It has been more than a year since the Reserve Bank (RBNZ) started making unprecedented moves to lower the cost and increase the supply of money to support the economy.

Yet the central bank still hasn’t examined how its ultra-loose monetary policy has affected different groups in society, and whether it has increased or decreased income and wealth inequality.

Rather, in a new analytical note, it has referred to international research that reached divergent conclusions on the matter.

Based on this, the RBNZ said it can’t say what impact loose monetary policy has had on inequality in New Zealand.

The RBNZ has loosened monetary policy by cutting the Official Cash Rate to 0.25%, doing quantitative easing through its Large-Scale Asset Purchase (LSAP) programme and providing retail banks with cheap funding through its Funding for Lending Programme (FLP).

To date, it’s bought $51.92 billion of mostly New Zealand Government Bonds through the LSAP programme and lent banks $2.86 billion through the FLP. So, it’s figuratively printed the equivalent of 17% of New Zealand’s Gross Domestic Product (GDP).

The idea behind all these programmes is to lower interest rates to boost inflation and employment in line with the RBNZ’s mandate.

‘Indeterminate’

The RBNZ noted the complexity of trying to figure out the overall impact of it taking the above actions, when these can affect the same household in different ways.

“With lower interest rates, borrowers are generally better off and savers are worse off, but this may be a matter of gains and losses for the same groups of people,” the RBNZ said.

“For example, a family with their own home could earn less income from money in the bank, but the family’s wealth may have also increased because of rising house and share prices.

“A first-home-buyer may need a higher deposit to get into a property because of rising house prices. That may be offset to some degree by lower interest rates on a mortgage paid over many years.

“Lower interest rates also encourage greater business investment and more jobs, and typically result in a lower unemployment rate.

“For example, lower income households tend to be more affected by the unemployment rate than changes in hourly wages. With lower interest rates, a lower income household faces a lower risk of becoming unemployed.”

The RBNZ concluded: “When assessing the overall effect of monetary policy easing on the distributions of wealth and income, it is important to consider all transmission channels."

“The overall effect of monetary policy on inequality depends on the strength of each channel, which may reinforce or offset each other. Therefore, the overall effect of monetary policy easing on inequality is indeterminate.

“The effect of each transmission channel on the distribution of wealth and income depends on a complex mix of various factors such as the existing distributions of wealth and income, household balance sheets and income sources.”

The RBNZ included some graphs in its paper, which show how income and wealth are distributed in New Zealand.

It noted that in 2018, the top 20% of wealthy households collectively held about 70% of total net wealth in New Zealand. Meanwhile in the year to March 2021, house prices increased by 24.3% on average, while the S&P 500 grew 54% and the NZX 50 26%.

However, the RBNZ didn’t go a step further, and calculate the overall net impact of loose monetary policy.

Wealth distribution in NZ

Here is a segment of the RBNZ report that looks at the distribution of wealth in New Zealand:

In aggregate, New Zealand households had $968 billion in non-financial assets (housing and land value) as at September 2020, $844 billion in equity and investment fund shares, and $206 billion in deposits as at December 2020.

Over the past year, the value of some assets held by some households increased. For example, house prices in New Zealand increased by 24.3 percent on average in the year to March 2021. Equity prices have also seen significant increases in the past year. For example, the S&P 500 grew 54 percent in the year to March 2021 while the NZX 50 grew 26 percent over the same period. On the other hand, despite the decrease in interest on bank deposits from 1.53 percent in March 2020 to 0.71 percent in December 2020, household bank deposits increased from $189 billion in March 2020 to $205 billion in March 2021.

In 2018, the top 20 percent of wealthy households collectively held about 70 percent of total net wealth in New Zealand. Half of all households held 94 percent of New Zealand’s total net wealth.

