By David Hargreaves

It's spreading. And how.

The plunging levels of business confidence seen since the Coalition Government came into power are now well and truly making their way into the minds of consumers.

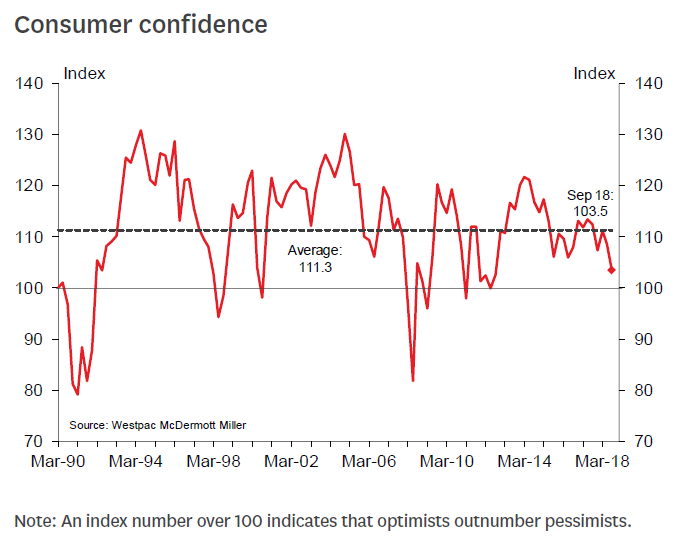

The Westpac McDermott Miller survey released on Wednesday shows the lowest level of consumer confidence as measured by that survey for six years.

Westpac economists say the drop in confidence "gives genuine cause for concern about how the economy is progressing".

To this, I would say while a survey is just a survey and people can have kneejerk reactions to what they see and hear and get grumpy about, the fact is the plunging levels of confidence will be a worry to a Government that was already showing signs of being worried indeed, if not to say rattled, by the falling business confidence.

The key thing is not so much that people get grumpy - but more what the grumpiness might lead to in terms of people 'shutting up shop', stopping spending, and otherwise changing their behaviour. It's this potential flow-on that then could have a big impact on the economy.

The latest survey will do nothing to dispel the thoughts and suggestions that New Zealand is starting to 'talk itself' into a downturn.

National's Finance Spokesperson Amy Adams said the Government doesn’t seem to realise its policy decisions "have an impact in the real world".

"Consumers have no confidence in the economic policies and management of the Government.

“There’s too much at stake to have a coalition Government learning on the job. Its anti-growth policies are having a real effect on how people view the economy which in turn affects how they behave within it.

“It means businesses are less likely to hire new workers, increase wages and invest. And consumers are less likely to spend as they fear the good times are coming to an end."

The knitty gritty of the survey is that the Westpac McDermott Miller Consumer Confidence Index fell 5.1 points in September, taking it to a level of 103.5. This is the lowest level for the Index since September 2012.

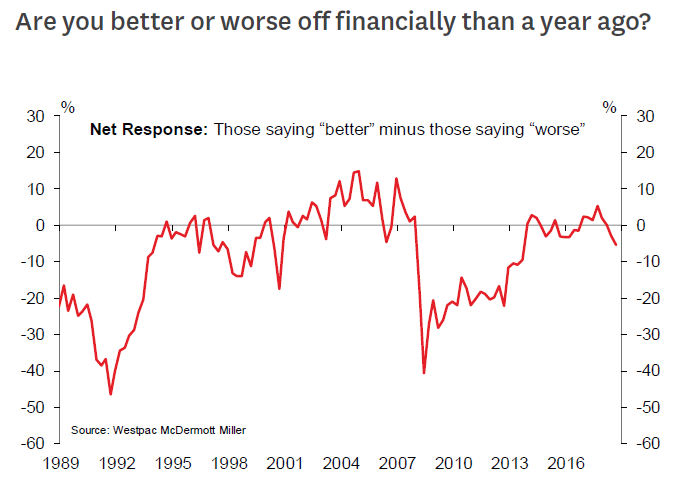

Westpac Chief Economist Dominick Stephens said New Zealand households are particularly concerned about the outlook for their own finances and the general economy over the next year.

"Expectations for their own circumstances in the year ahead are at their lowest, outside of an actual recession, in the history of the survey.”

Stephens said the groups that benefited from the Government’s Families Package, which took effect from 1 July, did report some improvement in their own circumstances. “But this appears to have been outweighed by other concerns in most consumers’ minds.

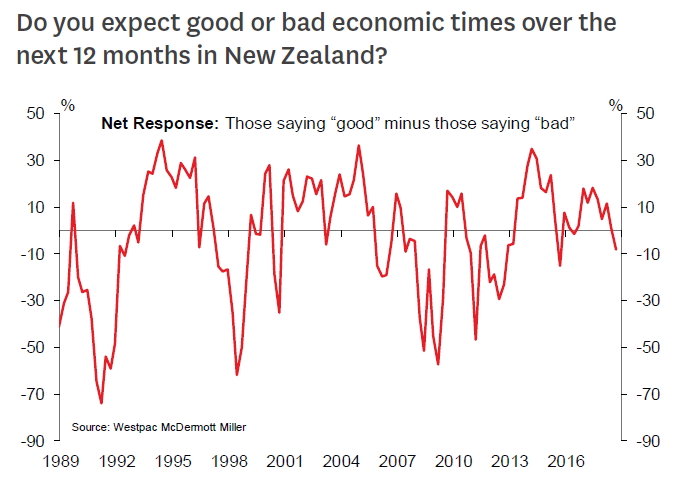

"The slowdown in the housing market and rising fuel prices are potential factors behind the drop in confidence,” Stephens suggested.

