By David Chaston

Is the average new mortgage getting larger or smaller?

Does the average home loan size track house prices?

How pervasive is the use of mortgage debt capacity as an ATM for household spending?

These and many others are questions fundamental to understanding the risk borrowers are taking, not only for themselves, but for our overall financial stability as well.

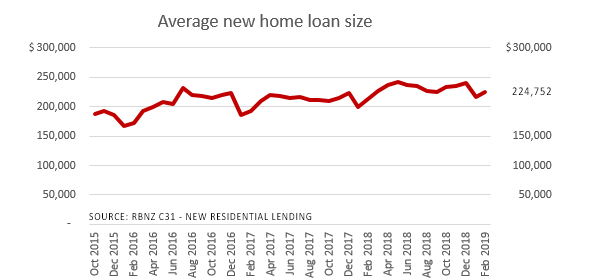

While these questions are actually hard to answer definitively, the Reserve Bank (RBNZ) does publish data on the value and volume of new mortgage lending, and this gives some insights. The chart above is from the RBNZ series C31.

Before we get into what this data shows, you should note a difference between the charts used in this story and the related tables. In the charts, the rate of change is from the current three months compared with the same three months a year ago. In the tables the 'change %' is a strict change from the listed month compared to the same month a year ago. When charted, the month-vs-month view is quite volatile, so the three-month-vs-three-month view smooths out that volatility.

Another point to note is that we don't have anything but national data for C31. This is an issue when trying to make sense of the averages and growth because the Auckland market is overweight in 'value'. Readers will need to draw their own assumptions about what this means and we have supplied both national and Auckland regional house price data in all the following tables to help give a sense of what that might be.

| All properties | Average loan size |

Median house price |

Average LVR |

||

| change | change | ||||

| $ | % | $ | % | % | |

| Feb 2015 | 178,660 | 430,000 | 41.5% | ||

| Feb 2016 | 172,275 | - 3.4% | 450,000 | +4.7% | 38.3% |

| Feb 2017 | 192,112 | +11.5% | 496,000 | +10.2% | 38.7% |

| Feb 2018 | 212,532 | +10.6% | 530,000 | +6.9% | 40.1% |

| Feb 2019 | 224,752 | +5.7% | 560,000 | +5.7% | 40.1% |

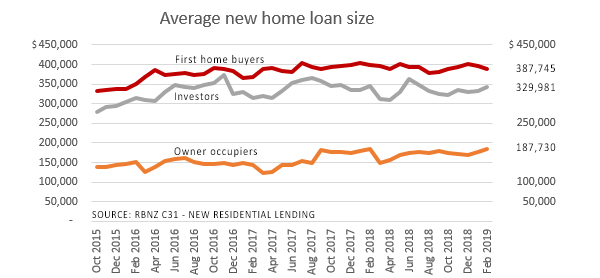

The RBNZ C31 data series can break this down by types of borrowers. And from that data we can derive averages over time for first home buyers, owner occupiers, and residential investors.

While there is a clear separation between the averages of each type, it is harder to ascertain borrower behaviour from this chart. To do that, we have tracked year-on-year changes. That gives noisey results, so the following are rolling three-month results and the trends stand out more clearly that way.

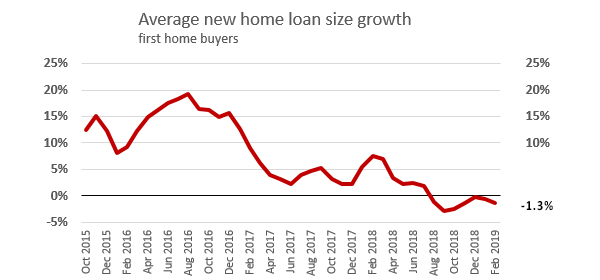

First home buyers

It should not be a surprise, but this data clearly shows that first home buyers are not increasing the size of the obligations they are taking on, in national aggregate at least. Household affordability gives the upper limit.

