Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE/LOAN RATE CHANGES

Kāinga Ora/HNZ have raised their 2, 3, and 5 year fixed rates.

TERM DEPOSIT/SAVINGS RATE CHANGES

NBS has raised a range of TD rates today.

SUCCESSFUL DECELERATION

Annual inflation fell unexpectedly quickly to 5.6% from 6.0% previously. Some falls were chunky, leaving housing and petrol prices the largest contributors to inflation during the September quarter. Both tradeable and non tradeable inflation fell and at about the same sharpish rate. This result suggests the Reserve Bank's interest rate rises of the recent past are working and that the threat of more rate rises are now much less. The OCR migh now be on hold for a while.

FAST PACE & ACCELERATING

Almost 200,000 people arrived in New Zealand on work visas in the 12 months to September, and in the month of September, work visa arrivals shot up to almost 20,000, indicating the fast pace is actually picking up.

MORE HAWKISH THAN EXPECTED

In Australia, they released the minutes of the last RBA meeting today and they were somewhat more hawkish than expected. They might raise fears that the RBA may be inclined to raise rates again which would be a 13th rise since they last fell. "[M]embers noted that some further tightening of policy may be required should inflation prove more persistent than expected." They have a target of "between 2 and 3 percent". The last monthly inflation indicator was 5.2% in August and the next one is released for September on Wednesday, October 25, 2023.The RBA next meets on Tuesday, November 7, 2023.

SWAPS ON HOLD

Wholesale swap rates have probably not changed much again today. But the real reaction will come at the close. Our chart will record the final positions. The 90 day bank bill rate is down -2 bps at 5.69% and now only +19 bps above the OCR. The Australian 10 year bond yield is back up +7 bps from this time yesterday to 4.54%. The China 10 year bond rate is up +2 bps to 2.73%. The NZ Government 10 year bond rate is up +1 bp to 5.46% from yesterday, but still above the earlier RBNZ fixing of 5.39% which was unchanged today. The UST 10 year yield is up another +6 bps from this morning at 4.72%.

EQUITIES START WEAKER

The NZX50 is little-changed, down -0.1% in late trade. But the ASX200 is up +0.5% in afternoon trade. Tokyo has bounced back strongly following Wall Street, and is up +1.4% in opening trade. Hong Kong has opened up +0.8%, and Shanghai has opened little-changed. Wall Street closed higher in Monday trade with the S&P500 up +1.0% and the NASDAQ up +1.2%.

GOLD SLIPS

In early Asian trade, gold is now at US$1916/oz and down -US$6 from this time yesterday. Earlier in New York it closed at US$1920/ox, and earlier still in London ir closed at US$1918/oz.

NZD WEAKER

The Kiwi dollar has changed little- since this time yesterday and still at 59.1 USc. Against the Aussie we are down more than -½c to just under 93 AUc. Against the euro we are soft at just under 56 euro cents. That means the TWI-5 is down -30 bps at just on 69.3.

BITCOIN LEAPS

The bitcoin price is firmer again today, now at US$28,323 and up +4.0% from where we were at this time yesterday. And volatility over the past 24 hours has been extreme at just under +/- 5.2%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

64 Comments

US 10 year yield vs market events:

https://pbs.twimg.com/media/F8VlqO9aQAAAOuz?format=jpg&name=medium

This is a wartime borrowing spree. Perhaps not too dissimilar to post Vietnam War path for interest rates.

It might be that the RBNZ has to just sit back and just watch our fixed interest rates go north with the global cost of debt.

Any attempt to reduce interest rates while wartime financing is in full swing, well, the RBNZ's war chest is only so big to prevent our currency from freefalling.

In light of events still unfolding, I think it's foolish to dismiss Higher for Longer.

Yip fiscal deficits are like we are at war - and then we wonder why we have such high inflation!

And yet if we stop spending like drunken sailors, the economy will crumple into a deflationary hell hole.

Problem - too much debt relative to productivity/economic capcity.

Resolution - reduce debt levels to more sustainable levels.

What are we doing - creating even more debt! i.e. digging ourselves into a deeper hole, requiring more future inflation (increased money supply/currency devaluation) to prevent debt defaults. Its a crying shame as it didn't need to be this way.