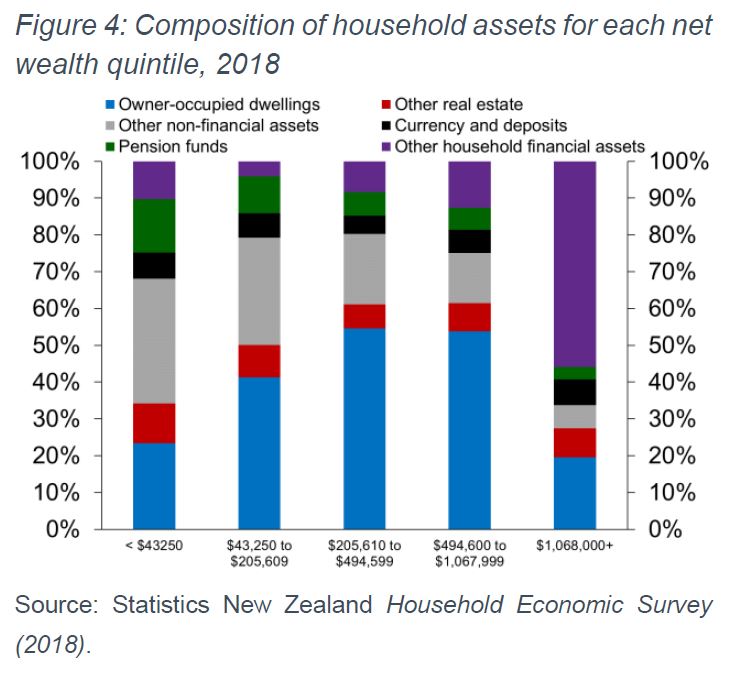

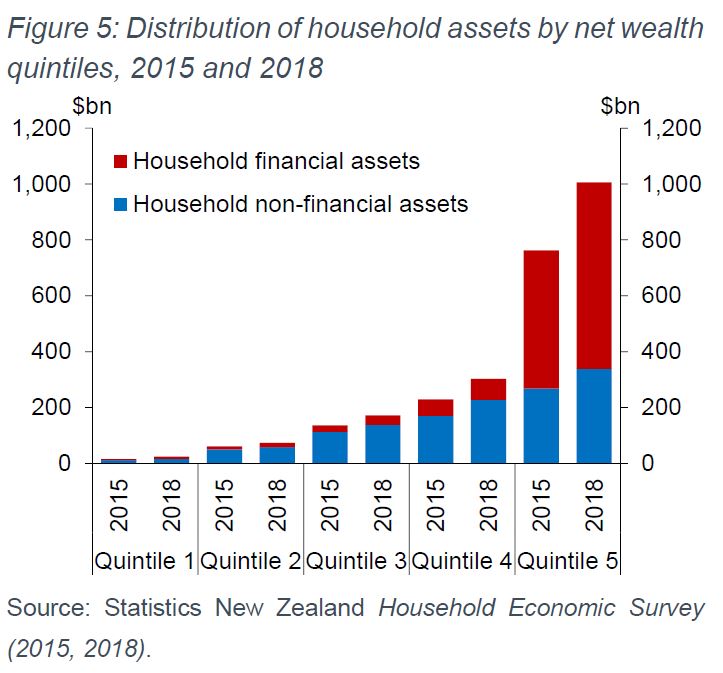

The composition of household assets varied over the net wealth distribution (figure 4). Non-financial assets made up a higher proportion of assets of lower and middle net wealth households while the wealthiest twenty percent of households held mostly financial assets, although this includes property that are held in businesses and trusts (figures 4 and 5).

Higher financial asset prices tend to benefit households with the highest net wealth as they tend to hold most of the financial assets in New Zealand. On the other hand, ownership of non-financial assets were more broadly distributed across net wealth quintiles (figure 5).

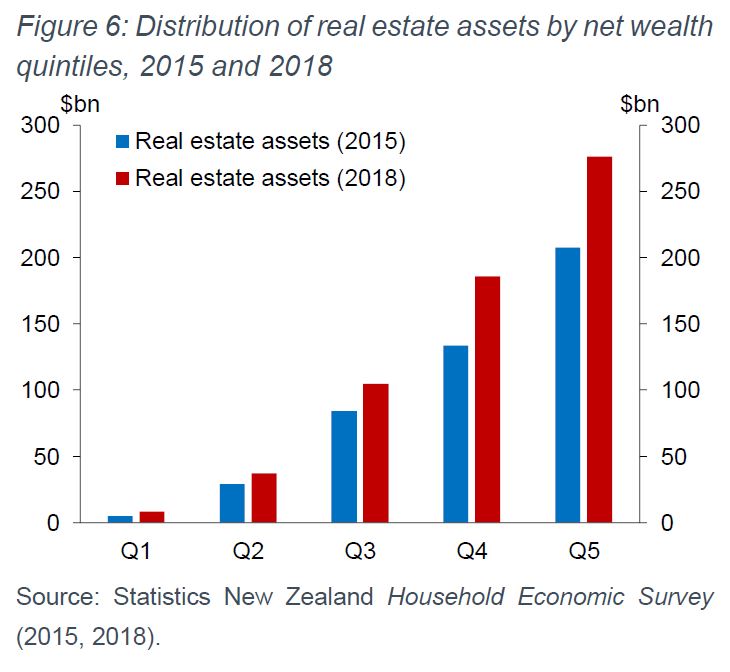

Wealthier households (the top 40%) saw a greater increase in their real estate asset values from 2015 to 2018 than the rest of the population (figure 6).