There may also be a geographic shift embedded in this data however. As first home buyers retreat in the high-priced Auckland market, it is possible that the averages here are being helped by fewer Auckland transactions, more regional transactions and thereby moving the weight of transactions to less expensive properties on lower priced markets.

Over all of 2017, the total volume of loans to first home buyers decreased. From 2018 onward they have been increasing. Without regional data it is not possible to know the impact of the non-Auckland mix variance, but that does correlate quite well with poor Auckland home loan affordability data we have.

The following table offers loan size comparison data matched against both the New Zealand national house price, and separately against the Auckland house prices. We have chosen to do the comparison at the lower quartile level because this is the more likely entry level for first home buyers.

This data doesn't make a lot of sense nationally with the effective loan-to-value ratio (LVR) looking like it is more than 100%. Clearly, this is a result skewed by the Auckland factor. And for Auckland alone, LVRs lower than 60% seem unlikely as well. So it is clearly somewhere between, likely above 80%. The tell-tale is that the 2019 data in this table suggests a slight relief and it might be a reasonable guess that this is more to do with the mix moving away from Auckland than anything else. Certainly this data shows Auckland first quartile house prices are not declining - just as they aren't nationwide. But those Auckland prices are more than 70% higher than the national average. NZ-excluding-Auckland prices will be lower again.

| First home buyers | ||||||||

| Average loan size |

NZ lower quartile house price |

AKL lower quartile house price |

NZ avg LVR |

AKL avg LVR |

||||

| change | change | change | ||||||

| $ | % | $ | % | $ | % | % | % | |

| Feb 2015 | 310,462 | 292,000 | 510,000 | 106.3% | 60.9% | |||

| Feb 2016 | 349,704 | +12.6% | 300,000 | +2.7% | 600,000 | +17.6% | 116.6% | 58.3% |

| Feb 2017 | 367,081 | + 5.0% | 332,000 | +10.7% | 630,000 | + 5.0% | 110.6% | 58.3% |

| Feb 2018 | 399,231 | + 8.8% | 360,000 | +8.4% | 668,000 | + 6.0% | 110.9% | 59.8% |

| Feb 2019 | 387,745 | - 2.9% | 391,000 | +8.6% | 680,000 | + 1.8% | 99.2% | 57.0% |

The data doesn't allow us to be definitive, but it helps us focus on better questions.

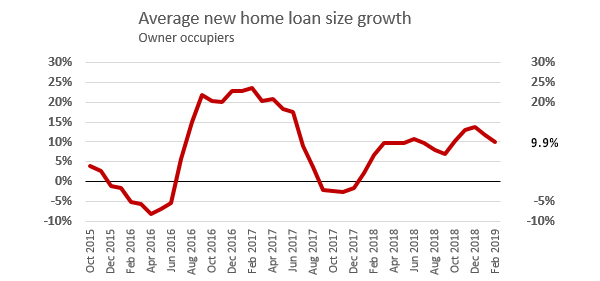

Owner occupiers

What stands out here is that the average loan size for owner occupiers is still rising, and rising currently at about a +10% pa rate.

These are 'new loans' for borrowers who already own a property. 'New loans' are defined that way as 'new to the bank'. To be a 'new loan' that must mean the borrower has changed banks. Or they are trading up. To be increasing so solidly, such borrowers must be upping their leverage, prior capital gains as a deposit on a new 'better' house, or are using their home as an ATM.

And it has been going on, on average, for a while. It was only in the shadow of the Global Financial Crisis that real deleveraging took place.

But remember, the great bulk of owner-occupier borrowers are not doing this. The data only captures the ones who are.

