The economic crisis and increasingly low interest rate environment have prompted people to make a range of sometimes contradictory financial decisions, according to new KiwiSaver data.

While a high portion of KiwiSaver investors panicked when share markets plummeted in March and switched to more conservative funds, those eager to enter the property market for the first time didn't hold back.

First-home buyers see opportunity

The value of KiwiSaver withdrawals by first-home buyers increased by 25% in the 2020 financial year.

First-home-buyers withdrew $1.2 billion in the year to March 31, according to the Financial Markets Authority’s (FMA) annual KiwiSaver report released on Thursday.

This was equivalent to 1.9% of the $62.0 billion of KiwiSaver funds under management as at March 31 - a slightly larger percentage than the 1.7% a year earlier.

More up-to-date Inland Revenue data shows there was a spike in withdrawals in March 2020, a dip in April and May, and then a recovery in June, July and August.

KiwiSaver withdrawal data matches bank lending data showing first-home buyers playing an increasingly active role in the housing market.

They accounted for a near-record 19.8% of new mortgage lending in August, contributing to the value of mortgage lending across the board reaching a record high for an August month.

‘Investing 101’ ignored

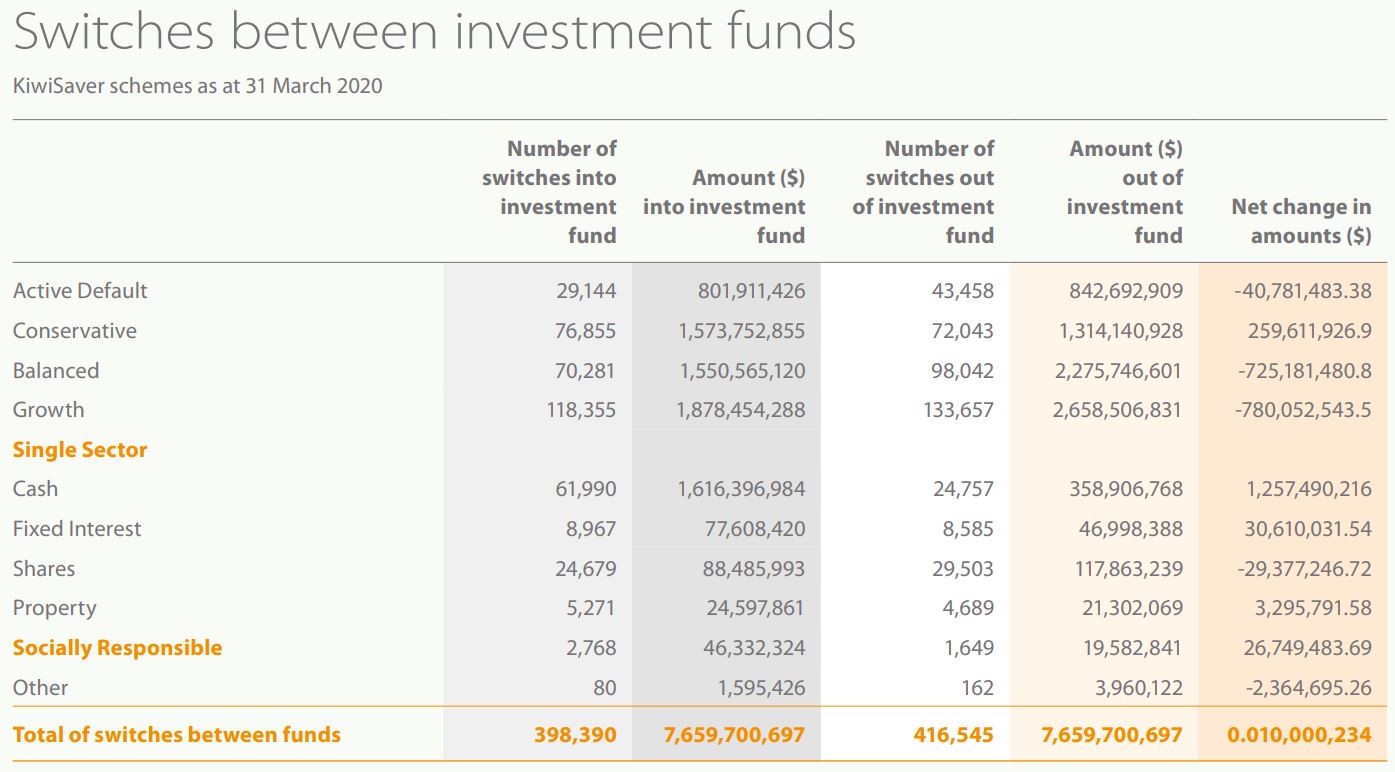

Elsewhere, the FMA’s KiwiSaver report shows the onset of Covid-19 prompted knee-jerk reactions from a relatively high number of KiwiSaver investors.

