By Jenée Tibshraeny

Question: “Why have you changed your KiwiSaver provider to your bank?”

Answer: “I figured it was easier to have everything in one place. Plus, now I can keep track of my KiwiSaver through my bank’s smartphone app. All I need to do is type in a four-digit pin to access both my bank and KiwiSaver details on my phone. Easy as.”

Question: “Do you have any idea how your new fund has been performing?”

Answer: “No. The bank teller, who served me when I went to tend to some other banking matters, told me the fund was doing well, so I figured I may as well jump ship.”

I take it this conversation I recently had with a fellow Gen Yer is making you wince. Common sense says you should choose a KiwiSaver provider based on its performance, not convenience.

But the reality is, we live in a “now” society. If we can’t access information quickly from wherever we are – the bus, the gym, or the office kitchen – we probably won’t access it at all.

For Gen Yers in particular, sifting through KiwiSaver statements in an arch-lever file, seems prehistoric. Not only do we want to manage our personal finances online, but we want to manage them on the go through our smartphones.

I trust those of you who take pride in your well-categorised arch-lever files are rolling your eyes at ‘the youth of today’, but we can’t ignore the fact this is where the world’s going.

The wonders of technology

ASB’s executive general manager of wealth and insurance, Nicholas Stanhope, says:

“In the same year that Steve Jobs launched the category-killer Apple smartphone, ‘iPhone’, the New Zealand Government transformed retirement savings with the world’s first national auto-enrolment savings scheme, ‘KiwiSaver’.

“Nine years later, more than 2.5 million New Zealanders have joined KiwiSaver, and one in five of them are using smartphones to engage with their KiwiSaver accounts.”

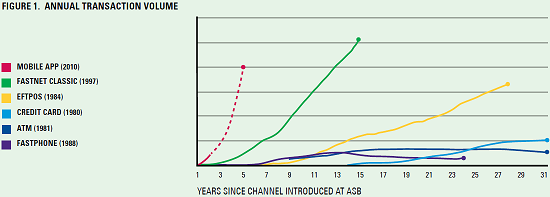

Contributing to KPMG’s Funds Management Industry Update 2016 released today, he says: “At ASB, when EFTPOS and online internet banking launched, they quickly became mainstream, and at the time it seemed the rate of adoption was fast. But ASB’s mobile app has seen even faster adoption.

“ASB KiwiSaver members, for example, are now making as many payments through the ASB mobile banking app, launched five years ago, as they are via the ASB online internet banking platform, launched 15 years ago.”

Stanhope says accessibility encourages people to pay more attention to their KiwiSaver.

“Making KiwiSaver more visible for customers via their preferred channels helps keep their long-term savings top-of-mind. This is important in the world of investments, as it can correlate to greater financial literacy.”

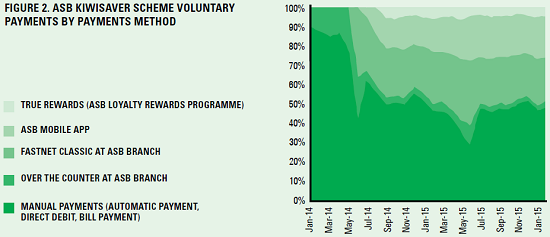

He notes digital platforms are also seeing an increasing number of people make payments into their accounts.

“This [digital payments] removes barriers for members who are not PAYE employees, and therefore can’t use salary deductions to contribute to their KiwiSaver account.

“…Enabling members to perform self-service activities on their KiwiSaver account demonstrates a maturing of the KiwiSaver product. It has transitioned from having its market growth driven by incentives to having growth generated by members looking to maximise their returns.

“Online fund switching is another example of this. This self-service technology development has been swiftly adopted by members.

“In the year to 31 March 2015, default KiwiSaver providers received 26,392 fund switch requests from default KiwiSaver members, who initially invested in default fund options. The largest recipients of these fund switches were growth funds and balanced funds, which have a larger proportion of growth assets.”

Digital divide puts banks ahead

I couldn’t agree more with Stanhope’s comments.

People will surely become more attentive to saving for their retirement, by having access to their KiwiSaver accounts at their fingertips, in the same way I’ve become more attuned to my spending habits since the advent of mobile banking.

But there is a “but”. Most non-bank KiwiSaver providers don’t have mobile platforms.

This I believe, may go some way to explaining why an increasing number of people are switching KiwiSaver providers to their banks.

For example, ANZ gained a net 24,298 KiwiSaver customers with net funds of $210 million in the year to March 2015 (when subtracting those who left its scheme from those who joined its scheme).

