By Gareth Vaughan

ASB has posted a 6% rise in annual profit as lending grew 10% and deposits grew 5%.

Annual net profit after tax rose $54 million, or 6.3%, to $913 million comfortably topping the previous year's $859 million. It's the sixth consecutive year ASB has recorded record annual profit.

Net interest income rose $95 million, or 6%, to $1.762 billion. However, ASB's net interest margin dropped 6 basis points to 2.32%, which the bank attributed to continued competitive pressure on lending and deposit margins and customers preferring lower margin fixed-term loans. Total operating income increased $140 million, or 7%, to $2.226 billion.

Total advances, or loans, to customer rose $6.7 billion, or 10% to $72.075 billion. Within this housing loan growth of 9% was above system, or higher than overall market growth. Business and rural lending growth, meanwhile, came in at 13%, also above system. Customer deposits grew $2.5 billion, or 5%, to $54.702 billion.

| Year | ASB net profit after tax | Ordinary dividend paid |

| 2016 | $913 million | $200 million |

| 2015 | $859 million | $1.140 billion |

| 2014 | $806 million | $400 million |

| 2013 | $705 million | $90 million |

| 2012 | $685 million | $500 million |

| 2011 | $568 million | $280 million |

| 2010 | $236 million | $160 million |

| 2009 | $425 million | $180 million |

Operating expenses and impaired lending both increase

ASB's operating expenses rose $21 million, or 3% to $826 million, which was attributed to higher staff costs, continued investment in frontline capability and technology, and marketing costs. However, ASB's cost-to-income ratio dropped 110 basis points to 37.3%.

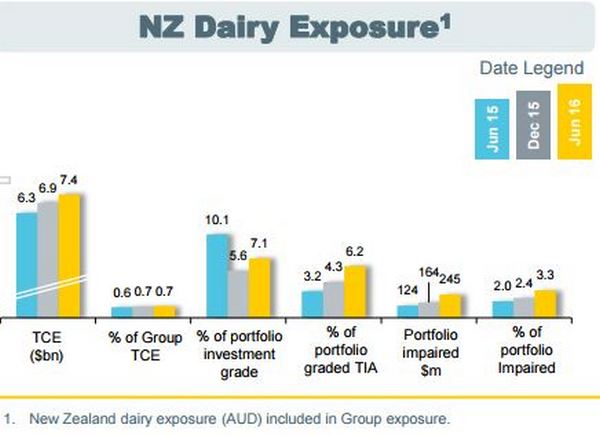

Loan impairments rose $41 million, or 46%, to $130 million due to increased provisioning of dairy farming loans, and higher unsecured retail provisioning. Some 3.3% of ASB's dairy portfolio was impaired at June 30, up from 2.4% at December last year (see chart below).

"We have taken a conservative position and have increased provisions in the dairy sector accordingly," ASB CEO Barbara Chapman said. "That said, we remain confident in the asset quality of our rural book and see our farming customers responding well and managing their businesses in response to the conditions."

(The chart below comes from CBA).

Return on equity falls

ASB's return on ordinary shareholder's equity dropped 100 basis points to 18.1% from 19.1%. Its return on total average assets was unchanged at 1.2%. The bank's common equity tier one capital as a percentage of total risk-weighted assets rose to 10.0% from 8.8%. The Reserve Bank mandated minimum is 7%.

ASB's funds management income, meanwhile, rose $11 million, or 15%, to $85 million.

"We have achieved this result against the backdrop of a highly competitive market and some significant headwinds in the form of global market volatility and fluctuating commodity prices. Despite this, we have remained focused on executing our strategy and pursuing initiatives to drive profitable growth across our business," Chapman said.

ASB paid annual ordinary dividends of $200 million, well down from $1.14 billion the previous year.

Total assets increased year-on-year by $5.7 billion, or 7.5%, to $81.606 billion, and ASB's total liabilities rose $4.3 billion, or 6%, to $74.794 billion.

ASB's cash net profit after tax - the bank's preferred profitability measure - rose $44 million, or 5%, to NZ$908 million in the year to June 30 from $864 million last year.

Sovereign, ASB's sister company and CBA's New Zealand insurer, posted a 15% drop in annual cash net profit after tax to NZ$105 million.

CBA pays out 76.5% of profit in dividends

CBA itself posted a 3% rise in annual cash profit after tax to A$9.45 billion. Its return on equity was 16.5%, an annual drop of 170 basis points from 18.2%. CBA's net interest margin also dropped, falling two basis points to 2.07%. The bank's paying a full-year fully franked, unchanged dividend of A$4.20 per share, equivalent to a cash profit dividend payout ratio of 76.5%.

CBA CEO Ian Narev said the bank was cognisant of the combined impact of weaker demand, strong competition and increasing regulation.

"An ongoing focus on productivity and credit quality will be important. But we remain positive about Australia's economic prospects, driven by population growth, our proximity to growth in Asia, and the attractiveness of Australia as a destination and a trusted source of a broad range of goods and services," said Narev.

11 Comments

no-one wants to get started on it?... just afraid to post inappropriate comment?.. :-)

"CBA pays out 76.5% of profit in dividends" on the money from the air..

I can't seem to recall the last time any of the big four in NZ had a lower yoy profit announcement.

Can anyone else?

Where is all of that YOY 'after tax profit' going?

Money from the air eh. No need for deposits or a balance sheet then. Off to the printery.

Well its not bad news for me I have a lot of money invested with them so with results like this they cannot cry if things suddenly get tough. The last thing we need is the banks going down the toilet.

Older people who have saved for retirement are once again being ripped off by offshore owned banks. You can't tell me they can't afford to give investors a decent return when they are achieving record profits. The whole banking system is in need of a big shake up. How can smaller NZ banks (i.e Heartland, Co-operative) offer higher rates than the big four?

buys some shares then.

19% roi sure beats 2% on term deposit.

Shares don't give the regular monthly income that a lot of older folk rely on. The share price is only increasing because of the number of investors switching from term deposits to shares. But that bubble will burst, sooner rather than later.

Lets see how much of the rate cut announced today that the ASB passes on after another "The banks made another record profit" announcement.

oh break out the champagne Dennis...

John Key would be loving this historical data........oh my farming lads look how successful National has been, we have doubled the profits of your banks!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.