Investors switched $7.7 billion of assets between KiwiSaver funds in the year to March 31 - more than twice as much as during the previous year.

Of the $62.0 billion of KiwiSaver funds under management, 12% was switched between funds. In 2019, this portion sat at 6%.

The total value of assets in conservative, cash and fixed interest funds increased by $1.5 billion in the year to March, while the total value of assets in growth, balanced and shares funds decreased by the same amount.

FMA Director of Regulation Liam Mason said this level of switching showed there was still more work to be done preventing people from using their retirement savings to try to time the market.

“If the market goes down and you sell, and then the market goes back up and you buy in again, you’ve just locked in all those losses. And I think that might be the story for some,” he said.

While the FMA doesn’t yet have data on the months following March, Mason said anecdotal evidence suggested people started switching back to higher-risk funds relatively quickly.

Indeed, retail investors around the world piled into the share market during this time.

Mason said the FMA was wary of how the low interest rate environment was affecting investor behaviour. He was particularly worried about it from the perspective of those in search of yield potentially falling prey to scams (outside of KiwiSaver).

As for the high level of KiwiSaver switches, Mason recognised the ease of being able to do so online was a contributing factor.

On the flipside, he noted technology made it easier for providers to reach their clients; in some cases, prompting them to consider their risk profiles, as well as the risk of locking in losses when switching funds.

Hardship withdrawals subdued

Turning to hardship withdrawals from KiwiSaver, Inland Revenue figures show between about 1600 and 2100 people made such withdrawals each month between March and August. This was only slightly higher than pre-Covid levels.

However the value of these withdrawals was up more significantly from around $9 million per month pre-Covid to around $13 million per month between March and August.

36 Comments

The biggest scam is the rip of kiwisavers by the Government taxing their kiwisaver balances on 1 April 2020 of 5% deemed income (totally unrealised) at 28% after they all made losses to 31 March 20. No ability to get a tax refund for tax paid on 1 April 2019. Its the only scam going where you make losses and pay tax for the year and then pay tax again on the first day of the income year as your kiwisaver recovers to previous levels.

"KiwiSaver members paid $538.9 million to the managers handling their money over the year to March, but lost a combined $820.9m – and there are concerns some of them may have locked in those losses."

All the while the Government let capital gains on house be tax free.

Isn't the 5% applicable only to offshore shares? I get that it's not equitable if they have fallen, but that was always a risk in having foreign shares in KS and and shouldn't be a surprise. The other issue with KS is you have no interest deduction for leverage. Why don't you keep KS to NZ shares and get the exposure to international stocks through CFD or ETF outside KS?

All of us know the rules which I agree favour housing. I decided early not to fight it.

Correct. That is the scam. Most KS funds are realising 1.5% or less in dividends in offshore equities and they are deemed to get 5%. Its fine if its realised but not unrealised. I invest direct and via a trust in US equities and S&P500 but have a fair amount of money stuck in KS. I would not invest in NZ share market. I get the same treatment via the other methods too.

I dont believe most Kiwisaver's are aware they are getting taxed like this. Most on this site may.

My biggest problem is our Government wants to have a huge tax distortion in favour of houses. When the market cant sustain itself Orr and Robertson want to bail it out without artificial interest rates. All the while punishing anyone with savings.

To be fair OC, QE supports stocks as much as houses - we all benefit. I agree the incentives for housing are greater, the biggest of which is access to leverage.

Bollocks. Stocks are not leveraged like houses in NZ. Stock investors are not benefiting from the interest rates being driven down by central banks. You will say its propping the economy up but I don't agree. Would rather the market sort the housing market out not Orr and Robertson acting as life savers thinking they need to act like the FED in the USA.

Oreo. What few realise is the deeply negative consequence of years of the FIF capital tax regime discouraging offshore investment both through its inherent unfairness and complex administration. Most kiwis have missed out on the significant capital gains in investing offshore over recent years and the risk mitigation effect of having part of your nest egg outside the tiny and vulnerable NZ economy. We are a lot poorer as a nation because of this punitive tax, conceived in envy. Fortunately with the advent of KiwiSaver NZRs are finally beginning to enjoy the benefit of offshore equities but the playing field remains tilted.

I regular post on this theft on this site. Some even say I rant about it,

But kiwisaver theft is happening by the tax being charged on it.

The FIF regime did not apply to the grey list countries including the USA until a few months before the kiwisaver regime came in. It was the government of the days money grab to ensure they get deemed 5% income on all kiwisaver funds on offshore equities on an unrealised basis.

i'm not sure what your background in corporate finance is, but it's not 'bollocks'. What is the average leverage of the NZX50? i'm picking at least 3 or 4 to 1 D/E, highly likely to be more levered than the average house. If you don't think stocks benefit from QE or that you own equity in a levered vehicle, I'm going to leave you to it.

