The Financial Markets Authority (FMA) has published data that reveals just how well different KiwiSaver funds are performing relative to the fees their managers are charging.

The FMA has taken the data KiwiSaver providers release through their quarterly fund updates and via the Companies Office’s Disclosure Register, and presented it in an interactive tool that will be updated every three months.

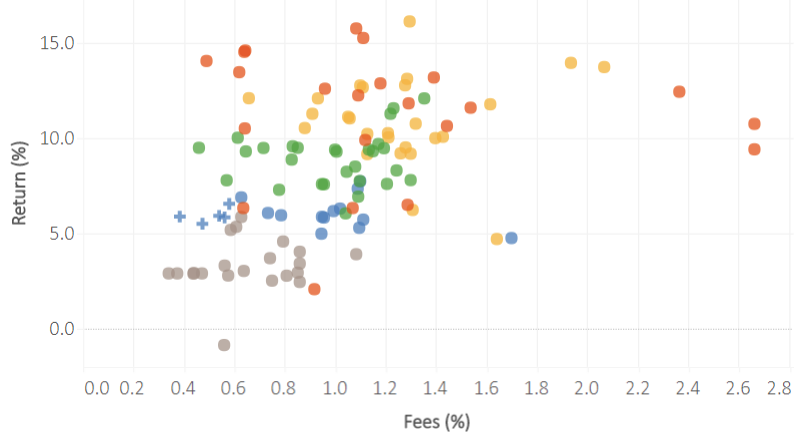

The ‘KiwiSaver Tracker’ makes it quite clear which fund managers are charging high fees, but aren’t delivering high returns, and vice versa.

The FMA’s director of external communications and investor capability, Paul Gregory, says: “Over five years, there certainly seems to be a link between higher risk investments and higher returns. However, the link between higher fees and higher returns is, apart from in the case of a couple of standout funds, far less obvious.”

This KiwiSaver graph, comparing average fees and returns after fees over the last five years, illustrates Gregory’s observation. (An interactive version of the graph can be accessed by clicking on the link above).

The top performing funds are growth or aggressive and have risk ratings of four out of seven - seven being the most risky. With the exception of two high risk SuperLife funds, all the funds with the lowest returns have risk ratings of one or two.

There’s less of a correlation when looking at fees versus performance. The fees charged by the top eight performing funds range from 0.5% to 2.1%.

In fact, with fees of 0.5%, the fifth highest performing fund (SmartKiwi Growth), is among the handful at the lowest end of the fees spectrum.

The two funds (Lifestages Growth Portfolio and NZ Funds Growth Strategy) with by far the highest fees, at 2.7%, have fairly similar returns to the other funds in their fund type category.

The two funds that stand out for having relatively high fees but poor performance are NZ Funds’ Inflation Strategy fund and Lifestages’ Capital Stable Portfolio fund.

Both the Lifestages funds mentioned here were closed in April last year, as its manager, Funds Administration New Zealand (a subsidiary of SBS), has launched a new range of products with lower fees.

Best and worst performers

Here is a list of funds that have had the highest and lowest returns (after fees) on average over the last five years.

The grey shaded boxes highlight the funds that have produced the lowest returns in their fund type categories, but have charged fees either equivalent to, or higher than, the funds that have produced the highest returns in their categories.