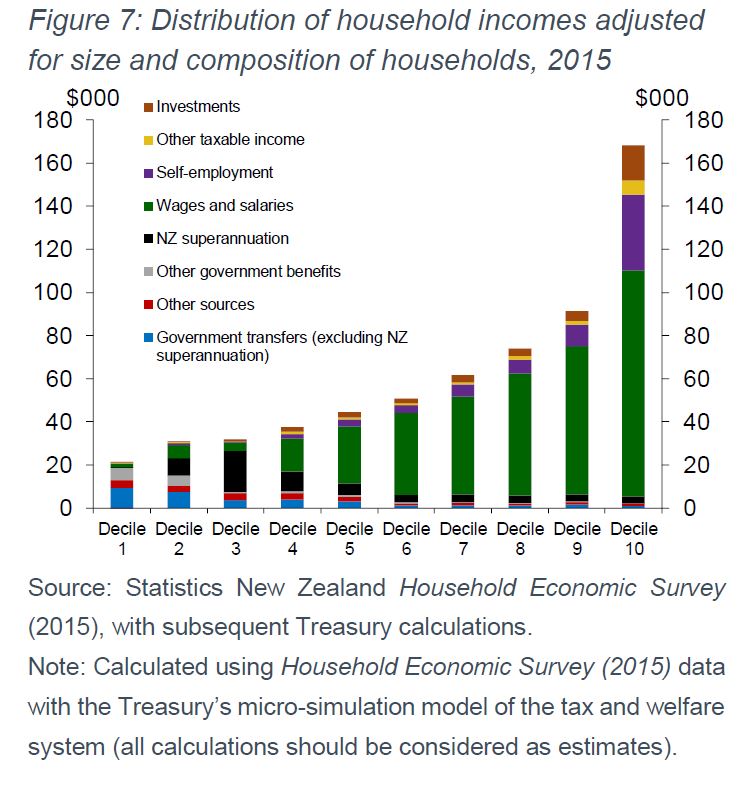

In New Zealand, lower income households tend to rely more on government transfers; middle income households primarily rely on labour income (wages and salaries); higher income households have more diversified income sources (figure 7).

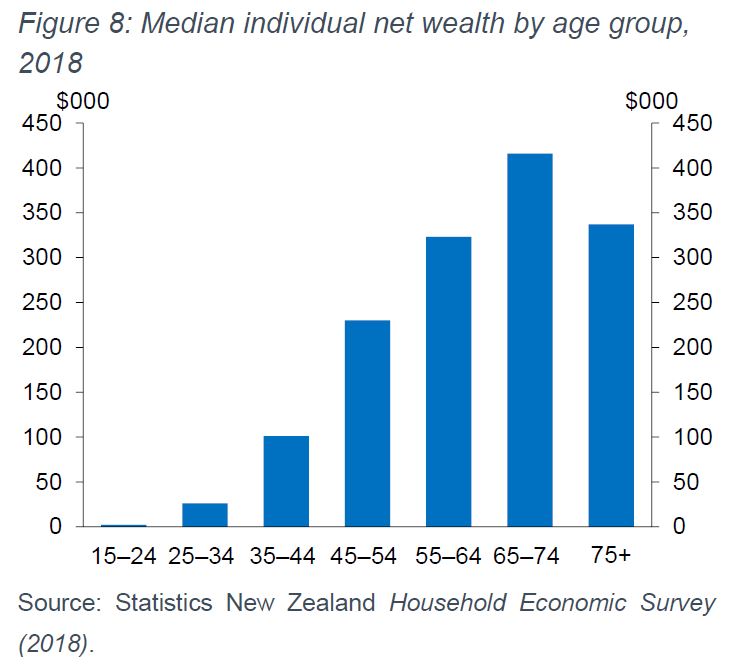

On average, older people are wealthier than younger people, which is consistent with a lifecycle pattern of accumulating savings over a working life for retirement (figure 8).

