Despite the fact that our mortgage debt is rising at the pace of more than 6% per year, the amount of interest we are paying is static.

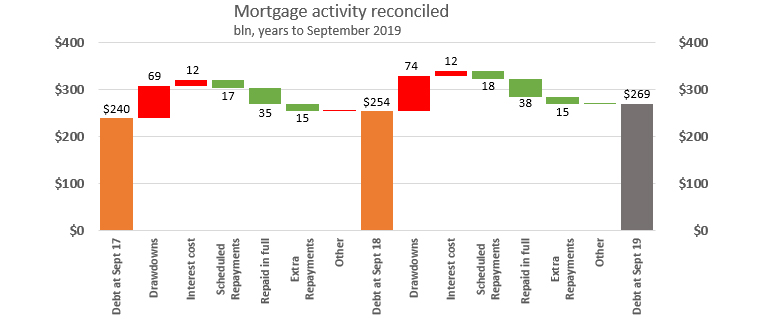

In the year to September 2019, we collectively added $15.4 billion to the bill we owe banks for housing loans, taking the overall liability to $269.4 billion

But in that same year, we paid them $11.9 billion in interest. And that compares with an unchanged $11.9 billion we paid in the previous year.

Low interest rates keep repayments low, allowing us to borrow more. I suspect the Reserve Bank thinks that low interest rates 'save' borrowers money. But borrowers aren't behaving like that.

The key driver is loan payment affordability.

And other data clearly shows that low interest rates are allowing more first home buyers into the market, even at the elevated house prices they have to pay. In fact, their buying competition is doing its part in pushing up house prices, especially in the lower quartile end of the market.

Further, Reserve Bank data collected from bank mortgage book activity also shows borrowers are still making more payments over-and-above those scheduled in their mortgage contracts.

In the year to September 2019, borrowers made $17.8 billion in principal repayments, and then added another $14.6 billion in extra principal repayments over an above the core obligations. That is a remarkable outcome, suggesting that payment stress is just not an issue.

Compare that with the year to September 2018. In that year, they also added $14.6 billion in excess payments on top of the $17.0 billion scheduled repayments. The habit of paying down quicker isn't slowing.

(This data does not include the "payment-in-full" activity that happens when an owner sells out, and these involved $37.7 billion in 2019 and $35.2 billion in the prior year.)

Knowing this data for mortgages allows us to derive what banks are doing with lending for loans other than for mortgages.

| year to June 2019 | Interest charged |

Mortgages (average) |

Other loans (average) |

Rate (average) |

| $ bln | $ bln | $ bln | % | |

| - ANZ (RBNZ Dashboard) | 6.523 | 78.536 | 51.031 | 5.03 |

| - ASB (RBNZ Dashboard) | 4.352 | 55.869 | 30.148 | 5.06 |

| - BNZ (RBNZ Dashboard) | 4.193 | 40.851 | 44.644 | 4.90 |

| - Kiwibank (RBNZ Dashboard) | 0.933 | 17.427 | 2.199 | 4.75 |

| - Westpac (RBNZ Dashboard) | 3.962 | 49.289 | 32.366 | 4.85 |

| - All others (difference) | 2.709 | 16.136 | 23.126 | 6.90 |

| Total all banks (S21 and C5) | 22.672 | 258.108 | 183.514 | 5.13 |

| Total mortgages (C35) | 11.871 | 258.108 | 4.60 | |

| All other lending (difference) | 10.801 | 183.514 | 5.89 |

"Average" bank mortgage rates of 4.6% are clearly higher than current fixed rate offers which are now well below 4%. As those new lower rates work their way through the mortgage book as fixed terms roll over, so it seems clear that the amount of interest borrowers will be paying banks is likely to hold or decline - and support rising prices that can be paid. Asset inflation, the consequence of low rates.

33 Comments

Good to see these numbers. I’ve often wondered how much impact lower interest rates actually have on credit availability/ability to borrow more given that banks stress test mortgage lending at about 6.5%ish no matter what the actual interest rate is. Seems that this particular factor may not be holding people back.

When the data came out I saw that the repayment deficiencies had reverted to where they would be expected to be. I think that for those partly defaulting on their payments the OCR cuts have probably helped.

