Perhaps no other downturn in the housing market has been as widely anticipated as the one which is supposed to occur this year.

Economists and commentators from almost every corner of the market have been telling us for some time that current house prices are unsustainably high and that rising interest rates, more restrictive mortgage lending rules, changes to the way residential investment property is taxed and the lack of inward migration coupled with a steady increase in the supply of new homes, will combine to cool the market and push prices down from their recent highs.

So when the Real Estate Institute of New Zealand's House Price Index (HPI) declined by 1% in December after a scorching run of monthly increases, did it mark the turning point of the market?

Certainly the decline was significant.

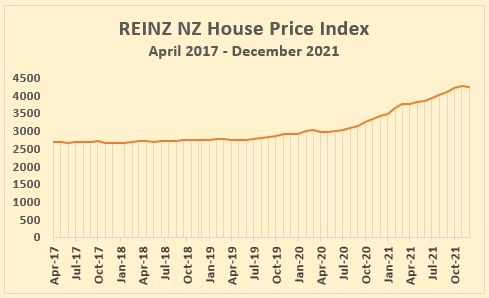

The graph below tracks the monthly changes in the HPI from April 2017 to December 2021.

It shows that from April 2017 to July 2020 the HPI posted relatively modest but steady growth, increasing by 12.3% over that 40 month period.

Then from August 2020, as the Reserve Bank started pushing mortgage interest rates down to extraordinarily low levels, house prices started rocketing up.

That saw the HPI increase by a staggering 51.4% over the 17 months from August 2020 to November 2021.

Considering that the HPI increased by 3.3% in October and 1.9% in November, the -1.0% decline in December could well have marked a significant turning point in the market.

The trouble is, one month's figures do not make a trend and December is not a very reliable month for picking changes in the market, because like January, it is affected by the Christmas/New Year break, when the market all but closes down for 3-4 weeks.

However there are three things that suggest that December's drop in prices was more than just a blip in the market.

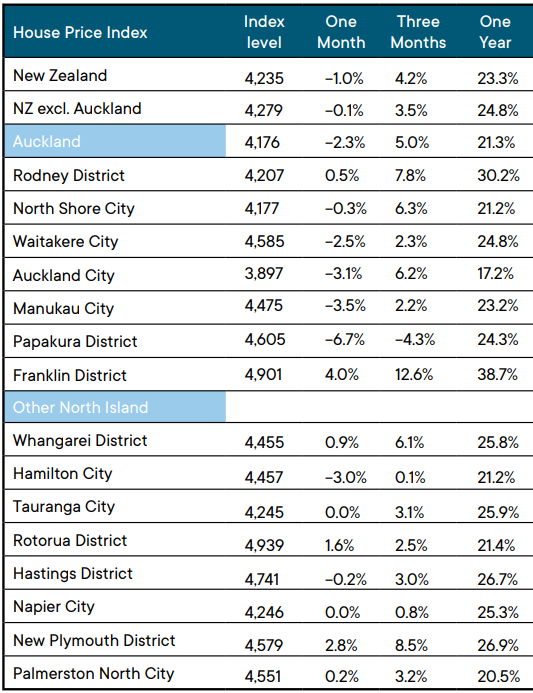

Firstly, prices were particularly weak in the country's biggest market, Auckland, where they were down 2.3% for the month, compared to an increase of 3.1% in November.

As the tables below show, prices were weaker in all of Auckland's major urban districts except for Rodney and Franklin, which bookend the region at its Northern and southern boundaries.

The monthly decline in Papakura was a whopping 6.7%.

Additionally the number of districts showing a decline in the HPI is increasing.

In November, just seven of the 26 major urban districts in the REINZ's HPI summary showed a decline.

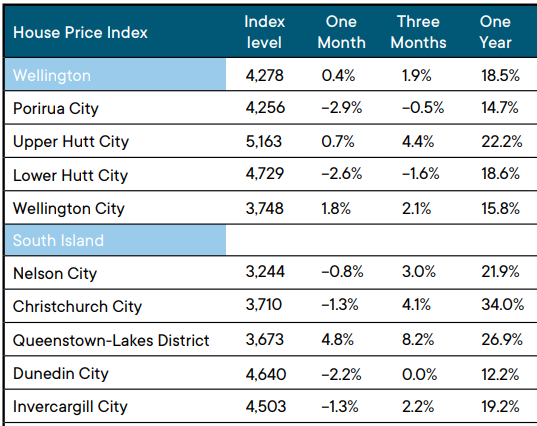

In December that number doubled to 14 and included the major centres of Auckland, Hamilton, Christchurch and Dunedin.

And finally, if a price correction was in the offing, you would expect it to be preceded by a significant downturn in sales numbers, and the number of residential properties sold in December 2021 was down by 29% compared to December 2020.

All of that suggests that December's HPI figures were more than just an aberration.

Although sales in January can be patchy, February/March is usually the busiest time of year for the real estate industry, so we shouldn't have to wait long to find out which way the market is headed.

Another month or two should do it.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

REINZ House Price Index - December 2021

181 Comments

Reality is lots of headwinds slowly building for a while and have been masked by printing and debasement of currency. Investors with lots of equity will yawn and not blink. Specuators with the famy home leveraged to the hilt to provide the only equity for the debt have a very different challange.

Monetary debasement would benefit those with debt more than it does those with equity, but unfortunately for mortgage holders, that's not what's been happening. We haven't been "printing money" a la Zimbabwe or Weimar Germany. We've been monetising debt, which is a different beast altogether.

I really like this comment regarding monetising debt. For the last 12 years kiwis have made purchases, borrowed against paper gains and sat back on mountains of liabilities cloaked in leaky wooden homes. I have no issue with smart leverage, but seeing homelessness and poverty on an insane scale whilst people call themselves service providers for being landlords makes me vomit in my mouth.

