By David Hargreaves

They are young, footloose, fancy-free...and broke.

The latest credit figures from illion (formerly Dun & Bradstreet) have shown a sharp rise in the number of people under 25 in this country filing for bankruptcy.

And it's a rise that is occurring at a time when the overall bankruptcy figures are falling.

According to illion, in the 12 months to June 30 there were 207 people aged between 18 and 24 that filed for bankruptcy in New Zealand.

That was an increase of 66.9% on the figure for a year earlier.

As recently as 2014 there were less than 20 people in that age group who filed for bankruptcy.

This means that the figure has increased 10-fold in just four years.

illion CEO Simon Bligh said while it was good to see an annual drop, the rise among young people was concerning.

“While the overall drop in bankruptcies is a good sign, no one takes this decision lightly, so to see young people increasingly turning to bankruptcy or insolvency agreements is cause for concern,” he said.

“It’s important to remember the numbers are still very low among the under 25s compared to other age brackets.

"But if they continue their current trend it won’t be long before that changes,” he said

The release of the information by illion didn't offer any explanation for what might be behind this sudden surge in youth bankruptcy in New Zealand - or whether it is a part of a global trend.

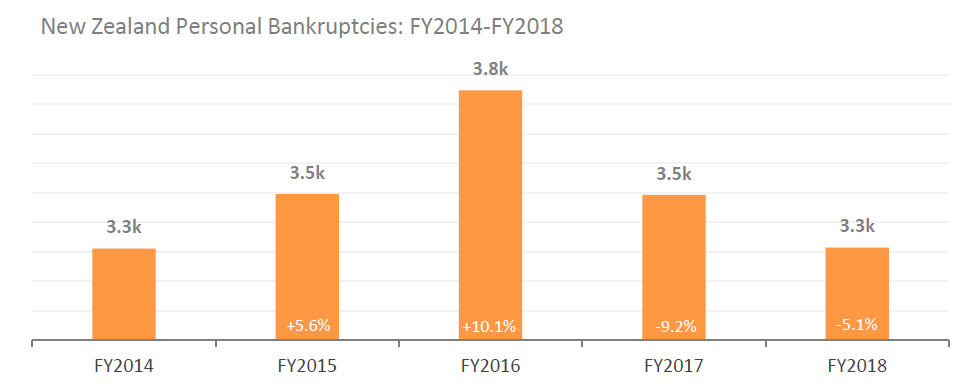

illion's analysis showed that overall, just slightly more than 3,300 people declared bankruptcy in New Zealand in the year to June 2018.

That's a drop of 5.1% compared with a year ago and is also well down on the 3,800 bankruptcies declared in 2016.

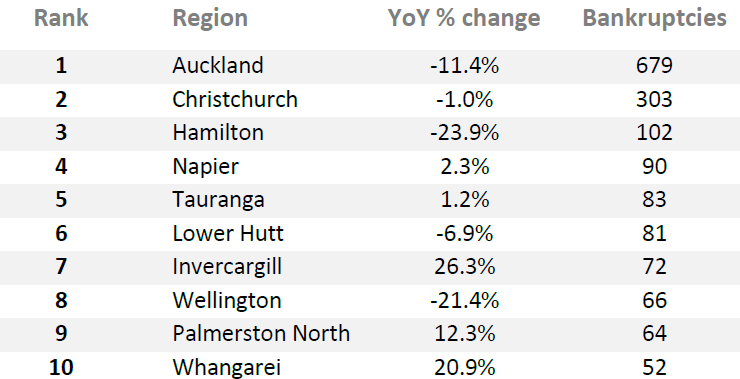

In regional terms, Auckland, again had the highest number of bankruptcies this year, up to June 2018, with 679 personal insolvencies. That was, however, down 11.4% on last year's figures.

Christchurch fell 1% to 303, while Hamilton rounded out the top three at 102 (-23.9%) during the 12 months ended 30 June 2018.