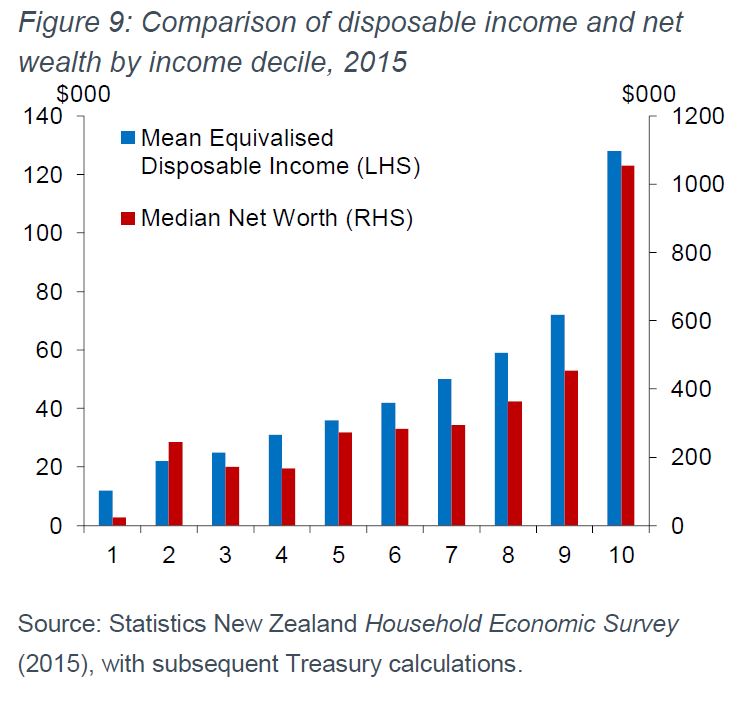

In disposable income deciles 2 and 3, there were some recipients of superannuation with relatively high net wealth (figures 7 and 9). Although their disposable incomes may be lower, older people tend to be wealthier (figure 8).

113 Comments

How much damage can be caused before the army steps in?

The Fed started the rot, they should be first against the wall.

New Zealand is a WINNER Takes ALL Democracy.

New Zealand voted AND Orr is Labour's Man. Welcome to getting what Kiwi's voted for... not really sure what else to tell you dude. You can try again in 2+ years.

O for Orrsome

The Political mood of the Country is rapidly changing bring on a Coup d'état and a snap election

.. the Queen , radiant as a blushing bride to be , will be wed in Gisborne next Summer ... her hero , Clark the Magnificent by her side ... and Neve , darling little bridesmaid ... so cute , oh , won't she be so cute ...

Yes ... at the most opportune time , the Queen will rouse the nation , will reinvigorate our adoration of her ... Jacindamania will reign once again .... SIGH ... ain't she luvverly ....

NZ is a nation of sheeple. They'll voter her back in, and the assortment of dingbats to the left of her

I won't be. No doubt in my mind.

Now this is what you call gross incompetence.

I don’t see why, inequality is not in their mandate is it?

Their mandate. So if the mandate of the RBNZ was to get rid of some old curtains, and they set fire to it (to get rid of it) but in that act, burned the whole house down, that’s ok? Their mandate was to get rid of the curtains only not to make sure the house is ok in the process? Nice. No wonder our tax payer dollars goes to incompetence over and over again, if we are ok with this.

Ignorance is bliss eh?!

Isn’t that ignorance by design?

For who and what benefit?

Written by the government and to the benefit of the existing power structure. This isn't the responsibility of the RBNZ, Orr is just doing his job, and he's doing that very well. He actually even took the care to inform the government on two occasions, both before covid broke out here, that to execute his mandate in a downturn his tools would likey cause inequality and that the government has the power to mitigate those externalities.

'that to execute his mandate in a downturn his tools would likey cause inequality'

Why was he saying that then, yet now he doesn't know if they cause inequality or not?

He said the outcome of UCM and low rates was uncertain but that it's likely to cause an increase in inequality. Later they provided a traffic light warning system and included both inequality and house prices. So while he doesn't know the magnitude, he does expect it to impact inequality and clearly expressed this concern. He went further to explain that government use of its powers to mitigate those externalities was warranted. These are not wholly solved problems but Robertson's response of 'im skeptical of the link between interest rates and house prices' says a lot about his background and experience.

.. it all depends upon one's perspective ... what is " gross incompetence " to you , is merely policy , business as usual , to the current RBNZ & government ... no problem ... let's be kind , huh ...

"RBNZ concludes - based on 'inconclusive' international research - that it doesn't know what impact low interest rates have had on inequality"

Does this gentlemen has any shame left.

If he does not want to act, should say so and not act but should stop insulting average Kiwi.

His arrogance, lie and manipulation is beyond and he should be kicked out in front of the media for all to see- sorry but he deserves no respect.

Yeah and:

“A first-home-buyer may need a higher deposit to get into a property because of rising house prices. That may be offset to some degree by lower interest rates on a mortgage paid over many years".

What a load of bollox! Its not offset. Its neutral. House prices are the ultimate elastic marginal product. There is huge competition. Always has been. (I first bought in 1990 for example). The danger now is that interest rates cannot appreciably go down any more. So the above comment is not true. The only way from here is no change or up!

Correctly said, he is laughing at average kiwi & thinking how single handedly he destroy so many kiwi dreams.