Property is cyclical and you cannot game the cycle without causing a crash. We pumped a bubble and now it has popped.

The housing market may well take a breather - after a lengthy buoyant period.

But don't expect a crash......

There remain plenty of people (in NZ and abroad) keen to purchase NZ real estate. And economic fundamentals remain solid.

TTP

PS My major focus this year will be on encouraging landlords to get their rental properties up to a reasonable standard. Far too many flats/houses are shockers.

economic fundamentals remain solid

I have no words.

Maybe he means support from investor politicians and central bankers? Economic fundamentals haven't been great without such central welfare and other support for a while now.

Low unemployment.

😂. Ostrich + Sand comes to mind.

Fundamental = RBNZ + Government = $$$$$$$$$$

Well he is not wrong: high economic activity, high household savings and low unemployment means the economic fundamentals are very solid - that should be rather obvious.

However housing is a completely separate story, with prices far detached from any sort of logical reality. They make zero sense to buy as investments from a cashflow perspective (and will be even less attractive if capital gain growth stop), and for first home buyers the debt to income ratio is way beyond any sense unless buying a small apartment.

IMO a crash is HIGHLY LIKELY THIS YEAR - in fact I think it has already started,

Usually what people say before Orr turns on the money printer and pipes it directly to the Retail Banks for mortgage lending.

So a 10% increase by the end of March?

Property, New Zealand's biggest welfare scheme. For the wealthy.

Almost all growth stocks are down 40% to 80% plus and bluechips 15% to 30% plus from ATH.

"IMO a crash is HIGHLY LIKELY THIS YEAR"

Famous last words.....

TTP

Wow...we agree.IMO its been overdue for some time and only delayed by extreme action from RBNZ and FED.

There's a lot of talk like this- house prices don't relate to fundamentals- but really is it that far out? If it was then section plus new build would be a lot cheaper than buying an existing house....

Depends on location and quality of house. 2500 bucks a square gets you a new house that meets code, but if you wanted to build a timber villa with a high stud you'd have to spend double or triple.

So true, we had plans to build a replica villa on our section in Lincoln, Christchurch. It had a hefty price tag, we have since decided to sell the section ( under offer) as it seems cheaper to buy a new house or one a few years old.

more deadlines and prices lately so we are happy to get out and hopefully buy with cash

I don't think this is how it works. As house prices increase, section prices will increase. With your logic, house prices always relate to the 'fundamentals' of section prices + building a house.

If house prices fall, section prices will fall in unison.

Chebbo: "I have no words"

Looks like you have at least 4

My major focus this year will be on encouraging landlords to get their rental properties up to a reasonable standard. Far too many flats/houses are shockers

Gummint already been doing that and failing by setting stupid standards where rules contradict. Resulting in houses staying empty and a loud outcry about ghost houses

TTP,

"PS My major focus this year will be on encouraging landlords to get their rental properties up to a reasonable standard".

What an influential chap you must be. Speaking as a landlord, there is no excuse for landlords who have chosen to provide substandard housing and they should be hit hard where it hurts-in the pocket. Those who continue to drag their heels should face compulsory purchase orders with the price suitably discounted to reflect the work needing done to bring the property up to a reasonable standard.

Economic fundamentals might be solid (and this could well be questioned - especially with regards to indicators such as inflation rate, private household debt levels and concentration on housing etc.), but the problem is that the current NZ housing bubble has reached levels that have gone well beyond any sensical relationship to such economic fundamentals.

If you wanted the housing in NZ to accurately reflect economic fundamentals such as income levels, then current house prices in NZ would have to be dramatically less of what they currently are, and no real estate agent speak can hide this very simple fact.

Multiple generations worth of wealth, productivity and plunder are tied up in property, not just 1, 2 or 3 people's current income.

If that we’re true, we’d see mostly linear growth in property prices. It seems doubtful that homeowners have become dramatically more productive over the past two years. This argument also ignores capital replacement costs. Until we see multi-generational mortgages (which looks increasingly likely), your argument is very wrong. Prices do eventually track incomes.

Multigenerational mortgages seem a symptom of government abandoning its people and governing instead on behalf of banks. The opposite of the post-war governments who built to make housing affordable for average Kiwis. Enabling this to happen would be morally reprehensible.

Unemployment at record lows, GDP per capita rising fastest than it has for a long time, and that's despite what we thought was our big money earner (tourism) being shut off for 2 years, now in it's 3rd. Our debt to GDP ratio is one of the lowest in the OECD. You're right, our economic fundamentals is solid and New Zealand is a desirable place to live.

Government needs to go down hard on scum landlords. Everyone deserves a warm, dry home to live in, and landlords who think they are doing people a favour by offering, damp, cold and mouldy homes for sky-high rents and not spending any money on the property need to be forced out of the market.

Looking forward to the banks coming after the highly leveraged landlords as interest rates rise.

Do you think $15billion dollars of wage subsidies over the last 2 years has anything to do with it, what's it going to look like now the payments have stopped and inflations here?

If this type ofnews continues for next quarter than can confirm the fall - though all indicators are pointing towards downside but still as this time if and when it falls will burn many,specially those who entered recently under FOMO by overstreching. It has already started in stock market and is happening ( Many retailers who entered last year and saw windfall gain are in for surprise) :

https://thekaka.substack.com/p/dawn-chorus-house-prices-fall?token=eyJ1…

....and all of those people that thought that because their house was worth x more dollars and interest rates were low, then surely they could afford a new boat and a new car....now they will have already lost money on the boat, and the car, and will be paying more interest and have shrinking equity and a whole lot more debt. Plenty of people are going to be in this position.

Yeah I'd never be comfortable with that approach myself, but many people have been doing it that's for sure, and from what I can tell banks have been quite encouraging of it.

