Well it was all looking so good. For the next three months, not quite so much.

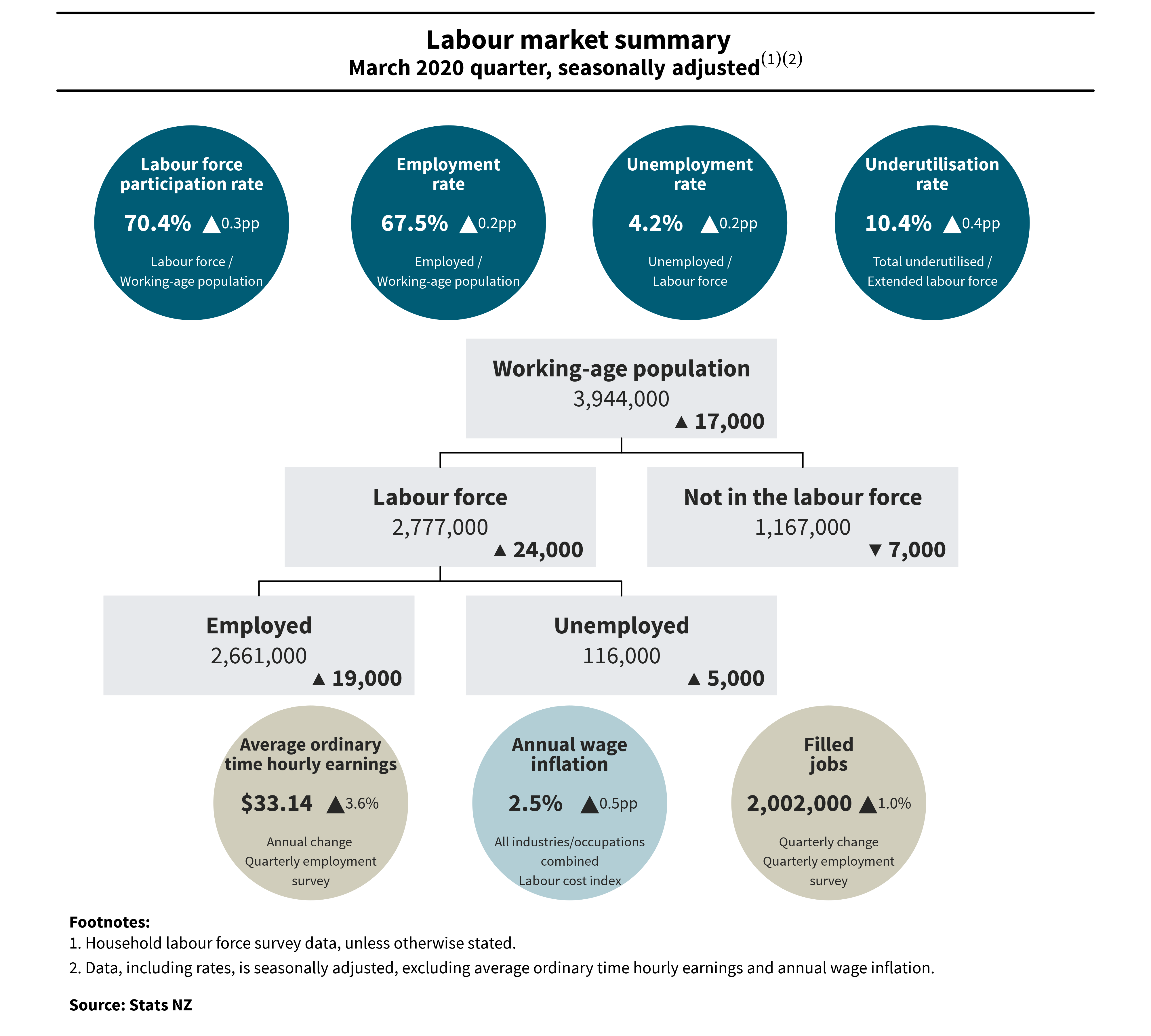

Statistics New Zealand says the seasonally adjusted unemployment rate rose to 4.2% in the March 2020 quarter, up from 4% last quarter.

In the March 2020 quarter, the number of people who were employed rose by 19,000 (0.7%) to reach 2,661,000.

The participation rate rose 0.3% to 70.4%.