"Indeed, these factors have been felt most acutely in the Auckland region, which saw a particularly sharp drop in confidence.”

Stephens said it may be that consumers are starting to feel "a real impact" from the economic slowdown that began in 2017.

"...Or it may just be that consumers are worried by what they are hearing about weak business confidence.”

Managing Director of McDermott Miller Managing Director Richard Miller also noted that urban Aucklanders’ confidence fell further than other consumers.

“Those working in the private sector, in particular, seem to be losing confidence in the economy, and are not expecting to be better off financially in the year ahead. They are pessimistic for the first time since March 2009, with their Consumer Confidence Index falling 10 points this quarter to 98.5. In contrast, Urban Wellington Kiwis remain firmly optimistic, albeit a little less so than last quarter at a Consumer Confidence Index of 109.4.”

Miller stressed the contrasting confidence levels between those in the public and private sectors.

"Probing questions indicate that both private sector oriented Urban Auckland and public sector dominated Urban Wellington are diffident about the effectiveness of Government policies, but there is a sharp difference in belief about what drives their own region’s economic future. Wellingtonians have confidence in their people to create good economic times over the coming year, while Aucklanders expect population growth and new or growing industries to lift the economy."

The survey was conducted over 1-10 September, with a sample size of 1,556. An index number over 100 indicates that optimists outnumber pessimists. The margin of error of the survey is 2.5%.

In their detailed economic note on the survey results, Westpac's Stephens and senior economist Michael Gordon say the survey results "present a challenge to our expectation that the economy will regain some momentum in the short term on the back of Government spending".

They say that unlike business surveys, consumer confidence covers "the whole spectrum of voters, so it’s not obviously slanted based on who is in power". They point out that up until now, the post-election consumer surveys have been mixed rather than consistently softer.

"So the latest drop in confidence gives genuine cause for concern about how the economy is progressing."

142 Comments

A few predictions that I first posted on 9th September;

'Growth will turn negative in the first quarter of next year and NZ will be in recession by the end of the second quarter (2 consecutive quarters of negative growth). Australia will be suffering a similar fate and before Q4 of 2019 one of the Australian banks will be trying to tap its government up for funds to shore up its capital ratios (My money is still on Westpac because they've been bleating the most inconsistency over the last 4-5 months, albeit CBA could also pose an issue because of the size of their loan book). Interest rates will be rising by Q4 2019 to hold up a heavily sold NZ dollar.

Unemployment will hit 6% by Q2 2020 rising to a peak of 7.4% by Q4 2021. Reserve bank rate will be 2,5% by Q4 2020 and 3.5% by Q4 2021. House prices will fall 15-20% at the lower end of the market 25-35% in the middle and 40-50% at the upper/luxury end of the market. The bottom of the market will be 2023/24 a couple of years later than BLSH's prediction of 2021 but ready for his next upswing.

In essence a heavy top down correction because of tighter credit from banks and lack of cash from foreigners at the margin, many of whom will be forced to flee with big losses for foreign banks who didn't learn from the GFC and carried on lending big multiples of income and too much interest only debt.'

The housing crash will be the cause of this recession rather than a symptom of it and will induce a spiral of asset price deflation and reduced consumer confidence.

Dartboard predictions.

Interesting that you envisage the OCR going above the (anticipated) neutral rate in the face of rapid growth in unemployment. Especially seeing as the RBNZ mandate is now directly focused on employment outcomes.

If the OCR was to raise 175 basis points over ~3 years with the unemployment rate increasing 18% each year, it would be a bloodbath.

I am very doubtful that this is going to happen.

Just putting it out there that this one will be a biggie. OCR will have to go up because NZer's won't cope with a collapse in the dollar and it's inflation impact. Remember that most householders don't have a mortgage but on fixed retirement income inflation would kill them. The Reserve Bank is merely providing a stay of execution for borrowers to get their ship in order, it won't be able to hold rates down indefinitely.

Out of curiosity, what was your method for arriving at this forecast?

I think Nic is underestimating the resilience that our still fairly low government debt gives us during this slowdown. Given that, it seems unlikely we will be forced to raise interest rates in order to be able to finance a government budget deficit. However, you cannot really predict what will happen during a period of chaos. Personally I think guessing is underated and I have convinced myself that it gets better with practice. We sailed through the 1998 crisis without much unemployment, so that is my basic guess, possibly balanced by a surprising new low for the NZD.

Happy to recognise that government has a bit of leeway to spend but that can soon get sucked up with a couple of bail-outs. Fonterra not making any money, Fletchers struggling, a few building firms going pop, bit of cash for a few Universities and then an Aussie bank comes scratching at your door for cash. All of a sudden the government coffers don't look too good. Tomorrows GDP will be interesting (because I have a feeling the Jacinda will have got it wrong) but for me the July- Sept quarter will start to show the true picture if business lending figures continue to fall as they did in August.