I guess as long as property prices were going up - and almost no one believes they can go down meaningfully in NZ - then it was seen as a safe strategy.

Although to be fair most people doing it wouldn't have even thought about strategy - it was just a 'no brainer' and 'everyone does it' (Keeping up with the Jones')

House prices increase Steep. MSM spin goes on overdrive, forecasting even more spectacular rises. When market falters wither MSM predictions of house price decline? With muted breadth, play around with words, a negligible per cent. As if its taboo to even mention house price falls. If the staircase going Up is steep, is it not the same staircase one uses coming Down????

Feels more like an escalator than a staircase.

If would-be house buyers can’t borrow the money then how can sales actually happen?

Even 4th time house buyers with 70% equity and good incomes cant qualify for loans. So vendors can’t sell under that scenario as they can’t rebuy.

Do you mean 30% equity? I'd be surprised if house buyers on good incomes with a 70% deposit wouldn't be able to buy unless they have existing expenses and commitments out of this world... the CCCFA simply requires lenders to see all expenses etc.

It's certainly a stink piece of legislation that seems to be having unintended consequences, but it seems that much of the complaining about it is often from those vested interest, like REA and especially brokers, who would see less commission from smaller loans. Smaller loans is a good thing. People should not be borrowing >6 times their income. The accepted benchmark is 4x.

Well this is the growing issue. Honestly first home buyers couldn't afford to buy for years now Without stretching themselves financially. The solution has just been, well do it or you'll miss out.

Banks suddenly decide enough is enough.

This is why its important to recognize unsustainable price growth and nip it in the bud early on. Or you'll suddenly find yourself with a shock downturn that catches everyone by surprise.

It will always be a shock rather than a slowdown, because banks will determine their losses due to a slowdown and be much more reluctant to lend, exacerbating the slowdown.

If you ask me, NZ banks are due some kind of reform to stop them preying on money. Seems a conflict of interest.

How many more articles will it take before you realise its CCCFA legislation and not bank process/policy. Banks hate it, cost 10s of millions to implement new systems, more staff needed for longer processing times, less lending etc

It's certainly interesting that when "personal responsibility" (something folk usually purport to believe in) becomes part of the picture banks are more careful about what constitutes responsible lending based on income and expenses. Makes you wonder what they were doing before when any negative consequences could be left for others to bear.

Prices are too high because of monetary and other policy support for keeping prices high. It's not a bad thing if they come down .

Sellers can always sell their houses, they just have to ask more reasonable prices based on what banks determine from income and expenses looks like sensible lending.

Some sellers can’t sell now - as the bank won’t approve their existing sized or similar mortgage on a new security ( Eg potential new home).

So more and more vendors will sit tight for 6 months until they are confident enough to move.

Sounds like the bank thinking that if personal responsibility is required some of their previous lending might not have been completely prudent, income and expenses considered. Maybe they were factoring in taxpayer and reserve bank as the backstop, rather than bank/personal responsibility.

That is a ridiculous comment especially in cases where,say, a couple in their 40s has been comfortably paying a modest mortgage for 10 years, then once they sell to move for various reasons they cannot maintain or secure new/revised similar borrowing precisely because of the banks implementation of the new CCCFA.

There are many examples of this occurring. It is not a pullback of risky or over-borrowing.

All we have to go on is the banks own behaviour when charged with taking some personal responsibility, and anecdotes from parties in whose interest it is to have more loosely flowing credit and ever higher prices.

An expectation of a modest mortgage for a good/secure income household is not an expectation of ‘loose lending’.

That's correct. Hard to imagine those have gotten the bank directors nervous about personal responsibility.

Maybe lower house prices are needed so NZers can have a modest mortgage for good/secure income households without requiring loose lending.

Let’s see what happens.

I lean toward expecting the politicians to do the banks' bidding. At the end of the day property has become a welfare scheme for the wealthy not a market with risk and price discovery.

Nats sure. If Lab protects the banks first against the interest of mid to low income NZ, it will be the biggest ideological sell out in NZ political history.

Watch this space....

Labour's already done this...?

Have you been watching for the last few years?

Yeah I've seen house prices go to the moon locking out low to middle income earners... Why? Labour did nothing & RBNZ pumped the market full of cash benefiting asset owners...

Am I missing something?

A fair few Labour MPs have property portfolios too, not just National. And the parties are now so close to each other as to in many ways be Natbour. (Also see Phil Goff turning into a NIMBY conservative mayor.)

They can just rent instead. Nothing wrong with it apparently.

It's no coincidence talk back radio is being flooded by stuff on the CCCFA. Banks have the vested interest and doing everything they can to embarrass the Government and force them to back down. The lady who spent "too much" at Kmart is just a pawn in the game.

Yes we are overdue a correction, but I'm not sure it will eventuate. I am looking and there really isn't much around at all in the area/property type I am looking at. Also lisitngs in the Auckland lifestyle hot spots (Coro and North East) are well below long term average. There are a lot of new build apartments/town houses listed however.

If you want to emigrate the border is open for business but there are thousands of Kiwi's trying to get back. Which means more pressure on housing whenever the border normalises.

If you want to emigrate the border is open for business but there are thousands of Kiwi's trying to get back. Which means more pressure on housing whenever the border normalises.

This scenario may have a chance of eventuating if the # of Kiwi's trying to get back > # of Kiwi's trying to get out. I'm not sure this is likely. There's better wages, schooling, weather, social care and health care only a short 2.5 hour flight to the west.

You can fly out tomorrow. As far as the bulk of Australia goes, I would argue that schooling isn't better and neither is the weather. Social care as a Kiwi in Australia, good luck. If you want to go, go. Stop b1tching and moaning about it and go.

People having attitudes like this is the reason why we got so many issues. When other people brought up issues, instead of listening to people, asking them to accept the current state or leave and not wanting any changes wont get us anywhere. It's just arrogance.