ASB’s KiwiSaver scheme gained net funds of $190 million during this time.

According to Morningstar, ANZ has grown its market share to 26.0%, up from 25.8% last quarter. ASB remains in second place, marginally increasing its market share to 18.6%. AMP remains in the third spot ahead of Westpac, while Fisher Funds (49% owned by TSB) remains at fifth.

Morningstar notes the industry continues to get more concentrated, with the six largest KiwiSaver providers accounting for 86.2% of assets on its database.

The performance of banks’ KiwiSaver funds has undoubtedly also contributed to them attracting more members. ANZ’s funds have been performing particularly well.

The Financial Markets Authority has also been investigating banks’ sales processes when it comes to attracting new KiwiSaver members. SavvyKiwi founder, Binu Paul, says there's anecdotal evidence which suggests banks have been known to offer lower mortgage rates to those who join their KiwiSaver schemes, for example. He believes it isn't a systemic issue, but happens nonetheless.

Looking beyond convenience

Bad sales tactics aside, there is of course nothing wrong with having your bank as your KiwiSaver provider. My concern is around people – particularly Gen Yers – choosing providers based on convenience rather than performance.

After all, KPMG partner and head of financial services, John Kensington, warns the average New Zealander is financially illiterate, often sticking to their default conservative fund even if they’d be better off in another fund.

This illiteracy, coupled with Gen Yers’ love of technology and banks’ savvy online presence and marketing tactics, can be a recipe for disaster.

It is for this reason I urge people not to be lured by the convenience of shiny mobile apps, but rather seek advice or use the online tools available to choose a provider on its merit.

The Commission for Financial Capability’s investor education manager David Boyle says: “Convenience is great, but that has to be aligned with having really good quality information and a bit of education around the fund that members are in, and how that impacts their overall financial wellbeing.”

While he admits convenience is one of the larger factors causing people to switch funds, he believes people will start paying more attention to the health of their funds as they grow.

Non-bank providers need to up their game

In the meantime, I urge non-bank KiwiSaver providers without good mobile phone apps to get up with the play.

Sure – you don’t want people to fixate on their balances and react to daily market fluctuations. KiwiSaver is a long-term savings scheme, so you need to think long-term fund performance.

But I fear young people and tech-savvy older people, could be missing out on the good returns offered by non-bank providers not doing enough to connect with them.

Kensington and Boyle maintain it’s only a matter of time before they improve their online/mobile presence, as they are well aware of targeting the “click generation”.

Kensington explains it’s been easier for banks to harness technology.

“When you’ve already got a platform like a bank does – where you can go online and see your bank balance, your credit card balance and all those things together – it’s a relatively small add-on to make.”

Boyle admits having a secure app does take initial investment, and while some non-bank KiwiSaver providers have jumped on this quickly, he maintains others are holding back from making balances readily available on mobile apps in the fear market fluctuations could cause members to make knee-jerk reactions.

“As an industry, KiwiSaver is still quite young… There’s been a lot of change and I think a lot of providers have been caught up with the legislative changes around the Financial Markets Conduct Act.”

Kensington concludes, there are different styles of reporting that attract different people.

While it’s a positive sign that my mate who’s changed KiwiSaver providers will now be paying more attention to her fund via her mobile phone, I hope the digital divide between banks and non-banks closes so that people aren’t sucked into opting for convenience at the expense of performance.

20 Comments

It's said that people will start to pay attention to their Kiwisaver, once the balance is about the price of a car. There will be increasing numbers of those people now, but is that statement true.

Funnily enough the statement is true as the balance is more meaningful once it is around 20K plus. The downside to greater visibility on the balance is the temptation to watch returns and every little blip up and down could drive the wrong behaviours (i.e. switching fot the sake of switching) to try and drive greater returns. We all know what happens when we chase returns.

There's a lot of people in the US that do that but they have the ability to buy and sell. Lots of people follow the buy high sell low cycle and destroy a lot of their retirement savings.

Thanks Craig. But you can't have it both ways. More visibility will lead to silly behaviour from some, but most I think will start to think seriously about which provider they are with that suits best their long term need.

The bigger problem is the bad behaviour with banks. Not just the bad selling. It would be naive to think that a bank with all those internal transfers and incentives will choose your interests over it's own. I think I'm better off with an independent. Sure they have their own interests, but far fewer 'internal' places to put your money.