None of us really know what will happen, but there are too many poor numbers for it not to be heading towards recession and pumping the economy with several billion dollars of debt for equity each month is unlikely to provide a cushion given the credit tightening going on in the market.

As for NZ dollar, the pain on consumers really hits at 50-55 cents and at that point rates will need to be looked at or we'll have the boomers up in arms again about losing money on their rentals and the cost of living- I can see all of that happening before the end of next year.

Hi Nymad

This is one of my favourite videos about banks. John Clarke and Brian Dawe explaining how it all works in a lovely simple manner. The sketch is several years old but the regulators stopped looking so it just carried on.

We’re due for a slowdown, the economy is cyclical after all. But the Armageddon you’ve described isn’t going to happen. Housing market flat until 2021/22, when upward phase will begin. I’ll be shocked if house values drop by more than 5% at the bottom of the cycle.

You’re going to have to change your username out of shame when I call you out on this in 2021/22 when things start to pick up again.

Let's see kiddo, when did you start building your 'equity empire' - 2011 I think you said, not even seen the full turn of the wheel before..

You make it sound like I was born in 2011! I graduated uni in 2009 and entered the job market in the depths of the GFC, so I've experienced the highs and lows of the cycle. NZ's economy isn't the Celtic Tiger you think it is.

What did you study?

Don’t be nosey Nic. I’m telling you my life storey over here while you won’t even divulge the general location of your “cottage”.

You know where my cottage is.

The wops?

A BA in Art History?

Bachelor of Interpretative Dance Theory

In 2011, Auckland prices had been flat for 4 years and that was pretty much exactly when the latest upturn began.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

I'm in the same position, graduated in 2007 in the UK and basically all I'm used to is rising asset prices. A whole generation of housing and share investors are in the same boat. When an actual downturn comes around we'll see how good our risk tolerances are.

To get an idea of what this can do to people, you might have noticed a few commentors even on here who refuse to buy shares because they still remember the 1987 crash. I know people in the UK who were turned off real estate because the crash in the early 90s put them in negative equity.

You can’t compare growth from this point compared to growth from 2011 because one is lower compared to fundamentals than the other. Rather you should pick the fundamental factors (income would seem key), measure prices relative to those fundamentals in 2011 then project to 2018 based on change in fundamentals. You’d probably find that current prices are semi justified by interest rates but very sensitive to either changes in incomes or prices.

Sounds like you have been brainwashed by one of those property investor gurus and their property clock theories if you believe prices are going to start rising again in 21/22 and that you have absolutely no idea what is happening both globally, Australia and in NZ with the credit and debt levels along with everything else going on. Seen you post this 21/22 prediction a few times on here and boy are you going to be in for a wake up call when it doesn't happen.

Ron Fong now keeps a low profile, BuyLowSellHigh, being one of his most devout disciples doesn't know how to stop.

Speaks volumes.

@retired poppy , debt could see the whole thing unravel

Boatman, I totally agree. It's just a matter of when. It's unlikely to happen in an orderly way either.

@retired poppy , debt could see the whole thing unravel

On Ron Fong now keeping a low profile ...

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

In many area it is already down by more than 5%

I can show you areas where it is up 5%. I can cherry pick you any result you want.

No cherry picking but is overall trend.

like it or not but for next few years housing market / boom is over. One thing is for sure that will not go up and will it be stable, is also a question mark (fall it has and will) and the only argument can be on the percentage of fall.

That only time will tel.

So wait and watch.This is just the begening and can only hope that is not drastic.

Yeah in many area is down by more than 10% but can safely says that is down by 5% (with some exception) and will be another 5% to 10% over a period of time is definite.

Many Vendors have realize it and all who were plaining to sell in near future are selling Now so will have more listing and also sold sign (As people who have to sell will sell at best available price, instead of waiting) specially in area where the non resident buyers were active and the same can be vouched by any real estate agent - Talk in coffee room.

Than why argue just wait and see as in few months, picture will be clear.

What are the suburbs where non resident buyers have been a large proportion of the buyers?

Wow, that's a very detailed forecast, and I agree with your baseline assumptions. Especially the housing price correction. As measured by the IMF, we are the most over valued housing market relative to wages in the OECD. Only a fool would buy now. I pity these self absorbed hot shots who put all their retirement savings into "property"; ie residential real estate in ONE small local metro market.

Overvalued does not equal price crash, or even correction. We've been overvalued for a long time, without a crash.

I'm not saying one won't happen, it's just there is no guarantee that overvaluation will lead to one.

Hope you're wrong. But I'm not optimistic either. My guess is that things will get worse but not as bad as you predict.

yeah that's my central view too.

the Black Swan is a global financial crisis.

@Nic , I also think there will be a recession , BUT I dont see a housing crash , the backlog demand is simply too great , Immigration still too high , interest rates too low , and Council too incompetent to open more land for development .

@Boatman. I agree that demand is great in terms of need and want, after all who wouldn't want to own their own house, people always talk about massive demand but demand has a price element too and with mortgage credit already being squeezed back by around 20% in terms of what buyers can access compared to earlier in the year and that is likely to go further, then that will have a self fulfilling impact on the market.

