Although there are some legitimate comparisons between the high inflation of the past couple of years and that of the 1970s, there's a key difference in that labour costs were a key inflation driver then whereas profits have been this time, a Bank for International Settlements (BIS) working paper argues.

"In both cases, the original commodity shock quickly transmitted to good and service prices, generating broad based inflationary pressures. In both cases also, fiscal policy stepped in, to cushion the impact of the shock, possibly worsening the inflation problem. Last but not least, the experience of the seventies has been flagged as a reminder of the cost of un-rooting inflation, short of early and decisive policy action," the paper says.

"We argue that this [1970s] comparison is ill-advised because the drivers of the recent inflation surge are fundamentally different from those in action back in the seventies. Back then, unit labour costs (ULC) were the main driver of GDP inflation. But more recently, unit profits (UP) have taken this role. The empirical evidence even points to UP having turned into a leading indicator of GDP inflation. We find evidence of this structural change for the United States, but the data also suggests a similar pattern in other countries like Canada or Germany. Moreover, this evidence is consistent with corporate profits (i) now accounting for a larger share of gross domestic income and (ii) having increased significantly post-Covid."

The paper, Monetary Policy with Profit-Driven Inflation, is authored by BIS senior economist Enisse Kharroubi, and Frank Smets who was the BIS Alexandre Lamfalussy Senior Research Fellow for 2023. Smets is former Director General of Economics at the European Central Bank and a professor of economics at the Department of Economics of Ghent University. The Basel, Switzerland based BIS is the central banks' bank.

Kharroubi and Smets say their paper investigates the issue of "profit-driven" inflation in the context of a New Keynesian model which they "enrich with reservation profits on the supply side."

"With this framework, we investigate the positive and normative implications of cost push shocks, taking the example of energy price shocks and focusing on monetary policy."

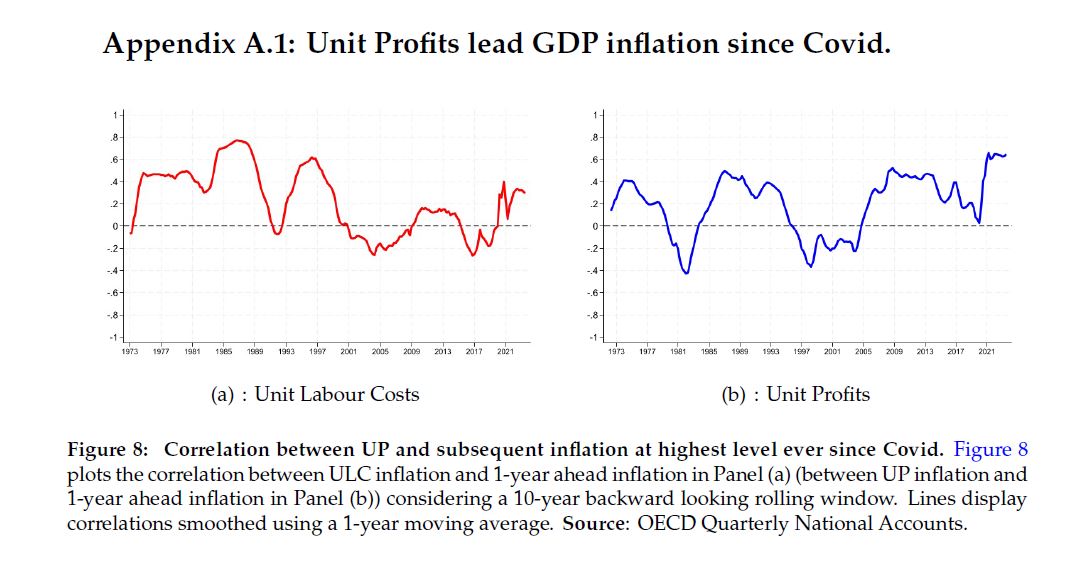

"Over the last decade, UP have essentially turned into a leading indicator of inflation, the correlation between current UP inflation and subsequent GDP inflation being positive and statistically significant up to six quarters ahead. Interestingly computing these lead/lad correlations over a shorter time window (in order to focus on the recent post-Covid inflation surge) provides similar if not stronger results, in terms of the leading properties of UP inflation relative to GDP inflation," say Kharroubi and Smets.

