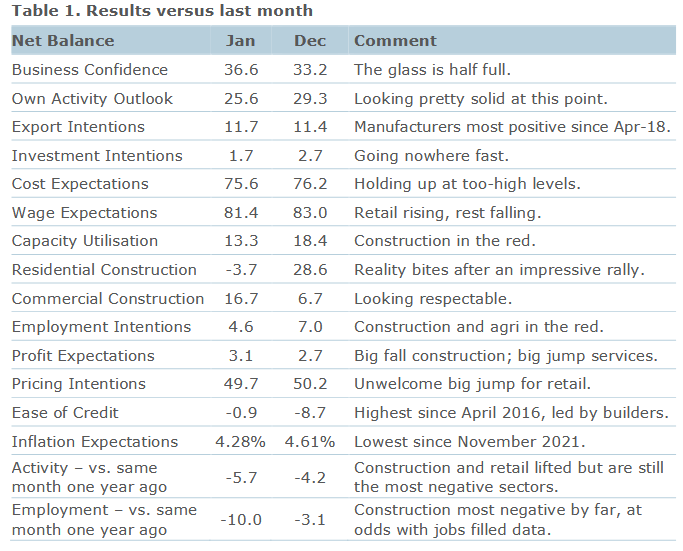

Overall business confidence, which has surged since the October election, rose another 4 points to +37 in January, while expected own activity fell 3 points to +26.

However, while inflation expectations were down they were still at 4.3%, above the Reserve Bank's target of 1% to 3% inflation.

And cost and price expectations included a "solid jump" for the retail sector in terms of firms expecting to raise prices.

"Firms’ specific estimates of what they expect to do with their own selling prices in three months’ time has been going sideways for seven months," Zollner said.

"Notable moves this month included a lift for retail and a fall for construction."

She said "renewed shipping woes" may be contributing to some extent.

The proportion of retailers expecting higher costs in the next three months rose from 72% to 76% this month, and the size of retailers’ expected cost increases eased slightly but remains higher than November.

"Overall, expected cost rises are still higher than expected price rises, so firms are certainly not expecting to be able to pad margins. Expected cost growth is 3.4% (unchanged) while expected price growth was 2.1%.

"Most helpfully for the RBNZ, construction sector respondents now expect just 2.3% cost inflation over the next three months, the lowest across the five sectors and a sharp fall from the peak of 7.8% in mid-2022," Zollner said.

Reported wage increases versus a year earlier were flat but are trending lower. Average expected wage settlements over the next 12 months fell slightly but appear to be flattening out.

Zollner said the surge in residential construction intentions over the past year had been "startling", but it "ran out of puff this month".

"It nonetheless suggests that dwelling consents and residential construction are about to find a floor."

Zollner said the economy is "at a delicate juncture".

"We are forecasting a pretty good outcome compared to some scenarios: the RBNZ has done enough; it’ll take a while for that to be incontrovertible but by August they can commence a steady stream of OCR cuts.

"Growth is nothing flash (particularly per capita) and unemployment unfortunately rises above 5%, but the overall the economy continues to unwind its unsustainable Covid-era excesses without any major drama.

"And we’re assuming no nasty global shocks, though we’ve built in some persistent sogginess in demand from China’s consumers for our exports.

“Overall, businesses also expect the worst is past. Although the medicine has been bitter, it’s working. We just need those pricing intentions to start playing ball to steer clear of another dose of monetary tightening.

"The RBNZ has given fair warning that their patience is limited. While the market is ruling out any chance of a hike at the end of February, we would not.

"There are definite signs of a stall in some of the leading inflation data, and the RBNZ may just decide they need to do more to be sure progress will continue, even at the risk of making a policy mistake.

"The hiking cycle that ended in 2008 features two pauses that were followed by a resumption of hiking. It would hardly be unprecedented."

Business confidence - General

Select chart tabs

7 Comments

Prices will continue to stay high for a while, hence rates will stay higher than people anticipate

Haha the thought process of a dgm is no doubt without logic.

Genuine question. Why do you think that? Can you provide a list of reasons?

Bank economists have given up on 'potential rate rises' and 'no OCR falls until 2025' and are now saying OCR reductions 'by August'? How about being honest and saying "BEFORE August"?

It is no wonder the economics profession is so despised.

BTW ... GDP might be slightly positive ending December 23. Per capita GDP? Sorry.

I really do question the value and credibility of this survey when it can swing so wildly within one month (ie. residential construction) for no obvious reason

Nailed it.

Banks love to have lots of information sources. They can then pick and choose which one to use when they're selling stuff.

“Growth is nothing flash” is a slight trivialisation isn’t it? At -1% / capita for the last quarter?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.