To put things into perspective: US Treasury auction sizes will in 2024 increase on avg 23% across the yield curve due to higher deficits and debts. (via Apollo) Link

Yip I look at that chart above and a US fed funds rate of 8-10% is feasible over the next 5-10 years (don't know dates/timing). Could go even higher.

Rates could drop during recessions, but the overall trend could well be the reverse of the last 40 years.

My responce to the 8%-10% Fed Funds rates is what my old solicitor from King Country used to tell me: "What can't happen-won't happen".

A 4-5% OCR was considered impossible a few years ago.

'The housing market and economy wouldn't tolerate it'.

My view was more open to possibilities to avoid being caught out.

I am in awe of the pace at which you put these briefings together David, but the bond data is incorrect. Non-residents hold 58.5% of the $136bn bonds held in the secondary market, which is $79bn. The $180bn total figure I think you have used includes some of the bonds owned by the Crown (RBNZ and EQC).

Our trade deficit leads to overseas investors holding NZ dollars in cash - makes sense to swap those dollars for interest-earning NZ bonds I guess.

Thank you.

"Country Garden's entire offshore debt will be deemed to be in default if China's largest property developer fails to make a US$15 million coupon payment on Tuesday (Oct 17), the end of a 30-day grace period.

Non-payment of this tranche is set to trigger cross defaults in other bonds as is standard in bond contracts."

https://www.channelnewsasia.com/business/country-garden-bond-coupon-pay…

The 90 day bank bill rate is down -2 bps at 5.69% and now only +19 bps above the OCR

The overnight interbank cash rate is ~5.36% - 5.38% and below the 5.50% OCR.

RBNZ issused $900m bills today to add to the $700m issued last Thursday.

Now, that's getting interesting.

The UST 10 year yield is up another +6 bps from this morning at 4.72%.

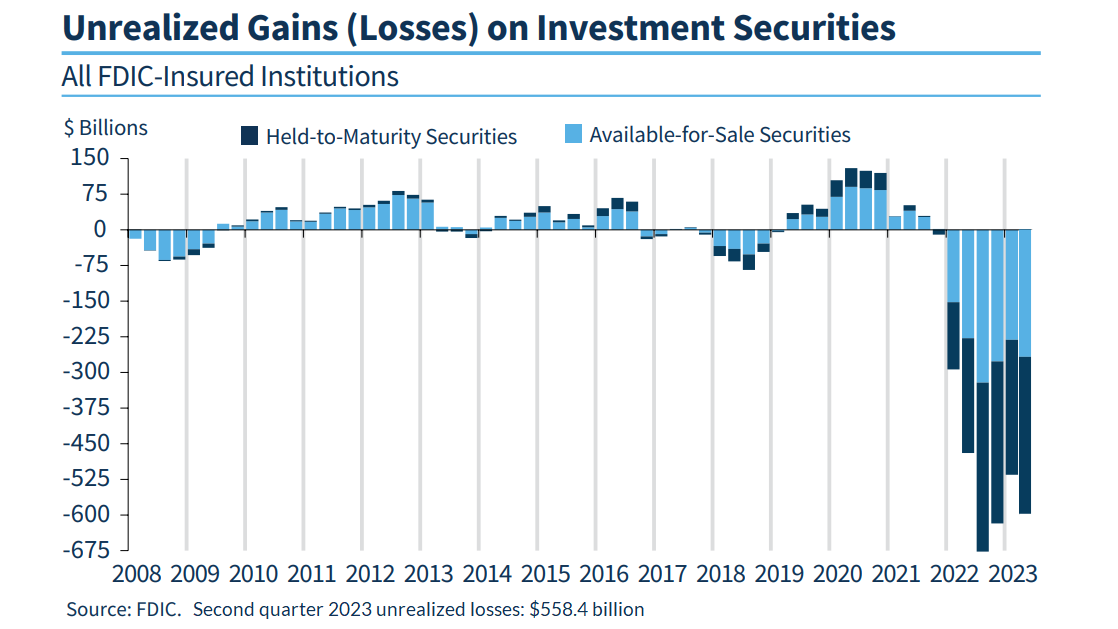

Balance sheet losses and debt burdens

Adding to the “skeleton of instability” created by rich valuations and unfavorable market internals, the chart below shows unrealized losses in the U.S. banking system as of the second quarter of 2023. Notably, 10-year Treasury yields have increased from 3.8% to 4.7% since then, so this profile has undoubtedly worsened in recent months. According to the latest FDIC quarterly banking profile, over 40% of U.S. commercial bank deposits are uninsured – a consequence of a Federal Reserve policy that forced trillions of dollars of reserves into the banking system.