I would put to you that demand for Aston Martin's is also 'simply too great' and would guess that most people reading this would absolutely love to have one of their own. Why don't we all have one - price!

I think you will find that demand for houses is actually getting weaker by the minute and it won't improve until there are significant changes in price.

@Nic , I concur , price is a major factor . We have one son ready to buy , but I have told him to sit on his hands becuase the prices are simply not anywhere near realistic , he is not homeless and has options .

I dont see prices softening in any meaningful way from the evidence I have seen so far .

You're a smart man Boatman as you've just shown with your comments on the Fonterra debt debacle. While you don't want it to happen because of your commitment to your business and it's people...deep down you know it is going to happen and that it cannot be avoided.

Your advice to your son shows that you know what's coming, I've given the same advice to my kids, this market correction could bring prices back a decade and although many of us will lose a fair bit of 'paper wealth' from our properties, it's only a problem if you planned your life on it.... I still think for most people a home is a home. Others that went a bit silly borrowing will just have to put their heads down and pay it off.

A lot of immigrants are here simply to send half their pay back home. When the dollar is worth nothing and the work dries up why wouldn't they go back home?

Permanent residency. In a world wide recession our welfare state will keep them here.

Essentially you are predicting a NZ GFC similar to the US/ Europe. These models would indicate a declining OCR with declining mortgage rates. Likely in this scenario a 10-20% fall in property prices. With those able to access credit/ large cash reserves, purchasing positive cashflow properties in good areas.

Early 2000s NZ dollar was down to 38c US, there were no major problems. One of the main concerns was exporters being able to cope with the eventual rise in the NZ dollar. NZ is better placed than previously as over 70% NZ bank funds are sourced domestically.

Hi mja

I don't think we can lower rates any further without collapsing the dollar. There are numerous factors that have created the bubble in the Southern Hemisphere, low rates, high immigration, lack of building etc etc but the big factor that seems to escape everyone is that whilst rates dropped across the Western World, to prevent a deflationary depression post GFC, what happened elsewhere is that controls were set by the Governing Banks to control access to credit in the post GFC era. In the UK and US lending restrictions were put in by 2010. The low rates were used to encourage the repayment of capital rather than it's massive expansion and lending restrictions such as 4.5 times household, removal of interest only lending and equity requirements with the best rates preserved for 40% equity borrowers all helped to temper what would otherwise have been very tempting cheap debt - London's top end market has barely moved in 10 years.

In contrast no such restrictions were put in place here and that is why we are where we are. Household debt will break the economy and the same will happen in Australia and unlike last time rates have no downward legroom to save it. If anyone is responsible it was whoever was preventing the Reserve Bank from putting the brakes on with more tools to it's armoury.

Low reserve bank cash rates/ quantitative easing do not necessarily lower the value of the currency. Note John Mauldin borrowed in yen once Abe announced Japanese QE, only to see the yen appreciate, and lose out on the deal. Unfortunately he lived in the world of what ought to happen. Soros first discovered this anomaly that does not gel with economic theory and made a large sum with some currency trades. This occurs as the lowered cash rate/ QE points to an improved domestic economy and creates currency demand that outpaces reduced demand from those purchasing currency to purchase bonds.

In markets what ought to happen typically does not happen.

In early 2011, amidst the doom and gloom about falling property markets. I was building a large fence by myself, and had plenty of time to think. And I thought what is the thing that in 2020, you think how did I not see that. At that time I decided property was a buy as there was a good chance we would have declining interest rates that would support property prices and make negative cashflow properties positive cashflow, upping prices. I did not anticipate that level of property price appreciation. But this one call has made all the difference in securing myself and my families future.

So what is the call for the next decade? Start with what do monied interests and governments want. In general they want the status quo to be maintained, as the present situation suits them fine. I see interest rates being driven down at any signs of recession. For NZ the debt load in Auckland (see low consumer confidence emanating out of Auckland cf Wellington), locking in poor retail spending in Auckland and ensuring rest of country benefits from low interest rates even if these are not required. So Auckland (and to a degree Hamilton and Tauranga will have low growth), whereas other centres especially Wellington, Christchurch will benefit from artificially low interest rates. Low term deposit rates will drive money towards income producing assets for retirement income. This should also benefit Wellington and Christchurch property prices.

The Rock Star has a hangover!

"Give him some more cocaine, that's what he needs" goes the cry.

Laxatives seem to be the current drug of choice and it's all coming out now. Housing market appears to have had an enema as well, with all sorts of crap hitting the market.

Not for Rock Stars surely? I thought they preferred amphetamines or cocaine, but then, I don't speak from experience.

Hangover or in need of debt de-tox ?

Still mildly positive but heading in the wrong direction for this Relentlessly Positive govt with the gung-ho approach shoving through agenda. Ardern will blame it on other factors and wheel out a mouth piece to say its national voters but this is a message for them to wake up and start moderating some of their proposals. The announcement banning future exploration, whilst appealing to a few extremists, will have a wider impact than they imagined.

I think we were heading in this direction anyway, but some of their policy implementations have given us a shove downhill.

The oil exploration ban had bugger all effect, it was a piss-poor performance, but actually changed bugger all.

Not to the people who allocate the truly massive amounts of capital that such real, productive investments need. They are a giant red flag, saying "Go Away, We Want To Be Poor".