We don't actually know how many homes have mortgages. In fact, things are more complicated than that. Many homes may have more than one mortgage. Borrowers may split their borrowing between fixed and floating, or a range of fixed terms. That all adds to the number of 'loans' against which 'new loans' are counted. About the only thing we can say is that there will be fewer houses than loans, but we just don't know how many fewer. You might assume that the ratio of loans-to-houses is pretty constant, and if you accept that then the trends from the data can be useful. But we actually have no way to test that the loans-to-houses relationship is stable.

| Owner occupiers | ||||||||

| Average loan size |

NZ median house price |

AKL median house price |

NZ avg LVR |

AKL avg LVR |

||||

| change | change | change | ||||||

| $ | % | $ | % | $ | % | % | % | |

| Feb 2015 | 139,265 | 430,000 | 687,000 | 32.4% | 20.3% | |||

| Feb 2016 | 126,546 | - 9.1% | 450,000 | +4.7% | 770,000 | +12.1% | 28.1% | 16.4% |

| Feb 2017 | 155,233 | +22.7% | 496,000 | +10.2% | 827,000 | + 7.4% | 31.3% | 18.8% |

| Feb 2018 | 173,185 | +10.9% | 530,000 | +6.9% | 855,000 | + 3.4% | 32.7% | 20.3% |

| Feb 2019 | 187,730 | + 8.4% | 560,000 | +5.7% | 850,000 | - 0.6% | 33.5% | 22.1% |

About three quarters of all new home loans are to existing owner occupiers - as they switch banks or raise their leverage. That may seem like a high percentage, but it is actually likely to be a low proportion. The last time the RBNZ disclosed the number of housing loans in 2004 there were 1.1 million of them. This new C31 data shows that in the past year there were only 17,200 owner-occupier borrowers, suggesting an annual churn of about a bit over 1%. That is very low.

These few borrowers have been raising their leverage as house prices rose. But it is clear that their ability to do that in the next few years will be curtailed.

These types of borrowers are unlikely to threaten financial stability with this type of behaviour. With about 98%+ of borrowers not doing this, they are very much the outliers. In the past year, their 'new loans' amounted to just 15% of all mortgages, and the house-as-ATM factor is probably about 1.5%. (Of course, it will be more than this, because redraws with the same bank that don't require new loan documents are not captured in the C31 data.)

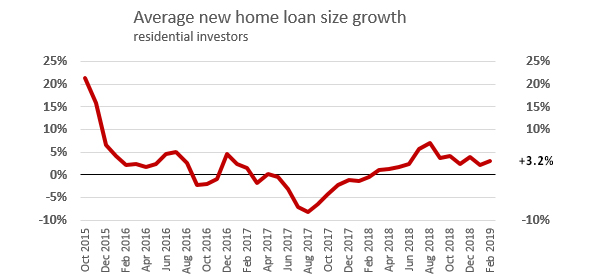

Investors

Residential housing investors seem much more restrained than owner occupiers. For at least the past three years the average loan size has changed very little. This suggests these borrowers take out the initial funding, then set and forget it.

The data also suggests that there are affordability limits for investors as well, limits that are pretty strictly adhered to. In five years the average new loan size has only grown by +7.5%.

If rents have been reasonably stable until recently, debt levels would have had to remain restrained as well for the commercial side of the investment to remain in balance.

| Residential housing investors | ||||||||

| Average loan size |

NZ lower quartile house price |

AKL lower quartile house price |

NZ avg LVR |

AKL avg LVR |

||||

| change | change | change | ||||||

| $ | % | $ | % | $ | % | % | % | |

| Feb 2015 | 306,595 | 292,000 | 510,000 | 105.0% | 60.1% | |||

| Feb 2016 | 315,749 | + 3.0% | 300,000 | +2.7% | 600,000 | +17.6% | 105.2% | 52.6% |

| Feb 2017 | 310,585 | - 1.6% | 332,000 | +10.7% | 630,000 | + 5.0% | 93.5% | 49.3% |

| Feb 2018 | 316,916 | + 2.0% | 360,000 | +8.4% | 668,000 | + 6.0% | 88.0% | 47.4% |

| Feb 2019 | 329,981 | + 4.1% | 391,000 | +8.6% | 680,000 | + 1.8% | 84.4% | 48.5% |

Having said that, rents have started to rise more quickly in 2019, and that might be behind the recent lift in average loan values.