There's a certain cost that comes with living in NZ. It's a small population stuck down the bottom of the earth. We're trying to have high end first world living conditions but lack economies of scale and higher taxation to provide it.

The whole thing is a compromise, so if your priorities are having much cheaper costs of living, or higher incomes, NZ is never going to compete with many other places. Hanging around and bemoaning the place won't get you anywhere, try it out somewhere else, it'll either float your boat, or it won't. Or work towards increasing your income and lowering your expenses.

It's not bemoaning the distance or the ability to do productive work and sell to the world. We know NZ can do that.

People are bemoaning the centrally driven wealth transfers from wages savings to those with assets. Wealth transfers to the wealthy have been making NZ a worse place for young Kiwis. It's stupid policy we've run over the last couple of decades.

Much of the trouble young Kiwis are facing is because the older generations rely on saddling them with massive debt (so they can spend that wealth) only to then also garnish their wages for their universal benefit.

FFS, get your head out of your a55 and actually take a look at the cost of living in Melbourne or Sydney, or even Brisbane and Perth. The exact same wealth transfer has happened there, in fact Australian interest rates are lower than NZ's. You want to live in a house in the Eastern Suburbs of Sydney - they start at $8m, apartments start at $3m (3br). Add another 7% stamp duty to that. You will spend $2m on a house 30km plus from the CBD with weather extremes and monster commute times. The wage gap just isn't as big as it's made out to be either.

Thank you for some facts. While there are definitely some better opportunities in Australia for some people and many people will move to be better off in Australia in the coming months, it's not always as simple as Australia > New Zealand and New Zealand is a terrible place to live. Life in Melbourne and Sydney can be tough. Until recently, Brisbane was good value but things have rocketed there too (wife is UQ alum and worked there before making a poor decision to marry me and return to NZ).

There are many good reasons to travel & work abroad and for some there wll be career and earning advantages. I know many people who have done it and done well and the vast majority returned to NZ and have not regretted it.

Well aware Aussie's pollies and their voters have been transferring wealth to themselves too. However, it's surprising you'd argue that the equation is as bad for Kiwis as here. I have multiple friends who live and work there, both renting and owning, and enjoying a better overall balance of wages vs. living and housing costs. And the rental equation is a key one at the younger ages, as lower rent and living costs are enabling them to build wealth more quickly than in Auckland or Wellington.

You may also need to withdraw your head from your posterior if you're unaware that this is a reality for many younger Kiwis.

As has been said, there's nothing overly unique to NZ in this regard. It's just that overseas, you have more options of cheaper places to live. We have them in NZ, just most people don't want to move there.

The options are not like-for-like though. Say for example you want to live in a city of around 100k people, with a University and a hospital nearby. There are no options in NZ where you can realistically get a house for less than 500k. Even in other places overseas where housing prices have also gone through the roof there are plenty of small cities with those kind of amenities which are way more affordable.

Oh yes the saving Nirvana that is Australia for all the people that have never lived and worked there.

One thing is certain about Australia I believe: If you are in your 20s or early 30s, go and save up at two or three times the speed you will here in the same job which is easily done even in Sydney. Over 5 or 10 years it makes a huge difference. Then come back if you want. It's what I did.

be a man not a kayway have a pess not a wayway

The current cost of building will keep existing houses elevated. Add in a little inflation and forever low interest rates, the desire of fhb will not wane but demand could soften as they might struggle to get the funds together.

I really do not buy that line. I trained as a QS in the early 90's, new homes were always more expensive than old dungers. The belief that an increase of 50c a metre for 4 x 2 will somehow increase the value of an existing house is absolute bollocks in my opinion.

Happy to have my mind changed with any actual evidence that proves otherwise.

Tell me this.... if the price of large size blinkers increases by 50 cents, then are your extra large ones likely to increase as well.

It's all about replacement costs and a house is a house is a house. Sure new ones might have AC, double glazing, what have you but those are just frills to something that has the basic function of housing someone from the elements.

Some people value new for newness sake though, for sure.

Well, I agree with you even if the general reception has been frosty. The evidence is pretty clear - there have been plenty of times and places where houses have sold for below replacement price, including in NZ (maybe not after the recent price explosion, but certainly a few years ago).

Even more than that - the majority of a 'used' house price these days consists of land value. Building costs haven't gone up by as much as house prices have - the balance is land price rises. This can obviously be reversed regardless of how much it costs to physically build a house.

The land price component is extremely obvious when you realise that it doesn't cost much more to build a house in Auckland than it does in Christchurch, and yet similar houses sell for twice as much. The difference is land cost, and this is not coupled to the rising building cost.

Thousands of kiwis trying to get back to visit family mostly. Not many are that keen to actually live here unless circumstances force it.

There are thousands of kiwis trying to get back to visit family etc., not necessarily to live. It seems unlikely that someone who hasn’t been locked in the hermit kingdom and steeped in its property mania for the past two years would want to buy a here IMHO.

What’s more likely, is an exodus of the entry-level FHB demographic. The bottom of the market is going to fall out, and take the whole economy with it.

NZ is a low productivity country, with no major competitive industry, far from any major trade route. Our wages are low, and property prices will follow.

"The year ended October 2021 (compared with the year ended October 2020) provisional estimates were:

- migrant arrivals: 46,300 (± 500), down 61 percent

- migrant departures: 48,000 (± 500), down 24 percent

- annual net migration loss: 1,700 (± 700), down from a net gain of 55,800 (± 30)."

https://www.stats.govt.nz/information-releases/international-migration-…

Looking at the daily customs data there have been over 5,000 more people leave than arrive this month and that's after a slow start. My prediction is that in a few months time stats NZ is going to report that we will have a net loss of over 10,000 migrants in the month of February. There will surely be a jump in visitors and migrants when MIQ is removed, but I think the migrant part is going to lower than people are expecting and the final net migration loss for the year will be quite substantial when that finally get reported early next year.