The labour cost index (LCI) all salary and wage rates (including overtime) increased 2.5% in the year to the March 2020 quarter. This increase continued to reflect the impact of collective agreements signed by nurses, police, teachers, and principals in 2019.

Annually, public sector wages increased 3.2% and private sector wages increased 2.4%.

But that was then.

Capital Economics Australia and New Zealand economist Ben Udy said looking forward it’s clear that the labour market will deteriorate markedly in the second quarter.

"Admittedly, the government’s wage subsidy scheme will protect some jobs, but requirements such as the need to have suffered a 70% revenue loss or the requirement that business still pay staff at least 80% of their normal wage may mean some businesses will fall through the cracks. Business surveys and online job ads are both consistent with a more than 8% fall in employment.

"We ultimately expect the unemployment rate to rise to 15% in Q2. What’s more we expect that spare capacity in the labour market will result in annual wage growth easing further to below 1% in 2021. The considerable deterioration in the labour market is one reason we expect the RBNZ to cut rates into negative territory this year."

Back on the March quarter figures. Stats NZ's labour market and household statistics senior manager Sean Broughton said: "Our surveys captured a robust labour market in the period before New Zealand went into COVID-19 lockdown. The unemployment rate has remained stable at around 4 percent since late 2018, after trending down since late 2012.

“The impact of COVID-19 on the labour market, including unemployment, hours actually worked, and underemployment, should be clearer in the June 2020 quarter,” Broughton said.

“There was a sharp rise in the number of people receiving Jobseeker benefit support at the end of March and start of April, though this is not the same as the official measure of unemployment.”

The lowest unemployment rate since the global financial crisis of 2007–08 was 4.0%, recorded most recently in the December 2019 quarter. After the global financial crisis, unemployment reached a high of 6.7% in the September 2012 quarter. This was considerably lower than the series peak of 11.2% in the September quarter of 1991, which followed significant structural changes to the New Zealand economy. This unemployment series started in 1986.

In the March 2020 quarter, the collection of labour market statistics was impacted by measures taken to slow the spread of COVID-19, at the same time as the ability to work was affected by the lockdown.

“The household labour force survey takes place over 13 weeks each quarter, which means it measures unemployment over the whole quarter rather than a single point in time at the end of the quarter,” Broughton said.

“We are confident these statistics are reliable, though fewer interviews took place in the final weeks of the quarter, following Stats NZ’s decision to suspend face-to-face interviewing, and later, the redeployment of contact centre staff to urgent work answering public calls about the Government’s COVID-19 website.”

Finance Minister Grant Robertson put out this statement about the figures:

News that nearly 20,000 New Zealanders entered work in the first three months of the year shows the economy’s underlying strength heading into COVID-19, Finance Minister Grant Robertson says.

Stats NZ reported today that the number of employed people rose by 19,000 over the March quarter, while the number of unemployed was up by only 5,000. The employment rate rose to 67.5%, while the unemployment rate also rose slightly from 4% to 4.2%, remaining near its lowest levels in a decade.

Wages were also rising at an annual rate of 3.6%, with average ordinary time hourly earnings up to $33.14. This was well above inflation at 2.5%.

“The numbers show that this Government’s economic plan has been working, as businesses had the confidence to increase employment and invest in their workforces by raising wages,” Grant Robertson said.

“Obviously much has changed in the last six weeks in New Zealand. While these numbers reflect the position New Zealand was in before the worst of COVID-19, they show we were in a strong position. The amazing work all New Zealanders have done through Level 4 and Level 3 to stay home and break the chain of transmission now means we’re well-placed to get a head start on our economic recovery.”

The Government’s focus is on cushioning the blow of COVID-19 on the economy by supporting businesses with cashflow and helping workers maintain or find employment.

“We do know that this global 1-in-100 year health and economic crisis will contribute to unemployment rising further. The investments we’ve already put in place are designed to minimise these impacts, and support those who are out of work to find new employment.

“We went hard and early in our economic response, putting in place the wage subsidy scheme to protect jobs and incomes. The scheme has paid out more than $10.6 billion, covering the wages of more than 1.7 million workers.

“Our $3 billion tax refund scheme put into law last week will start paying out in coming days to support viable businesses with cashflow and costs like rent. This is being complemented by the Small Business Cashflow Loan scheme, the Business Finance Guarantee and a range of tax measures to encourage investment.”

