The Institute of International Finance (IIF) says given an unprecedented increase in global debt, it's not clear how the global economy can deleverage without meaningful negative implications for economic activity, and suggests a "reflationary fiscal response" over the next decade.

The IIF, which describes itself as the global association of the financial industry, makes these comments in its latest quarterly Global Debt Monitor, which tracks international indebtedness by sector.

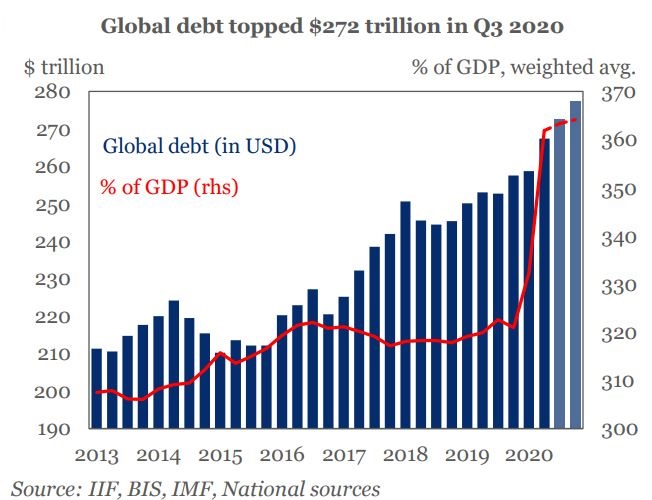

"The pace of global debt accumulation has been unprecedented since 2016, increasing by over [US]$52 trillion. While some $15 trillion of this surge has been recorded in 2020 amid the COVID-19 pandemic, the debt build-up over the past four years has far outstripped the $6 trillion rise over the previous four years and over earlier comparable periods," the IIF says.

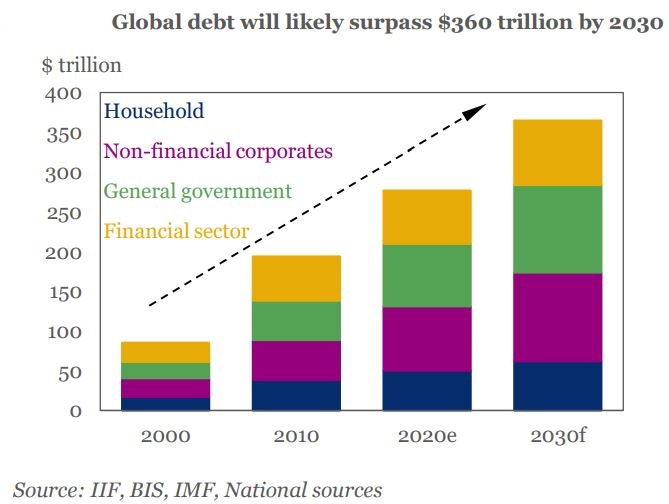

"As a result, there is significant uncertainty about how the global economy can deleverage in the future without significant adverse implications for economic activity. The next decade could bring a reflationary fiscal response, in sharp contrast to the austerity bias in the 2010s. If the global debt pile continues to grow at the average pace of the last 15 years, our back-of-the-envelope estimates suggest that global debt could exceed $360 trillion by 2030 - over $85 trillion higher than current levels."

The IIF says strong rises in both government and corporate borrowing as the COVID-19 pandemic drags on saw global debt increase by US$15 trillion in the first three quarters of 2020 to more than US$272 trillion.

"With little sign of a slowdown in debt issuance, we estimate that global debt will smash through records to hit $277 trillion by the end of the year," the IIF says.

"Following a record surge in global debt-to-GDP (from 320% to around 362% in the first-half of 2020), the rise in the third quarter of 2020 was more modest, at less than two percentage points—helped by the strong global recovery. We expect that the global debt-to-GDP ratio will reach some 365% of GDP in 2020."