So we desperately grovel to attract investment in low productivity faux investments like casinos and hotels and sell our housing stock to new residents, preferring scussy rental and homelessness for own people. We encourage our children to move to the Land of OZ where riches can be earned from mining in all its forms. This is the Kiwi Way. There is always a price to be paid.

I'm just going by feedback from a mate who works out there, in the oil industry. I'll get an update this weekend when I catch up with him and his lovely wife, but even tho he is a staunch national supporter and his job is entirely dependant on the offshore oil & gas industry in the 'Naki, he admitted it made bugger all difference in reality. The exploration has already been done in the areas they thought were worth investigating.

Thanks for the anecdote. I take anecdote seriously, so, darn it, your evidence refutes my theory, at least partially. I have to retreat to the fallback position of "not yet", in a knowing and serious tone.

I'll take his coal-face experience over your hand waving anyday.

Scientific fact is nothing more than a collection of anecdotes observed to be true.

So I'll add mine as well (also in the industry in the Naki)

Investment, etc... peaked in about 2008. Most of the offshore seismic is coming back with little to nothing of value. This is why most of the permits have been returned, lapsed, or only having the minimal required work done under them.

Further investment in exploration before the announcement was sketchy at best. They have a fairly good idea of what is around NZ. We do have reserves, but none of them are technologically/economically viable for maybe 50+year if at all.

Given most forecasts have us at maybe 15 years (+/- 5) of current reserves. We would have run out before the ban has any major impact anyway.

Operationally the industry will continue on as though the ban had never happened until the gas/oil runs out.

Politically though it was a disaster. They satisfied a few thousand voters at the cost of alienating just about every single business Domestically and internationally.

It turns out "Shutting down" an industry overnight with little to no thought, consultation, or alternatives is completely idiocy and sends out only one message "Who's next?"

The O&G shutdown, plus the murmurs aboot No Mining on Conservation Land Evah Again, will all play into a longer-term impact, IMHO, Roger.

Consider the education and career prospects in Godzone for a kid who's shown promise as a rockhound.

Why bother here, with a science/geology/engineering-with-a-mining-twist course of study? Better to up stakes, head over the ditch, and study/graduate/work there.

"Oil industry bidding for new exploration permits was set to be the strongest in years in 2018, industry body Pepanz claims, with government officials seeing a sharp upswing in interest.

Documents released under the Official Information Act show the petroleum and minerals team at the Ministry of Business, Innovation and Employment (MBIE) was receiving more interest from oil explorers at the end of 2017 than it had seen since at least 2012."

https://www.stuff.co.nz/business/104974545/oil-industry-claims-before-b…

Mining is very sensitive to commodity prices. The size of the resource tends to go up exponentially with price as uneconomic areas become profitable and as more areas become accessible. The resource is not fixed, it is price dependent.

You are preaching to the converted. Just pointing out the fact exploration in the country was not at an end anyway as some like to suggest.

I really don't think the double whammy on Auckland petrol prices was a smart move. Saw Goff on TV raving about how good it was that he had $13 Million in the first month to spend. Well that's $13 Million that is not gonna get spent elsewhere, of course it has crimped spending. Almost certainly this was very poorly timed.

Goff. The palestinian terrorist hand holder. That shocked me. It was a long time ago but never forgotten.

Poorly timed and a poor policy, put in place as it was to avoid raising rates on properties that have received significant value increases from the activity of the city and communities surrounding them. Instead, forcing poorer folk to foot the bill.

The $150 million collected per annum from fuel taxes in Auckland goes into a slush fund which will then be drip fed into developing transport infrastructure.

CCNZ (Civil Contractors NZ) made a submission to MoT last month on how the government's rethinking over major road projects in favour of mass and rapid transport options will lead to a serious downtime in 2020-2023 period. This means there are reasons to believe major project won't hit the ground till late 2022.

You don't need to be a rocket scientists to join the dots here: benefits from the money currently squeezed out of NZ households in fuel taxes won't be visible for years.

Reasons for concern: yes!

The direct transport benefits maybe not.. but that money sitting in the bank will help offset some of the $8 billion of debt they are paying interest on. in fact the fuel tax might just cover the interest.

FD interest on $12-14 million installments a month compounded to cover interest payments on $8 billion in debt? Also, you mean Aucklanders should rejoice for the fact that every $100 extra they pay in fuel taxes will relieve their rates bill by $4 (at best)!

I think the only way that pool of money from fuel taxes covers anything but a minute portion of interest payments on the $8b debt pile is if the money were to sit with a hedge fund manager, not a bank.

No, I meant the revenue from the fuel tax will in all reality be spent paying the interest on ACs mountain of debt... then they will borrow more when they need to fund actual projects. They are a hopeless bunch of spendthrifts who don't have the balls to just raise rates to the level they need to.

This Fuel levy was expressly raised for NEW PROJECTS we will not stand by and just accept the funds being whittled or frittered away , going into servicing existing debt or inflated salaries .

Goff can go ................ himself if he thinks we are going to let this happen

The revenue from this regional fuel tax is strictly earmarked to be spent on the 14 or so projects as specified under the Land Transport Management Order 2018 . So the council would be breaking the law if it were to use this money for BAU.

http://www.legislation.govt.nz/regulation/public/2018/0103/latest/LMS52…

Maybe he can upgrade from business to first class on his next junket. Meanwhile morning traffic volumes seem to be down on the Northwestern in the last few months. If people have an alternative to driving they are starting to use it. Would be interesting to see stats from fuel industry on actual liters sold in Auckland pre and post tax.

