By Gareth Vaughan

The Australian Prudential Regulation Authority's move to make Australia's big banks reduce non-equity exposures to their New Zealand subsidiaries is a key factor behind the drop in Westpac New Zealand's net interest margins, CEO David McLean says.

Westpac NZ eked out a 2% rise in half-year cash earnings as impairment charges in the first-half of last year's financial year swung to write-backs and loan recoveries this year. Cash earnings were up $10 million, or 2%, for the six months to March 31 to $462 million versus the equivalent period of the previous year.

The bank's net interest margin (NIM) sank 22 basis points year-on-year to 1.96%. McLean told interest.co.nz APRA's decision in late 2015 to tell the Australian parents of ANZ NZ, ASB, BNZ and Westpac NZ they have until 2021 to reduce their non-equity exposures to their Kiwi subsidiaries to below 5% of the parent's Level 1 Tier 1 Capital, is a key factor in this NIM compression.

McLean says competitive pressures among the major banks have moved away from lending and into deposit gathering over the past six months or so.

"I think a lot of that was driven by different banks having a task to refinance some of their financing to comply with that APRA requirement that the Aussie parents had to limit their inter-company lending to 5% of Tier 1 Capital. Some banks had a much bigger refinancing task than others. We didn't have a particularly big refinancing task but we were caught up in the competition for deposits that seemed to result from that," McLean says.

Westpac NZ has to repay its parent $500 million, ANZ NZ has to repay its parent $8 billion. ASB has only said its parent, Commonwealth Bank of Australia, expects to be compliant with the new APRA rules within the five year transition period. And BNZ has said it's "well placed" to meet APRA's requirements because its parent, National Australia Bank, has no outstanding senior unsecured loans to BNZ and does not conduct any business through a branch structure in NZ.

Westpac NZ also cited lower fixed rate break fees at $12 million (no comparison from the previous period was provided) for its reduced NIM.

"This time last year when people still thought that [mortgage] rates might be coming down a bit, there was still quite a lot of activity going on and people paying us break fees. Whereas this year there's almost no break fees being paid and that would go into the NIM as well. I think it's really a story that competition is favouring deposit customers," says McLean.

Income down, expenses up

Meanwhile, Westpac NZ's net operating income fell 1% to $1.078 billion, and operating expenses rose 2% to $468 million. Impairment charges of $9 million in the six months to March last year reversed to write-backs of $36 million this year. Net interest income fell $11 million, or 1.3%, to $838 million.

Over the six months from September 30 to March 31 Westpac NZ's total deposits declined by $700 million, or 1.2%, to $56.8 billion. Net lending grew $1.4 billion, or 2%, to $76.5 billion. The deposit drop was attributed to lower institutional deposits, and a decline in Asian deposits.

McLean says Westpac NZ is focusing on quality lending and targeted growth in a challenging environment with increased pressure on deposit and wholesale funding margins.

“We are seeing growth in positive sentiment and market share in key segments. Westpac New Zealand’s campaign to support first home buyers through the re-launch of our HomeSaver offering aligns with a steady increase in withdrawals from the Westpac KiwiSaver Scheme by first home buyers. At the same time funds in the Westpac KiwiSaver scheme have increased 20% in the past year with the average balance increasing from $5,800 in December 2012 to $11,400 in December 2016," McLean says.

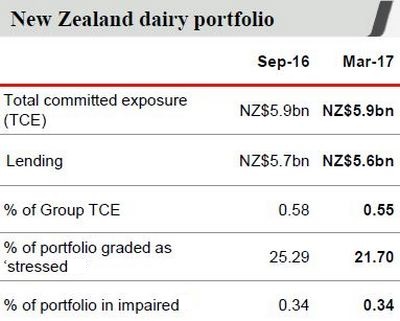

"An improving dairy sector and continued underlying economic growth contributed to a strong asset portfolio with impairments $45 million improved on the same period last year."

“We saw growth in targeted market sectors, including Auckland and millennials, and it is good to see a continuing recovery for many of our dairy farming customers, which is reflected in our significantly improved impairment position," says McLean.

“At the same time we experienced reduced net interest margin, [which was] a result of strong lending competition and increased funding costs.”

McLean notes both ANZ NZ and BNZ also reported margin compression last week. ANZ's fell 10 basis points to 2.30% and BNZ's dropped 12 basis points to 2.15%. He agrees with his BNZ counterpart Anthony Healy that mortgage rates are likely to rise.

"Both the other reporting banks in this period have seen also NIM compression and it can't go on at that rate for too long," says McLean.

Base rate signals globally show interest rates rising, and some inflation is emerging in NZ, he adds.

"The cost of wholesale funding has gone up as well as the local deposit funding has gone up, so I don't think I am the only NZ bank CEO who is saying this but I think there's likely to be higher interest costs for borrowing," McLean says.

Stressed loans up year-on-year, down since September

As of March 31, Westpac NZ's total stressed assets to total loan exposures stood at 2.41%, up from 1.78% a year earlier, but down from 2.54% at September 30.

The bank's half-year cost-to-income ratio came in at 43.4%, down 156 basis points year-on-year, and down 198 basis points since September. In terms of higher expenses, Westpac NZ said it booked a $10 million increase in investment spending as part of a three-year transformation programme to improve customer service and improve self-service offerings such as ATMs and digital banking. The closure of 19 branches reduced full-time staff by 153.

