As usual the Reserve Bank's latest bi-annual Financial Stability Report, issued yesterday, is full of charts and tables detailing crunchy information about New Zealand's financial system.

I've plucked 10 out that caught my eye. They, and a blurb or two about each one, feature below.

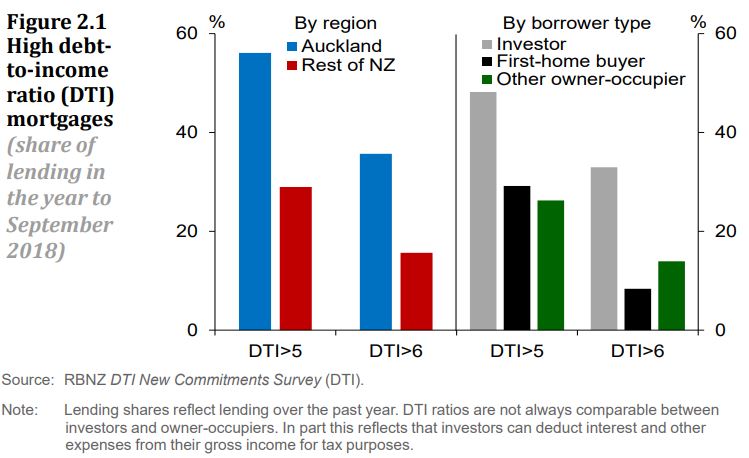

1) Highly indebted households.

About 60% of bank lending is to the household sector and New Zealand’s household sector carries a high level of debt relative to its income. The Reserve Bank notes debt in the sector is concentrated within certain types of borrowers.

"The most indebted households are typically those with mortgages. These households tend to have higher-than-average incomes, but have far higher levels of debt. Their debt-to-disposable income ratio, at 325% on average, is near its historical high. Debt is further concentrated among those households with investment properties, those who have had less time to pay down debt, and those who have purchased in regions with relatively high house prices, such as Auckland," the FSR says.

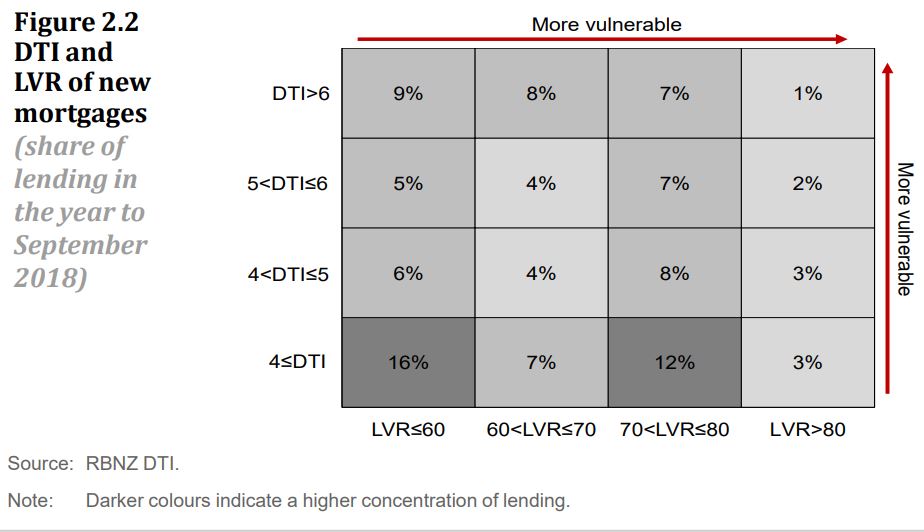

2) 'Over a third of borrowers look vulnerable.'

Following on from 1) above, the most vulnerable borrowers have debts that are large relative to both their incomes and the value of their assets.

"Only 1% of the value of new mortgages is to borrowers with both DTI [debt-to-income] ratios above six and LVRs [loan-to-value ratios] above 80% (figure 2.2 below), but over a third of borrowers look vulnerable on at least one of these metrics."

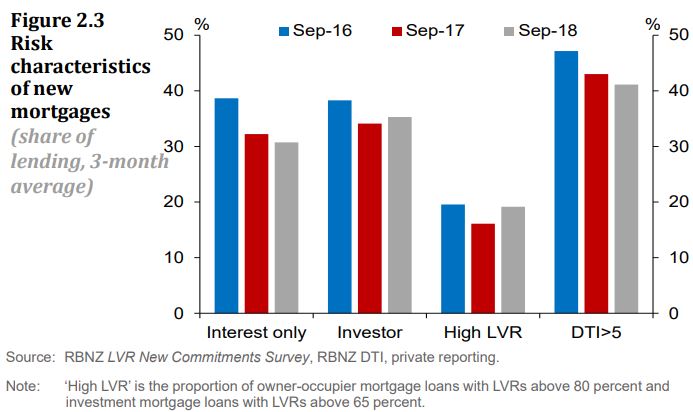

3) Household debt 'now growing at a more sustainable rate.'