| Fund | Return after fees (%) | Fees (%) | Fess as a % of returns |

| Default winners | |||

| Superlife Overseas Non-Government Bonds | 5.9 | 0.6 | 9.7 |

| Superlife Overseas Bonds | 5.3 | 0.6 | 10.2 |

| Default losers | |||

| SuperLife UK Cash | -0.9 | 0.6 | - |

| Aon ANZ Cash | 2.4 | 0.9 | 26.1 |

| Conservative winners | |||

| Aon Russell LifePoints Target Date 2015 | 7.7 | 1.1 | 12.4 |

| Aon Russell LifePoint Conservative | 7.4 | 1.1 | 12.9 |

| Conservative losers | |||

| Lifestages Capital Stable Portfolio | 4.8 | 1.7 | 26.4 |

| AMP Conservative | 5.0 | 0.9 | 16.0 |

| Balanced winners | |||

| Milford Balanced | 12.1 | 1.4 | 10.1 |

| Aon Russell LifePoints Target Date 2035 | 11.6 | 1.2 | 9.6 |

| Balanced losers | |||

| AMP Moderate | 6.1 | 1.0 | 14.7 |

| AMP Moderate Balanced | 6.9 | 1.1 | 13.6 |

| Growth winners | |||

| QuayStreet New Zealand Equity | 16.2 | 1.3 | 7.4 |

| Milford Active Growth | 14.0 | 1.9 | 12.2 |

| Growth losers | |||

| NZ Funds Inflation Strategy | 4.7 | 1.6 | 25.9 |

| QuayStreet Australian Equity | 6.2 | 1.3 | 17.4 |

| Aggressive winners | |||

| OneAnswer Australasian Shares | 15.8 | 1.1 | 6.4 |

| OneAnswer International Shares | 15.3 | 1.1 | 6.8 |

| Aggressive losers | |||

| Superlife GEMINO | 2.1 | 0.9 | 30.8 |

| Superlife Emerging Markets | 6.3 | 1.1 | 14.5 |

Note there are a number of new funds, like those of Simplicity, which haven’t been around for five years, so haven’t been included in this comparison. The KiwiSaver Tracker allows you to compare funds based on returns over a year, but interest.co.nz hasn’t focused on this, as performance can fluctuate dramatically over a year.

What about the banks?

While the major banks have usurped the bulk of KiwiSaver investors, their funds haven’t stood out for being particularly strong or weak performers.

Banks’ funds generally sit in the middle of the pack in terms of net returns across the various fund types. Their fees are also at the lower end of the spectrum.

In contrast, smaller providers such as Aon, Funds Administration New Zealand, Booster, Quay Street and NZ Funds, have higher fees as a proportion of returns.

ANZ’s general manager of wealth products and marketing, Ana-Marie Lockyer, says ANZ has already cut its fees across its funds by about 20% since 2009.

She says ANZ is “starting to deliver some economies of scale to members”, but it is not yet at a point where it can reduce fees. She says this would see a reduction in much-needed investment aimed at educating investors and making advice accessible.

Are actively managed fund managers getting a raw deal in this debate?

What the FMA’s KiwiSaver Tracker does not tell you, is how actively managed various funds are. Investors generally expect to pay higher fees for more actively managed funds, and vice versa.

While passively managed funds typically do well when the market does well (as it has in recent years), more actively managed funds are in theory supposed to soften the blows during downturns.

It is on this basis that Booster’s chief investment officer, David Beattie, points out that given KiwiSaver launched towards the end of the Global Financial Crisis, we haven’t yet seen how funds perform in a downturn where active management is supposed to show its value.

Once this happens, and KiwiSaver goes through a full market cycle, he believes we will be able to have a more realistic discussion about fees versus net returns.

“I think there is going to be some significant differences that will emerge out of that process. And we sort of have to go through that cycle to get to that point,” he says.

Are fund managers already ‘lean and mean’?

Nonetheless, asked how much room there is for Booster to drop its fees, Beattie says: “The industry is obviously growing, and growth brings capacity to be able to reduce fees over time. But we’re already running fairly lean and mean.”

In fact, Funds Administration New Zealand’s executive director, Graham Dunston, who is responsible for the Lifestages funds, believes the amount of funds providers need to have under management to have a sustainable business has increased from around $100 million to at least $500 million over the last 15 years.

He puts this largely down to an enhanced regulatory regime with necessary, but more cumbersome, compliance requirements.

“Even if you’re pursuing an outsource model [of certain services related to funds management], you still need to have an operating infrastructure that can actually manage and monitor those relationships,” he says.

As for technology - “potentially it’s an aid, but you can’t default to it. You still need someone with a hand on the tiller, making sure things are being done the way they should be.”

Are fund managers prioritising advice over fees?

Dunston says the environment “absolutely” makes it difficult for new entrants to enter the market.

However for the smaller operators, facing tough competition from banks, he believes the future lies in targeting a segment of what will become a more fragmented market.

In other words, providing niche product offerings with different asset allocations, more granular information, and advice to larger net worth individuals, while leaving the banks to the mass market.

This has happened in Australia, so he can’t see why it wouldn’t happen here.

Beattie says Booster is already placing great emphasis on advice.

“We make no apology for the fact that we’re slightly above average in terms of our fees relative to the market. Because we’ve always embedded an element of access to financial advice in our fund offerings,” he says.

“Of the fee that we collect, we typically pay advisers up to 0.5% on an ongoing basis, in order for that member or KiwiSaver client to have access to an adviser. When you multiply, 0.5% times an average KiwiSaver balance of let’s say $20,000, that’s $100 a year that someone’s effectively paying to have access to someone to talk to.”