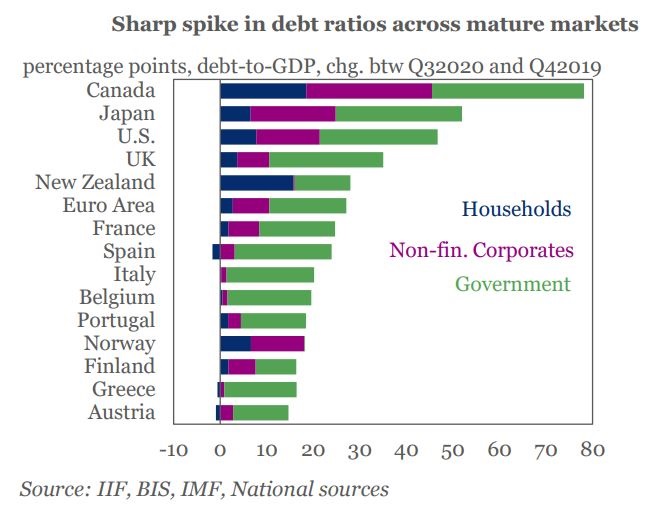

Meanwhile, the IIF says debt in so-called mature markets topped 432% of GDP in the third quarter, an increase of more than 50 percentage points from 2019. The United States accounted for nearly half the increase, with total debt on track to hit US$80 trillion in 2020, which is up from US$71 trillion last year. Most of the rise was in the general government, up US$3.7 trillion, and non-financial corporate sectors, up US$1.7 trillion.

Debt outside the financial sector reached US$206 trillion in the third quarter, up from US$194 trillion in 2019.

"Governments accounted for 60% of the $12 trillion buildup in the world’s debt pile, excluding financials. Global non-financial corporate debt rose by over $4.3 trillion to a fresh high of near $80 trillion, while household debt rose by $500 billion, to near $50 trillion," the IIF says.

The IIF chart below highlights New Zealand's high level of household debt compared to other countries, except Canada, in the chart.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

42 Comments

"Following a record surge in global debt-to-GDP (from 320% to around 362% in the first-half of 2020), the rise in the third quarter of 2020 was more modest, at less than two percentage points—helped by the strong global recovery.

"...strong global recovery" - show me the evidence?

Suddenly, everything at once had been lined up perfectly, absolutely perfectly for reflation. A reckless Fed pledging more. Overseas announcements of already more. Stimulus, lack of rioting, vaccine. Everything, I mean everything, was happening the right way. Treasury rates were primed to head to the moon (and the dollar to zero).

So, why didn’t they?

For one thing, the Treasury market wasn’t primed to selloff at all. Nominal yields had been pushed higher, sure, but not on actual reflation which continued to be conspicuously absent in all the other key bond market prices and indications. Only beginning with the short end (bills).

What had been happening was simple and misleading: long bond/end shorts were using whichever news to short some more – and that’s all it was. Link

Ouch! US retail sales growth has dropped to a six-month low…Retail sales only rose by 0.3% in October, disappointing economists who expected a 0.5% rise…Growth is better than the alternative for retailers, of course, but this does flash warning signs that the US economy is slowing this quarter. It’s the weakest monthly rise since the spring lockdown ended. Link

Thanks. Arguably the most important news is that about interest rates. I'd wondered about the US 10yr, I wasn't looking hard enough. I'm of the opinion that when interest rates do get to the upper trendline in the downward trend that we are probably not far away from another crisis that will push them down again.

Thanks Gareth.

Some of us were pointing out that this overhang was inevitable, some time ago. Here's the best explanation of the problem: https://surplusenergyeconomics.wordpress.com/

Everyone reading this thread, who is of an economics background, needs to read that piece. Take the time. It's where we are going, so worthy of much cranial crunching. Essentially, there ain't enough surplus energy or enough good-quality resource stocks left, to repay the debt (by doing the work to the future stuff). So it will remain unrepayed - even below zero interest-rates.

So either interest goes, or it increasingly disenfranchised increasing numbers of others - who will vote for charismatic promisers. Who can't deliver. Ultimately it means collapse or war(s) and we are naively unprepared for either.

The same rational is explained succinctly here

Any article that does not know the difference between government debt (the issuer of its unit of account) and private sector debt (the user of the unit of account) cannot be taken seriously.

Also as economist Wynne Godley described with his theory of 'stock flow consistent modelling' for every liability there must be an equal and offsetting asset and so there can be no assets without equal liabilities.One persons asset is anothers liability.