The FSR says the Reserve Bank remains concerned about debt levels, but notes the annual growth rate of household debt has slowed from 9% in 2016 to 6% in September 2018. According to the Reserve Bank, household debt is now growing at a more sustainable rate, broadly matching the pace of household income growth.

"There are signs that households that borrowed in recent months are in a better financial position than those that borrowed in previous years (figure 2.3 below). Borrowers are tending to borrow less relative to their incomes, and the proportion of new mortgages that are not being repaid over time – those on ‘interest-only’ terms – has steadily declined. The share of loans going to investors is below the level seen in 2016. Investors typically pose a higher risk to the financial system than owner-occupiers, partly because they have a greater incentive to default strategically when house prices fall. Investors can also amplify undesirable swings in house prices by buying and selling as conditions change," the FSR says.

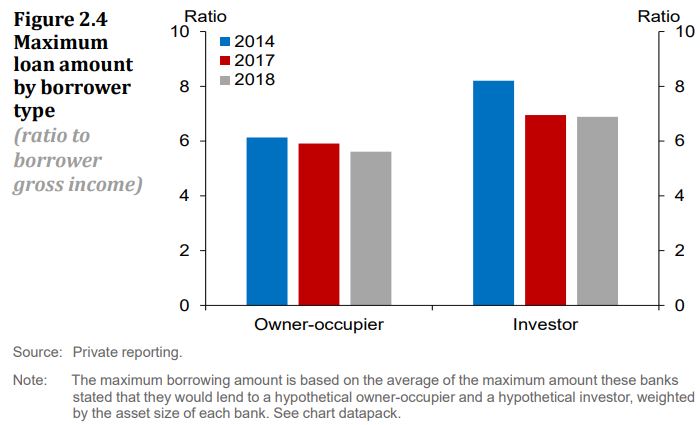

4) Banks prepared to lend less to the same set of borrowers, relative to their incomes, than they were four years ago.

The FSR notes banks have gradually strengthened their loan serviceability policies over the past two years and are now assessing households’ ability to make loan payments against higher living costs and interest rates.

"In a recent exercise conducted by the Reserve Bank, banks estimated the amount they would be willing to lend to a range of hypothetical borrowers. The results suggest that banks are willing to lend less to the same set of borrowers, relative to their incomes, than they were in 2014 (figure 2.4 below)."

"Despite the easing of LVR restrictions at the beginning of 2018, banks have tended to maintain or tighten their serviceability standards. Banks are expected to maintain their serviceability standards, but household sector risks, and banks’ exposure to those risks, could quickly resurge if serviceability standards were to ease," the FSR says.

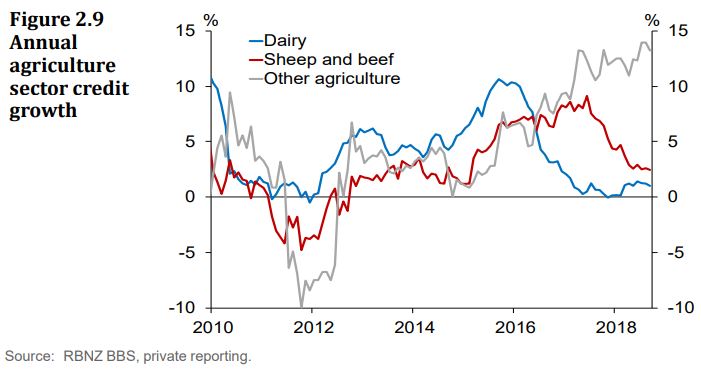

5) 15% annual growth in horticulture lending being monitored.

The agriculture sector accounts for around 14% of banks’ total lending exposures, which amounts to $61.9 billion. Some two-thirds of this lending, or $41.5 billion, is to the dairy sector. Dairy farming became "highly indebted" after a period of strong investment, a run-up in land prices, and two significant milk price downturns in the last decade, the FSR notes.

Additionally debt in the dairy sector is concentrated, with some farms carrying disproportionately large debts. The sector remains vulnerable to another price downturn.

Thus banks have been diversifying their agriculture lending portfolios. They have $14.1 billion of lending to the sheep and beef sector, and $6.3 billion to other agriculture. This last segment - highlighted by horticulture - has been growing, as demonstrated in the chart below.

"Lending growth to the horticulture sector has been particularly high at around 15% in the year to September, while lending to the dairy sector has only grown slightly. Although diversification can help to reduce risk overall, most agriculture sectors are at risk of swings in commodity prices, and prices for agriculture commodities often move together. This may lessen the benefits of diversification. In addition, rapid growth into smaller sectors can carry risks of its own. The Reserve Bank will continue to monitor growth in lending to these sectors," the FSR says.