The rate of increase of mortgages seems unaffected though. Too bad that mortgage debt is growing 12 times faster than productivity, that's asking for a correction.

e: A note on drawdown and excess repayments. Those include revolving credit. While the repayments are good the drawdowns are exceeding repayments. Some will be in a better position and others worse.

"Too bad that mortgage debt is growing 12 times faster than productivity, that's asking for a correction". Yes and then some! Even worse is that rising rents and property prices actually kills off real economic business due to sending the cost of living sky high!

Is this a surprise? I thought this was obvious to most people who have looked at housing and debt with more than just a cursory glance.

Good work

Now, DC, if the numbers of mortgages were available, and able to be set alongside this analysis, it would allow a per-mortgage average to be ascertained. Which could be Interesting. Yes, yes, there would be some double-counting: 'mortgages' aren't 'people' in the sense of business entities or households. But, still, Interesting......

Well done, David. Excellent analysis.

Some people are using lower interest rates to borrow more

Others are paying more off and borrowing at lower rates on renewal basis.

Government and banks do not want to reduce credit availability or increase in rate of growth of mortgage credit as this slices GDP growth and consumer demand. So, FHB are worshipped accordingly as older borrowers are more savvy

Government and banks do not want to reduce credit availability or increase in rate of growth of mortgage credit as this slices GDP growth and consumer demand

Yes. A continuation of an existing model that is the "crux" of the economy. What is more interesting is the extent this credit-driven approach to economic prosperity. It doesn't seem to register with the ruling elite (publically anyway) that this credit-driven approach is approaching limits (even if those limits are not clearly understood). Someone aske me a 'what if': if h'hold debt to GDP is 100% and the monetary system can accomodate, why cannot it not be 200% or even 300%? I don't really have an answer to that, however the idea of instability comes to mine. Steve Keen explains it well, despite the chagrin of the status quo cheerleaders.

Excellent summary David. It confirms that bureaucracies favour the status quo. This is actually a strength, a lot of the time, as it provides stability and continuity. Against that, it also means trends tend to overshoot badly.

https://www.dlacalle.com/en/crises-happen-when-we-believe-there-is-no-r…

If you are an investor, it is pretty pointless paying off much principal if at all, unless you are negatively geared nowadays.

Positively geared investors will be out there buying good positively geared property if they are able to get more money from their lender.

Opportunities are Always out there.

Opportunities are Always out there.

Exactly:

Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky. Link

Good analysis David and very good link Roger. It's a pleasure to read accessible economic analysis and commentary.

Asset inflation, the consequence of low rates.

More a consequence of low BIS imposed RWA bank capital requirements for residential real estate lending, which contributes little to GDP.

There were two major evolutions in money and banking that seem to fall outside the orthodox narrative. The first was a shift of reserves and bank limitations from the liability side to the asset side. The second was the rise of interbank markets, ledger money, as a source of funding rather than required reserve balancing: replacing the old deposit/loan multiplier model. Courtesy of J. Snider from Alhambra

The empirical tests rejected the financial intermediation and fractional reserve theories (Werner, 2014a, 2015) and showed that banks do not need prior savings, nor central bank reserves or other deposits to lend. Instead, banks create new money when they do what is called ‘bank lending’, and add it to the money supply (see Figure 1). Bank loans thus do not transfer existing purchasing power, but add net new purchasing power. The banks’ lending creates 97% of the money supply. Bankers’ decisions about how much money is lent – and thus created and added to the money supply – and given to whom for what purpose quickly reshapes the economic landscape and affects us all. Sadly, no regulator has asked banks to ensure they lend for productive and environmentally projects – over two thirds of UK lending is not for productive purposes that creates jobs or boosts GDP, but instead for assets, causing asset price inflation. (same in NZ) [my bold] Link

Two thirds of NZ households are mortgage free, thus the remaining third with mortgages, corner 60 %+ of bank lending.

The consequences are graphically clear for all to see here and here.

Interest rates spiral down, in concert with extended periods of poor GDP growth, and central banks follow them down.

{kind=link}

{kind=link}

Great article David.