30 Comments

This is the best analysis of kiwisaver performane I have seen. Makes it easy to see net returns before tax. Thanks very much FMA and Interest. I'll be changing my provider based on it

Great example of a proactive regulator, in consumers' interests. Not just reacting to defalcations after the event, and shrouding regulatory data. When the market failed to do so, proactively using regulatory data to introduce transparency helps remove the opacity that favoured poor performers, enabling consumer choice and promoting genuine competition; benefiting consumers and good funds managers.

I hope more people start focusing on their kiwisaver returns. It's a big deal for those that are younger and can benefit more from compounding.

There are still problems with too many people being on seemingly permanent contributions holidays (I know some people in this situation and it's about cash flow/making ends meet). Then there are others that are making a choice to buy a house and it's really a decision between having a house or a retirement when they shouldn't be mutually exclusive.

Contribution holidays are more often just dumb dictator. Immediate benefit at the cost of giving away free money. But what can you expect when overall New Zealand does not have an investment culture.

Given that a lot of property "investors" aren't interested in their return on investment there's a long road to educate the population.

There are people taking contribution holidays due to having kids, loss of their job, or finding their minimum payments for consumer debt are increasing each month. Those credit card minimum payments are more important than being able to retire.

I've just started a contributions holiday after purchasing my first home, because I'd rather put that extra money onto the mortgage. If i continue with that additional payment throughout the lifetime of the mortgage It'll shave at least 9 years off the mortgage if all variables remain the same.

You should still make the minimum required payments to get the free govt money, its one off the few times a working person can get free money from the govt.

There is a hard and unpalatable fact of life Nzdan. You should not be choosing between paying off your mortgage and paying into Kiwisaver. You need to be doing both, not either or. And yes, it is hard.

At very least people should be putting in $87/month which means that they will receive the full member tax credit which is a 50% gain on their money. A 50% return + investment returns exceed any floating rate or fixed mortgage out there.

However I do know plenty of people that have a cash flow squeeze that's so tight that they don't have a choice. Or as people say on another forum it's expensive to be poor.

Hopefully after a year of paying down a floating rate or putting money against a fixed rate they will resume kiwisaver contributions. The potential loss in compounding gains is a lot more than the money saved in mortgage interest. People having to choose between a house and a retirement shows how broken and useless New Zealand is.

There's also the employers match for those eligible to receive it. Absolute no-brainer for me to put in 3% to collect the full employers contribution and the tax credit. My savings over 3% go elsewhere.

There's a bit of false news. ---- She says ANZ is “starting to deliver some economies of scale to members”, but it is not yet at a point where it can reduce fees.

Perhaps she could have told the truth. "ANZ is starting to deliver some economies of scale to ANZ"

ANZ is suing the FMA according to NBR

Interesting graphics. The first four categories are nicely layered and about what you'd expect. But the aggressive funds are all over the place, and this after five years of bull. Looking at a previous KiwiSaver article we are due to head back to the start of the cycle and some if not all the aggressive funds are going to look very sick for a few years after.

Several of the aggressive funds are single-market share funds e.g. 100% NZ shares or 100% AU shares. Many of these are normally bundled together to make a portfolio. Once this diversification is added, the overall returns are in line with the expected risk/reward band.

Exactly kiwimm, and that is why it is not as black and white as this chart deviously tries to make it. People invest in these types of funds usually for specific reasons, and not necessarily via kiwisaver - they are just a different type of fund in a suite of options, and they also happen to be available for investment via your kiwisaver account.

To then try to compare that against a standard diversified fund is to misunderstand its purpose entirely.

You're probably right red cows. May not be a good idea to switch to an agressive fund now as you may be buying in at the top of the market (like Auckland real estate).

If already in one though, and you're able to handle short term risks (you're not 64 and just about to cash out); I personally think its okay to hang in there - accept over the long term a little risk can produce better long term returns.

Still not sure this is telling me about fees. It is telling me fees as a percentage of returns so if the return is good the fee will seem reasonable and vice versa. Shouldn't I be asking what the fee is per dollar or thousand dollars invested and then forming a separate view on performance??

Its hard to put a figure on that, as some funds have fee structures that depends on returns. eg Milford active growth fees are

$36/year admin fee,

+1.05%pa of the gross amount in the fund as a capped management fee.

+15% of returns exceeding 10% after the capped management fee has been deducted.

No - it's the bottom line that's important.

The first fees column is the fee on your balance, taken regardless of performance. Most of these fund managers seem averse to the idea of risk sharing, thinking they should get their cut regardless of performance.

Simple law change. No fees on capital - it should only be on returns.

The importance of this will become apparent when their is a downturn.