To sum up this gentleman is full of Arrogance, ignorance, and incompetence. But he will be there for next 2 years and may be get extension afterwards.

Tane Mahuta reckons it's all good though...

Lower interest rates have smashed the elderly.

Not the elderly who own investment properties...

Agreed. It is crystal clear what the impact is.

Orr must be blind or eating what ever puppet food they are giving to Biden. Housing (a basic need) is in a huge financial mess from being over leveraged to screw the population over with debt driven profit the only winner. Speculators are just the risk medary for the banks. Its a jenga tower founded on welfare funded debt payments, tax offset (thankfully now gone) and ongoing money printing and low rates all targeted at keeping the moron bubble allive. A mess that's putting our banking system at risk, and thus exposing the average tax payer to hyper or worse stagflation. Yet Orr fiddles while housing, wage earners, and retired savers burn. All under a back to back left wing Govt. Shameful is not a strong enough word for it.

Tooth Fairy and Fat Controller you were voted in to address this s#&t show. Do so, or this is the legacy you will be forever be remembered by.

They haven't seen the international research which concludes that lowering interest rates doesn't increase employment once levels are below -- from memory -- approx. 4%?

Ocr below 2% has little effect as well.

On the surface that doesn't sound correct as employment and interest rates are strongly corrolated both above and below 4%, do you have any more information to help me find a source?

There’s definitely a Tui ad in there somewhere.

How's that greater business investment working out, Adrian?

They haven't worked that out yet or they don't want to and never will work that out.

All this was as plain as the nose on your face well before Christmas, but these buffoons and the others in government did nothing to correct the situation.

I told you so always feels pretty empty and like a failure to make folks see sense, but late last year, I was posting that we were headed for the mess we find ourselves in now.

Central banking is the greatest cause of inequality.

Bitcoin fixes this.

Bitcoin relies on incompetent central banks. If they become competent, bitcoin isn't needed.

If you're a crypto fan, you'll be hoping they remain incompetent.

Central banks will remain incompetent so long as they maintain the ability to print currency at will. The only way to prevent that would be to revert to a gold standard, which simply cannot happen.

Fix the money fix the world.

May I recommend the book The Creature From Jekyll Island?

Fix the money, fix the world.

The world in the absence of a 'numeraire' a standard unit of economic measurement is adrift at sea, and the financial powers that be have no interest in reintroducing one, after centuries of conquering every possible candidate - gold being the last high profile one. Centralized monetary policy is more dangerous to nations than standing armies. Take that statement as literal fact. Tie it to politically expedient governments who buy votes with government spending and a low IQ voter base who vote for said payouts and you have the death spiral of democracy. Low interest rates will devastate the productive capacity of a land better than the scorched earth policies of World War 2. This financial hegemony affects everybody, personally. It is the silent destroyer of worlds, scientifically linked to socioeconomic issues, mental health issues, biophysical issues. You become your economic system. The system has no sense of equity in it. It is abrasive to the human spirit. Something will have to give. It won't be pretty. The change won't come from the invested generations. It will come from those with nothing left to lose. It will happen slowly, then all at once.

Just when you thought Orr and the team couldn't get any worse...

I just imagine that song from Benny Hill playing and the Reserve Bank notables all running very fast, around in circles, going nowhere at pace. It just seems like such a farce. They are just rowing the boat around in a circle, waiting for something to happen. It's the same plan as deliberately blowing up asset bubbles to stimulate a 'wealth effect'...in fact it's not a plan as the exit strategy was never devised. There is a plan but the last page is missing. You distort markets to inflate asset prices...now what happens? It's like a balloon - either you have to keep adding more air (and it eventually bursts), or the bubble deflates. Neither option is palatable.

Is this satire?

It's getting increasingly Kafkaesque, Pythonesque etc

Monty Python does Kafka. I'd pay to see that.

Does Orr realise that without restoring the balance between saving and borrowing, the distortions we are seeing are only going to get worse? We are burying ourselves under an ever growing mountain of debt and he is peering out from under it and squeeking that everything is fine.

Its ok as there's price growth.

Thats the mindset that cause this. Being enslaved under crushing debt is the problem - not the fix.

Was it a 19% rise in house prices last year?

During a time when the economy tanked due to our misguided leaders pseudo scientific interventions.

I mean what could the effects of low interest rates possibly be?

We definitely need more data. And more caviar for our friends in banking and real estate sales.

'However, the RBNZ didn’t go a step further, and calculate the overall net impact of loose monetary policy.'

Couldn't be bothered, there was something interesting on the telly.......

Given the numerous warnings from Orr to Robertson on the very topic of low rates and UCM on inequality, I hardly think they were distracted by the telly. I think we should be asking the finance minister if he has the necessary experience to manage the finance portfolio.