A brief tale from overseas with some interesting comparisons. I'm selling a house in the UK, in a city roughly the size of Wellington. It's a 2 bed semi-detached solid brick house, reasonably well located, 300 square meter plot. Great for a FHB or young family.

First interesting comparison - the house will be marketed at the equivalent of $360k.

Second interesting comparison - I've had a few quotes from estate agents to sell the property, ranging from $2k to $3k equivalent all inclusive, fixed fee, no sale no fee.

Just a little taster of how a slightly more sane housing market is working at the moment.

Interesting - compared to 25k to 35k to sell an average NZ house.

What is the rate of capital gains tax you will be charged

Not much payable, perhaps a couple of k. Price is up from about $250k equivalent ten years ago, and the house was our primary residence for some of this - the gains are discounted based on how long we lived in it. Add in a couple of tax free allowances and the remainder is minimal.

Based on a 100k capital gain 2k is obviously only 2 percent and sweet FA. Kiwis did not want a bar of the late sir michael cullen capital gains tax because he was proposing a 33 percent tax rate. That was never going to get buy in

Seems reasonable to just apply the same tax rates to all income whether earned (productive work) or unearned (windfall). Graduated tax bands.

In this case, the majority of the 'windfall' comes from inflation. Some accounting for that would be reasonable (and pretty easy to calculate and subtract from the gain).

RS That is the attitude that sunk CGT... you got what was deserved.

I merely pointed out - as John Key did - that income from one source is the same as income from another.

All you're demonstrating is your own freeloading entitlement mentality. The bludger mentality that actually sunk CGT.

Based on a 100k capital gain 2k is obviously only 2 percent and sweet FA. Kiwis did not want a bar of the late sir michael cullen capital gains tax because he was proposing a 33 percent tax rate. That was never going to get buy in

mfd,

When I sold our home in Glasgow in 2003, the agent's fee was 1% and you are paying less than that. It's been the most puzzling feature of life here that so many Kiwis are quite willing to pay the exorbitant fees charged by agents.

There are lots of agents, so competition should have driven these down, but to my knowledge, all the main players have very similar fee structures. An informal cartel perhaps?

It's a mystery that people continue to pay so much. Here in Christchurch I have put an offer on a house sold by total realty who offer 1.25% commission, probably plus GST and maybe other fees. Still expensive in a UK context but significantly better than most. They were perfectly fine to deal with, very efficient and quick at selling, and we didn't get it despite our sealed bid being over asking price so they got some good offers together.

Not sure why people don't vote with their feet - perhaps they like funding real estate agents lifestyles?

I get the impression that the charge is so high because they achieve so few sales per agent, and spend half their time drumming up business. How do we get to a world where there are half as many agents selling twice as many properties each and charging half as much?

In the UK agents are employed with a base salary + commission. The agency advertises not the individual agent. My brother in law got his real estate licence in Auckland. Commission only and had to pay his own advertising. Not even minimum wage is paid. If NZ agents don’t sell they don’t eat. No wonder there is some sharp practice and high fees.

Yes, I find their fees absolutely staggering.

There was more justification when it meant coordinating newsprint advertising week by week and there were newpapers, printers and distributors clipping the ticket, but now with online advertising doing a far better presentation for a tiny fraction of the cost, then prices to the agents must eventually start to move downwards.

I can't fathom the folk who migrate from one home to another each decade. They might fool themselves that they're upgrading or riding a wave of rising prices, but in reality they are throwing a handsome proportion of any price gains into the arms of the real estate folk, and it's total madness.

A softer landing will be engineered through via repeal of overbearing CCCFA regulation and reopening borders. Also RBNZ could skip a rate hike by directing attention away from rampant inflation and towards Omicron.

The music can't be allowed to stop given property is New Zealands economy.

Don't know about repeal, that would be very embarrassing for the govt.

Soft landing will be engineered by inflation. House prices stay the same, but the real value of the money being paid will be slowly less and less.

After a massive rally....some places are up by as much as 100% since the start of pandemic, so a fall of of 5% to 10% will be symbolic and may only help in cooling FOMO. In NZ Housing market will not crash (Even in 2008 had fallen by 10% to 15%) but may not rise again for next few years.

Only this time as the market was funded by cheap and easy money ( not to forget government generosity to even thos not effected by pandemic) as never seen before, may be this fall could be different than witnessed before in NZ.

Have noticed many of those old houses on 600 / 800 sqmt sections are not going as now mum n dad builders or new builders have become extinct, hard to find so not getting the price that vendors are expecting. This scenario is not only because of higher interest rate or getting hard to get finance but more because, now maths does not work with the asking price / risk to reward is not favourable and many matchboxes houses that have mushroomed all over are not to able find buyers easily not even at discounted prices.

So many who had overstreched and were in it for short term ( unable to sustain / hold for long) will break and may have domino effect but that will be a while, if it has to happen. Those will deep pockets are in rent to mortage situation may hold for long till the market turns again.

Risk to Reward in a ponzi like situation justify paying any amount of premium on top of premium - do not mind paying 1.2 million for a million dollar house as know that will soon sale for 1.4 million and the person buying for 1.4million is buying to resell for 1.6million and so on....As long as the chain is in motion, it keeps moving higher and higher and the moment this stop like any PYRAMID SCHEME...it ......

Think, it is for this reason those old house with 600sqmt sections are not selling and also news or rumors now in market is that houses being built on this section are also not attracting much buyer and if those houses start selling at discount as possible as situation may arise where mum and dad builders are happy to sacrifice profit to avoid lose. It may set a chain reaction in motion.

Traditionally you can counter this argument by pointing out that we have an increasing population so the location of a house generally becomes more sort after over time as a city expands.