Figure eight, below, provides evidence of the correlation between current UP inflation and one-year ahead inflation rises, reaching the highest levels in the last 50 years of data, just after the outbreak of the Covid-19 pandemic, they say.

"Comparing the seventies to the recent period, the conclusion in a nutshell, is therefore that UP have replaced ULC as a leading indicator of inflation."

"We first show that energy price shocks lead to inefficiently large supply contractions and thereby inefficiently large (profit-driven) inflation, as firms which retrench do not internalise the social costs of doing so. Second, we show that optimal monetary policy follows a pecking order. It first aims at shielding the supply side from the fallout of the shock, thereby undoing the negative retrenchment externality. It then splits the burden of the shock between supply and demand, when insulating the supply side is too costly. Finally, when the energy price shock is very large, monetary policy looses traction. Budget-neutral fiscal interventions, e.g. redistribution from high-to-low-income households and/or from high to low-profit firms, can then restore monetary policy effectiveness," Kharroubi and Smets say.

Speaking in the Of Interest Podcast in December, Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr said profit-led inflation had been happening in New Zealand as it had overseas. (Also see: UBS chief economist Paul Donovan unwraps profit-led inflation in our Of Interest podcast).

BIS says its working papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of BIS.

The RBNZ holds shares in BIS. As of June 30 last year, the RBNZ owned 3,211 BIS shares representing 0.6% of BIS shares on issue. The holding was valued at $293 million in the RBNZ's annual report.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

26 Comments

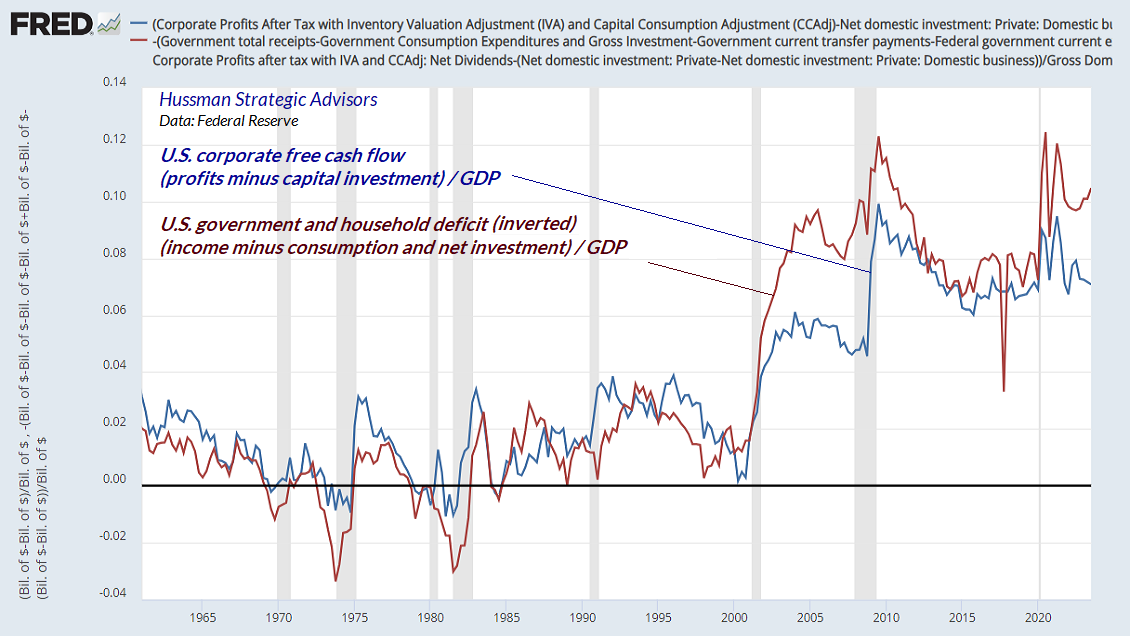

On the subject of corporate earnings, it’s worth repeating that the surplus of one sector of the economy (income in excess of consumption and net investment) is always the deficit of other sectors (government, households, and foreign trading partners). That’s not a theory, it’s just an accounting identity. Nothing – not monetary policy, not debt creation, not bank lending – nothing changes the arithmetic. It’s just math.