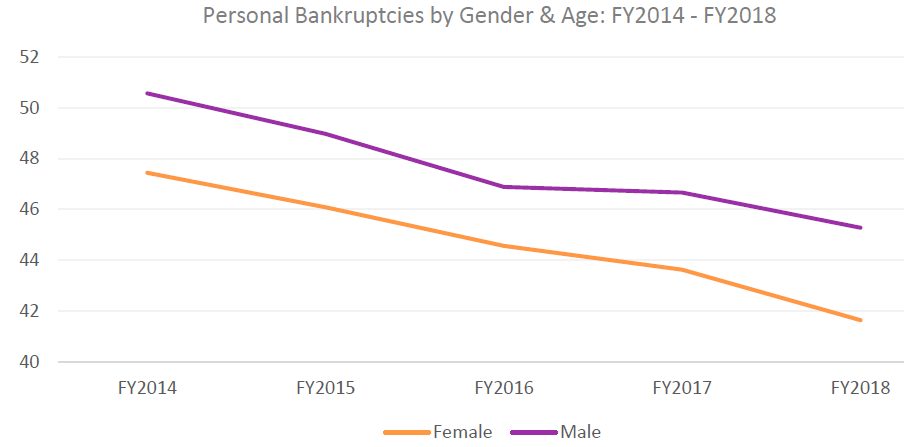

illion’s analysis shows the gap between male and female bankruptcies has closed during the year, with 45.3 years being the average age for a male bankrupt, compared to 41.6 years for a female.

Men remain marginally more likely to suffer personal insolvency, accounting for 50.4% of bankruptcies in FY2018.

22 Comments

Shame there's no graph about bankruptcies by age group

Bankruptcies are most probably low at the moment due to continuing low mortgage interest rates.

In the past few years I have seen very few properties advertised as "mortgagee sale" compared to pre-GFC when interest rates commonly fluctuated by 2 or 3% within a year.

I am very sure that any significant increase in mortgage rates over the next few years will see this current low rate of bankruptcies increase significantly. This especially applies to current FHB who are at their limits, not inclined to pay down debt as a priority, and face an unexpected change in personal circumstances (e.g. one of the couple looses their job).

printer8, well said. Cheaper money has provided considerable "time limited" breathing space. It won't last. If the young are heading to the wall in greater numbers then I suggest this has more to do with peer pressure and poor role models at home.

Young Dumb and Broke!

Bankrupties in the 18- 24 year old group.

I struggle to see how this young age group managed to:

- learn their trade

- learn how to deal with customers

- learn how to deal with staff, employment contracts recruitment, redundancies…

- learn how to properly do accounts, understand cashflow, overheads, pricing, ATB, ROI…

- learn how to deal with IRD requirements (wages, PAYE, DED, GST, FBT etc…)

- learn to understand commercial leases before entering into a lease agreement for their premises

- learn how to be persevering when things didn't go well and adjust the course of their business when invariably things don't go as planned

by the age of 18 - 24.

Hi Yvil

Your comments tend to suggest that bankruptcies are about being in business.

I don't know of the current situation, but I know of two instances (they were mates of each other) some years ago who purposely went into bankruptcy to clear their student loans.

As I said, I don't know whether or not this is still feasible, but these two definitely did do this and I understand that others were also doing it. (It really annoyed me at the time as the two had spent time during the university holidays surfing overseas.)

Someone may be able to comment on the current situation and whether this accounts for the increase in this age group. The opening comment "They are young, footloose, fancy-free...and broke" suggests that this may be possible.

P.S. I note that Invercargill for its size features surprisingly highly in the above data - but that is the town which Mayor Tim attracted students through fees exempt education. However, such students would have no doubt student loans related to course fees and accommodation.

Yeah, I have seen similar things.

Tick up a student loan, Couple of HPs, personal loans,etc...

Head off on the OE, declare bankruptcy while overseas, then stay overseas through your 20s returning in your 30s with no issues and a whole lot of cash.

Hmm, that needs to be fixed. Student loans should not be cleared by bankruptcy. If you're in Nz you don't have to pay anything if you genuinely aren't earning, so its not dragging you down, and with the current no interest its not getting worse. It can sit there forever until you start earning again without weighing you down.

Problem is if you do that, unless we are very sane and sensible in the way we approach education funding and the running of our universities, we'll end up heading down the exploitative American path.

A quick Google:

"Overseas graduates declaring themselves penniless are among the 483 debtors whose $18 million in students loans have been wiped by bankruptcies."

Stuff - Oct 1 2016.

"When a person becomes bankrupt, their student loan is written off by the Inland Revenue Department."

Parry Field Lawyers - October 27 2017

"Any debt that exists at the date of adjudication will be written off, except for child support or debt owed because of fraudulent activity. You will be liable for any debt incurred after this date.If you have a student loan, you need to change your tax code so that your employer stops making deductions."

IRD Nov 13 2017

Note: No need to go overseas; this can be managed in New Zealand if one is purposely in a low paid job (an informal sabbatical) and rakes up other debt (other than a house as that gets too messy).

So a likely speculative reason for so many young being declared bankrupt is possibly not too hard to guess.

Heck, maybe they just take their lead from the white collar crims and the treadmill of building outfits etc that wind themselves up and walk away leaving broken people in their wake?