I have an Aussie fund I keep as an experiment. It has taken 9 years to recover from the GFC (i.e. to return to the same value I had in 2007). Year 1 lost over a third due to the market, but then continued to be negative for 5 consecutive years solely due to fees. It's only the last 3 where it has improved (again more due to the market than the management)

You don't think there might be an issue when providers go broke left right and centre when there's a global downturn? No fund can isolate itself from the world. Best case, overall fees increase to compensate for their new lumpier nature.

Agree there is a problem with high fees, but that is better dealt with by migrating to lower fee platforms (I'm with Simplicity for that reason).

If providers go broke, that is fine by me. At least some of the risk would then be on them for a change. As it stands, they can lose all my money and still walk away with a hefty profit looking for the next sucker.

There is nothing stopping them

- charging a higher fee on the return. or,

- a flat fee across the year.

I just don't see it as right that they charge a percentage on Capital.

I disagree. Any fund losing 100% (or even doing significantly worse than its peers) will be impacted in terms of people switching away and fewer new sign ups. If funds are strongly incentivised to increase returns, the most obvious way to do this is by exposing their clients to higher risk. If it were possible to increase returns without higher risk, they would all already be doing so. I come from the point of view that fund managers are not Gods, cannot repeatably outperform the market, and encouraging them to try to do so is dangerous. Hence my money being in a passive (but aggressive) fund.

furthermore, a flat fee for all customers collecting the same total amount would mean a significant fee reduction for clients with large balances, and a significant increase for clients with small balances, i.e. those just starting to save for their retirements. Taking several hundred dollars from a customer who only has a couple of grand in their account would be a very significant drag to their retirement savings, acting as a strong disincentive to sign up for a Kiwisaver. I'm not sure if that would lead to a better world.

"I disagree. Any fund losing 100% (or even doing significantly worse than its peers) will be impacted in terms of people switching away and fewer new sign ups."

THe problem with that argument is

a) "Past returns do not equate to future returns", and

b) they are all doing it so makes no difference.

I agree fund manager's aren't gods, so why do we pay them as though they are?

I agree, similar funds are highly correlated and there's no way to predict which will do well. Many fees are too high. This all points to one conclusion - sign up with a cheap passive provider like Simplicity and step outside of the game.

Nice overview, the chart has a good amount of detail to drill into, (easy enough for family and laymen), the other site ref I recommend for family wanting a quick comparison currently is sorted but I will be sure to recommend this data to them as well. Often some fund managers have failed basic management backend processes which leaves the funds under by hundreds per year (quite a large amount to loose in bad tech). Perhaps I should call that a buggery fee, it sure is noticeable enough to provoke a change in providers just to be able to avoid spending hours on the phone getting the amount fixed in the accounts. Ah the continuing trials of Kiwisaver investments... easy to see why many take holidays to have more control and better returns on other investment strategies.

Good article.

Some might remember Convertible Life insurance. It was commonly sold years back. The promise was at age 60 (44 yrs on from policy purchase 4 me) one received $25,000. Great as my wage was 12 per week then, but 25k, 44 odd years on buys little. 44 yrs back it brought 3 houses a few new cars and so on. The rules changed as I recall and provider demutualised., lucky escape.

Younger people in Kiwisaver must realise the large lump of cash at 65 may not be the nest egg it purports to be as time passes. As in the Convertible insurance, the sum offered would buy little today.

Kiwi saver is similar, apart from the tax rebate. Previously 1040 earned a 1000 tax rebate / contribution from Government, that later reduced by 50%. The scheme is a no brainer if managed around the rebate program. Pretty much the providers can do what they like and the scheme works.

After that or if the rebate regime ends, the Kiwisaver providers are little different to other managers of cash.

Savers can and do much better. The chap above investing in a home for example, over 40 years that investment will compound as every ten years history says, the house value will double. That is certainly a no brainer, especially if he could manage to contribute enough to receive the current rebate - while it lasts.

10 per week into selected shares is also a no brainer as history shows similar outcomes.

What else to the Kiwisaver providers actually do?

The likes of Simplicity (very low fees) are probably worth a long-term investment, especially if you're balancing emerging markets with mature markets and high-cap with low cap. At least in their case the percentages being taken out aren't going to be crippling - compared to, for example, a 2.7% per annum cut of your balance, which is just ridiculous.

Good article, but agree with some of the comments. The tool is misleading using calculation of the fee as a % of the return. It makes some of the lower performing funds look better than funds whose overall return less fees is higher. After one year in Simplicity, very happy with them. Their growth fund return has been ahead of, but just now just slightly behind my old bank fund. The lower fees (0.3% versus 1.1%) put Simplicity ahead in dollar terms. They also give 15% of the admin fees to NZ charities.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.