I drive to Albany from Greenhithe to work. Even with road works starting for Consta Dr traffic is much lighter in the past few weeks.

Toughen up. Wellington is still paying around 10cpl more than Auckand. And that's without a regional tax. I suspect we continue to subsidise the more competitive areas.

@Markl The last time I checked , Auckland was not Wellington , dont compare us .

Wellington is one massive sheltered employment experiment , almost everyone there ss on the Government payroll

We in Auckland are not a city that relies on its entire income riding on the back of the rest of New Zealand, we actually work and make stuff here

How do you feel about the South Island? We pay about the same as Auckland now you've got the extra levy. We certainly didn't enjoy subsidising your fuel in the past.

I doubt we were subsidised by you . The cost of transporting fuel is real , and given the low population and distances the price is not surprising

It's more to do with the national chains charging more down South to compensate for their more competitive pricing in the North. Sadly the drivers of this competition haven't set up shop down in Chch just yet.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

91 unleaded. The peoples fuel comes pre refined ex Asia via tanker to Marsden Point were it is sent down a pipeline direct to the Wiri Terminal and distributed a relatively short distance to the 100's of service stations in the Auckland area to service the 1.5 million population. Of course it should be cheaper. It's simple economics. Vs the cost of sending it via coastal tanker from Marsden Point to terminals and stations all over the entire South Island with a population of 1 million. If anything Auckland subsidises the rest of New Zealand.

To be fair, an Aucklander shouldn't be the one saying this since Auckland does not produce anything of international value either. NZ's exports are generated in the regions - dairy, wood, tourism, fruits etc. The city hogs a lion's share of what the rest of NZ produces with little value addition. Much of your businesses rely on income from low-value services at eye-gouging prices to migrants generated with the help of migrants.

On your point about the government of NZ, which for all its flaws is more efficient and capable than Auckland Council. Our government is number one in the Global Transparency Index but I wish we could say the same about AC.

My walllet is firmly closed , but to be fair its not ALL the fault of the COL Government

I am not comfortable that we are not facing some kind of recession or global shocks with Trade wars , unresolved debt issues in the EU , us Kiwis blocking foreign investment from China , and falling commodity prices .

Messing with laws that are actually working in the area of labour legislation and litany of ongoing strikes, industrial action and labour disputes is another factor that is concerning and which reminds me of the awful 19070's is another thing that is a worry ...................... just like the Vietnam War.........we dont ever want to go back to those days

A big factor is that I dont trust this Government one bit .

New taxes and levies at every turn , summarily banning whole sectors of the economy without a hint of consultation , messing with kids futures whose parents are trying to get them into the best schools , social engineering with the families package ( just tax them less! ) flipflopping and disagreement as to whether we want the criminal element masquerading as refugees that no one wants on Manus Island , policy logjam , major policies that have no traction such as Kiwibuild/buy/rent/flop/buyoffplan which was wishful thinking to start with ........the list is endless .

It's not just here! From Aussie, yesterday....

"My father has been involved in retail since 1949, and he thinks August was the quietest month in 70 years"....People are focused on essentials...."August wasn't very good [for us], and September so far has been a little bit worse actually,"

http://www.abc.net.au/news/2018-09-18/retailers-take-action-after-sales…

Yes, it's anecdotal, but at some stage, it translates into statistics!

There was a great Australian 60 Minutes segment that somebody linked to yesterday (?Nic) about the property bubble crash that's appeared to have started over there. From the documentary interviews you get the impression that Australian's seemed to suffer the same delusion that 'property prices only ever go up'. Pretty naive really. I could have sworn I've heard things said like this somewhere before...

60 Minutes Australia - Bricks and Slaughter:

https://www.youtube.com/watch?v=smPR0s2W-Ck

Anyway, I'm sure it's doing wonders for confidence at the moment.

What struck me was the naivety of some of those interviewed like the 70 year old with investment properties all on interest only mortgages and now the bank is asking him to pay principal.

How can anyone feel sorry for this guy, he’s taken a big risk to get rich quick through capital gains and his plan has fallen apart.

Especially when they didn't budget for the payment increase. People don't realise what the debt recovery teams at banks are like.

We've got a lot of them here too and some of them are as young a 31.

Johnathan Brownlee - 11 Properties at 21 years old, valued at $3 million.

He's created $1m in equity and expects to pull in more than $60,000 per year in after-expenses income once he finishes his next renovation.

Will be interesting to see where he is in a couple of years time.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Just wait until his fixed terms come up and the banks tell him he must move to P & I.

Prime real estate that Flaxmere. Get in there TTP and BHSL.

From the previous article:

Now he has 11 properties in Wellington, Hamilton, South Auckland, Hastings, Dunedin, Masterton, Whanganui and Invercargill - having chosen to hold onto all of them rather than sell.

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12102563

Quite a territory to service, particularly to make $60k on a $3 million portfolio (2% return). I hope his tenants in Masterton don't do a runner on him like what happened to the rental around the corner from us. Sat empty for 6 months, tenant owing $4000 (only $900 rent arrears).

