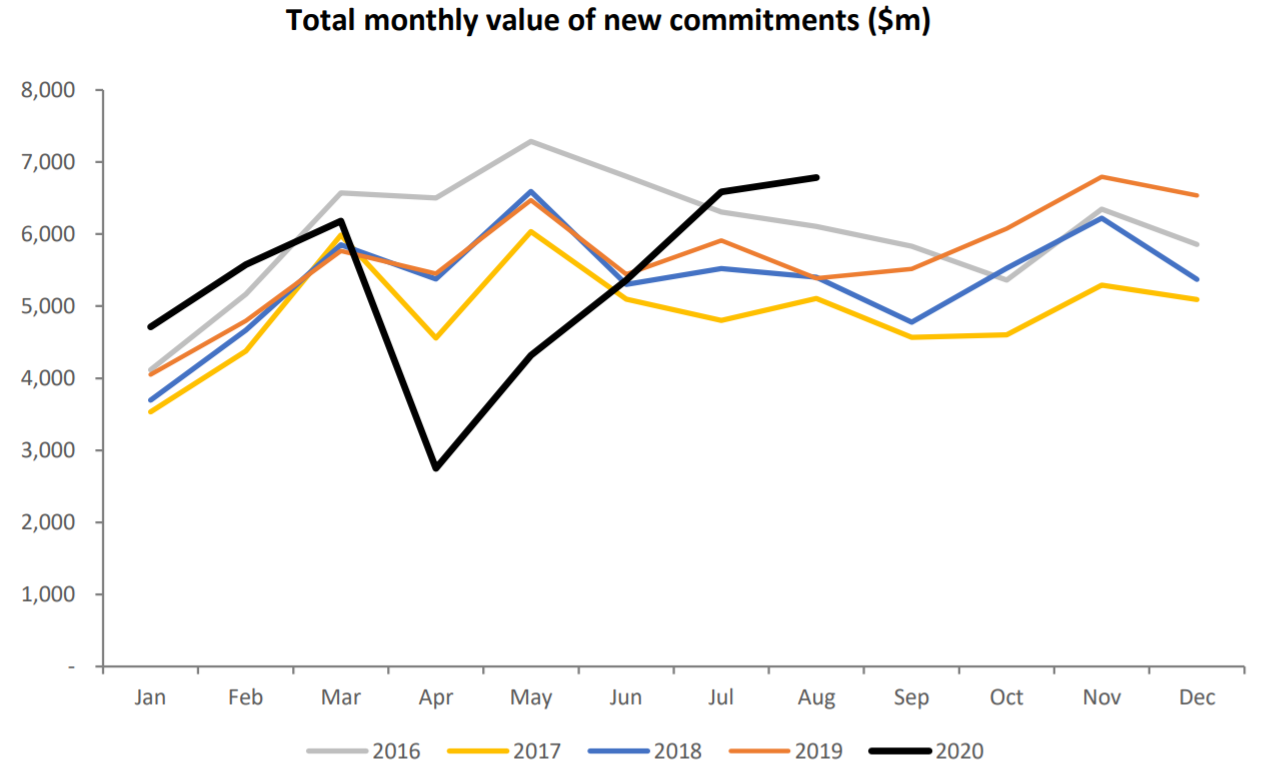

The housing market's bounce back from the lockdown has continued strongly, with mortgage lending last month hitting a record high for an August.

The latest Reserve Bank residential mortgage lending by borrower type figures show that nearly $6.8 billion was advanced in mortgages last month

This follows a record for a July of nearly $6.6 billion the month before. The RBNZ has been compiling this series of monthly data since 2013 and publicly releasing it since August 2014.

The all-time high in this data series for ANY month was the nearly $7.3 billion advanced in May 2016, which was shortly before the RBNZ applied tough lending limits on investors. The RBNZ in May 2020 removed all the loan to value ratio (LVR) limits, including those on investors, for at least 12 months.