Meanwhile, things are not going well inside the Federal Reserve’s balance sheet. By our estimates, even giving the Fed credit for all the interest it has returned to the U.S. Treasury since it launched quantitative easing in 2008, the Fed has lost nearly $750 billion dollars, at public expense. Excluding interest that the Fed has remitted to the Treasury, the actual hole in the Federal Reserve’s balance sheet – liabilities in excess of assets – is close to $2.5 trillion. In effect, the Fed has created government liabilities that are no longer backed by corresponding assets, as the Federal Reserve Act intended.

There is no immediate legal or regulatory consequence to this, but the public should understand that this hole will be filled by the Fed over time, by retaining interest that would otherwise have been returned to the Treasury for public use. For a full discussion of the difference between illiquidity and insolvency (the Fed is not illiquid, but it is most certainly insolvent), see the September comment, Central Bankers Wandering in the Woods.

{kind=link}

Yip people keep talking about our CPI in NZ but if you want to know where the world is heading you need to be watching the US 10 year yield. And it looks like its broken out of a 40 year cycle (downwards).

https://fred.stlouisfed.org/series/DGS10

The 2/10 yield inversion is starting to normalise as well - so watch this space for potential recession the next 12 months or so.

Non-tradable (imported) inflation excluding petrol dropped to just below zero this quarter. Yes, below zero.

Non-tradable (allegedly 'domestic') inflation was almost all due to local govt rates, insurance, public transport (end of subsidies), and rent (driven by Auckland booming at over 9%).

Now, for those still begging for higher rates, please explain slowly how they will help moderate price increases.

There's a feedback loop Jfoe - and we have perhaps just exited a 40 year feedback loop cycle where falling interest rates created cheaper input costs for goods/serivces and showed up as deflationary pressures for central banks to fight - which they did by dropping rates further and making the issue even worse.

Now the shoe might be on the other foot, where raising rates to fight inflation, just creates even more inflation, which results in even higher interest rates.

But the problem is the amount of bad debt that is extended while interest rates are dropped below what would have been a moderate/neutral setting - and I'd argue that we've had a lot of that 2008 - now where we were in stimulus mode to 'avoid deflation' that was created by dropping interest rates too low.

What we could have done post 2008 was increase interest rates to create inflation (when we were fighting deflation) and it would have reduced the quantity of debt that was extended and not be in this predicament - e.g. do that opposite of what has happened.

Fair points. I think the 1990 to 2008 period was the killer. Govts tried to shrink into the background and let the free market drive us all into endless prosperity. But all we did was transfer billions of Govt debt to private debt. In NZ we went from about a Govt debt to GDP of 50% in 1990 to 0% in 2008, whilst private sector debt went from around 75% to 160% of GDP. Once we had household and business debt at this level, low interest rates became an absolute necessity. Look at us now that we have got rates at 5% - interest on business debts is running at $22bn per annum - that's more than corporate tax (about 1/6th of total wages paid). Don't get me started on mortgages.

Rockstar economy = debt bubble. Same in my view for Canada and Australia who also loaded up with private debt over this period and the insane house prices that have resulted relative to incomes/productivity.

In NZ we went from about a Govt debt to GDP of 50% in 1990 to 0% in 2008, whilst private sector debt went from around 75% to 160% of GDP.

And I suspect the composition of pvte debt is important. Early 90s are important for how banks changed debt allocation in terms of the ratio to mortgages / consumption to business.

Yes, business debt went from 45% of GDP in 1990 to 75% of GDP in 2008 but is now back at 45% again. Households are bouncing along at the 100% ceiling.

The biggest upwards pressure on wages now is interest rates. I still think we're totally screwed in 2024 and we have idiots in charge.

https://www.reuters.com/markets/mouse-that-roared-new-zealand-worlds-2-…

https://www.rba.gov.au/publications/confs/2018/mcdermott-williams.html

And a little background history

https://nzhistory.govt.nz/culture/the-1980s/overview

It would appear we've never had a clue as to the drivers of inflation. Maybe we've been entirely wrong to dismiss "money" creation/supply? Economists and politicians just don't have a wide enough knowledge base, unable to take into account tax and accounting laws, or understand how an underlying belief system influences everything? Too trapped in their own self interest to be able to serve the public interest?