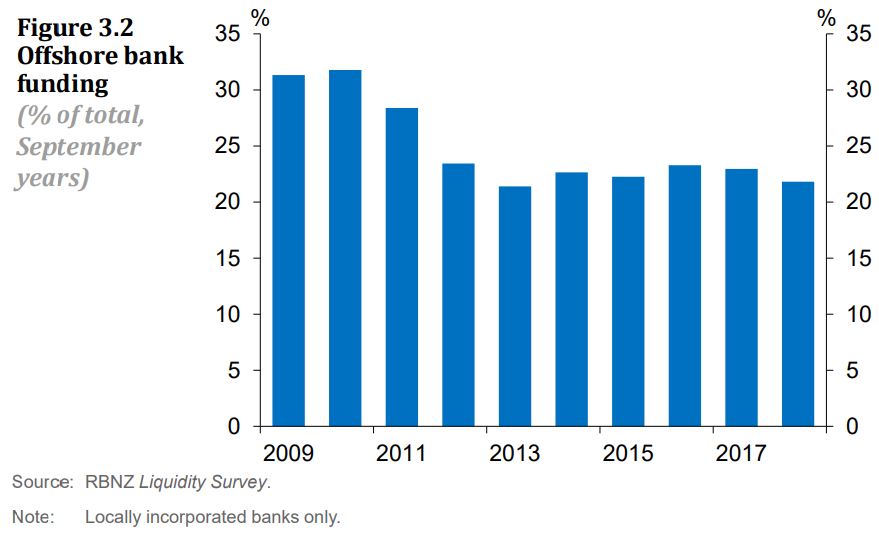

6) Reliance on offshore funding drops.

New Zealand banks’ reliance on offshore funding has, fortunately, decreased since the Global Financial Crisis. According to the FSR, our banks currently source 22% of their funding from abroad, down from 31% in 2009. Additionally, the average maturity of banks’ market funding has increased, reducing the proportion that would need to be replaced during a market disruption.

"Banks have also improved their resilience to short-term disruptions in funding markets by increasing the average maturity of their market funding. The share of banks’ outstanding debt with maturities under a year declined from 49% to 37% in the two years to September, while the proportion with maturities greater than three years increased, from 24% to 31%," the FSR says.

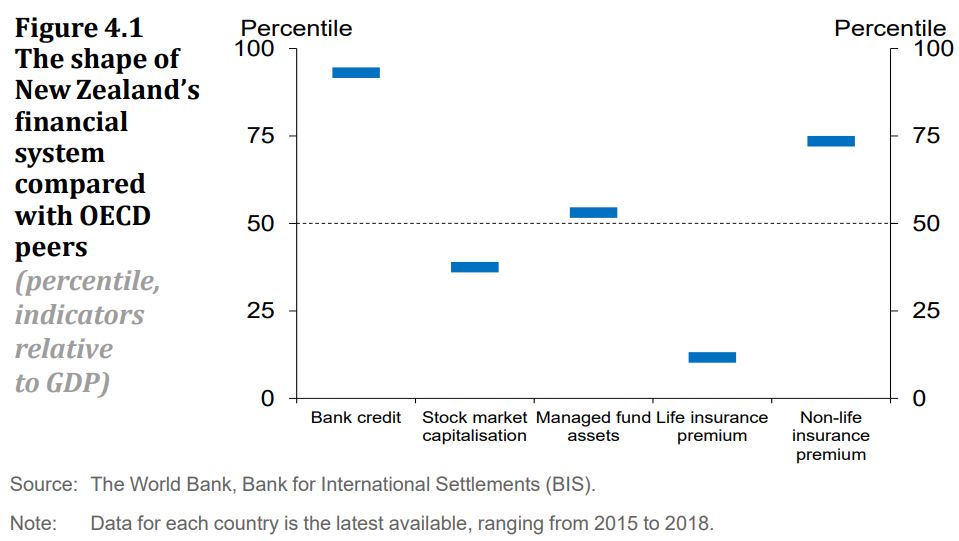

7) Our banking system is big relative to the economy's size in comparison to other OECD countries.

"The financial system improves the investment and consumption opportunities available to households and firms by intermediating funds between savers and borrowers. In New Zealand, this role is dominated by the banking system, which is larger relative to the size of the economy than in most other OECD countries (figure 4.1). New Zealand’s banking penetration is high, with over 99% of adults having bank accounts," the FSR says.