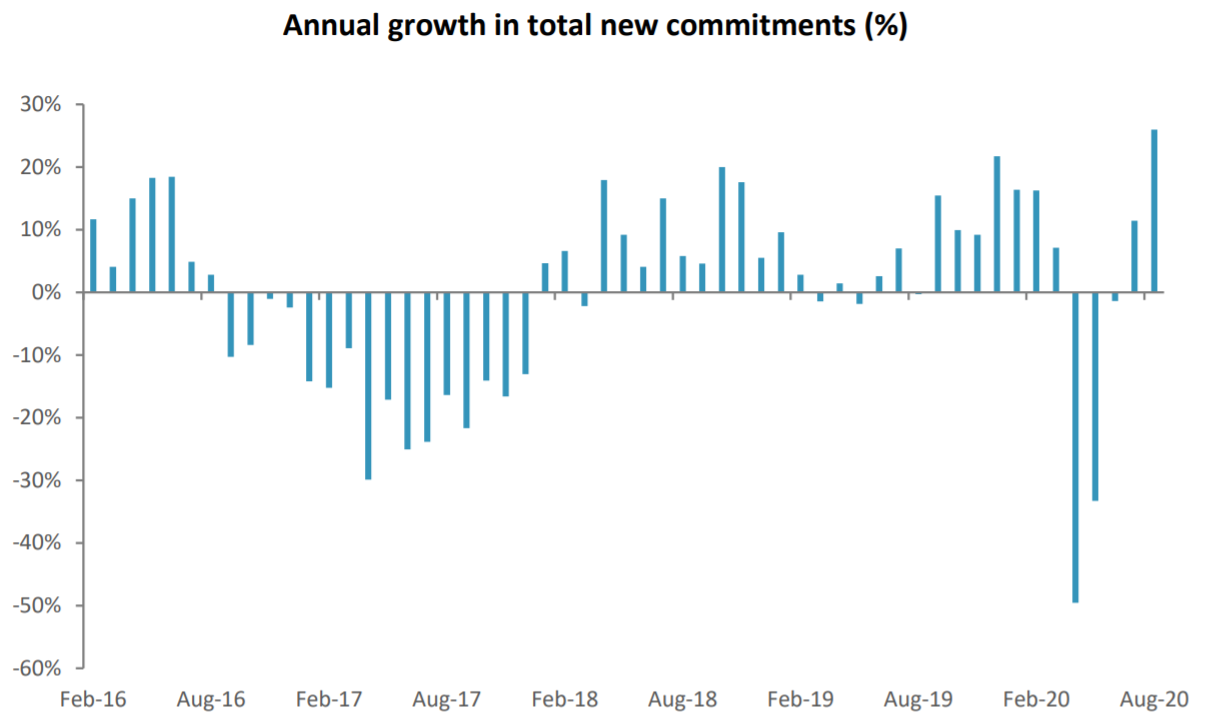

The $6.8 billion borrowed in August 2020 was up some 26% on the figure for the same month a year ago (nearly $5.4 billion). Last month easily surpassed the previous record August tally, which was $6.1 billion in August 2016.

In August 2020, first home buyers were again strong in the market, exactly matching their record borrowing level of $1.344 billion borrowed in July 2020. The July FHB total was also a record in terms of its proportion of the total - at 20.4%. Of course because the overall amount borrowed in August was higher, then the FHB proportion dropped a little - to 19.8%.

Investors borrowed almost exactly the same amount in August as they did in July too, with $1.452 billion.

The amount of high loan to value ratio borrowing by investors (regarded for investors as loans of more than 70% of the value of the property) again increased, though not by as much as the previous month when it more than doubled. High LVR borrowing from the investors totalled $491 million in August, which was up 10.3% on the high-LVR borrowing in July.

Among FHBs, their amount of high-LVR borrowing (which for them equates to over 80% of the value of the property), was $554 million, which was slightly down on the $577 million of high-LVR borrowing they did the month before.

The market has been stimulated by ever-lower interest rates. On the one hand this means cheaper, more affordable mortgages, while on the other the very low rates now available on deposits make alternative investments, such as property, appear more attractive.

Now the Reserve Bank has indicated it will likely go ahead before the end of the year with a Funding for Lending Programme (FLP), involving directly lending to banks at cheap interest rates at around the level of the Official Cash Rate (currently at 0.25%). This will put further downward pressure on retail interest rates both for mortgages and deposits. And this could well be supportive of the housing market in the run-up to Christmas.

Here's some of the highlights of the month's mortgage figures as detailed by the RBNZ:

- Total monthly new mortgage commitments were $6.8b in August – the highest August on record since the survey began in 2013. This is an increase of $0.2b (3.0%) from July 2020 and up 26.0% from August 2019.

- New mortgage commitments to first home buyers were $1.3b in August and remained consistent with July while other owner occupiers increased from $3.7b in July to $3.9b in August.

- First home buyers accounted for 19.8% of new mortgage commitments, down from 20.4% in July while other owner occupiers share of new commitments rose from 56.7% in July to 57.9% in August.

- The nationwide year-on-year growth in value of new mortgage commitments to first home buyers was 45.6%, while new commitments to investors was up 41.9%.