I see a reference to asset prices in the conference paper, and one could suggest this is the biggest factor in financial stability, yet where did it ever feature in monetary policy?

Have we been blindly led down a path of no return? Or maybe we must walk the path of darkness and suffering in order to know the light?

Thank you Audaxes, Jfoe, IO, JC and KiwiKidsNZ.

Your comments are extremely helpful to me, as I try to make sense the (financial) world!

It's highly likely the financial world is one of those phenomenon that we'll never understand. One day we might look back and marvel, and most likely laugh hysterically at the follies of our ancestors.

As a man made construct it's devoid of any natural law, driven more by animal spirits and emotional fears than actual logic or intelligence. It's subject to too much influence by the big players and insiders, and most are just along for the ride. Unfortunately it's also a central focus point of our lives with maybe too much effect on everything.

I wonder how prevalent trading-bots are in the 'system', and whether they are a stabilising factor (taking some of the animal spirit out) or at risk of going septic if coded poorly.

(I'm a mechanical engineer, so apologies if that came across a bit 'tinfoil-hat' to you SW guys and gals!)

Great post Jfoe, thanks

Before we go out partying and celebrate the death of inflation:

- Q on Q is the highest since Sept quarter last year and significant higher than March and June

- If transport costs stay elevated during Q4 expect inflation to bump back above 6.0%

- Since May 2023, last raise of the OCR, the wholesale interest rates have been increasing between 0.7 and 1.25% depending at which term you look.

- Today's NZDM T bill auctions accepted yields between 5.60% (6 months) and 5.825 %. (12 months maturity)

So nothing to celebrate her.

Source: https://tradingeconomics.com/new-zealand/inflation-rate-mom

Yes a lot of the effects of higher fuel costs yet to flow through, and international money still rising.

Most (60%) of those higher fuel costs were the reintroduction of fuel excise duty. We also had public transport subsidies cut last quarter and local govt rates hit the CPI in Q3 every year. None of those things are going to happen next quarter.

The current price of petrol and diesel will flow through over the next quarter as businesses and agriculture are forced to pass it on.

Yes, agree with that for sure. Big risk is higher fuel prices sustaining over next year.

In case you missed it.

Junk-rated debt now exceeds top-rated AAA debt for the first time in history.

AAA had previously always been the largest category. AAA have fallen to 6% of total debt outstanding, down from +40%.

Everything is fine.

https://www.bloomberg.com/news/articles/2023-10-10/world-is-dominated-b…

OMG, I wasn't aware of this... the world is indeed... well how do we put this politely... in very bad shape. 2024 is looking menacing

Yesterday the Bitcoin market CAP went up by more than $50 billion in minutes on "fake news" surrounding the SEC's approval of Blackrock's ETF. Estimated money flowing into ratty was less than $500 million, so a ratio of 100:1.

A former Blackrock Director said that we can expect $150-200 billion flowing into Bitcoin in 3 years when the Bitcoin ETFs are approved.

Using the ratio above, a $200 billion inflow would mean a market cap of $21 trillion. That would put the BTC price at $1 million.

You're not in the market for a bridge perchance?

Cycle bridge?

Imagine if that $150-200 billion flowed into something that actually made a difference, something that served humanity.

A market cap of $21 trillion sounds pretty amazing for a meaningless number.

I wonder if the US govt could confiscate it and repay their national debt, sort of like they did with gold :)

It will serve humanity. Each of the 200 million bitcoin collectors stand to make a 200+ fold return on investment.

Sounds plausible, aye.

No, it won't.

Nothing productive was done, so it is a zero-sum game in real terms.

Sheeesh

I was being sarcarsick

We don't value things solely on their production value though. But obviously something that costs nothing to manifest will only hold any value as long as people want to believe in them.

I know it wasn't a great auction, but it seems there were TWO successful bidders?

Inflation fell or the rate of inflation decreased? Until I see a minus, inflation hasn't fallen anywhere.