I agree. Also, we can't treat all public debt the same - a proper economic analysis would ascertain the amount of public debt going into new infrastructure (capital assets) vs what's being borrowed to keep the lights on (opex).

Debt is a forward bet. Doesn't matter who holds it (except to them, vis a vis each other).

If there isn't enough future underwrite, the debt is irreconcilable.

Period.

T'ain't rocket science.

The government can repay its own debt at any time that it chooses just by the push of a computer keyboard button, its called QE. It just sends reserves back into the banking system from whence they came.

try this

"Trying to export inflation will fail for these reasons: first, our currency will fall in value, making our imports more expensive (so re-importing the inflation). If we respond by starting more factories here, that will defeat the plan to export the inflation. Lose either way.

Second, if we flood the world with cheapened dollars, they will recycle those dollars to the US by investing their surplus dollars in US assets, including real estate. That money will go into the real economy and create inflation.

Excess printed money going into giant corporations is no safeguard against inflation. They will still circulate the money through the economy. And it doesn’t matter what they spend the money on. Some people have recently acquired the goofy idea that if you spend the money on something useful, it will not cause inflation. Wrong. Production growth is not productivity growth.

The same with financial institutions. They are not allowed to spend or even directly loan out bank reserves, but cash earnings are a whole different story.

“delay debt repayment”–no, we can’t. US debt is in bonds and creditors expect to be paid as it comes due. We roll our debt over all the time. If you fail to do it, it is called a sovereign bond default. But in the event of inflation, they will not hold those bonds. They will unload the fast depreciating assets as quickly as possible, destroying the US bond market and credit rating. And people will not be stashing their money in savings accounts because people don’t like to save in dollars in an inflationary environment. They want to spend the money before it depreciates further.

“big institution can borrow for next to nothing” — not because we are big, but because they think an institution this big can afford to repay them. But if we are trying to repay with cheaper dollars, our borrowing costs will rise in a hurry. Remember the 1970s?

Finally, MMTists want to use the new money to fund either Universal Basic Income or, more frequently advocated, government jobs for every adult who wants one, none less than $15 with full benefits and no firing. The productivity of the job will not be an issue. (I read online the paper that many of them are citing as a guide to the future.) I guarantee you that a lot of that money will stay right here in the USA and fuel inflation.

I keep telling these crazy online MMTists there’s no free lunch, but these utopians are determined to believe there is. When QE is injected into the banking system as bank reserves, and the US Treasury is required to accept broad money only (not bank reserves) for its notes, bills, and bonds, it is not a serious inflation risk. But if it is used to monetize government spending, then you are following in the steps of the Weimar Republic and a substantial number of other hyperinflationary victims that are not as well publicized.

MMT=Monetary Madness Theory"

MMT does not support a universal basic income but it does promote a job guarantee, unemployment has seriously negative social outcomes and what is the productivity of an unemployed person on a benefit?

Banks are not permmited to lend their reserves except to another bank, they use their reserves for the operation of their exchange settlement accounts. Bank reserves are created in the first instance by the government spending into the economy. Bond sales drain these reserves and QE returns them.

The Weimar Republic had to pay war reparations for the first world war, this is not a situation that NZ is in.

My recommendation to you is to find a new source for your information and not this rambling incoherent nonsense.

or in other words ....Hyperinflation everywhere will not work; its part of what will put an end to most of international trade.

or this

"Short sharp summary:

Energy underpins the existence and value of money.

*********

The existence (creation) of money cannot and never will underpin the existence of and supply of energy."

Can money not build wind turbines and power stations?

Or

its is CONSUMPTION that gives us jobs/employment

Not money

The question is, will consumption be available (if we have money printing but little productivity)?

Maybe ask the soviets how that went

There is always unused capacity and demand in an economy and that is why we have unemployment and poverty. The government should match its budget to need and not some imaginary shortage of money. You seem to be unaware that the banks create money in far larger amounts than the government does, hence our surging house prices.

Economist Prof Bill Mitchell gave a scathing report on Labours obsession with budget surpluses and its failure to tackle child poverty here. http://bilbo.economicoutlook.net/blog/?p=38819

And you (treadlightly) seem to be unaware that we live on a finite planet.