Agreed, rather than blaming the buyers splurging, the reality is that lower interest rates create increased demand in the market:

More/cheaper money -> increase in number of buyers -> increased demand for houses -> increased competition -> increased prices.

Sadly, the result is that the FHB just has to pay more to be competitive in price when trying to secure a property.

Another "sad result" is that you distort the economy, particularly for the younger generations. In effect, younger people are lumped with the largesse of retail banks and central bank hegemony.

No quite, we still see the volume being sold very low.

We are in the unusual position where our OCR is very low and set to go lower but employment is good, trade balances are good and the economy is still performing ok and providing close to target inflation.

So with these OCR proactive cuts to get "ahead of the game" , what happens when those other things catch up ??? yes you know!!!

Good analysis. I think that there is another aspect too. That of the savers. If you are a saver and interest rates drop, then you are less inclined to spend. So as I have been saying for years now; while the model that ties high inflation to raising interest rates makes sense, the converse does not. It is totally counterproductive and the only sort of investment that it encourages is in non productive assets like property. We have been labouring under this flawed model since the 2008 crash and really have not made any meaningful progress in addressing the problems. So now that we are facing even more problems we are "turning up" the knob further.

"The beatings will increase until the morale improves" Or as Einstein said - the definition of insanity is to keep doing the same thing and expect a different result.

As I have droned on about before, there is also a another very destructive flaw with this model. That is, it totally prevents society from benefiting from increased productivity as follows

As productivity increases, relative prices of the effected products fall. This is not allowed by the inflation/interest rate model, so interest rates are dropped. This means money is channelled into fixed asset speculation so these assets rise in price. e.g. housing. There is also a rise in the price for goods that are not subject to strong competition and the forces that drive productivity (in NZ case building materials, food, petrol, power) The net effect is that the price falls due to rises in productivity are more than offset by the price rises from fixed asset speculation and price rises in low competition, low productivity sectors of our economy; so that inflation can remain positive. By this mechanism there has been a huge transfer of wealth from working people to some industrialists and the capital owning classes.

It is totally counterproductive and the only sort of investment that it encourages is in non productive assets like property

I disagree. Performance of equities has been superb. Even the NZX50 ETF, drip feeding say $2000-3000 per month since the GFC would have resulted in substantial capital gains.

Capital speculation. Fits the argument perfectly.

Everything bubble

Following the upside of US indices underwritten by stock buybacks, funded by cheap debt, caused by a failure to invest in productive capacity.

Outcome then Chris M is that New Zealanders are worse off. Not a problem in the view of the last few governments.

Good to see the practical data confirming theory, ie if you increase demand (by supplying more money via cheaper rates) without increasing supply (of what they are spending the money on ie housing), then any savings gained through having a low rate are capitalised into the price of the property.

The real kicker is that this increase in price is non value added and only exists because of the in balance, which can quickly be reversed if interest rates increase and/or supply of housing increases to meet/exceed demand.

The price can go backwards in real or nominal terms but your debt is locked in.

Indeed. Leverage can work in reverse. I'm sure no one thinks about it after the last two governments in NZ but it is in the text books.

David, is there any way to look at; of the 69 billion last year and 74 billion this year, what portion of this is for new housing stock vs existing housing stock. If their are a lot more new houses coming onto the market then this low interest doesn't necessarily translate into inflated house prices for existing stock.

Also if a customer moves from one bank to another does this result in + drawdown and - repaid in full, therefore net change is $0 unless a little bit extra drawdown for rennovations?

I think it is quite hard to state "clear evidence that low interest rates aren't used to save borrowers money, they are used to bid up prices and debt levels" without addressing these two possibilities of paying for new housing stock and rennovations.

Completely agree.

While the data shows that statement could be correct its by no means clear evidence

The problem might be addressed by cutting back significantly on immigration.

This will force wages up to a point where the reserve bank can then restore some stability by raising interest.

This would then start reversing the low wage low productivity hole that our economy is in and force our businesses to raise productivity if they want to survive. If they do not want to rise to the challenge, then they will fade away and the more highly valued workers will move to enterprises that can raise productivity and pay higher wages.

Less people coming in would also significantly ease the pressure that we face in housing and infrastructure.