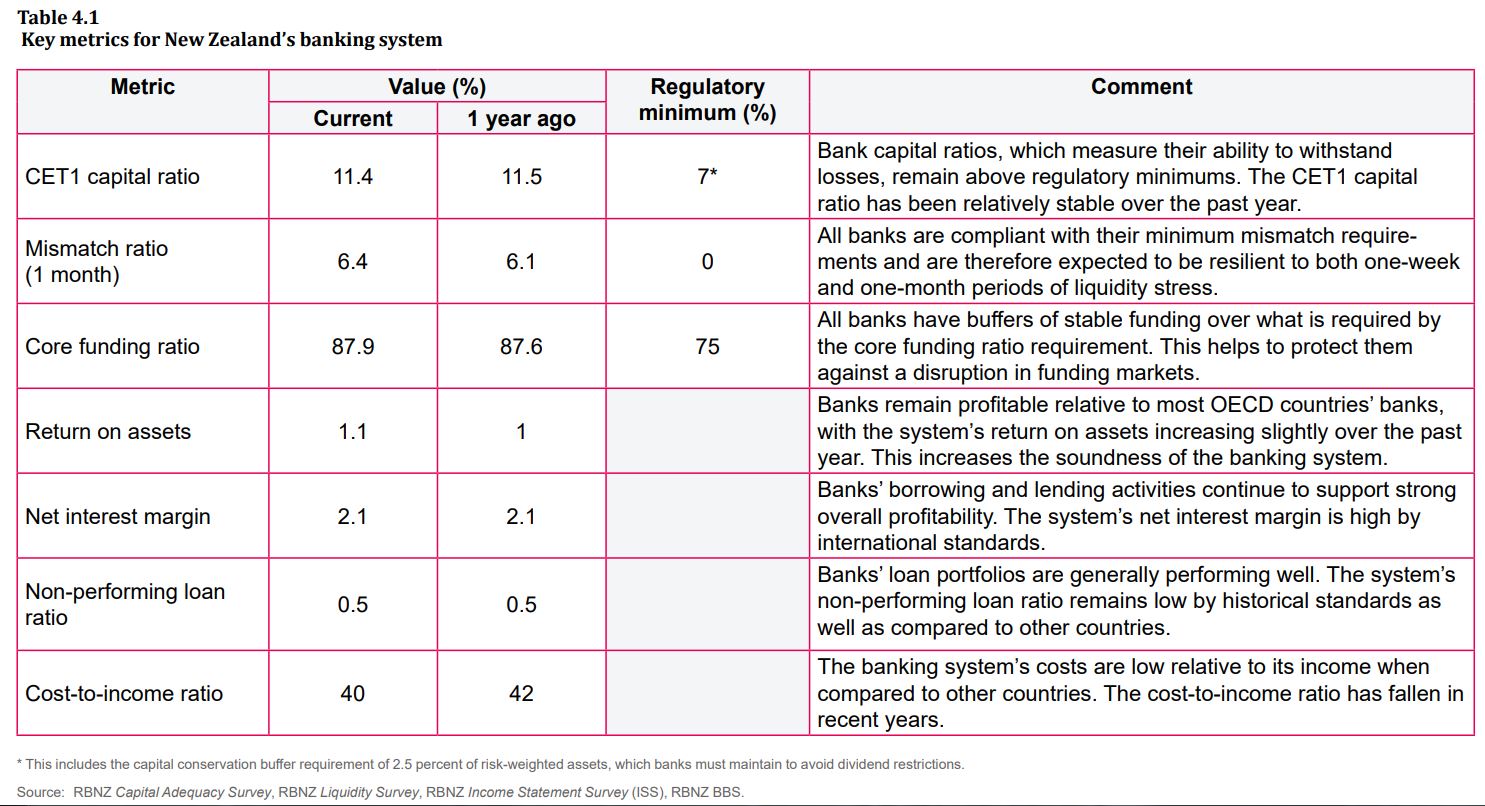

8) Key metrics for New Zealand's banking system.

The FSR notes banks have increased their total capital over the past two years, from 13% to 14% of risk-weighted assets.

"This trend has been evident across both smaller and larger banks. The smaller banks tend to have higher levels of common equity Tier 1 (CET1) capital, which is the highest-quality form of capital, whereas larger banks tend to make more use of additional Tier 1 (AT1) and Tier 2 capital. A well-capitalised banking system is critical for the overall soundness of the financial system. The Reserve Bank is reviewing its capital requirements for banks," the FSR says.