Also for the last 30 years we have lived through a period called the great moderation where interest rates have steadily fallen supporting rising prices.

both these points are not currently in play.

Auckland is going to see a ton of unaffordable ‘affordable’ townhouses on the market over the coming year. Developers will be crying into their beer because FHBs can’t borrow 950k for a two-story townhouse in Flat Bush anymore. Yet there’s now so much equity available to long-time property owners that prices for genuinely desirable stuff will probably remain high. It’ll play havoc with the indices. I think we’ll see more of a two-speed market, with more divergence between what actual FHBs can afford and the high-end.

Next to watchout when many of this developers start to give out house with whiteware / furniture.

Those will deep pockets may still survive but many who had diverted everything and are over leveraged should worry as for may those townhouse will be ready in next few months or years and if downturn gathers momentum will be finished unless they get out on time.

I predict a very significant increase in the housing stock for sale coming February and March

That's a no brainer.

OK, go ahead and make another prediction and see how it pans out (put a date on when your predicuion will happen).

I predict in the middle of winter, the number of housing going on the market will decrease.

There, we've both just "predicted" annualised trends in real estate marketing.

I assume Yvil means more than the usual seasonal lifts in February / March.

Pa1nter, I was talking about the "stock for sale" you reply by talking about housing going on the market = listings, you might think it's the same metric, it isn't. Housing stock is determined by both, the number of listings and the number of sales. The reason why I predicted a significant lift in the housing stock for sale is that I see more houses coming onto the market AND fewer houses selling = more stock for sale.

Another prediction? I just said it’s a no brainer. it’s down hill from here...

So nothing of substance, just a vague opinion without any specifics or timeframe… weak

rastus

re: "That's a no brainer."

Nothing is certain: Just from my library of how wrong one can be:

"by rastus | 21st Mar 20, 6:00pm

Shares just correct instantly, housing will follow like night follows day."

Have a great day. :)

In a free market it would have occurred. QE and a crooked bunch of bankers has bought some time....but so what. It’s happening now. I’m ready, are you?

The Fed will force Orr's hand and interest rate hikes will need to occur to prevent inflation on imported goods adding to the domestic inflationary pressures we already have. The size of the rises will be less significant than the fact the the RBNZ is putting inflation and currency in front of housing, at least for now. That will dry up what optimism remains that property is still a blue chip asset and we will see a correction as investors pivot in greater numbers to other asset classes. The next questions are how much, and how fast is this correction going to be allowed to happen before we see "stability" threatened and counter measures deployed?

A good article although:

Perhaps no other downturn in the housing market has been as widely anticipated as the one which is supposed to occur this year.

Could have been written at the beginning of 2019 when Covid arrived

True - it is the much heralded events that never actually seem to eventuate, a la Evergrande. The true clusters happen before anyone has realised like the GFC.

Massive welfare wealth transfers from govt and reserve bank to the rescue again to keep prices up, you think?

I think things are going to deteriorate by winter 2022, not just housing other economic data as well. When that happens, yes I expect the same RB and Government response as previously

Which is a big part of the problem, really. The government and Reserve Bank turning housing into a welfare scheme for the haves helps drive FOMO, as young people recognise they're on the wrong side of farcical, morally decrepit wealth transfers.

Terrible governance in NZ over the last couple of decades.

So much business is propped up by the housing market, it is inevitable that when house prices begin to normalise the pain will hit the whole economy. Standard eggs in one basket outcome.

Good point.

"""Dark clouds gathering" more like an off white fluffy cloud just popping in to say hello.

Imagine being a FHB in Papakura. You bought your first home in November. You somehow managed to scrape together a 20% deposit. Phew. You're on the ladder.

Your equity is now 13.3%.

Play stupid games, win stupid prizes.

Is wanting a home for your family a stupid game? Some would argue not. If you buy and intend to live there for 20 years and can afford it, then best not to worry about prices and enjoy your family. Worrying about prices will do nothing but bring you stress and resentment. If it was a rental or to flip... well that is another story!

Wanting a home for your family is not a stupid game at all.

Intending to live in Papakura for 20 years on the other hand...

Touche Brock! lol..

Seems pretty pathetic to have a go at people just wanting to buy their first home.

These people are grown adults.

They should have well developed abilities to control their impulses and to assess risks.

The Auckland housing market is obviously a very stupid game right now.

Brock you could have said that about the past decade

No time in the past decade has even been close to the current level of stupidity.

I would argue when COVID arrived on these shores there was far more pessimism regarding the housing market

That's sentiment.

The numbers stacked up far better than they do now, however.

Sure, but you'd have to excuse younger Kiwis for seeing that the government and Reserve Bank step in to prop up house prices at the drop of a hat and being on the wrong side of this causes a massive loss of wealth to them. That drives the FOMO, seeing their wages and savings become meaningless. They're stuck between a rock and a hard place, and they don't know how much more the government and Reserve Bank might pour into housing prices to keep them going up.

Exactly. Labour, National and the RBNZ have shown they are willing to ignore the fact that the vast majority of people think prices are already too high, and may well be willing to continue to ignore inflation, increased financial risk and just keep propping up the bubble.

Brock, your lack of empathy for people in this situation makes me think you would have made a good landlord if you were born 20 years early.

Nah mate. I empathise. I've been faced with the same dilemma.

I'm just voting with my feet instead of sticking around Jonestown to drink the Kool-Aid with the cult.

Buying a lousy townhouse in Auckland right now is a very risky thing to do.

I can't believe we're discussing the idea of "feeling sorry for homeowners" right now.

The Aussie market will likely shit the bed at around the same time as the NZ one.

Your new place might be worth less than what you paid before it's even finished.

Hi s1mple.

Who knows. It's unlikely the way that it's going in that region at the moment.