- The year-on-year increase of 26.0% in new mortgage commitments was largely driven by Auckland region. New mortgage commitments in Auckland increased from 3.9% in July to 24.5% in August, while new commitments outside of Auckland rose from 17.6% to 27.1%.

- Monthly new mortgage commitments with high loan-to-valuation ratio increased since the restrictions were removed in May 2020. High LVR new mortgage commitments to investors saw an increase of 10.3% in August.

37 Comments

Any sane person should be concerned...borrowing more as the economy goes down the toilet.

Then they lower rates and undertake a massive media ra ra ra yip yip yippeeee role up fill you pockets and pump those house prices campaign to keep it all going.

Yes they think bidding up houses will pull us through.

Mental.

Any sane person should be concerned...borrowing more as the economy goes down the toilet.

At the same time, the Aussie bank share prices are under severe pressure. For ex, ANZ's share price is down 50% since 2017. And these are stocks paying world-beating divis and with franking credits. Make a huge proportion of the ASX and Aussie h'holds have piled into them.

What is this telling us?

It's telling us that investors don't like it when the RBA/NZ allow their banks to hide non-performing loans. Share prices plummeted when the RBs said COVID deferrals don't have to be reported as non-performing - how do you value a bank when they hide their exposure to this crisis?

Stock price has been in decline way before Covid. It really started at the GFC.

Criminal

You should dial 111

Can they put me through to the SFO?

Have a go mate....do something

.

RBNZ need the banks to substantially increase the amount they lend each month. Have a look at this recent upload which might give us some clues as to what could be on offer soon to lure in a few more buyers. https://youtu.be/qL-CZWc3RME

The buying of debt by investment banks for bundling (securitization) has already been happening again in the U.S.

Good vid - thanks.

Another piece of bate could be home builder grants, which they are doing in Oz ($25k):

https://treasury.gov.au/coronavirus/homebuilder#:~:text=HomeBuilder%20p….

Have been watching that and also watching the land prices go up $25k. Funny that.

The Reserve Bank’s (RBNZ) Monetary Policy Committee is planning to introduce a FAYS programme.

"Well, behind the scene, FAYS has been running for quite a few years, but we'll publicly announce it in coming months."

Excuse my ignorance sir, what is FAYS. "That's the F#%k all you savers" programme.

It's all going to be interesting from here.

Tbh as someone wanting to buy but can't understand the market (i.e. current prices) that is a justification I play with

Has this statement been totally defunct by the RB's / FED

“Be fearful when others are greedy. Be greedy when others are fearful"

Warren Buffett

The shepherd (RB's / FED) will look after the herd.

My 2020 interpretation of this statement goes perhaps something like this:"Be fearful when ALL others are fearful. Be greedy when ALL others choose to be greedy."

I think that is much more sensible. Two thumbs up!

Buffett is proving to be right on largely staying out of the market and also noting if you do be prepared for the very long haul. The US share market is starting to pull back significantly even with the FED doing as much QE as they can and making its statement this week that they will be there for as long as it takes. Apple is now down over 25% from its recent high.

Bugger - re "That's the F#%k all you savers" programme. Funniest Sh#t i have read on here in a while.

I find the number of borrowers a more telling measure due to changes in property prices (and consequently the size of mortgages) fudging the results as has proved to be this month.

The number of borrowers, number of FHB and number of investors all down from July. To me neither consistent with the tone of the article nor a seemingly hot market - dgm will be happy with that.

The reduced numbers may well be due to Level 3/2 lockdowns from 12 August but worth noting what happens over the next few months.

Changes in number of borrowers July to August were:

- All borrowers 25,641 down to 23,844

- FHB 2966 down to 2884

- Investors 4324 down to 3935.

Still 9,703 FHB and investors in August who by choice thought it a good time to be buying.

Hi Printer

factual and honest as usual.

I continue to suspect that there is a limit to pent up demand that resulted from higher int rates and LVRs prior to May 2020

Ie there is a finite number of folk who have been waiting to buy and held off pending recent easier conditions re finance/regulation and a finite number (at this juncture) who are able and willing to move up 10% on their borrowing re price bracket and/or mortgage.

My inkling is that this wave is slowly subsiding and will flatten as October ends.

Then we will see a normal market til around end of February, after which all bets are off as no one really knows how bad or good the economy will be for rest of 2021.

Entry level properties in the Auckland Double Grammar Zone appear to be getting extraordinarily good prices currently. Brick and tile units going for 1.25M for example.