But yes, annoying.

@Yvil, one more thing to the list:

- Learn to accept that the older generations have screwed up the housing situation and they will never be able to afford one.

My guess is its consumer debt. These are bad choices by the young in areas like whangarei which have had a percentage increase while other areas are dropping.

On persevering, I'm glad that those who sailed to nz on voyages of expedition didn't give up and turn around or just say they couldn't be bothered trying in the first place. Those journeys took determination.

If this is your argument, then you would expect the number to stay roughly the same over time unless we are now pushing more young people to self-employment

I suspect many individuals that opt for a NAP believe that after a few years their credit files will be wiped clean.

the reality is that credit providers search the insolvency register and this isn't swept under the carpet.

Any subsequent credit obtained will more than likely include a significant risk premium.

There is no such thing as a free lunch

I was surprised to learn a while back that you can wipe mortgage debt by going bankrupt.

I friend of mine and his now ex wife owned a place, the bank foreclosed, they owed money, she went bankrupt and they came after him for the lot.

And he negotiated! Another thing I didn't know you could do. He basically said to them "I'll pay you $x or go bankrupt as well" and the bank had no choice but to agree.

6 months later a bank gives him a mortgage on another home...

Smart guy not going bankrupt or he couldn't have got the next mortgage for the new property.

Yes all though, even then, it's only 3 years.

I previously would have thought a bank wouldn't touch a bankrupt, but now I tend to think they probably would.

After all they create the loan out of thin air, so no way to lose really.

Hi Davo36

Re: "I was surprised to learn a while back that you can wipe mortgage debt by going bankrupt . . . and the bank had no choice but to agree".

Not quite as simple as that, and under the circumstances of a separation (especially with an evil ex-wife) I suspect that your mate may not have given you an unbiased or full account of what actually happened.

A mortgage is secured (i.e. a secured loan) against the house in which the bank will require you to have a level of equity at the time you take the loan.

The purpose of the bank requiring you to have equity is simply to protect themselves in the event of your default on loan repayments.

The moment that you are in default of a payment or two they will be looking very closely at you. The instant that they believe that you are not capable of servicing the loan, they will require immediate repayment of the mortgage (which under the mortgage terms they will have) and, as most likely, you being unlikely to do so they will force a sale of the property (a mortgagee sale).

They will be acting promptly to ensure that they can recover all - or at least as much as possible - of not only the initial loan/mortgage but all outstanding interest and penalty payments due.

In a mortgagee sale you lose control of both the sale process and the price obtained that your (shortly to be former) house sells for.

The bank needs to demonstrate that they will get the best price possible so this will be most likely done at auction and they are most likely to accept the highest bid regardless of what it is. Their concern will be to get their money and they will have little regard to recouping your equity - in reality you are likely to lose most if not all of your equity and the purchaser typically gets a bargain at a mortgagee sale (which are happy hunting grounds for property investors).

So, as you head towards bankruptcy, the bank will have got in first to sell your house to recover the outstanding money owed to them. When the mortgage was granted, the level of your equity would have been estimated to be sufficient to ensure that there was sufficient of a buffer for the bank recover its money in a forced sale situation.

If they are unable to recover all outstanding amounts of the loan and interest and penalty payments, and you are unable to meet these, they can initiate bankruptcy procedures and attempt to recover outstanding amounts along with other of your creditors from the forced sale of any other of your assets (e.g. car, tv, computers, kitchen pots and pans and cutlery etc) that you may have.

My understanding is that there is currently dispute as to whether in bankruptcy the creditors can seek some redress against your KiwiSaver (less government contributions) under the KiiwiSaver hardship provisions.

Possibly the bank negotiated a settlement on the other assets especially if the remaining assets were of little value (such as the car was secured against money owing on it and was likely to be repossessed) and it was not worth their while pursuing these.

So your mate probably didn't probably give the full story - they agreed to settle only because he had so little it was not worth their while pursuing any further.

So it is not a simple case of wiping the loan; the bank will be in there recovering all that they can and giving your equity secondary consideration. And don't ever think that the bank has no option but to agree; the only time they will agree is if they choose that it is not worth their while bothering as one has so little.

Young and broke. Looking at you saving_for_auss, Houses Overpiced & PropertyPrices2Fall...

Little sympathy from me I have seen how a large group of them behave. They all think they are smart because they know how to use a phone but in reality they just have no self control or discipline. I can understand to some degree because things have changed so much and there is now so much influence via social media and the internet that they think they can all live like rock stars. Its hardly surprising that at some point you have to pay the piper for that lifestyle.

Grumpy old man yells at cloud.jpg

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.