Don't think its just isolated to Australia. After the boom here. There will be a ton of those same people in NZ. Over leveraged to the max because they wanted to make a quick buck or didn't want to miss out. And because of them & the banks lending where they shouldn't. They're ultimately the ones going to reduce the value of the market for the wider populous. Get rich quick more often than not always ends in disaster.

That old boy John should never have been let out of the pokies room and god knows what was going on when they gave him access to that much credit at his age. Mortgages should have a lifespan as they do now in the UK and US where the final date for repayment of all capital is when the borrower turns 65 (retirement age). But lending in the Southern hemisphere is diffrunt.

DFA is always worth listening to. Use of actual statistics is good and the interviews with those in the Australian mortgage market are very interesting. The rebalancing of Westpac's mortgage book in Australia is also very interesting.

With 60 minutes interviewing DFA that's a sign that the tone in the property market has changed substantially over there.

Oh well , everyone will be pleasantly surprised when things get better.

Everyone loves an optimist

Just ask yourself what can the government do to stimulate the housing market if it goes down much further.

They are making changes at the reserve bank in preparation. Power is very addictive and home owners vote.

It's about balance though, eh...A government that used land tax to break up land banks was voted in to power in NZ when too few average Kiwis could access land. If home ownership continues to fall enough then enough voters will have a mind to seek policies that help them more than they protect landbankers.

Over the past 1 year , we have seen this hapless Government either lurch at lightening speed, or lethargically bumble form one self - induced crisis to the next .

Banning Oil and Gas was done at lightening speed has reached crisis point and has gutted confidence in the way it was done .

The Auckland fuel levy is sucking a quarter of a Billion dollars out of the Auckland economy to go on Council salaries , and there are already unintended consequences

The lethargy over dealing with pay disputes (and industrial action) Kiwibuild and the illegal under-age drinking at a Labour Camp, is just astonishing .

We are in policy limbo over just about everything , from the "so-called" refugees on Manus Island ( people which Australia does not want for very good reasons ) to things like sorting out education .

Education Policy is being formulated on the fly , and its going to end badly

Kiwibuild is a joke , thats not even funny anymore , its now an absolute fiasco

And all they have as a response is ...............For the past 9 years .........blah blah blah

The coalition partners seemingly dont agree on anything and we need to ask where is will end , It all adds up to an appalling state of deficiency , mismanagement , and negligence and a lack of leadership

Feel better after getting that rant off your chest? I hope so, cos otherwise it served no useful purpose.

@pragmatist , call it a rant or whatever you like , its a shambolic state of affairs and its going to hit us all in the pocket eventually , starting with the poor .

We are now in trouble. The news regarding consumer confidence confirms that our economy is about to tank.

Our business has a couple of large capital projects on (committed to under the prior government). Once these are complete we will put all capital expenditure on the back burner. Similarly for any home renovation that we have underway.

Between JA, the COL, and Goff they have killed the economy. Totally self-inflicted.

Correct , we are likely to end up in a recession if we carry on down this road , and as you rightly point out , its 100% self - inflicted

In just 1 year taken the economy and done everything possible to wreck it, spectacular by any measure .

That's rubbish. Government policy has only been part of the reason for the confidence fall away. There are cyclical factors at play too.

dream on Fritz. Read the business section. Compare it to 12 months ago. Then have a think about what might have happened in the intervening time... and join the dots.

The economy was starting to weaken anyway.

I agree the government's policies have weakened economic sentiment, all I

am saying is that it is highly unlikely that the government is solely to blame.

I think that is a totally reasonable and accurate position.

when an economy starts to weaken, is not a time to "double-down" and make things more difficult for both business and consumers. Should we go into recession, and that is looking more likely by the day, then the government will need to "prop up" the economy. Inevitably this means ensuring the government takes on risk, and more debt. In order to do this the Crown needs to have a very strong balance sheet. With the lolly scramble Labour have dished out, and what I see as poor quality spending the Crown accounts have eroded over the past 12 months. Having an inexperienced PM (on financial matters) at the helm is a disaster of epic proportions. I hope for everyone's sake a financial tsunami is not heading our way.

When John Key himself came out and acknowledged that the economy was built on cheap credit, massive immigration volumes, and rising house prices...You are not giving enough credit to the architects of the current issues, over and above the lot who have inherited the economy built on those factors.

Nothing to do with the architects of the problem Rick. NZ is in a similar boat to most other western economies - Australia included. National failed miserably at controlling house price inflation. However in Keys defence so did just about every other western country around the globe. My gripe is that JA is woefully inexperienced in financial matters - she admitted that just yesterday. I therefore have no confidence in the current government.

ICYMI - a recent talk by John Key

https://www.facebook.com/TaxTraders/videos/1160405714117471/

The economy is important but so are other things.

In my opinion social outcomes have been sacrificed too often for economic ones. If there is a bit of economic damage that comes from that, so be it.

Cyclical alright. Labour get in every 6-9 years.

The cyclical factor is that every 10 years or so the NZ electorate forgets how damaging Labour is when in power. Every labour government since the 1960's has left NZ in recession for incoming National governments to fix.

Insanity: doing the same thing over and over again and expecting different results.