Looks to me that we are leaving behind a stable period and entering a chaotic period. We get fat and lazy start experimenting with socialism and the wheels come off.

We rob Peter to pay Paul. Then the gods of the copybook headings with terror and slaughter return!

This is just gross....does the RBNZ have no shame?

I'm actually sitting here at my computer desk drinking a couple of strong whiskeys right now, pondering what might have been. It seems to me whoever doubts the Auckland property market is punished by the gods of property. Never, ever, sell an Auckland property unless you absolutely have to. They rank amongst the world's greatest treasures.

They might be cold, damp, sh*t boxes, but that is irrelevant. The facts speak for themselves.

Yep. Many NZers believe NZ and Auckland are the best places on the planet. Granny Herald occasionally runs an article quoting a travel magazine to reinforce this.

Yeah, I've always been cautiously optimistic and slightly bullish, always tried to hedge, and not overleverage.

To some, maybe I've appeared slightly aggressive, but could just be my risk profile. I think I'm slightly conservative in risk though.

Anyhoo, it is looking pretty ridiculous the prices for Akld houses. Especially if they're not flatlining from here

Then again term deposit yields are ridiculous too...

Not a hell of a lot of winners anywhere really, esp if this makes a greater divide

I do think behavioral economics and financial literacy should be more compulsory than some other subjects at school

I'm sitting at my computer drinking a glass of wine and almost chocked laughing at your comments. If Auckland is one of the worlds greatest treasures , you've been in your bubble far too long...LMAO!

Real prices seem likely to move downwards sometime. If so, will it be through a devalued currency or falling nominal prices? If by falling nominal prices, will it be triggered by future rising interest rates (the usual trigger) or something else? E.g. a collapse in demand after NZ population decimated from the, presently unknown, full impact on life expectancy due to the Wuhan virus?

Does anyone think the LVR limits will come back on. There must be some pressure to tame this market

tillers

Not sure - they don't seem interested in taming the market. .

Announcing FLP policy (with the stated intention of lowering mortgage interest rates) will be adding fuel not taming a hot market.

Treasury needs to take some responsibility for under-estimating how long Covid-19 infections will affect NZ.

In its May forecast I thought Treasury had its head in sand when it forecast all international borders would be open by 1 April 2021.

In their latest Sep forecast they have changed border opening to 1 Jan 2022 & have assumed from 1 Oct 20 to 1 Jan 2022 NZ would be at Level 1.

To assume no further resurgence of Covid-19 in NZ until borders open in 2022 is again far too optimistic & this is reflected in Treasury’s overly optimistic forecasts.

NZ government needs to look closely at its Net Assets as they could get perilously close to zero In next 5 years if NZ had several resurgences of Covid-19 or another major disaster.

If that happens NZ’s credit rating will fall, unemployment will continue to increase, interest rates will rise & housing prices will fall.

Note the Reserve Bank’s stress tests showed that if unemployment increased to 13.4%, house prices would fall 37% & banks would just be able to cope, but if unemployment increased to 17.7%, house prices would fall 50% & NZ banks would require a $7 billion dollar bailout.

Treasury’s optimistic forecasts suggest that NZ government would be able to bail out the banks but I think Covid-19 resurgence will continue in NZ over the next couple of years as well as another disaster related to climate change. If this happens NZ will look back in 5 years time & wonder what happened to all the government’s Net wealth & Kiwis lost property values.

Unfortunately, Treasury and practically ALL economists are pervasively over-bullish on the future.

Witness chronic over-est of future GDP over many years, esp in USA.

GDP had been falling each half of year, for 2 years prior to CV19 arrival and at that points only 2.25% pa.

Ie with inflation deducted, GDP growth was nil in February 2020.

So, it is highly improbable that GDP will rise above zero growth prior to end of 2021, despite predictable trumpeting from gov and MSM when it rises 10% in next quarter, RELATIVE to Q2 only.

Adrian and his Reserve Bank cronies have completely lost their mind! We all know not a cent of that FLP is going to businesses, it’s all gonna get poured straight into houses.

Just when the Aussie reserve bank governor admits publicly that property prices could fall 40%, ours acts to prop this sucker of a ponzie scheme up come hell or high water.

The question becomes which direction is more irresponsible- propping it up or letting it correct? We’ve reached a point where both directions are highly detrimental to our economy.

The young and poor are being ignored by Adrian Orr. In the USA the protestors have found that their voices are only heard when they protests right outside of the home of their oppressor. I bet a group of 10'000 would make the MSM news and would help inform the masses of exactly how Mr Orr's policies are ruining their lives whilst making the rich MUCH richer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.