28 Comments

Let's fisk GR's statement that "businesses had the confidence to increase employment and invest in their workforces by raising wages":

- Raising wages has been done at least in part by central fiat via Minimum Wage increases. That has aught to do with business viability or confidence.

- 'Businesses' is a generalisation: if most of the 20K increase in those 3 months was in Hospo, for example, then more than half of Those are currently Goneburger.

- 'Investing' assumes that the jobs in question need more than a few days working alongside others and imitating them. I'd doubt that 1 in 20 jobs actually requires an 'investment' in terms of study, attendance at a training course offsite, or acquisition of a credential of some sort.

Pure pre-election puffery.

GR is being way too optimistic

Sadly job losses are gathering pace daily, as employers start to realise this will not be a short term issue.

If I could only suggest one thing, buy locally made and owned products and services. This should extend to banking and insurance services, as it will keep profit local. NZ can not afford to keep exporting $20 billion per year in profit to overseas investors (last count), even in the best of times. All these overseas owned franchises are nothing more than parasites. Any decent business people would understand that.

Any politician who encouraged the sale of our assets to offshore interests has clearly been on the take. Time for us to take back our country.

@Good Samaritan ......the days of us remitting $20 Billion in profits to overseas investors are over for now , and I would not be surprised if some of those businesses are sold by the foreign investor , especially where the foreign investor has borrowed in their home country to buy the asset in the first place

I would suggest that the unemployment rate could top double figures in Q2

" We ultimately expect the unemployment rate to rise to 15% in Q2"

" The lowest unemployment rate since the global financial crisis of 2007–08 was 4.0%, recorded most recently in the December 2019 quarter. After the global financial crisis, unemployment reached a high of 6.7% in the September 2012 quarter. This was considerably lower than the series peak of 11.2% in the September quarter of 1991, which followed significant structural changes to the New Zealand economy. This unemployment series started in 1986."

Combine the record levels of expected unemployment, with high household debt levels (and those debt levels are based on two incomes), and high house valuations.

Also combine the above with the concentration in debt.

Remember that 8% of households owe 40% of the household debt. - https://www.stuff.co.nz/business/money/104323467/reserve-bank-says-8-pe…

So if a proportion of these households get into cashflow stress (and the probability of this occurring has significantly risen due to COIV-19), there will likely be more than just one house that will be sold for each stressed borrower - there could be many houses sold.

For example. a property owner who owns 3 properties all for rent in the Airbnb market.

8% of 1.76 mln households is 141000. Total mortgage debt in NZ 280 BLN. 40% of that is 112 BLN

divide by 141000 = 794000 average per each one of those 8% households.

Good luck paying that off with no job and no rental income.

The Man 2 claims to have seen a $35k drop in interest payments over the past year, thanks to reducing interest rates.

If interest rates have dropped 1% (the 2 year fix was 4.3% around this time last year) then The Man 2 has $3.5 Million in mortgages.

Here

by THE MAN 2 | 29th Apr 20, 12:34pm

......but we are continually getting pay rises due to fixed rate loans expiring and interest payments decreasing significantly. This past year our interest payments have decreased by over 35k, which isn’t too bad, with more on the way.

That stat 8% vs 40% blows my mind CN - every time you post it.

Is it possible to work out how many homes that 8% own based on an 'average house price' of say $600,000?

Take the $112bn of mortgage debt owed by the 8% as calculated by WestieAJ above.

Depends on LVR for these borrowers.

1) assuming an LVR of 40%, then that would be house value of $280bn. Using $600,000 median house price - then that is 466,667 houses

2) assuming an LVR of 50%, then that would be house value of $224bn. Using $600,000 median house price - then that is 373,333 houses

3) assuming an LVR of 60%, then that would be house value of $187bn. Using $600,000 median house price - then that is 311,111 houses

3) assuming an LVR of 70%, then that would be house value of $160bn. Using $600,000 median house price - then that is 266,667 houses

So anywhere between 266,667 to 466,667 houses.

For context

1) NZ has 1.87mn residential dwellings (2018 census) - https://www.stats.govt.nz/tools/2018-census-place-summaries/new-zealand…

i) 266,667 represents 14%

ii) 466,667 represents 25%

2) in the last 12 months, there were approximately 75,000 house transactions.

i) 266,667 represents 3.5 years of transactions

ii) 466,667 represents 6.2 years of transactions

Note that during the GFC in 2009 the average number of property transactions the last 12 month period was about 61,000.