When investors look at current record profit margins and corporate free cash flow, they should recognize that this apparent prosperity is possible only because of massive deficits in the government sector, and depressed savings in the household sector in recent years. Sustaining one requires sustaining the other. Again, that’s not a theory, it’s just arithmetic.

The chart below is a slight rearrangement of our usual “sectoral deficits” chart. The blue line in the chart below shows U.S. corporate free cash flow (profits less investment). The red line is inverted, and shows the sum of U.S. government and household income in excess of consumption and net investment. There are a few addbacks and deductions to avoid double-counting and I’ve left out the foreign sector for simplicity.

The key point is simple: the “prosperity” of U.S. corporations here is the mirror image of massive government deficits and weak household savings.

While temporary pandemic subsidies drove a brief push to record profit margins in 2021, the larger structural difficulty for both government and households has been a progressive collapse in their income as a share of GDP, resulting from a combination of aggressive tax cuts and weak growth in wage and salary compensation. Corporations have been the primary beneficiaries of both. The problem for investors is that maintaining deficits of this size is likely to prove unsustainable without a debt crisis. Link Hussman

{kind=link}

Every person who does not understand the difference between correlation and causation ends up dead.

Even if you do understand the difference, you end up dead, Spike. That's the only certainty in life !

I think that may be the joke

Thanks Yvil for proving my point.

Once a corporate entity becomes Too-Big-To-Fail all risk is socialised. Literally cannot lose.

Sadly, it is not just individual corporate entities anymore - well-funded lobby groups are usually able to achieve desired outcome for the sectors they represent. Case in point: tourism, dairy, meat and, most of all, residential investor "associations" always have things their way in NZ.

Well, when the PM has a $20 million plus conflict of interest in property, and underling MPs have similar, that's certainly proving a problem.

The graphs are poor. Why isn't ULC and UP overlaid by the inflation measure, to assess the claimed correlation?

Great piece - thanks.

Profits, f course, are just numbers.

And they avoid debt-incurred anyway.

Meaning we have turned from meaningful (at least partially) to meaningless, in 50 years. Blindly; absolutely unaware of the Why?

Hi PDK, as a regular poster, I was wondering if you think that the staff at Interest deserve a little financial support from you ? How about it ?

Tell that to JimboJones Yvil!

I supply this site with many op/ed's.

I don't charge for the time I take to assemble, research and check them.

Or for the time I spend doing the research - that which Yvill avoids like the plague.

Interestingly, I'll guarantee all his 'income' is parasitic; that he does nothing physically productive. Which makes his comment all the more oxymoronic and asks an important question; where does the 'money' he 'pays', come from? Meaning, what backs it?

But he'll run a mile from that. discussion, I'm sure....

Stocks and flows folks.

Brand new beautiful NZ dollars flow into the economy from two sources: (a) Govt deficit spending (spending minus taxation) and (b) Net bank lending (new loans minus repayments).

Where do those shiny new dollars flow? In to household and business bank accounts and then into the economy where they exchange hands as people and businesses earn, buy, sell, transact with each other etc.

Some people have enough money to save some - so those lovely dollars get stuck in savings accounts and term deposits. Some businesses / fund managers have a LOT of spare cash they need to keep safe, so they swap some of their dollars for Govt bonds. Govt bonds are basically term deposits at the central bank that pay interest and can be traded.

There is currently roughly $670 billion of cash and Govt bonds circulating or saved in the economy ($80bn owned offshore). This is the result of banks having lent out $550bn net and Govt having spent about $120bn more than they have taxed. All the money in our bank accounts is someone else's debt. Money is debt.

What's that got do with profits? Profits are just a count of the dollars that have accumulated in the bank accounts of businesses over a given period of time. They don't stay there - they become income for share holders / business owners (or they get destroyed by taxation). Wages are the same - a count of the dollars that have been paid to workers, and then mostly spent back into the economy where they continue their happy journey making things happen.

When inflation picks up, it is typically because either (a) imported input costs go up, pushing businesses to increase prices to cover costs (hello diesel / fertiliser in 2021) and / or (b) the conditions are right for businesses to increase their margins, and therefore increase the flow of dollars into their profit bucket.