Just so silly – we still have emergency OCR rates – but the emergency has passed.

Resulting economic distortions and poor financial behaviour becomes ever more rampant.

It will be very difficult for this to end well.

Is there anything that they actually do know? They seem to not know anything? They are always waiting for more information? Funny how quickly they acted when they percieved that their ponzi was under threat. An immediate independant review of leadership capability is now absolutely essential before the damage gets even worse.

Com'on, really???

Low interest rates increase asset prices, therefore asset holders (= wealthy people) get richer and people owning nothing (= poor people) get nothing. Outcome: increase in inequality, no fancy graph needed. How can the RB not see this?

And the more they defend the bubbles they created, the more they enrich those existing asset holders. It’s so obvious!!

And they benefit personally from their decisions because they are asset holders. Would they believe that it was a "first class problem" if they held no assets? Personally, this conflict of interests is a grubby episode in NZ's history that will not be soon forgotten. I thought we were better than this, how wrong I was. I now see NZ as being no better than many other corruptly ran countries. Throwing so many people under the bus to further enrich the rich is an anathema to me and many other plebs like me. Hopefully the police will get involved in the independant investigation that is so badly needed.

Its difficult though when its a state entity doing the damage against its own people. And then denying that they're actually doing any damage at all....but then you watch the news and see record numbers of people living in motels and go for a walk down Queen St and view the homeless and realise the people in the ivory tower are dodgy AF!

National saying (JK and BE) that having out of control house prices was worthy of celebration is a point that was vomit worthy and has, in my view, damaged my ability to vote for them for a very long time.

National??? How the heck did you get from the article above, the RB and the above comments to the National party? The article is about the RBNZ & Labour have been in power for 4 1/2 years

There has been a party that calls itself Labour in power for 4.5 years but it is certainly not a Labour party.

I can trash labour as well if that makes you happy Yvil! They just haven't said the bubble is worth of celebration (yet).

We don't have much corruption but we have a huge amount of cronyism.

New Zealand ALSO has the least investigation of corruption in the developed world.. think on that.

If they say it (causation of rising inequality) exists the pressure will be to do something about it. So they problem will never be recognised.

#EndTheFed! (and RBNZ...)

Exactly. What a bunch of clowns.

Yvil, we both know the RBNZ is Gas Lighting here.. and doing an appalling job at it.

Labour and National serve those with means.. or at least those with real estate. Those with nothing aren't their concern, rather they become the police's concern and a middle-class complaint.

That seems to be the developing situation.. then full blow communism by the looks of it.. and I'm allergic to gulags!

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.”

- Upton Sinclair

Duurrrrrr

Central bankers are like a strange cult that is out to destroy the quality of the future of young people while further improving the lavish lifestyles of the already wealthy.

What a morally corrupt group they have collectively become.

#shame

Hear, hear! And to compound the problem, they are un-elected bureaucrats who hide behind the so-called "independence of the central bank" concept to excuse themselves from any accountability for their misdirected actions.

Unfortunately you are correct and the backlash will be something like the Trump cult.

“With lower interest rates, borrowers are generally better off and savers are worse off, but this may be a matter of gains and losses for the same groups of people,” the RBNZ said.

No they are NOT the same people, nobody (I hope) borrows money at 2.5% and then deposits it back into the bank for 1% interest. Are the people at the RB on meths ?

It is now the only logical explanation!

“For example, a family with their own home could earn less income from money in the bank, but the family’s wealth may have also increased because of rising house and share prices."

A family with their own home most likely has a mortgage, not a stack of extra money deposited at the bank, so they win by having a lower interest rate PLUS by having the equity on their home rise

Low interest rates very clearly benefit people with large amounts of borrowing. They also boost house prices - so wealthy people with large mortgages and wealthy homeowners benefit = increased inequality.

The QE that is used to support low interest rates also clearly drives money into stocks and shares, boosting the price of these assets. So wealthy people who own lots of stocks and shares (or have large pension funds) make a fortune = increased inequality. It's not rocket science.

So RBNZ won't conclude the obvious, but they will state that “lower interest rates also encourage greater business investment and more jobs, and typically result in a lower unemployment rate." This is actually much less certain - the evidence to support this is inconclusive.

“A first-home-buyer may need a higher deposit to get into a property because of rising house prices. That may be offset to some degree by lower interest rates on a mortgage paid over many years."

A FHB's saving for a deposit has been slashed by reducing interest rates PLUS the deposit needed increases much faster than his/her savings, he loses doubly

Plus they pay RWT on any interest paid on the interest (minimal) they receive.

If the cycle reverses though, interest rates rise and they receive more interest, and it will decimate asset prices.

