The ANZ Banking Group says its New Zealand subsidiary has posted a 13% drop in unaudited interim profit as the bank moves to writedown software costs faster, credit impairments rose, operating income fell and operating expenses increased.

ANZ Bank New Zealand, the country's biggest bank and largest rural lender, posted net profit after tax of NZ$763 million for the six months to March. That's down $114 million, or 13%, from $877 million in the same period of last year.

Operating income fell $36 million, or 1.9%, to $1.895 billion, and operating expenses increased $76 million, or 10.3%, to $815 million. The bank's credit impairment charge climbed $19 million, or 61.3%, to $50 million.

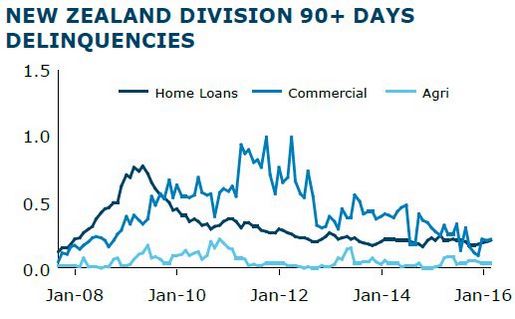

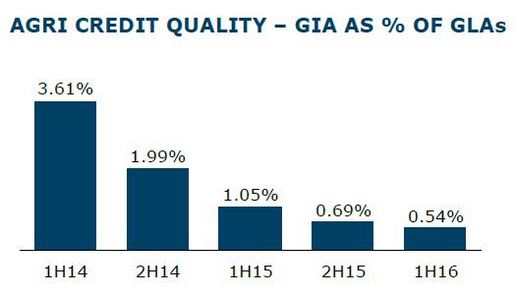

Just 0.54% of agriculture loans stressed

Of ANZ NZ's $17 billion worth of agriculture gross lending, 70%, or $11.9 billion, is to the stressed dairy sector. However, the bank categorised just 0.54% of its agriculture lending as gross impaired assets as of March 31, down from 0.69% at September 30 last year. Some 10% of the bank's lending is to the agriculture sector. (See more on ANZ NZ's bad and doubtful debts in the charts at the bottom of this article).

ANZ NZ CEO David Hisco told interest.co.nz ANZ's low level of impaired agriculture lending in a time of significant stress in the dairy sector comes after a major strategic push by the bank since the last dairy downturn in 2009.

"We've been emphasizing with our farmers that cashflow is important rather than the value of their property. And there have been farmers who haven't wanted to hear that and they've gone and refinanced with another bank. But by and large we think our (dairy) book is in a better position than it was first time around (2009, 2010)," Hisco said.

"Our stress year on year has gone up a little bit, (but) I saw Westpac's go from 3.9% to 7.8% (in the six months to March 31) (and) ours has gone from 4.39% to 5.75%. So it has moved up a little bit, but it's not as stressed as they are."

"We think we have built a more sustainable dairy book going into any downturn. Obviously the longer the milk price stays down the harder it's going to be for everybody. And there comes a point when it will get stressful no matter who you are. But at this point in time we're working hard with our farmers to get them through and a little bit of luck on the milk price would be a good thing," Hisco added.

Interest free Fonterra loans 'a good release valve'

Asked if he thought stubbornly low international dairy prices were due to structural changes in the industry or cyclical issues, Hisco said probably a bit of both.

"There are probably structural changes. We're not the only supplier. We've been talking with our farmers about getting themselves to a lower cost position. It's no different to owning a bank. In the end the best way to weather a crisis to be a low cost operator and some of them are not low cost operators. It means that you suffer when things turn down."

"If our farmers have to compete with other dairy farmers around the world who can operate at a lower cost, then you've got to ask yourself whether you are set up for the long term to win," said Hisco.

Asked to what extent the $390 million interest free loan package Fonterra made available to its farmers is helping, Hisco said this was a very good initiative.

"It was a good release valve and it was what people were looking for Fonterra to do, show a little leadership and empathy around the plight the dairy farmer is going through. I think anything that Fonterra can do that's imaginative that helps farmers will be greatly appreciated right now," said Hisco.

One-off cost from accounting change

ANZ NZ said its half-year results were affected by a $87 million charge associated with an accounting change to the application of the ANZ group's software capitalisation policy. Although unaudited cash profit fell 11% to $751 million, without the accounting change, it would've fallen just 3%.

Of the accounting change, which the bank said was also the key factor in its rise in operating costs, ANZ NZ said it had introduced a greater level of discipline to the management of software costs, bringing forward the recognition of software expenses resulting in lower amortisation charges in future years. The group lifted its software capitalisation threshold and is directly expensing more project related costs. (There's more on the change here).

Net interest income was a bright note for the bank, rising $71 million, or 5%, to $1.493 billion.

Meanwhile, the bank said credit impairment charges increased largely due to lower write-backs in its commercial lending unit. Gross impaired assets fell $76 million, or 18.1%, over the six months to March to $343 million. As a percentage of the bank's gross loans and advances, gross impaired assets came in at 0.29% at March 31, down from 0.48% a year earlier.

Half-year profit at ANZ NZ's retail unit rose 8%, it increased 1% at the wealth unit, but profit at the bank's commercial unit (including rural) fell 9%, and profit sank 42% at the bank's institutional unit.

Net interest margin falls

ANZ NZ's net interest margin, meanwhile, fell 8 basis points year-on-year, and 3 basis points over the half-year, to 2.19%. This was attributed to lending competition, an "unfavourable lending mix" with customers continuing to prefer lower margin fixed rate loans, and the impact of a March capital notes issue.

The bank's cost-to-income ratio climbed 470 basis points year-on-year to 43%, and was up 520 basis points over the half-year to March.

Net loans and advances increased 3% in the six months to March to $117.470 billion, and customer deposits were up 6% to $90.148 billion.

ANZ group cuts dividend payout ratio

The ANZ group posted a 22% drop in interim net profit after tax to A$2.7 billion following an A$717 million net charge the bank says is related to initiatives to reposition the group for stronger profit before provisions growth in the future. The ANZ group also cut its fully franked interim dividend by 7% to A80 cents per share, and cut its dividend payout ratio to between 60% and 65% of annual cash profit from 65% to 70%.

"Following a period of dividend payout ratio expansion in the Australian banking sector, ANZ will gradually consolidate to its historic range of 60% to 65% of annual cash profit. This setting better reflects the changed banking environment in which we operate and the greater demands for capital," group CEO Shayne Elliott said.

The ANZ group reported an A$918 million provision charge, equivalent to a 32 basis points loss rate and in line with a sharemarket disclosure made in March.

Here's ANZ NZ's release, and here's the ANZ group release. And here's a video interview with ANZ group CEO Shayne Elliott from the bank's BlueNotes website.

8 Comments

Sold the rumour, last June - what next, buy the news? - I think not.

One of my oldest friends, Steve Targett, will be having a quiet one this evening! He never saw John McFarlane's Asian Dream as sustainable, and so 'lost out' to Mike Smith.

Does 0.54% of gross impaired assets in their agri book seem a bit low?

as long as the payments are made and revalueations are done they will not reduce the value on the books

its only when they go to sale that any loss will be taken on board

Yeah, I reckon the decimal point needs moving to the right maybe.

I wonder how different that number would be without the interest free advance on offer from Fonterra?

FYI, I've updated the story with some comments from David Hisco on the Fonterra loans.

This number will change drastically with the falling of farm prices that ANZ cannot control as other banks move forward in receiverships

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.