Both banks and Govt are 'creating' (interesting word; it's keystroking, nothing more) ever-more debt, trying to increase your so-called 'capacity and demand'. What you fail to understand is that supply is the problem. That comes when you are trained (I'm guessing) in a discipline which misses, avoids, ignores (in who knows what combination) real Limits.

Which we're up against. Any Economics Prof will be WRONG - and we can see that in Child Poverty. It is, in real terms, Child lack of access to Resources and Energy. Because you end up needing processed resources, the processing takes energy, and (economists haven't realised this yet) 99% of work is fossil energised. (They also can't understand ' productivity', for the same reason; it represents energy-efficiencies, and will therefore come up against thermodynamic limits. Real ones). He may well be a Professor, but he's peddling bollocks. As many then repeat-peddle.

In a 100% closed economic system, where everything is sold and bought using the currency issued by the government that holds true. However, the only closed currency system at present is US (the world trade currency is USD). Anyone else needs to convert their local currency to USD. Are you suggesting that government debt has not impact on exchange rates?

Also it is basic mathematics: If total money in circulation at p1 is X units, at then the government increases that by 100% by borrowing from the Reserve or Central bank, and gives the money to everyone without there being any new goods, assets or services in the market, then the price of everything will increase by 100%

X (total currency in circulation) = Q (quantity of everything measured in money) * P (price)

2X (increase currency by a multiple of 2)= Q (is not affected as no additional goods/services/assets can be created in short time) * 2P (price has to increase to absorb all the printed money).

As you can see, simply increasing government debt is pointless unless the Q can be increased. The Keynesian argument is that where there is a lot of spare capacity, printing money will result in more Qs. However, as we have seen over the past decades, increasing X in saturated western economies, does not affect their Qs, instead it increases the Qs of China and similar countries.

So if government debt simply means inflating the value of other things, it creates a devaluing whatever has to be paid in the currency. So all the things that exist or or benchmarked to things other than the currency will hold their value, while the value of things that cannot benchmark will decrease (e.g. wages). This is exactly what is happening in NZ: asset prices soaring, so your wages (and anything else that cannot be pegged into asset prices) lose their value.

Except in practice, we’ve seen that countries *can* continually expand debt without that foreign exchange pressure showing up — perhaps not in every case, but at least for ‘advanced’ economies. It seems to be far more about confidence than debt levels.

This is where taxation and savings come into the equation, taxation deletes currency and government debt is just the deficit left over that adds to our savings. An explanation here. http://www.matchesinthedark.uk/spending-chains-sankey-diagrams/

Economist Steven Hail explains here why issuing government debt is not necessary. http://www.global-isp.org/wp-content/uploads/PN-121.pdf

The Levy Economics institute explains here that taxation and borrowing don't fund the government. http://www.levyinstitute.org/publications/can-taxes-and-bonds-finance-g…

It is the money that is created by the banks that causes asset price inflation. The Bank of England explains banking here. https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Taxation deletes currency? In imaginary MMT land perhaps, not in our current system.

I just don't understand how you stimulate something in terms of reflation, when globally rates are near zero. Do we cut tax rates across the board and just run with severe deficits for a long period of time and allow government debt to pile up to the point of no return?

That chart makes it scarily clear that all newly-created debt in the last few quarters added to the consumption side of our economy.

It looks like the private sector is doing nothing that will lift wages or grow our productive capacity in the long run, leaving us to scramble over whatever we already produce or import.

That's insane. Can't rule out that happening here in NZ.

MSD's recent report on Otago's skill shortages said if a large number of hospitality workers were to move to construction in Queenstown, there might be enough workers to build new hotels but nobody to staff them.

Looks like a lot of pressure is building on sectors that have gotten away with poor wages and lagged productivity for years. Could this spark wage inflation in NZ?

LOL, nonsense, how do you know that's not just a shot from a traffic camera at morning rush hour?

Read Grapes of Wrath.

We've been here before, but never at global-limits scale.

That Otago 'report' is what you get when you assemble flat-earth believers and ask them to report on the distance to the furthest land-mass. You are pre-determined to fail. As they did.

Things not much better here for some families, this article in Stuff today. https://www.stuff.co.nz/national/education/123425176/hunger-means-schoo…

We have all become too conditioned now into thinking of budget deficits as a sign of poor economic management rather than of something that can have beneficial results. We need to be far better educated about how the governments finances work, starting with our politicians.