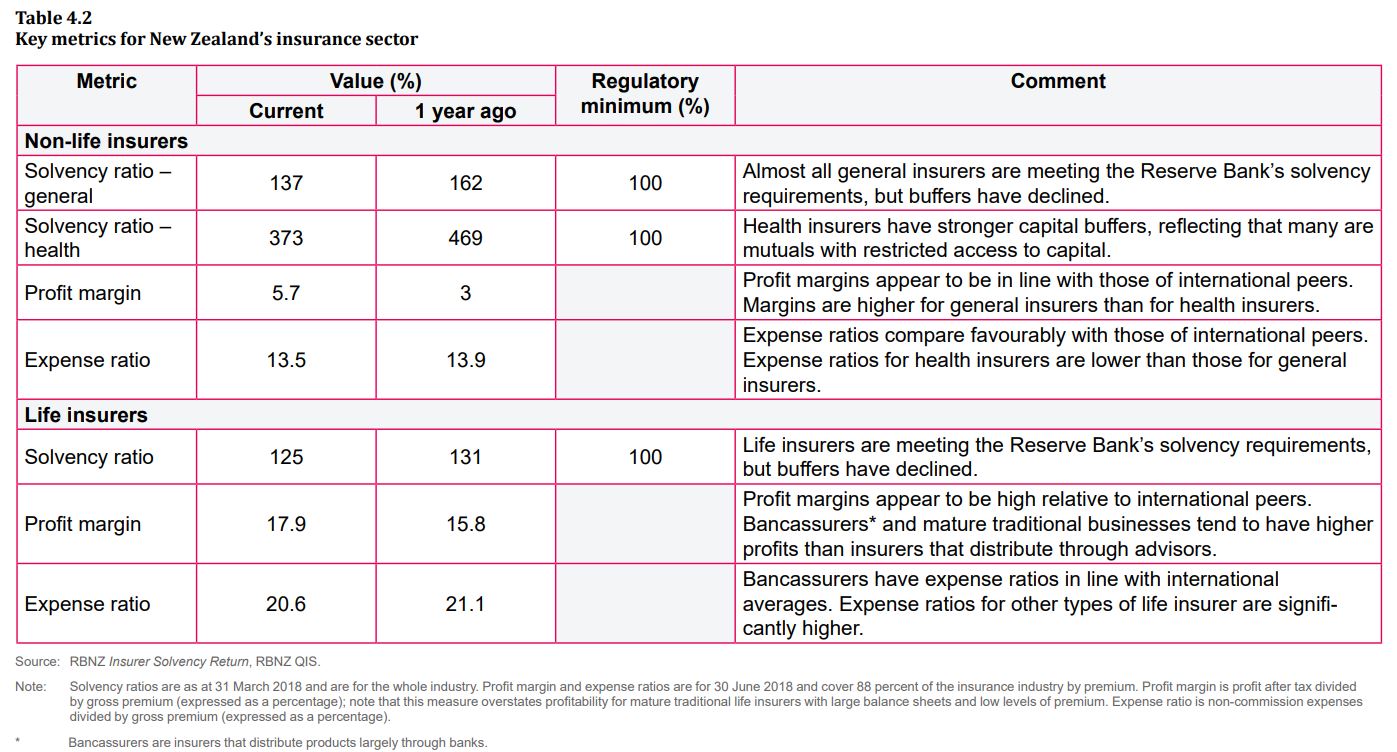

9) Key metrics for New Zealand's insurance sector.

The Reserve Bank says a prerequisite for a sound insurance sector is that insurers are strongly capitalised to withstand a range of possible loss events. On the whole, it says NZ's insurance sector is profitable and almost all insurers are meeting their minimum solvency requirements.

"However solvency ratios have fallen across the main classes of insurer, indicating a reduction in the sector’s capital strength. Furthermore, the distribution of solvency ratios raises concerns about the ability of some insurers to comfortably meet minimum requirements in the event of an adverse shock. As at March 2018, 12 out of 59 insurers had solvency ratios below 120%, and seven had solvency ratios below 110%. Given that solvency ratios have been volatile in the past, these insurers’ buffers above the minimum requirements are small," says the FSR.

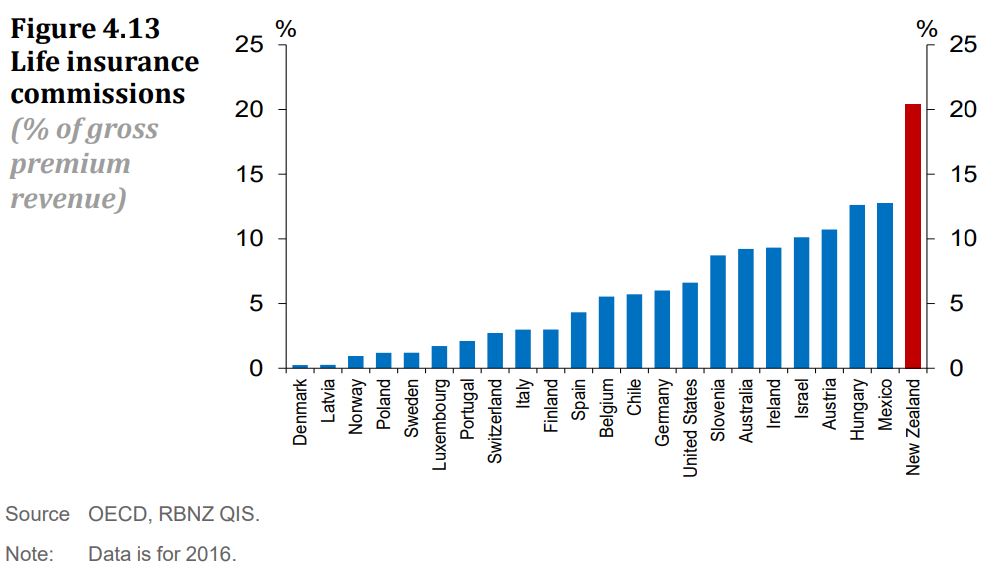

10) New Zealand life insurers pay high commissions to advisors.