Good analysis. Shows that DTI ratio limits are the only answer.

If the borrowers think that they would not be making any profit by using the borrowed money, after paying the interest, why would they borrow and lose whatever they have to invest themselves and face insolvency ?

The business optimism drives investment and borrowing not low interest rates. If any one does not understand that, then they have no business being an expert and running the show of the nation.

"The business optimism drives investment and borrowing not low interest rates."

Exactly; and I would add creative thinking and sound judgement.

As I have said before, any board of directors who's investment judgment is swayed by these low interest rates should be cast out along with any business proposal that is so flimsy that it relies on these low interest rates.

Interesting analysis. What I learned was that mortgages dominate bank lending far above all other products combined but the other products actually command a higher interest rate. That's fairly interesting when you think that business lending, margin lending, personal lending etc. are actually such a small part of banking. Mostly...it's just mortgages.

DC's last sentence; "Asset inflation,the consequence of low rates". Indeed,while inflation as conventionally measured remains low, it has inevitably led to asset inflation. Minsky warned of this a long time ago. To quote from Felix Martin's excellent book, Money, The Unauthorised Biography,"The more successful a central bank is in mitigating one type of risk by achieving low and stable inflation,the more confident investors will become and the more they will willingly assume other types of risk by investing in uncertain and illiquid securities". "Monetary stability will actually breed financial instability".

Surely nobody can regard the Auckland property market as normal? $2m for a nice but unexceptional villa is patently absurd. The level of our stockmarket has concerned me for some time and I have been gradually taking some money off the table. Despite the low return on cash,i am comfortable with the liquidity this gives me.

You can see evidence of an increasing amount of Minsky's definition of ponzi financing in low yielding residential real estate in NZ. Look at the large number of residential real estate properties that are negatively geared and have tax losses. That number increases when these borrowers also have to pay principal on P&I mortgages. If a sufficient number of these owners come under cashflow stress and under pressure to sell, then there could be a large imbalance between supply and demand in the property market.

From John Mauldin:

"Minsky moment" - the point at which excess debt sparks a financial crisis.

The late Hyman Minsky said that such moments arise naturally when a long period of stability and complacency eventually leads to the buildup of excess debt and overleveraging.

At some point the branch breaks, and gravity takes over. It can happen quickly, too.

Three types of debt

Hyman Minsky spent most of his academic career studying financial crises. He wanted to know what caused them and what triggered them.

His research all led up to his Financial Instability Hypothesis. He thought crises had a lot to do with debt. Minsky wasn't against all debt, though. He separated it into three categories.

1) The safest kind of debt Minsky called "hedge financing." For example, a business borrows to increase production capacity and uses a reasonable part of its current cash flow to repay the interest and principal. The debt is not risk-free, but failures generally have only limited consequences.

2) Minsky's second and riskier category is "speculative financing." The difference between speculative and hedge debt is that the holder of speculative debt uses current cash flow to pay interest but assumes it will be able to roll over the principal and repay it later. Sometimes that works out. Borrowers can play the game for years and finally repay speculative debt. But it's one of those arrangements that tends to work well until it doesn't.

3) It's the third kind of debt that Minsky said was most dangerous: Ponzi financing is where borrowers lack the cash flow to cover either interest or principal. Their plan, if you can call it that, is to flip the underlying asset at a higher price, repay the debt, and book a profit.

How Ponzi Financing Triggers a Full-Blown Crisis

Ponzi financing can work. Sometimes people have good timing (or just good luck) and buy a leveraged asset before it tops out.

During the housing bull market of 2003–07, people with almost no credit were flipping houses and making money. It attracted more and more people, which created a soaring market. The phenomenon fed on itself.

Bull markets in houses, stocks, or anything else can go higher and persist longer than we skeptics think is possible. That is what makes them so dangerous.

Minsky’s unique contribution here is the sequencing of events. Protracted stable periods where hedge financing works encourage both borrowers and lenders to take more risk.

Eventually, once-prudent practices give way to Ponzi schemes. At some point, asset values stop going up. They don’t have to fall, mind you, just stop rising. That’s when crisis hits.

https://www.mauldineconomics.com/editorial/the-market-is-headed-for-a-m…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.