Our words and how they're used are as much a psychological influence as the numbers, and it would appear most are caught under the spell.

Spot on. The news made it sound like a real positive. It’s still going up!

Inflation did fall. It is still positive, so prices are still going up. Prices and inflation are not the same thing, inflation is the rate of change in prices.

Think of pressing the brake on your car - the speed reduces (inflation) but you are still moving forward (prices). Negative inflation would be going into reverse.

Do the laws of physics ie the car analogy actually apply to the monetary inflation phenomena or are you comparing apples with elephants?

No, different laws, but a derivative is a derivative. Inflation is to prices as speed is to distance. In your original comment you compare 'inflation' to 'rate of inflation' - these are the same thing. Inflation is the rate of change in price.

Na I don’t think so. Inflation is to prices as acceleration is to speed.

The rate of acceleration (inflation) can fall but the speed (price) still increases.

If you like, sure. Acceleration is the derivative of speed so that works too.

Not sure it's quite so clean - with mine prices bring stationary is equivalent to the car being stationary. When the car (price) is moving, that means it is travelling at a certain speed (inflation). Acceleration would be the rate at which inflation is changing, but we don't normally dig that deep. We're basically taking pictures of the car every quarter and seeing how far it has moved since the last picture to determine its speed over that time.

So people think it means everything is becoming cheaper, when really it's just getting less more expensive ?

It means things are now getting expensive more slowly than they were. We target making things more expensive at a rate of 1-3% per year, but they are currently getting more expensive faster than that.

Things getting cheaper would require a negative inflation rate i.e. deflation.

Isn't that the premise of free market competition and economic theory, cheaper goods?

Good analogy. If inflation went negative we would have other problems, potentially much worse.

Would we though? What's worse than what we've currently got?

All we've been told is deflation bad but inflation also "evil".

All the infrastructure, the factories, the shops, the houses, the tangible resources, the people will still exist... Deflation gives purchasing power back to our tokens of exchange which must be a positive.

Therefore, the real problem lies somewhere else and either we're too dumb to figure it out or we're being prevented from a different way of doing things.

In a deflationary environment you will likely see a decline in production and investment. What's here already will remain, but the prospects of more tangible resources being produced and bought are reduced.

If the different way of doing things involves people being content with less, then no problem. I suspect however many will struggle with that concept.

From 2024 Japan will make investments in mutual funds and equities tax-free for citizens for an unlimited period. There will be an annual limit of up to JPY2.4 million and total investment limit of JPY18 million.

Inflation by quarter 1970s. There were also quarters in (1970) and (1972) when inflation looked like to be heading in the right direction - but that was not to be. House prices also dropped big time.

Q1 Q2 Q3 Q4 ANNUAL

1978 - 14.6%12.3%11.1%10.1%12.0%

1977 - 13.7%14.0%14.4%15.3%14.4%

1976 - 17.2%17.7%17.2%15.6%16.9%

1975 - 13.2%14.9%14.8%15.7%14.7%

1974 - 10.3%10.0%11.5%12.6%11.1%

1973 - 6.0%7.6%8.9%10.2%8.2%

1972 - 8.5%7.4%6.5%5.5%6.9%

1971 - 10.3%11.0%11.1%9.1%10.4%

1970 - 4.8%5.2%6.1%10.0%6.5%

Looking at your link it's quite clear it all started with decimalisation of the currency in 1967, as I've long suspected.

What's your point?

I also arrived in NZ in 1967, but I don't think decimalisation or my immigration were the cause of much inflation. Surely it was a small matter of the Middle East having a massive bing bong, the infamous oil shocks, and a big ramping up of govt entitlements over the 60s. I'm going to stop now in case you were being sarcastic and I already look like an idiot.

😉👍

No risk in the Middle East right now so we need not worry about that 🤪

Or the FED leaving the gold standard in 1971 to retain it's hegemony over world finances...

Almost 200,000 people arrived in New Zealand on work visas in the 12 months to September

WOW !!! That's hugely high. It will have to lead to higher unemployment. Together with the delayed effects of the higher interest rates... the recession will arrive. Granted, it's taken longer than most expected, me included, but the downturn is coming. Unfortunately I think 2024 won't be good for NZ.

It will stimulate the economy through demand, which will paper over the cracks of the fundamental flaws that stop NZ advancing

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.