Increased profit margins are not necessarily a result of an overall increase of the flow of money into the economy; it could be because customers suddenly want a lot of some product and they don't want to spend their money on other stuff (e.g. goods vs services during COVID). Or it could be because people decide to spend the money they saved during a lockdown. It could also be because companies find a way of reducing their input / labour costs so that they can divert more money into profits without changing prices (import price drops in 2020).

Obviously, higher prices are contagious in an economy and we saw this in spades during 2021 and 2022 as the import / profit margin price shock spread through the economy. Note that wages have fallen in real terms since then and it is higher debt costs that have held prices up in NZ as import prices have fallen.

Side note: In the old days, Governments, under the influence of Keynes, concerned themselves with keeping dollars flowing around the economy and stopping them getting 'stuck' in the savings of rich folk. The faster flow and exchange of dollars (aka velocity of money) meant that the economy could function with lower levels of Govt and private debt because, simply put, not as many dollars were required to keep the economic engine running.

Jfoe, I love that you're able to explain complex economic situations in a plain and simple language. Kudos to you and please keep your posts coming.

Agreed, although he could take it back one more step. And in doing so, might find that his 'taxation' comment is wrong.

If you look at it in resource/energy terms, 'budgeting' is really; Allocating so much of so many resources, and so much energy, to a proposal. If supplies of those are not available, or are decreasingly so, inflation here we come (given a static or increasing collection of debt-tokens).

But governments can allocate resources and energy too. The proxy they mark it with, was privately or corporately 'owned' (does ponzi-conjured 'wealth' really exist?) then taxed (commandeered for the public good) and allocated. It isn't 'lost' at all - another way of saying Government is US, not a 'them' (a mistake now societally endemic thanks to propaganda-spawned blind faith in 'the market'; a religion by any other name.

I am with you on the real resources point - but energy, labour, materials need to be considered together. Govt spending and bank lending create calls on those resources... taxation and loan repayments delete those calls.

If you pay me to do your tax return and I pay you for energy efficiency advice, who loses?

How then does the 20billion in wage subsidies and just over 35billion LSAP all into it all?

Correct me if my train of thought is off here. More money to transact, supply side price increases and wage increases all driving the inflation. Large delay in increasing the OCR from record lows to counter said stimulus alongside large increase in debt creation from retail banks thanks to RBNZ removing LVRs and creating the FLP.

It is very clear that despite the supply side influences the RBNZs incompetence removes the need for any congratulations of things slowly coming back to normal.

The $20bn in wage subsidies was Govt deficit spending - it increased the wealth of the private sector and let to some increased spending. The LSAP is a non-event really - just led to fund managers buying financial assets to replace the Govt bonds they sold at a healthy profit. No drama.

The debt creation that RBNZ stimulated doubtlessly boosted the economy, with increasing spending, employment etc. But did it lead to higher prices becoming embedded in the economy? I am doubtful. We just imported more stuff.

re ... "But did it lead to higher prices becoming embedded in the economy? I am doubtful. "

Now that comes as a surprise. Are you referring only to the LSAP?

It's just fine to make low paid battlers unemployed all for the greater good. Ruin their lives to fight inflation.

But touch profits. Clearly immoral. Let's not speak of it.

The upward 'wealth-pump' has been in lock-step with diminishing REAL growth. It hid same for a while, the same way total GDP hid per-head GDP reduction.

Bu sooner or later, the bottom-end has nothing left, no matter how hard you squeeze the sponge. And they're being hit on multiple fronts now; landlords trying to stay afloat (and there will be a groundswell of those, for whom I have zero sympathy; they were merely parasitic); local governments, government, all are feeling the effects of entropy (and none are correctly identifying the problem; 3 Waters was always unsolvable a the desired level of service, as is current infrastructure collectively).

Gonna be an interesting few years.

for whom I have zero sympathy; they were merely parasitic

With comments like this, it's no wonder you're being asked to stump up while others are greeted with encouragement!

He's not asking me to stump up - he is a spinner and wants my narrative gone. 'Tís inconvenient.

But the question as to what it actually is that he is 'contributing', is an essential one

:)

It's a simple issue. A rational tax structure matched with someone with the guts to implement it.

Nice to have experts back up what I've been saying.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.