Having spent 10 years being institutionalised within a large Aussie owned bank and looking after client money for high net worth individuals I couldn't agree more re remuneration and conflicts of interest. Saw it every day and as long as the Private Bankers were hitting their targets life was good and not too many questions were asked.

There is an old saying that goes along the lines of...tell me how I'm going to be remunerated and I'll tell you how I will perform - still applies today unfortunately.

Which is why I don't bother and stick to ETFs and suck up the pain when it inevitably occurs.

Those that have employer matching are getting up to some pretty decent balances already. One of my friends on good pay and a good employer match said that they are doing pretty well. We do need to get some education going that they shouldn't just spend it on a car and that they need to be able to live off it or draw 4% per year for living costs.

I saw research out the other day (I think from Morningstar but I could be wrong) which suggests the old 4% rule which was originally done based on US retirement savings is no longer an appropriate measure for NZ or Australia as the portfolio of 50% shares and 50% bonds (which the study was originally done on) won't generate sufficient long term earnings to sustain that level of drawings and keep a majority of the capital intact.

I saw something similar, I think a few months back. If not 4% then some other suitable figure for the current environment. Although if a kiwi only did a 4% annual draw down on their kiwisaver it would still be lower than what most would do.

There's also the separate issue of low interest rates destroying retirement but let's hope that gets fixed before too many retirements are destroyed.

Also I noticed you said keep the capital intact, the 4% drawdown is for use of capital and interest so that the capital is depleted by the time you die.

I'd like to hear more about the 4% idea. Seems to me that if you have a capital sum and take from it at 4% then it's going to last you 25 years. (assuming you are not want to preserve capital) (and -assuming you will get no income off the capital. But actually you will get some.)

Some people say your cashflow need goes down after 80. My dad was leading a very quiet life after 90 and was saving money. On the other hand I know people in their 80s regularly off to the house in France and spending well.

Seems to me the National Super will be quite adequate after 90. Which is 25 years after 65. Assuming you own where you live.

Then there is the idea you have of how long you will live. I'm working on the 100 years idea. Ha. I once knew a guy mid 50s who was going to buy his last car. His self concept was that he would be gone well before 70.

KH - here is a link to one piece on it which links back to a T Rowe Price study done over 30-year period in the US. http://individual.troweprice.com/retail/pages/retail/applications/inves…

Here is another link to paper by Auckland Uni which address dis-saving in NZ backdrop http://bit.ly/1NXQjOP

Craig's first link should give you a good idea of the concept.

For my age I'm supposed to provide for 27-30 years of retirement. It's a long time so not being afraid to dip into some capital is good, rather than thinking that surviving on interest only is the only way to retire.

If you search for "retirement calculator" on www.wolframalpha.com and select the withdrawal percentage version you can simulate retirement savings and spending.

17 years ago my rates bill was <$600, it is now $2400, suggesting another 4 fold increase for when I retire. That will be $10k, before tax that is $15k. Before I eat, heat the house or do anything else that more than eats one small pension I have. Even if it ever pays out and frankly I dont think it will given what is coming. So I am resigned to either never retiring, or moving to somewhere way smaller.

It's a frustrating situation. I'm finding myself having to invest a lot to have the retirement that I want. I may still run a business into my retirement. I still have another 24 years before the current retirement age so there's still time. There's going to be a giant retirement age population by the time I get there, New Zealand's economy will function rather differently.

Looks like the definition of financial literacy is having the belief that high risk managed funds will give you a better return in the long run;is anyone who believes otherwise illiterate??

They will definitely give the fund managers a better return.

I wonder what would happen in the short and long term if everybody piled into growth funds.

BAU grow for ever on a finite planet with un-limited oil to burn and no climate change effects scenario, um no.

Would a bank's kiwsaver fund be impacted by an OBR event? by this I mean directly not say via the fund just happening to own those bank's shares.

Only to the extent any of the KiwiSaver funds are held in cash instruments. A lot of the more conservative funds hold a portion of the KiwiSaver funds in their own cash PIE product.

KiwiSaver funds held in other assets aren't subject to OBR.

inflation is going to deal to kiwisavers...invest not save into something that adjusts with the threat of inflation. Have you noticed the Bruce Allpress ad thats out consciously telling people that its not going to be enough, when the government finally allow you to have your money, in incremental payments when your 95...no thanks houses, gold, silver, mining shares, agriculture is where its going to be...savings will be obliterated...

Older workers do not deprive young workers after all

http://www.nytimes.com/2016/05/14/your-money/disproving-beliefs-about-t…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.