This is where the potential for the huge imbalance in the property market is between effective supply and effective demand. We don't know :

i) how many property owners can come under stress, (a proportion will be positive cashflow investment properties) nor

ii) how many properties they own (and could potentially sell).

iii) how many properties will be listed for sale,

iv) how distressed they will become, nor how time constrained they will become.

v) or how the banks will respond - they may be willing to extend and pretend - this is dependent upon the magnitude of house price changes -

a) if prices fall such that LVR's reach unacceptable levels, then banks may be willing to ask property investors to reduce their mortgages.

b) if prices don't fall, and LVR's remain at acceptable levels, then banks may be willing to extend and pretend (and even defer mortgage payments and capitalise the interest)

There is a potential negative price feedback loop.

The above numbers don't even include those owner occupiers who bought in the last few years, using high levels of leverage (and high debt service ratios) and then suddenly experience a large drop or loss of income.

Or those with holiday baches ...

Then there are people likely to be in similar circumstances as this businessman (who had interests in 8 investment properties in addition to their owner occupied house)

Tremewan said he had tried to protect staff by putting about $600,000 of his own money and from another company he owned into Welhaus.

He had sold his family home at Redcliffs and his family would be renting from the settlement date in January, he said.

According to Terranet Advance Web and Ahei Ltd, companies owned by Dan Tremewan and his brother Colin, and directed by Dan Tremewan, own seven properties in Christchurch and one in Akaroa.

Tremewan said some of the properties had since been sold and the remainder were being put on the market "to keep financiers happy".

They would be used to pay first and second mortgages and he did not expect there to be any extra money.

https://www.stuff.co.nz/business/property/116378021/ecohouse-businesses…

or the foreign owners who are net sellers

" In the 12 months to the end of March overseas buyers purchased 669 New Zealand residential properties and sold 1290."

https://www.interest.co.nz/property/104800/sales-residential-property-f…

For negative cashflow property owners - read comments here, highlighted a year ago. (that number may have decreased due to lower interest rates since then)

https://www.interest.co.nz/news/99060/we-look-changes-average-loan-size…

This is a perfect storm of:

* massive govt, personal and business debt

* OCR almost at rock bottom

* soaring unemployment

* overinflated house price to income ratios

* mickey mouse monetary policy

* bad habits reinforced by GFC08

The tsunami is here and it's time to find out who's houses are build on sand.

*average household debt to income around 163-164%

*small open country heavily dependent on the global economy

*vulnerable risk associated currency

Good point about currency - I have very low confidence in NZD fiat. In the last 2 weeks have shifted investment strategy and now there's $0 in NZ cash.

I bailed in Jan and am waiting for it to collapse easy profit and can sleep at night knowing my money has a guarantee unlike NZ.

I will send it back to buy more assets once price slump which should coincide with dollar collapse fingers crossed.

Can I ask where you bailed to? I'm looking at doing something similar

Overpriced houses built on sand...sounds like Papamoa....surfs up!

I think NZ has the second to lowest government debt : GDP of all the OECD countries. Private debt however, that's a different story

Deleted.

I'm more worried that the failure of NZ Inc to diversify further than it has will really come back to haunt us in the coming years. We have a tech sector yes, but its only a fraction of what it could have been had the right governments been behind the sector all those years. Xero could have been 100 by now.

One hour of paid work per week makes you employed. So if pre lockdown you had 2 part-time jobs giving you a total of 20-40 hours per week worth of pay. Now one of those employers has gone bust and the other ones cut you back to 5 hours per week. You are still "employed" but you are broke.

Give us the stats/spend on WINZ benefits (all types) week by week. That tells a truer story.

The article highlights once again the slow, out of date & almost irrelevant data coming from our state services sector. If the virus has shown us anything, it's the importance of up to date & relevant data.

NZG: Fail.

I stumbled onto these more up to date numbers once. They give until April 25th for Jobseeker.

Quite a shock.

https://www.msd.govt.nz/documents/about-msd-and-our-work/publications-r…

Unemployment will be 20%. If you factored in those that lost jobs that didn't qualify or took a pay cut or reduced hours the actual impact is even worse than official numbers are ever going to show.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.