The main takeaways

This data doesn't deliver a clear conclusion. But it does help frame better understanding of new mortgage level trends.

My key takeaway is what it it doesn't show. It doesn't show pervasive irresponsible borrowing. In fact, you can hardly see any evidence of borrowers splurging with debt. Sure, there may be a few outliers who use their mortgage as an ATM for conspicuous consumption, but that does not show up in the data at all. Loan growth on average is quite restrained.

And this data shows we need it regionally because the twist the large Auckland market gives to the national figures can't be separated here. It should be. The risks to financial stability might be growing in the Auckland market under the cover of national averages. Who knows? (Well, hopefully the RBNZ knows.) If we guess that they might be, then the rest of New Zealand needs policy decisions that isolate the remedies to where the problems are. Only with regional data can we discuss this more intelligently.

The restraint of both first home buyers, and also investors, is good to see. It suggests borrowers are making sensible financial decisions. First home buyers aren't ignoring affordability risks and investors aren't ignoring sensible commercial settings.

And finally, it is surprising and reassuring that the churn implied by the level of owner occupied borrowing is very low indeed.

C31 is a helpful resource. Let's hope that the RBNZ plans to include regional data.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

26 Comments

What struck me are the awesomely low LVRs overall All Properties table

Or perhaps you just missed the unsustainable ones in the FHB and Investor tables ?

The LVR data are only really useful to show whether they have been increasing or decreasing over the last few years and it's great to see that for FHB and Investors (the 2 most exposed categories), the LVR's have decreased over the last 4 years.

The LVR's for AKl are unfortunately meaningless because they are calculated by dividing the NZ wide mortgage by the AKL median house price. Could we get an average mortgage size for the Akl region only?

:) no I didn't, I looked through that section of the table but couldn't reconcile the high investor numbers ... some were over 100 percent. That conflicted with figures in another section. I thought someone would have a dig, but would not have bet on you doing that David. Overall I was impressed thanks

Had another look at your investor figures david, I cant make head or tail on several counts not the least of is the comparison with LVR requirements. Under res housing investors table In 2019 the reported investor lvr is 84 percent and in 2016 over 105 percent of loan. RBNZ LVR (2013) investor rules I think allow only 5 percent of loans to be over 70 percent lvr, not an average LVR of 105. So how can that be? Maybe the new lending amount is taken in isolation as an lvr of the new asset purchase rather than of total portfolio LVR? This, if it is the case, would screw with your results. Banks usually assess a new property loan based on total portfolio and will still do no money down loans on the basis of the whole portfolio.

C31 tables show in 2019, 4 million dollars of investor lending greater than the 80 percent lvr. There is total investor lending of 886 million. In other words half of a percent of the value of lending is above 80 percent LVR. You show an overall investor LVR of 84.4 percent in 2019 showing in the Residential Housing Investors table. Please elaborate David

Houseworks, read my comment above (19th April, 5:42 PM) and you'll understand

Great stuff David. Of course, this data is representative of all loans 'not extinguished' so I'm sure you would see stark differences in the data sets if you could compare 'Total loans issued' with 'all loans issued since 1990', 'all loans issued since 2000', etc.

Actually, it is only for 'new loans' in the month, not all loans. Details are here.

"Total value of monthly committed residential mortgage loans, which are finalised offers to customers to provide mortgage loans or to increase the loan value of an existing mortgage loan, as evidenced by the loan documents provided to the borrower."