That's a part of the problem. Another major roadblock to long-term policy making is our 3-year election cycle that adds a lot of uncertainty to the workings of our public agencies.

Priorities shift dramatically with constant changes in government and new pollies at the helm tend to rescope, reprioritise or scrap funding for strategic policy work already underway. There needs to be more bipartisan support for creating a steady pipeline of work deemed critical to NZ's socioeconomic wellbeing.

Wow. I knew the US were in disarray, socially, politically and economically speaking. But these images surprised me.

At least the stock market is at all time highs! (who cares about lines for food, the economy is great...just look at share prices...)

Independent_Observer,

I was amused to read a forecast that the US market will hit 40,000 sometime next year. It reminded me of Irving Fisher's 1929 comment about the market having reached a plateau from which he couldn't see it falling. Indeed, he saw it rising sharply. That was only just before the Crash.

Would be interesting to see that graph go back past 2008. I suspect that there has been no paying down of debt since that round of stimulus.

We have been here before, just after GFC 2008. Too much debt, more money pumped in, counter party risks exploding, governments to the rescue, money flowing to assets building, gradual easing in unemployment, etc. I think the Central Banks have all of it in control. Expect flood of free money and make use of it, if you can. Only problem is, most of it won't go where it should. Pity.

Oh thats easy peasie! Everyone just carrys on 'printing' and wait till the Mellinials rule the world and take possession of the government benches globally. Then, they'll all universally forgive everyone of their debt! A "Golden Jubilee!" For everyone! And then lets party!

That's the whole point.

The punch-bowl is half-empty, and the last half is the last doubling-time (exponential growth is a sod).

So no party.

"Fear and euphoria are dominant forces, and fear is many multiples the size of euphoria. Bubbles go up very slowly as euphoria builds. Then fear hits, and it comes down very sharply. When I started to look at that, I was sort of intellectually shocked. Contagion is the critical phenomenon which causes the thing to fall apart."

Alan Greenspan

Who is the global debt owed to - the man on the moon? Surely global debt has to balance to zero - isn’t that a simple accounting certainty?

4 days and still speaking like an economist.

The answer is no, but as a hint, try learning before spouting. It makes for a better debate. What you'll find, 3 down from the top, is a link I put up. I'll put it here again. Try reading the first post in that link, maybe take the time to read the first 2-3.

https://surplusenergyeconomics.wordpress.com/

So there's a shortage of underwrite. Sure there is owing, but no ability to repay. So default. So global 'debt' doesn't 'balance to zero' - it is increasing exponentially while the energy and resource stocks diminish ditto. Exponential growth meets finite planet (known as a Bounded System). Those trained in economics weren't told about limits. Which leaves them somewhat limited themselves.

Spectacular bit of talking past the other. I am a firm believer in thinking of the system in terms of its real resources (I’m a scientist and engineer not an economist). My comment was about the actual article above and the ridiculous notion of a purely financial global debt.

Prior to 2008, I though economists were competent. After that (and having noted peak conventional oil in 2005/6, and being aware of EROEI) I started learning about economics. And came to the conclusion that - via externalities (a bin for: Things we don't understand, or which don't fit our per theories) they are ignorant of the real world.

They facilitated 'growth', by issuing more - exponentially-more - debt. Every time, including Covid; it's the only weapon they have. The problem is unaltered; ever-more debt, ever-less planet available, ever-worse energy options remaining.

So the question is: Whither debt? And the answer is: Increasing default. Whether it happens in jerks or one collapse event, is unclear, but it was forward betting and there will be ever-less bet-underwrite. So the debt is written off; bankruptcy being the process whereby it disappears. Interestingly (pun intended) it appears that inflating debt away doesn't work at this end of the energy/resource curve. So it has to be written off. Reminds one of Mack and the Boys in Cannery Row; hitchhiked down to Monterey, haggled for 3 days, then wrote our an IOU for $1.75; which the fellow has yet.

And much of the collateral for the 'borrowing', was nominal numbers against aging houses anyway. We are heading for the biggest 'wealth' loss the planet has ever seen - or can ever again. A one-off event. Nobody is addressing this, or the ramifications.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.