The Reserve Bank says the life insurance sector appears to have been slow to adapt to new technologies and changing consumer preferences towards online product distribution. Rather it has continued to rely on the traditional advisor sales channel, where life insurers pay high commissions to advisors. Commissions in the New Zealand market are very high when compared with those in other countries, according to figure 4.13 below.

"Insurance advisors have an important role in helping buyers select insurance products that meet their needs. However, the high level of commissions and other incentives that life insurers pay to advisors can create conduct risk. In some cases, advisors could be incentivised to encourage policyholders to switch to different insurance policies even if the changes do not benefit the policyholders. Such activities can compromise the efficiency of the sector, because policyholders may not be matched with the best policies, and ultimately end up funding high commissions through high premiums," the FSR says.

The Financial Markets Authority and Reserve Bank are currently reviewing the conduct and culture of life insurers. Onsite visits began in August and finished in November. A report is expected to be published in late January 2019.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

27 Comments

Nothing to say about the report, but I Do like them Embiggen widgets.

"the proportion of new mortgages that are not being repaid over time – those on ‘interest-only’ terms – has steadily declined."

From 40% to ~30%; that's still a recipe for disaster. How many were issued prior to 2016? Heaps I'd suggest, and those are coming off 5 years interest-only onto 'Scheduled Repayment' ( mustn't get that confused with Principal and Interest repayment, which it is not!) are doing so in ever-increasing numbers. Add the burden of increased mortgage servicing costs ( as a result of going off Interest-Only) to increased rates from the latest round of 'revaluations' across the country ( I believe Tauranga, for instance, is getting theirs now, and 25% increase is not unusual! ), and the wave of P&I default looms large.

Why are we still issuing Interest-Only Mortgage to residential borrowers? (that's where the 325% loan to Income comes from?)

Why are we allowing Off-Set Loans (which in my view defeats the object of IRD 'tax on interest' rules)? (NB: Most countries don't allow it)

The answer to both of those questions, of course, is because we can't afford to rock the banking boat at this stage of the game. That will come later, if at all!

I agree with all of your points bw.

One slight saving grace in the short term might be that interest rates are slightly lower than when these interest only mortgages were written in 2015/16, making the transition to P&I slightly less painful. Whereas in Australia the punters dealing with the same transition could be facing higher interest rates.

I wish the RBNZ provided good data on what proportion of 'interest only' loans were offset vs. actual interest only, and then a further breakdown of average/median offset balances (or something like that).

" interest rates are slightly lower than when these interest-only mortgages were written" which is the NUMBER ONE reason why....mortgage rates are going...a lot lower!

@bw After your first 5 years on interest only most borrowers extend for a further 5 years. Even if they do not, those that bought in say 2013 have very small loans as property was comparably cheap back then. Properties bought for $350,00 in 2013 have rents of $450+ today. That means the 25 year table remaining costs less to service than the rent that comes in. There will be a shortfall after costs of ~$5,000 pa but that is hardly severe.

It is rare to see interest only on owner occupiers. But the reason you see IO on residential rentals is because it is tax efficient to repay your home loan before your investment loan.

What do you mean scheduled repayments are not principal and interest by the way?

Rates do not rise with valuations. Rates are set by relative value.

Offset loans are common place and both the UK and Ausi use that function. The USA, which does not, is behind the game on this. In the USA you have to use the antiquated product called revolving credit, its the exact same outcome but clumsy.

" most borrowers extend for a further 5 years"

Do they?! Have you tried it recently? I have, and I can tell you that it's under extreme sufferance that banks will want to extend the interest-only period. The main reason they will extend is the incapacity of the borrower to be able to pay the new Scheduled Repayment Amount. Yes, time extensions are being given, but I'd suggest that it's an exception rather than the norm ( and keep in mind, if the Principal of a 25-year loan has been compressed into 20 years by the interest-only period of 5 years, guess what happens after 'another 5'?! That's' right! the Scheduled Repayment Amount becomes the full principal + current Interest payable to be discharged over, not the 20, but 15 years. Do the maths and see what the Repayment amount would be then! That's'why the banks are reluctant to 'extend' - its' a known problem for later down the track)

To your other question: After the Interest Only period expires, whatever Offset Amount you may have saved to lower the Interest Payable over that time, vanishes for calculation purposes when Scheduled Repayment kicks in. Anyone who assumes that banks will charge Principal + Interest ( interest payable on the net amount after Offsetting what they've saved) is wrong. The Banks will make THE FULL repayment each week/month - the Scheduled Repayment Amount - regardless of any offsetting that might have applied in the past. I had to go to the Ombudsman to argue that, and even though I still believe the banks are wrong on the issue, gave up in frustration.