Today I learned Labour caused the GFC.

To help your education: Clark/Cullen had NZ in recession from the 1st quarter of 2008, 9months BEFORE the shit hit the Lehman brothers collapse ushered in the GFC.

Indeed. I picked up signs of trooble-at-mill in early 2006, then got an absolutely stupid offer out of the blue on the old shack, took it, paid everything off, and downsized. Best move we ever made. The signs were all around for those without political blinders on....

That's rubbish. Government policy has only been part of the reason for the confidence fall away. There are cyclical factors at play too.

Re "cylical factors", you would probably would be better to refer to "structural factors." And this is a global, well particularly Anglosphere, issue. Money creation and the manipulation of the price of money has spawned massive economic fragility.

You could talk yourself into failure if you love public self- flagelation. However, like many other small business owners(who are proportionately the largest employers) my business turnover and profitability is increasing, particularly this year. But don't let good stories stop you.

Does anyone have an idea of how much of Wellington’s economy is driven by govt spending, consultants and associated taxpayer funded analysts? That would probably explain the higher confidence figures I believe, and just the product of big govt squandering our precious taxes.

@Ludwig , correct , If you were a Government employee and money just arrives in your bank account every fortnight , as it has always done , you would also be more confident than the bloke who actually has to do something to earn his keep .

This survey hasn't asked the right question.

Try asking if your grandchildren will thank you for what you've done in the last year.

Foget about counting casino-chips - there's already too many of them and the music is about to stop.

Consumer confidence down - bank profits up.

Perhaps there is a correlation.

Creaming it while they can.

The time has arrived for the big crash. Watch out for blood in the streets bhuahahaha!

希望房价永远的倒塌下去,永不翻身,呵呵呵。

Double-GZ. - Did you lose your R.E Job ? Glad to hear you have seen the light, but what ever happened man ?

跟这边1线2线城市一样,南京二手房已经卖不了了。

Funny, we sold ours without any problem.

Really? We have had my mother-in-laws house on the market for six months in Nanjing and have lowered the price twice already.

Yes, but I suppose it had some fairly unigue features, 4 double brm, 3 bathroom, 2 living areas, private courtyard and around 200sqm. A family member also sold an apt near FuZiMiao recently. If is ain't selling the price is too high.

NZ politics, consumer confidence, price of gas, energy, property prices etc has an impact but it's not as material as the state of the global economy - our wagon is hitched & we're not at the helm.

Bring on Brexit, unintended consequences from US isolationist policy, Italy's default, Australian banking crisis, Argentina's collapse, massive withdrawal from the ECB withdrawing from the purchasing of 30 billion euro's of assets per month (ECB owns 2.4 trillion in assets now).....it's like black swan hunting season.

Consumer confidence should be dropping, it's a freakin massive debt mess that could unravel.

Boatman, whybare you not spending?

We are the total opposite, in that we are spending on improvements to property to lessen the tax bill!

What has gone up is the insurance on property.

Just got insurance this week on an As is where is property and it was over $1700; has increased the value however by plenty, so I suppose not too bad!

Off overseas tomorrow for well earned break, as you know it isn’t always easy beingva provider of accommodation for people, even though Twyford may think it is!

You're hilarious. I'd believe you legitimately cared about providing accommodation if your purpose of spending was to improve the living conditions of your tenants rather than tax avoidance.

I guess you've come to believe your own lies.

He's a genuine case study in Narcissism.

What's the bet he'll continue to comment on here throughout the duration of his "holiday" like when he was in Australia a few months back.

He's probably not going anywhere, he'll set his alarm clock for some crazy hour in the morning so he can get up and comment on Interest so people think he's in a different time zone.

I think he means he's going to Wellington.....obviously to help needy kiwi families by getting them signed up into ghetto rentals for sweet profit and altruism.

"... so people think he's in a different time zone". That implies at some point he was in the same time zone as the rest of us.

.

Any comments on the stockmarket?

To quote Amy Adam “It means businesses are less likely to hire new workers, increase wages and invest. And consumers are less likely to spend as they fear the good times are coming to an end."

yes, indeed, because a country cannot rely on debt to sustain an economy forever.

If you fancy a laugh - check out Tommy Tiernan's "when the Irish had money"

https://www.youtube.com/watch?v=EUo93Hw7LSw&lc=UggtewuqznTTP3gCoAEC

New Zealand needs to take notes from what happened to Iceland and how their economy hit the dirt due to them rolling on unregulated free credit. Sounds familiar.

Just think both NZ and Oz have benefited from lots of money pouring in from Asia (Mostly China) over the last ten years and now that tap has been turned off. So of course we have to build an actual economy rather than relying on dodgy money and credit.

BBC article; Iceland: What Happened Next?

https://www.bbc.co.uk/programmes/w3csxhj3

New Zealand is different to Iceland.

Did you even take a listen at the BBC article Zachary? I'm sure you'll recognise a lot of similarities to what happened in Iceland has happened here to cause their economic downturn.

By the way, how are the baked beans, I'm sure you'll be stocking up now with the prolonged Auckland property value drop.

The government spends on all and sundry and people who work and businesses pay for it. No surprise confidence is low

Why won't any one comment on the sharemarket?

Because in NZ it is all about term deposits and property speculating.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.