You not reading what i said. I said STOCKS meaning the INVESTORS who buy the STOCKS are not leveraged like houses. It is bollocks saying that stock investors have benefited as much as the debt fueled buying houses,

Owners of stocks are not being bailed out like the owners of houses getting mortgage deferrals to sustain them and artificial manipulation in the market to drive the interest rates down. As trading banks wont lend on stocks.

If we had no QE and no Mortgage holidays there would have been forced house sales. There would have been no forced stock sales per se by no QE and no mortgage holidays

We'll have to agree to disagree, there has been plenty of support for industry. The NZX50 is up almost 50% from it's low in March - are houses up 50%? QE supports most assets. Put your anger at housing to one side and look at the facts. Also, supporting housing supports consumer spending which again indirectly benefits business. The system get's bailed out, not just homeowners.

Agree to disagree. NZX50 is down from high in Feb. Yes it has gone up and down but if you owned the NZX50 in mid to late Feb and are still in the market you are sitting on a small loss of 2.5% but effectively you are even. So its gone nowhere.

I'll give you that, but it's still up 100% since 2015 - it's definitely not 1 for 1. but the correlation will be quite positive.

...still more work to be done preventing people from using their retirement savings to try to time the market

Where is Kate? She thinks it's all to easy to time the market.

Real tragedy the number of long-term investors that don't stay the course and end up locking in losses when they panic and swap to conservative when the market is down.

My comments here went unheeded:

https://www.interest.co.nz/news/104176/nz-super-fund-ceo-has-dropped-89…

My growth KiwiSaver has now recouped the losses from earlier in the year. Those that switched to conservative would've missed the upswing and locked in the losses.

Agreed timing is a fools game. But one can take advantage of the panic and buy stocks when on sale and everyone is fleeing. I invested heavily in mid march in US stocks as they were on sale. By August those investments were up 45% but have pulled back a bit to around 35% now. I am making it sound easy but they were stocks I had been investigating for some time. But one could have just bought the S&P index and achieved similar.

Oreo. Buying stocks when on sale is a limited form of market timing. This has also been my very rewarding strategy for many years and as you say, it’s not especially difficult to identify when the world is on fire and buy into index funds. While the egregiously extortive FIF tax regime appears administratively complex for average joe citizen, the calculation is actually reasonably straightforward once you get your head around it and for those who don’t wish to a suburban accountant will do it at modest cost.

The difficulty is a mental one hence the reason even when NZ announced a lock down all the capital flew out of the NZ market. Most cant go against the crowd and buy when everyone is shouting sell sell. I am not talking in a small way more meaningful amounts of say a house value or double or triple them.

The calculation is not the problem. You are robbed of compounding by paying tax on an unrealized income that you may never receive and you cant claim a loss or claim a tax refund for tax paid when you never receive it.

You also pay tax again when if you hold and your stocks recover.

I made helluva money when I bought during and after the GFC, so I can say that I did time the market successfully then.

To my deepest regret, however, I must say that I completely missed the mid-march dip - I was stupidly waiting for the market to dip significantly more, and so I ended up missing it out almost completely. It is not just about identifying a dip and buying it, but also estimating how deep the dip is going to be.

Good on you for getting the mid march dip right!

My growth KiwiSaver has now recouped the losses from earlier in the year. Those that switched to conservative would've missed the upswing and locked in the losses.

A monkey could have made money in these markets.

A monkey in a growth fund would've. They don't have the wherewithal to switch to a conservative fund. A panicked human of low acumen on the other hand could easily lose out by switching, and plenty did.

Cash Fund is King.

Unless you’re beginning your working life.

Most of the KS annual gains come from your employer contribution and the Govt June gift.

The investment returns are proportionally minimal if you’re in the last few years of working life.

I wouldn't agree. Just looking at the last 10 years, my investment returns on KS make up 36% of my total balance. That's a huge amount to have missed out on if you were 55 back in 2010.

Interesting.

In my case (cash) returns = 14% of balance over 10 years.

What's the problem here? If people want to buy houses with their savings, let them do as they please. Furthermore, this is what the ruling elite wants, isn't it?

I would happily have access to Kiwisaver to pay down mortgage I have retired early at 60 and feel I can make better use of KiwiSaver funds.

Great to see greater FHB activity.

I wish them well and provided they can service the mortgage they have little to fear as short term fluctuations are irrelevant.

Data doesn’t indicate the timing of withdrawals but to date those who have been in for much of the year will have seen increasing property prices. This is contrary to what many were posting last year on this site . . . I hope that those posters acknowledge this at least to themselves.