Laminar makes a good point, it's very different if you're an owner-occupier or investor.

- for an owner-occupier by all means repay your mortgage as soon as you can

- for an investor there's no need to ever repay your mortgage at all. Firstly you pay only about 2.7% interest (4% - 33% tax deduction), secondly your tenant pays for your interest and thirdly it gets better over time as rent and house value slows goes up (long-term).

I think 1-2 years back there was a reasonable chance of there being a property crash in Auckland in particular. While it's still a possibility I do think the risks have reduced somewhat. A decent external or interest rate shock would be enough to do it, especially now that foreign capital inflows have been reduced.

Aside from a crash, the next question is will there be a moderate correction over the next few years? It's impossible to know, but I still think the risks are weighted somewhat towards the downside. I think prices could easily drift 5-15% lower in nominal terms and 10-20% lower in real terms over the next few years. It's very difficult for prices to remain elevated as lending standards are tightened and incomes are out of sync. Immigration and 'housing shortages' don't create much demand at current prices.

At a guess, I'd put probabilities for Auckland prices for the next few years;

Rapid price growth (5%+ pa) - 10%

Inflation price growth (1-3% pa) - 30%

Modest declines (-1 to -5% pa) - 50%

Big declines (-10%+ pa) - 10%

One thing is for sure, the "next upward swing in 2020/21" is nonsense, unless there is a specific driver for it, i.e. interest rates go lower, bank lending standards collapse, immigration skyrockets, foreign capital is allowed in, tax changes, etc. There has always been a catalyst for house prices increasing and without one there won't be an upswing.

Another interesting chart in yesterday's report was the house price to income chart on page 10. According to the RBNZ it has reduced from 10x to about 8.8x in Auckland.

If DTI lending limits is 6.0, and if LVR limit is 20%, then the price to income of the house to be purchased is only 7.5 (=6/(1-0.20)). As noted, in Auckland, the average price to income is 8.8, which is 17% above what can be supported by lending even at these extremely lax levels. A ludicrously high DTI of 7 is required to make the arithmetic work.

Agree Peri. I think the bank of mum and dad, investors, and falling prices (over time) help explain the gap.

As do lower and higher interest rates.....

ie.. they are a big part of the Story..

Thanks Gareth, that's a really useful summary. Like the graphic that accompanies the article, very appropriate.

A question for you... David and I have had a few discussions about what is 'interest only' and what isn't. It appears that 30% of loans are still being written as interest only. Does that 'interest only' data, include offset mortgages as David has suggested in the past? My view has always been that offset usually follows a payment plan for capital and only the excess is held as offset against interest.. therefore offset mrotgages are not interest only products...and therefore 'interest only mortgages' are exactly that, interest only.

Can you help me to confirm?

Many thanks

Nic

Agreed Nic - a great article.

Some positive trends there (e.g. source of bank funding, new lending ratios and type etc), but with cooling and uncertainty in future of property market as well as protection against external risk factors, these trends need to continue.

Hard to fathom as to why NZ life insurance commissions (20%) are twice that of Australia (10%). Clearly some concerns worthy of FMA investigation into insurance.

Indeed, the life insurance commissions were a bit of a surprise.

Example:

Anyone who drew down an Interest-Only Loan 5 years ago; stuck the whole borrowed amount into a call account with the same bank ( and had 100% Offset, in other words) was not charged any amount whatsoever during the first 5 years. Interest was Offset; Principal repayment wasn't due until after the first tranche of the loan expired and it reverted to "Principal and Interest Repayments". But...

If the loan remains 100% 'Offset' after the first 5 years of Interest Only expires, the bank will start charging the full Scheduled Repayment Amount ( innocently called the Principal and Interest Amount) regardless of any offsetting Amount - that previously reduced Interest Payable to $zero..

What the bank does is - it charges the full Scheduled Repayment Amount ( call it the P&I, is you like!) and any Offsetting Amount that is 'surplus' to the calculation it uses to reduce the term of the loan. In the case of a 25 year on, where the Principal is to be repaid over the remaining 20 years, that effectively reduces the term to about 10 years. It's compulsory!

Interest Offset only applies during the 'interest-free' term. After that Interest-Offset is used to reduce the term of the loan regardless of what the customer may understand or want.

Here's' how it works ( and should do in my opinion!) at Barclay's in England.:

"That creates a saving that you can use in 1 of 2 ways.