Figures released by parent Westpac Banking Corporation show Westpac NZ shed marketshare in consumer lending and deposits in the year to March 31, but grew business lending marketshare.

| Westpac NZ | March 31 | Sep 30, 2016 | March 31, 2016 |

| Consumer lending | 19% | 20% | 20% |

| Deposits | 19% | 20% | 21% |

| Business lending | 17% | 17% | 16% |

Over the six months to March 31, Westpac NZ grew residential mortgages by $1.1 billion, or 2.4%, to $46.2 billion. Reserve Bank sector credit figures show housing loans grew 2.9% over the same time period. Meanwhile, Westpac NZ grew business lending $200 million, or 0.7%, to $28.6 billion.

Meanwhile, Westpac Banking Corporation posted a 3% rise in interim cash earnings to A$4.017 billion. Its fully franked ordinary dividend was unchanged at A94 cents per share representing a payout ratio of 79% of cash earnings, and a dividend yield of 5.4%. The bank's return on equity of 13.95% was down 20 basis points.

Here's Westpac NZ's press release and here's the Westpac group release.

19 Comments

Westpac New Zealand eked out a 2% rise in half-year cash earnings as impairment charges in the first-half of last year's financial year swung to write-backs this year.

What is happening in respect of the veracity of bank financial status disclosure policy, given cash earnings have currently assumed benchmark status?

And yet: BNZ's half-year cash earnings, which is not a statutory financial measure, is not presented in accordance with NZ Generally Accepted Accounting Principles, nor audited, rose $40 million, or 9%, to $484 million. Read more

Where are the regulators when one needs them most to intervene and stop the irregular nonsense?

"Where are the regulators?" - I think they are resting from their labours of setting up the NZ depositors as scapegoats for RBNZ non-regulation with their unique OBR scheme designed to protect the banks (both NZ and their Australian parents). In the meanwhile the RBNZ are busy generating a "dashboard" to further distance themselves from responsible regulation of the NZ financial system.

billsay,

Well said. I made a brief submission to the RB last year on their 'Dashboard' proposal and I have little confidence that it will do anything to enlighten depositors,but would allow the Bank to claim that it had done everything possible to inform the public,in the event of a bank collapse.

Stephen, I had a look at cash earnings/profit a few years back. Here http://www.interest.co.nz/bonds/61213/banking-analysts-outline-how-they-believe-big-banks-have-been-overstating-their-profits and here's what the RBNZ said - http://www.interest.co.nz/bonds/61411/analyst-frustration-mounts-bank-cash-profit-reporting-rbnz-points-fma-guidelines-key

I am not a great fan of this metric either.

So this is all great but once again I find myself asking how much tax do they pay? Can anyone answer that? I assume it is not $129m being 28% of cash earnings as that is not profit.

"more than 70% of our customers are ahead on their mortgage repayments" Cool! But that " ( includes mortgage offset balances)". Balances that are enough to service the next mortgage payment and that can be withdraw at the flick of a key. What would the mortgage book look like without those Brian? And the fact that you have also excluded from that 70% figure any loan that has no principal repayment component.

On the principal repayment topic - I went for a beer with an old friend a few weeks ago. He tells me he owns three homes in Auckland - owned them for 5 years but hasn't paid back any principal. He's working interest only. How much of this is going on?

He's also getting a bit nervous and thinking about listing them all, taking his capital gains, escaping the traffic and getting out of the city..

Zero years left for your friend! 5 years is supposed to be the limit of the interest-only period. Come the end of that time, it's P&I for your friend. I hope he's ready! Oh, and 'lots of it is going on' and in the blissful ignorance in many case that 5 years....is it!

Makes me wonder how many people are in that position - if interest rates rise and they have to start paying back principal - things will start getting pretty tight financially for a lot of people.

I don't think the five year rule is set in stone.

It will be stated in the original lending documents and yes 5 years interest only forms part of the banks terms. The bank can actually recall loans at any time too.

Unfortunately he should have had sold contracts with settlement dates by November last year. Since then the Auckland Property market has stalled because of a major change in lending practices with our Big 4 Banks. The Credit Crunch is real and so is the Chinese Capitlal Flight because they will never buy in a tanking market. I have many friends who purchased investor properties in Auckland on "Interest Only" terms and their 5 years is also up. The market is about to be flooded with desperate sellers and the buyers can't pay the sellers asking prices even if they wanted to, because the banks have already changed their lending policies 4-6 months ago. APRA call the shots now.

2%?!?!?!? Embarrassing!

Tip for Westpac management: Put all your pennies in an ANZ serious saver account at 2.35% - Magic!

2.35% interest is magical

I cannot even reach 1% up here in a mega bank

Is there any other business that will generate $2.500.000 cash earnings PER DAY out of thin air?

Are you referring to residential property investment as a business?

Jerry - certainly not many in NZ, but then again, probably not many including you who are able or prepared to investment multi billions of their capital into this country to try to generate a profit. A 14% return on capital is pretty average for many NZ businesses

I found westpacs deposit rates in the last few month, weren't as high as what other top tier banks could offer. They also wouldn't offer me any better rate unless I had 500k to deposit! So I moved most into other banks.

McLean says competitive pressures among the major banks have moved away from lending and into deposit gathering over the past six months or so.

"I think a lot of that was driven by different banks having a task to refinance some of their financing to comply with that APRA requirement that the Aussie parents had to limit their inter-company lending to 5% of Tier 1 Capital.

Hmmmm....

Aussie parent funding to underwrite regulatory capital demands associated with domestically fabricated asset growth -

“..... a private bank’s liabilities are widely accepted as a medium of exchange, banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet.” Read more -

is no longer readily available. Hence the need to source off-balance sheet derived NZD swap hedged foreign funding.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.