Doesn't really matter either way. It's a home to live in. Great climate, nice house, no debt. Freedom.

Maybe you can come do the painting for me.

And with a median house price of $1m in Papakura, that makes putting it into dollar terms easy.

Our hypothetical FHB just lost $67,000 in a month, or 1/3 of their deposit.

Yes, shame on those FHBs that chose to purchase a house that they could afford to provide stability for their family....they should have just kept their house buying plans on hold for the crash that has been predicted every year for the past 5 years.. sarc

Having a bit of a chuckle looking at the housing market in the Hutt Valley. Currently 410 houses on the market - which at 40 houses sold a week is 10 weeks stock - the most stock in 5 years.

Most people listing are in La La Land still when it comes to the value of their house. A 3 an 1 in Alicetown listed last week for 1.275M - meanwhile in nearby Woburn (The hutts highest price suburb) a 3 and 2 is listed at the same price and thats been on the market 3 months, whilst in the next suburb in Petone - equivalent 3 and 1's (some with more land and floor SQM) are going for less than $1.1M.

Another house in Stokes Valley listed for 1.15M - 100K over its homes and QV valuation - meanwhile much nicer houses are currently listed at 100-200K below their QV and homes valuations and have been on the market 2-3 months.

Surely Real estate agents can clearly see the market, the equivalent stock and current prices - your just wasting yours and the sellers time listing in a slowing market at a ridiculous price

Been watching the Hutt market as well. Seems rent prices might be coming down. And I agree on some of the asking prices - take this one;

https://www.realestate.co.nz/42086594/residential/sale/10-martha-lawson-lane-central-hutt

2 bed, two bath (row) townhouse on 123m2 land. Asking Over $1,145,000.

Purchased in 2019 for $850,000.

So many of these have sprouted up in the past two years, I fear a lot of these owners might have purchased a devaluing asset. And, as I mentioned, rent prices seem to be coming down.

I saw this one too, interestingly its QV valuation is $1 410 000 - they think its a 3 and 1 and not a 2 and 2 - so this is a good example of an agent listing it more closely to what its worth, although given most of the 2 and 1's are selling at $600-750K in the valley and it was built before 2020 (so the "new build" tax laws dont apply) you would think it would be too pricey for a FHB and unlikely to be of interest to an investor who can pick from multiple developments at the moment.

What does '3 and 1' mean? Three bedrooms and one carpark I assume?

it means 3 bedrooms 1 bathroom

It's certainly a significantly better than average quality of design and finish.

I assume that they feel they can get that kind of price given the potential to convert the study to a bedroom? Relates to the conversation I initiated the other day about my own townhouse and potentially adding another bedroom.

true- i was thinking a downsizer who doesn't want a garden and house to maintain, wants to walk into the CBD - would probably pick it up. Sell their big house in neighbouring suburb Woburn for $1.6M and have plenty of change left over.

Can't see myself ever wanting to downsize to a section that's smaller than the house :-). And the Woburn house on a full (600-800m2) section would be worth over $2m in comparison! Plus, these common two story townhouse designs aren't the best for a retirement home as all the bedrooms are upstairs. But, yeah horses for courses. But to me, even half a million for a row house is way over the top. NZ market prices are in lala land (the one I live in included, of course!).

You're right. From experience I would not recommend those over 50 years buying a two or multi-storey townhouse. Time flies and before you know it you are in your 60s and suddenly you feel yourself making mis-steps, and then you hit your 70s and you find climbing those stairs several times a day more of an effort. I'm in my mid-70s and fortunately have a one storey townhouse, but I have similarly aged friends who have multi-storied town houses and wish they didn't for the above reasons.

In fact, I would recommend that anybody wishing to by a property to see them through retirement should be looking at this matter from their 40s.

And, of course, nobody with young growing children should confine them to a puny townhouse with no space to play outdoors.

Depends where those townhouses are (re parents with young children). I've seen good ones in places where the provision of shared and council green spaces provides the kids with a far better play environment than just a smaller backyard would. Not all, of course...

Totally agree with Kate and Streetwise multi-storied townhouses are dangerous as you age and make you lose your independence earlier. With young children you have to be so much more careful than in a single level home. Craziest I ever saw, was a three level town house in a nice Wellington area with kitchen and living room on the top level. Who wants to carry their groceries up three levels? Also not recommended for elderly pets.

When I was working for one of the big ones it was routine when trying offer new lending to customers who had previously gone through brokers that the broker had cut so many corners that even with more equity, and better income, this customer would never have got that same lending now 2-3 years later.

This CFFFA "credit crunch" is more a symptom of,

- Banks choosing to trust broker applications

- Brokers framing themselves as the "People's champion" by cutting corners for their customers and over extending credit

- The whole industry having to little to no hindsighting

- The Government not fully understanding what was happening in their own home

When the minister of finance is a lawyer first, the CEO of a bank a politician, the broker a cowboy, and the customer is to be sheared (with the odd skinning), it's no surprise that when a law with teeth (even baby teeth) get introduced everyone is doing their zip up and seen running from that sheep.

The real question is who gets sacrificed first for these years of over leveraging our children, will the Banks catch the Brokers, the Government catch the Banks, or the less likely (but much needed) we finally catch the Government?

Great post. Sounds like there has been a sort of kiwi-version of liar loans via brokers. When will we ever learn?

Agreed. Very apt and humorous angle to you post. Adding in a bit more, sheep that have recently been absolutely well "fleeced" do not do well when the inevitable late winter storm hits. Many are lucky to be recycled into dog food.

I do recall seeing and hearing some pretty sketchy advice from mainstream brokers when dealing with them and when viewing their posts in a private Facebook group. "Just don't tell them" in various ways, even up to the level of disclosure in a portfolio split across different banks. Which seems...interesting.

Brick to much sense , cut it out , tax payer will be left holden the bag..