Use the saving to reduce your payments

You can ask us to use the interest you save to reduce the amount you have to pay each month over the term we agreed in your mortgage offer letter.

Or use it to pay off your mortgage sooner

Alternatively, you can use your savings to help reduce the length of your mortgage by offsetting them against your mortgage balance – and reducing the amount of interest charged."

https://www.barclays.co.uk/mortgages/offset-mortgage/

The first alternative doesn't apply in New Zealand, and most customers will not be aware of that.

Number 11. use of credit

amount of credit used for activities to increase GDP

amount of credit used to increase consumption

amount of credit used for transactions trading/purchases of assets

After looking at those first 2 graphs & commentarym I'm more baffled than ever as to why they would reduce minimum investor LVRs.

Absolute madness.

Have the debt metrics 'improved' as the percentage of Auckland sales as a percentage of national sales has fallen from 40 percent 3 years ago to the current low 28.8 percent .

Just for information at the height of the UK's property boom interest only lending accounted for around 16% of all mortgages written.

Very useful report Gareth. With over a third of borrowers looking vulnerable, this is enough a party killer in the event of an overseas borne shock. Then there's dairy.....

One of the things coming out of Aussie, is the irresponsible lending to the farming sector.

Our market is imo not to dissimilar. Most farms are reliant on capital appreciation (land) to remain solvent. many actually run operating losses. Balance sheets are often characterised by large revaluation reserves.

Without this many would be insolvent (have negative assets)

This will put the banks credit/lending departments under the pump. There will be some very creative accounting going on to support various assertions.

the RBNZ will no doubt scrutinise this sector. The risk to the banks/rbnz and crown has just risen massively.

Getting rid of foreign buyers amplifies the problem. As many farmers when they retire look to offload property to wealthy immigrants. That tap has been well and truly turned off by this government.

Adrian Orr will be well aware of this, and just this week came out and made comments around the agri sector risk. And that the banks here may need to increase the capital they hold. This will be in direct reference to this, along with risks directly associated with Akl property.

We following the Basil rules when setting minimum capital requirements for the banks. However as a country, we have so much of our wealth tied up is overpriced real-estate. These measures, along with the non existent provisioning by the banks (less than 1%) is hardly prudent. The minimum capital requirements stipulated by the Basil committee assumes we follow the global trend. We don't. We are at the extreme end of the risk spectrum, both in terms of concentration of assets, large exposures to few counterparties, and massive DTI rates. I would argue we should set our own capital requirements. The higher the better, as this will stop the parent banks dragging out excessive dividends to prop up problems there.

The other matter is how banks foreclose on farms. The softly softly approach will most likely result in a few additional basis points added to the risk premium of the average agri loan.

Ball and chain goes on the people (mortgagors) in this country, not the house...

Those Auckland numbers are craazzzyyyy.

What makes Auckland special that it can sustain so many mortgages at > 6? The answer, nothing. The market up there is dependent on prices going up to sustain it. Which might explain why the reserve bank felt it needed to give it a little boost and is too scared to raise rates.

It would be funny if it wasn't so serious. Massive bank lending for housing, completely out of all proportion to our economy. RBNZ desperate not to rock the boat. Government intent on underwriting a house building scheme....

If immigration goes down, for any reason, we could easily have a sudden surplus of overpriced new build houses. The government then has to choose; keep building and reduce prices, thereby risking a slowly cascading fall in all house prices; or stop building immediately, and get some more immigrants in pdq. My guess is they will keep building, as decent affordable housing really is a worthy cause. Remember, they are an idealogically driven lot, them bureaucrats and politicians. The shared ideology being that they know best (ie better than us lot, which may actually be the case, but not enuff to matter). The problem is the slowly cascading fall then cascades faster and faster, which leads to interesting times....

Do we end up with cheap houses by accident? Presumably the RBNZ will support the government (I mean, the governor almost sounds like a government spokeman, bless him), steadily reducing interest rates to make the overpriced new builds "affordable". Employment should stay strong, lots of jobs bending nails with hammers. Eventually the party has to stop and overbuilding cease, either that or we are back to desperately seeking new immigrants.

We seem to have two ever so slightly different flavours in the Bureaucrat and Politician Party, those who favour more immigration and much higher house prices (especially their own), and those who favour more immigrants and more houses and steadily rising house prices (especially their own). So, given the impossibility of them getting it right for long, presumably at some point we get less immigration and lower house prices. Or something else we don't expect.

I still think the banks will end up being nationalised.

Nah, what I think will happen is the RBNZ will be acquired by Westpac and dissolved.

listen words say,

the banks need more capital

https://www.youtube.com/watch?v=StjBB_F-4f0&feature=youtu.be

and the plan is house prices flat, incomes rise, but it just a plan.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.