While it is good to see analysis David, I fear you may have misunderstood the definition of new lending. The definitions include increasing existing loans... and it doesn’t require a change of bank

So let’s assume there is a scenario where a borrower increases loan by 50k to say renovate... that just appears as 50k in the owner occupied column. You cannot infer LVR from this data .. as it is not the full exposure. This data generally matches the speed limit data the rbnz also puts out, which includes top ups. Well, that’s my take. It would explain what you see as massively different lives. Whereas a FHB cannot by definition be skewed by top ups

When people take out a mortgage, the majority of the time it gets split up into smaller loan amounts on different terms. In Australia, the RBA released data that showed the average loan size was quite small but then Deutsche bank economists found the RBA data to be wrong and misleading of the overall picture. The RBA had been using all of the smaller loan portions to create their averages instead of the larger complete totals of the overall mortgage. I wonder if the RBNZ is making the same mistake here and presenting their data in this same way?

The NZ loan average data is my construction from the gross data. It is not the RBNZ claiming these averages. There is no suggestion at all that this represents the average mortgage obligation per property. Of course it will be more based on exactly what you say. But we are looking for changes here, not the absolute level. This analysis is not claiming to be an 'accurate science', just revealing the data we know.

Very interesting article David, deserving of a better title than "Is the average new mortgage getting larger or smaller?"

The only regional splits for LVR data are the Auckland/non-auckland splits on the c30 web page.

You can see what data the RBNZ collect in the LVR survey their surveys page.

ooo ... I missed that. Thank you. Will take a look and see what it shows. It is almost certainly useful and I am a bit self conscious we missed it.

Hi David. Did you uncover any response to my previous question about whether split loans were being counted by the RBNZ?

Given 16,000 new loans were recorded in Feb against 5900 transactions. Overcoming the LTV issue would be easy if for a bank if $1,000,000 purchase were as an example to be made up as a deposit of 250k and Loan of 375k on 1 year.. (one mortgage reported to RBNZ) Second mortgage of 375k (same deposit) but on a three year term - but therefore a different mortgage to report to the RBNZ? The c31 numbers are so out of line with the significant decrease in the volume of transactions over the last couple of years that c31 reporting - like APRAhas discovered in Australia starts to becomes questionable - would you not agree?

Banks are required to report the number of commitments as 1 per loan application. Eg split loans are grossed together and counted as one.

You can see the LVR reporting requirements on the RBNZ website.

Despite the pickers of holes amongst the commentariat, DC, at least the article starts to ponder the real questions about loan size versus house price levels.

Of course there are lacunae in the data. Everywhere from international digital trade (trillions uncounted), our very own Census or should that be small-c "census", immigration levels, and so on. But until research like this happens, the gaps aren't apparent, and the effort to plug 'em has zero impetus thereby.

Well done.

David,

Is there any data on debt servicing payments to household income ratio, debt to income ratio levels? Any financial stress by the majority of borrowers on residential property is likely to be in the area of excessive debt servicing relative to household income levels.

Yes. The RBNZ has a specific series on that, here. And you can download their data. Serviceability is at record-low stress (data goes back to 1998).

Thank you David.

Just trying the understand the calculation inputs into the serviceability statistic.

Can you explain how the "nominal disposable income" is calculated? Is it at a national level, and not the individual household level?

Is this the nominal disposable income figure that they use in the above calculation? - https://figure.nz/chart/PrIY7u3FsNNYKia1-OjlH3rHOOkj26fEj

see Notes to C21, which includes this:

"Household disposable income

Household disposable income (gross disposable income plus interest) Data for March quarters is Statistics New Zealand estimates from the household income and outlay account. The latest March year estimate is using the growth earnings over the quarter, published in Statistics New Zealand’s Quarterly Employment Survey. Data for other quarters is Reserve Bank estimates interpolated between March year benchmarks. Revisions will occur when new annual benchmarks become available."

For more than this, you may need to email: stats-info@rbnz.govt.nz

Many thanks to you for that David.

So just to confirm, the "Servicing as % nominal disposable income" compares

1) debt servicing of all households in NZ with

2) the nominal disposable income of all households in NZ.