Most likely they're saving via shares or index funds though, which have increased a lot.

LEVELS OF COMPETENCY:

1.Know what your doing before you do it

2.Dont know what you're doing, but pick it us as you go

3. Don't know what you're doing, don't learn as you go, but figure out the consequences after.

4. Don't know what you're doing, don't learn as you go, clueless as to the consequences after.

5. Don't know what you're doing, don't learn as you go, completely clueless.. but put together a detailed report about why being clueless is perfectly reasonable.

Thank you RBNZ for showing me there was a level of incompetence below 4.

“Lower interest rates also encourage greater business investment and more jobs, and typically result in a lower unemployment rate."

I'm a business owner and also a multiple property owner and I can tell you it's much more work and risk to run a business than to own real estate, especially when asset prices rise so fast.

Conclusion, lower interest rates encourages investment out of business and into property

Really! The poorer people within our community are being left further and further behind.... the are hit by a constant barage of information bia news channels about how high house prices have gone and that any increased costs in housing that effect a landlords profit will be passed onto them as tenants. We also have big problems with gang culture and associated crime. All this being driven by more and more inequality primarily driven by ridiculously low debt interest rates. It’s happening all over the world and will get much, much worse. Incidentally, non of the other leaders or central bankers can see it either.

There's no point seeing something that means your entirely philosophy and point of existing is a fraud!

"RBNZ yet to work out the overall impact of low interest rates on inequality"

What hell do they do in office..and what is it that he does not understand and need to work on, which every knows except the master.

Remember Karma is a bitch.

I cannot see a single reference to the rising present values of discounted cash flows associated with liabilities for insurance companies and individuals.

ACC announces $8.7 billion deficit for year as interest rates plummet

Falling interest rates

As was the case in 2018/19, interest rates continued to decline, influenced in part by COVID-19. Falling interest rates affect ACC in two keys areas: the valuation of the OCL and investment returns.The OCL is our assessment of the net present value of how much ACC needs today to support already injured clients for as long as they require it. Falling interest rates result in a lower discount rate being applied to our OCL. In 2019/20 this contributed $7.3 billion to our deficit. The single-effective discount rate1 applied to our

OCL has an average duration of 20 years. This rate fell to 1.86% at 30 June 2020.Investment returns for the year were 7.59% ($3.4 billion) after costs. Two-thirds of our investment portfolio is in fixed-interest products. This acts as a partial hedge to the interest rate exposure present in the OCL valuation.

In the past two financial years ACC has recorded $14.6 billion in deficits. These deficits have primarily been driven by economic factors outside ACC’s control. These factors affected the valuation of ACC’s OCL by $16.4 billion.

Although these deficits are not cash losses, they do have impacts on the funding ratio of the levied and Non Earners’ accounts, which in turn affects levy and appropriation requirements. Link: https://www.acc.co.nz/about-us/corporate/

In March 2017, former Treasury and Federal Reserve (Fed) official, Peter R. Fisher, delivered a speech at the Grant’s Interest Rate Observer Spring Conference entitled Undoing Extraordinary Monetary Policy.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1…

Dear RBNZ

Just ran across this from Peter Schiff recorded after the stock and RE bubble bursts in 2008/09 - hope it helps:

https://www.youtube.com/watch?v=WN_8A3gUnVY

Cheers

Rob

So sensible and grounded in reality. Totally different to the buffoons in Wellington.

The clowns at the RBNZ are now joking at our expense, am I right ? Or is their incompetence really so deep ?

They're laughing at us

Well of course it's inconclusive because they don't know what the solution/answer looks like, they only know enough to ask the question.

Because for example, in jurisdictions that have less restrictive land-use policies, lower interest rates have not caused house prices to rise so not only does it not cause further inequality, but also gives more disposable income to spend on other things.

Go figure?

We have witnessed the Mugabe-tisation of the Reserve Bank of New Zealand. They have ensured that multiple property owners have taken enormous wealth out of the system for themselves and they have also burdened new buyers with debt unseen before in New Zealand or nearly any other country for that matter. The RBNZ's chosen winners locked in their tax free capital gains. They have got rid of run down shacks for millions. They are now vastly wealthier than they could ever have imagined. The clock cannot be turned back. The damage is done. If a crime has not been committed, then the closest thing to one has!

Can that money be clawed back from the looters once we have confirmation that the central bank and retail banks have colluded to run a Ponzi scheme with those at the top cashing out and those coming in at the bottom left holding the steaming bag?

Its's as inconclusive to Orr as climate change is to oil companies..who also can find studies to make inconclusive reports.

Its pretty obvious his goal was to be inconclusive..