IMO, all allowing FHB to withdraw their savings has done, is increase house prices even more. I means FHB can afford to pay higher deposits more quickly, to allow them to get larger loans. It is going to end in tears for some when they realise they have paid too much compared to their earnings, and if prices go south and some lose their jobs. We have been warned that we are in for a rough time in the next few years when the real economic effects of covid start to take effect. .

WtgnInvestor

Yes, we live in turbulent times and as always there is risk and currently some heightened risks but it is not all doom and gloom.

Its great that while there are affordability issues for FHB, interest.co notes that due to falling interest rates this is improving - that's great news and something many FHB have wanted. $1b taken form KiwiSaver accounts is support for FHB.

However, as to risks for FHB, banks are taking a conservative or cautionary approach. It is not in their interest to have borrowers defaulting on mortgages so they are protecting their butts.

- Banks are looking at employment records more closely - and have been criticised for this - as what was fine pre-Covid, is no longer fine now.

- Short term fluctuations ("if prices go south") are not significant provided one can service the mortgage - so yes, having job and income security is more important.

- Despite fall in mortgage rates, the banks continue to apply a 7% stress test - can borrowers still afford loan repayments if interest rates go to 7%. Talking to a mortgage broker who said many FHB are missing out on this criteria.

- Interest rates are considered by most commentators to be low and remain low for longer - and RBNZ signaled this with the proposed FLP which was specifically noted as intended to reduce borrowing costs for households.

- Government is currently keen to see employment high as part of the post-Covid recovery. Already they are announcing support for apprenticeships and trade training.

For a FHB, if your bank is prepared to lend to you, then they have assessed your risks and have deemed that its acceptable to them. The general view is that banks are not lending recklessly.

I don't think banks are being as conservative as you think, P8. I have an approval from last month (post covid) for an amount that, should interest rates go to 7%, would mean my mortgage would be 65% of my take home pay. I've also had it suggested by brokers and agents and the like that I should lie about intending to have flatmates.

I don't think its sensible advice to tell people that if the bank says you can afford it, then you can afford it. Potential FHBs need to do their own calculations.

I agree, I'd be willing to bet most approvals are being provided on the basis of dual income no kids. Are banks just expecting none of these FHB are going to want to start a family? What happens when one wants to go on mat leave?

The problem is the increasing house prices, and not affordability. Affordability can be changed with the flick of the switch when the reserve bank reduces interest rates. But al that does is increase asset prices. When these increase more than inflation and wages, then the gap between the haves, and have nots grows. NZ already has some of the highest house prices vs incomes,. One problem is just a lack of tax around housing. But the main problem is people can buy cheap money, and there is a lack of supply.

This recent asset price bubble is occurring all over the world during the pandemic, and history has shown that bubbles can pop.

We are ready to condemn those that try to time the share market lows and highs as bunnies . . . and likewise those who reacted to KiwiSaver despite financial advisors suggesting otherwise.

But I would have lost count of the numerous posters on this site both during last year and during the height of the Covid lockdown to time the market - “wait, wait for the market to bottom”. The market didn’t bottom . . . rather there were significant increases. Do we categorise those posters likewise as bunnies?

Great to see those FHB with initiative make a commitment, get on with their life enjoying the security of homeownership for them and their family, and doing well.

Yes, hindsight is great, but they were clearly looking at the signs and prepared to back themselves. Need young Kiwis like that.

Housing is the one thing that should be allowed for Kiwisaver withdrawals because it supports retirement hugely.

There is a problem looming with people who still rent at retirement. Owning your own house completely is eessential at that time.

Also. Yes. Timing the market cost some folk over lockdown. On the other hand going conservative might be a good long term strategy as the market seems shaky to me

I was there in the 80s. Made big money on shares, then got scared and withdrew completely. Later crept back in, in a small way, and then in 87 whammo, lost big.money on the smaller amount.

The bad thing can happen.

There is a problem for rest homes, if people still rent at retirement age, because they won't be able to sell license to occupy contracts.

Yes, yes we do categorise them as bunnies

Very charitable of you P8

It’s time IN the market, that is more important than when to get in (caveats obv)

Yes, I'm a bunny.

Failed with every plan (the only thing I didn't plan was kids and they turned out fantastic) entirely and now expect to rent in retirement. There's no way I can expect make enough by working to buy a house. An alternative will be a camper or caravan.

Overall, NZ house prices fell 1.6% from February to May. Not earth shattering news, but when we drill down into area with a large sample of sales, we see Hamilton and Tauranga bucking the national trend lower and actually showing a minor increase in value, no doubt owing to their low exposure to tourism and hospitality industries. A promising sign for local investors. Wonder what will be the effect on kiwisavers. JM | Insect control

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.