The issue is that we are comparing the debt servicing of all households and comparing this to the income of all households (and this includes the household income of households with no debt). If there are a large number of households with no debt included in the denominator of the above calculation, then the above ratio would look unduly low and could provide a false level of comfort with respect to financial stress vulnerability levels.

For a real indication of potential debt stress, shouldn't the comparison be comparing the debt servicing of households to the household income of only households with debt? After all we don't need all households to be in financial stress, we just need a sufficient number of households to be in financial stress.

If you look at a micro-economic level and at the individual household debt levels, here is something to consider:

https://www.interest.co.nz/personal-finance/97115/325-debt-disposable-i…

One area of concern regarding property investors is that in the 2016/2017 tax year, there were 116,000 tax filers who claimed tax losses resulting from rental property ownership. (Refer http://tenancieswar.nz/other/loss-ring-fencing)

1) the average loss claimed was $7,138, which means a total of $828,008,000 of losses.

2) assuming little non cash expenses such as depreciation, this is cash that has to be paid from household budgets.

If these rental property owners experienced unexpected financial cashflow strains, then that is likely to increase financial pressures. Some potential areas of cashflow strains:

1) costs to meet Healthy Homes requirements

2) interest only mortgages that are converting to P&I mortgages - in some cases debt service payments could increase 30-40%.

3) potential ring fencing of losses from rental property operations

There are also rental property owners who are profitable from a tax perspective, yet the property is also currently a cash burden on household budgets. The negative cashflow arises from the required payment of principal of the mortgage payment in a P&I mortgage.

There are also rental property owners who are profitable from a tax perspective, and the property is currently cashflow positive due to interest only financing. If that interest only mortgage becomes a P&I mortgage, then the debt payments may result in the rental property now becoming a cash burden on household budgets. Remember when these mortgages were taken out in 2015 / 2016 when there were auction frenzies for property in Auckland, many assumed that interest only loans would be rolled over into another interest only mortgage - the credit environment in 2019 is very different to the credit environment in 2015 / 2016.

All of the above are vulnerable in a recession when unemployment rises which results in a lower household income if a household income earner is laid off (or has lower wages) and there may be households that need to sell their rental properties as they are cashflow stressed in meeting the costs of maintaining ownership of the rental property.

The 116,000 claiming tax losses on rental property represents

1) about 22% of rental properties owned in NZ by my estimates.

2) based on the last 12 months sales transactions of residential real estate in NZ of 75,320 - that 116,000 represents 154%, and at current sales volume levels would take about 18 months to sell through. You can put your own assumptions as to how many could come under stress and wish to sell.

3) based on the current national sales listings of 37,713 on realestate.co.nz, even if you take 20% of the 116,000 coming up for sale that is 23,200 or about 61% of current listing levels.

And this is before counting for those profitable rental property owners who may come under cashflow stress, or owner-occupiers who may come under cashflow stress.

That is how there becomes an imbalance between effective supply and effective demand for residential real estate. If property owners find that there are no interested buyers at their price expectations levels, and if the property has been listed for sale for a long period time, the vendor's price expectation may drop to attract potential buyers.

One key variable is what the banks will do with financially stressed borrowers - they may choose work with borrowers to give them time - they may extend loan repayment periods, allow borrowers to go on interest only for a period of time (I hear that these techniques were used in 2008/2009). If a borrower is already on interest only terms, then there may be little that the bank will do.

I also hear anecdotal stories that many who are unable to get financing from the big 4 banks are seeking alternative lenders such as non banks and other banks that might be less stringent in their debt servicing credit standards, so this may help those in financial stress.

Remember that in free markets, prices are set by the marginal buyer and seller. You don't need a large number of sellers if there are fewer active buyers in the market.

Most of the loss making investment properties are likely to be located in low yielding locations such as Auckland & Queenstown. So if you compare the 116,000 loss making properties with the level of transactions in those areas, the potential imbalance for effective supply and effective demand is even higher than on a national level.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.