RBNZ has no mandate to even consider the gratuitous transfer of wealth much less take any action, that's governments job.

Government have stated "no new taxes."

What is 'financially stable' about an ongoing central bank drive to enrich asset holders at the expense of everyone else? Eventually the 'everyone else' come for you with sharpened pitchforks!! Not good for stability!!

Asset holders are the majority. What if they sharpen their own pitchforks in return?

The renters can destroy ALL assets and have nothing to lose.

Burn down your parent's house? Destruction just for the sake of it. It's hard to feel sorry for you Groat.

What reactions. Did Jenee expected this reaction on the article or is she surprised.

Did not realised that Mr Orr is so infamously famous.

Is this reaction only on this website or does it reflect the overall sentiment in NZ !!

A Ponzi caused by the Government colluding with the Fixer of supposedly "Fair" and equitable interest rates is still a crime in my belief.

If not, then some people have been totally and inexplicably.. screwed over...and over and it is not worth "Working slavishly" for..........funny munny. ...created out of unbelievable debt. And tossing to tossers in Government and our so called..Land Lords.

Stop working. I did....it is a Slave Market. And They have you by the Short and curlys. Socially and Figeratively speaking. It is a con job.

The biggest in History.

Most of middle NZ are very content with Mr Orr's actions.

Those in poverty are miserable and oblivious to his actions.

The only ones who care are those younger kiwis who are locked out of housing and do care. And the very occasional enlightened homeowner in middle NZ.

It's probably no more than 30% of NZ'S population

Disagree. Many parents are s*** scared about what the future holds for their children who remain (for now) in NZ.

100% this /\ /\

Everyone I know is concerned with the way house prices are rampantly disconnected with the fundamentals. Even those that are investors are worried. How can anyone believe this can end well/be good for our country…..

It's not just house prices, but the inequality that flows from there.

It won't be a 'kiwi' society anymore when the haves and have-nots continue to be further apart than ever. I can't think of anything good that will come of it.

Don't understand what's the commotion about. I don't see a reason to believe low interest rates causes inequality whether through common sense or sophisticated analytics.

Stop pressuring RBNZ into becoming your personal political party- they are meant to be independent.

The Gini coefficient measures income distribution but can be blind to asset distribution.

It's truly fascinating seeing the dunning-kruger effect in action with each one of your gemlike posts, clown world.

It's amazing you can keep talking without knowing what you're talking about. No surprise you're where you are my dear sample. The Gini coefficient is the gold standard in measuring inequality and you think you know better.

On the first page of the Analytical notes in fine print

The Analytical Note series encompasses a range of types of background

papers prepared by Reserve Bank staff. Unless otherwise stated, views

expressed are those of the authors, and do not necessarily represent the

views of the Reserve Bank.

They are certain the Maori economy is the future, climate change must be dealt with by Orr's iron fist, but just not quite sure about this.

Orr need to go back to high school to get some basic stuffs right....

I said it before October and I say it again, be careful what (who) you vote for and scratch a bit deeper below the surface. Unfortunately people voted for the smiles and glamour, not substance. And now they know what a hangover feels like once the party comes to an end....so I hope they think a bit deeper next election.

"Half of all households held 94 percent of New Zealand’s total net wealth."

Inconclusive.

No inequality to see here. Move on, theres a good chap.

Recoverable Proxy is an idea many might think fitting. Imagine we remove our support today rather than wait.

From the sentiment, we would already be in the new paradigm.

Conservative approaches in gubormint are out of balance with the pace of technology. Technology wins, 70% of time, all the time.

It is pinnacle of incompetence! It is incredible that such incompetent people are running the show!

Unless, it is all part of the plan - in that case they are doing stellar job!

What exactly is equality. How is it defined? Is it strictly measured in financial terms?

Is there more overall equality now, than say there was in the 1950's?

It's about options. Realistic options for young people to plan their futures in homes where they can raise their families. I raised my children in the early 90's. We lived with dignity and hope on one and a half fairly average wages and no Govt hand-outs in sight. Saved money, read them books, gave them basic healthy meals, warm baths and put them to bed with love in a warm dry house that we owned. Is that too much for young hard-working people to ask for?

That's a good answer, Mountie. Although some would say other inequalities existed then (and in earlier times). That perhaps don't exist as much today. Perhaps there is more inequality now overall, or some of it has been transferred to different groups.

Interest.co Can we get Jenee to ask Adern for her definition of equality?

Its when one group of people own lots of assets and another group doesn't. Then a state entity makes one group with assets wealthier while rendering the other group into a new form of slavery aka neo-feudalism.

That's the answer you're after eh Dave?

Dear RBNZ Open your eyes.

I'll DM you with an address to send my cheque to

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.