Jacinda will walk off into the sunset...later this year

Here's Robbo.

A common one from brokers over the last couple of years "we'll just say you're going have 2 boarders paying x amount per week, that will increase how much you can borrow" They have been the masters at fudging applications...anything for the deal to work and to get that comission. I have no doubt they're coming up with new ways to work the system.

Nifty1 you are 1,000,000% correct here, I once went through one of the nation's "top brokers" to see how his lending methodology differed from the Banks.

People in my office now call him Weasel, and they were already fairly loose themselves.

I wonder if some have been trying on an 'ethnicity angle'.

That is, multi-generational living is common in South Asian and East Asian households.

Brokers might argue that households will have boarders (relatives) from Asia staying with them, studying here.

So when Mr and Mrs Patel are looking to buy the 4 bedroom house with their one child, just put down that two cousins from India will stay in the 3rd and 4th bedrooms, netting say $400 extra.

When providing lending one should always ask,

"How would you defend your acceptance of this lending application if it landed you in court?"

If your reason for extending Mr & Mrs Patel lending was because of an assumption based of ethnicity then you'd quickly be staring down the barrel of a fairly unpleasant court ruling.

The main job of a lender is to extend credit while mitigating risk and adhering to the law, assumptions don't fit well with those preogatives.

Respectfully, the main objective of the bank is to push credit onto consumers and businesses and earn their interest (as their income) and play within the boundaries of the law.

If banks are able to use brokers to 'help' consumers take out loans and to 'own' their own homes, the bank has simply outsourced their sales teams and reduced their legal liability in the case of court proceedings made against by any consumer in the case of irresponsible lending or mortgage fraud.

The bank will simply argue that they had 'accredited' mortgage brokers on their panel and it was them that had to do reasonable checks on their income/s and character and due diligence on their loan applicant before submitting it to the bank's credit assessment team for approval.

Any mortgage fraud caught will be in the the hands of a mortgage broker or firm rather than a bank employee and the bank will would be absolved of such criminal allegations. The former will take the fall for the latter.

The main reason house prices went up is interest rates we’re dropped too emergency levels now inflation is high around 5% interest rates raising and look like will go back to a normal level over next year, with inflation at 5% interest rates should be 7-8% also NZD tanking .huge amount people and investors over leveraged this is a perfect storm which will take down housing market. Some people on here still thinking it’s a small bump in the road. Wake up the banks know what’s going to happen most smart investors have already sold.

Wonder how long the RBNZ can pontificate on and "look through" inflation to defer raising interest rates to achieve their inflation target.

This expert talking on CNBC network, what if he is correct - possibility.

Check it out.

So many views.

A correction (beginning) then a melt up....followed by..

First signs of rain from the dark clouds gathering over the housing market

You folk misworded "ray of sunlight gathering over the housing market", for younger Kiwis.

Yes indeed, it could very well be. Here's hoping. The Govt would need to follow the Helen Clark line about stepping to take over the loans of young families that find themselves underwater with a bank that's getting nervous. Foreclosure happened to so many young US buyers that went underwater during the GFC. And for many of those, their household incomes/circumstances hadn't changed - it was just that the value of the homes plummeted and banks got aggressive.

What about property investors? Would it be fair for the government to step in for them too?

Obviously not. On a financial website we should surely all agree that investments are about risk and reward. The government taking risk out of an investment (as they and the Reserve Bank have done in the last year) changes property from an investment into a welfare scheme.

I can't wait for the government to use my tax dollars to bail out those who were less prudent.

I wonder what moral hazard is in Maori.

How'd you feel if you moved city/country, away from family, to purchase your first home just to have a smaller mortgage and take less risk. You then see the government bail out FHBs in the city your from, who fought over each other at auctions and purchased homes with 10% deposits with zero regard to the future...

This is what's going to happen.

Not a bail out - HC is talking about a taking over of the mortgage by a government entity. Effectively a transfer of risk from private to public.

Anyone who blames a FHB for buying during these crazy times must never have been a renter standing in line to get in to see a property behind 50 other hopefuls.

Get real. The world has moved on from 'in my day...'

The mean-spirited selfishness of some people never ceases to amaze me.

How is that not a bail out of banks and home buyers...?

January is coming to an end.

There's still room for upward valuation.

What is our economy made up of? If houses stop going up in nominal terms and people can't use them as cash machines then what level of reduction will there be of people buying rental houses, renovating and extending houses, decorating houses, plus boats and other purchases. If they let this happen (continue pulling back stimulus) then what's left? People don't seem to save up for this here. There's not much flowing in from overseas for tourism but I guess there's a few people making money from selling milk powder and logs. If that enough? High tech growing.. Maybe the struggle to attract talent/retain talent will get better if prices fall..i don't know how it works or what the main things keeping us going are.. . I'm hoping house price falls will force us to think of new ways for NZ economy to function Too bad we can't get into cannabis industry but there must be other ways.

The first ones are moving.

REMINDER: Registrations closing soon to buy a home below market value!

This is your friendly reminder to register your interest to buy one of the six brand-new one-bedroom homes in The Aviary Apartments by Monday, 31 January.

The apartments are capped at $650,000, well below market value, and are built from high quality materials with low ongoing maintenance costs.

Here are some key details:

- Priority will be given to first homebuyers who have a strong connection to Tāmaki, to help them get their foot on the property ladder

- We require just a $5,000 deposit (however, your bank’s lending criteria will differ)

- Each apartment comes with one car park

Visit our website to see if you’re eligible and to register your interest today. You won’t be locked into anything – it just lets us know you’re interested and helps us understand a bit more about you and your situation.

Great , I hope to pick up another bargain to add to my rental property portfolio

House prices have risen over 50% in 18 months and when they drop by 1% for one month everyone starts panicking and saying the sky is falling. What kind of property cult is this place?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.