By Bernard Hickey

Reserve Bank Governor Alan Bollard has delivered a speech lauding the resilience of New Zealand's economy through 2011 in coping with the twin shocks of the Canterbury Earthquakes and the European financial crisis.

However, in the speech to the Canterbury Employers' Chamber of Commerce in Christchurch Bollard said the earthquakes that hit Christchurch just before Christmas had delayed the Reserve Bank's forecast for the main rebuild into 2013.

The bank now also estimated the total claims from the earthquake at NZ$30 billion. Before the December quakes the bank had estimated NZ$20 billion worth of damaged property would be rebuilt. The much higher claims cost relates to business interruption costs, relocation costs, claims processing costs and other non-rebuild costs.

Bollard said the later start to the rebuild may mean the contstruction is compressed into a shorter time frame, worsening inflationary pressures.

"Our working assumption before the December 2011 aftershocks was that around NZ$20 billion (in current dollars) of damaged property would be rebuilt. This would be equivalent to around 10 percent of GDP – a very large shock indeed," Bollard said.

"The nominal cost of rebuilding could be higher as construction costs and prices for materials may well increase over the coming years, and as reconstruction incorporates quality improvements. Furthermore, we estimate that the total cost of claims stemming from the earthquakes could be much higher – around NZ$30 billion – as this includes claim handling expenses, claims for business interruption, temporary accommodation, consequential loss and other non-rebuild related costs," he said.

"Recent aftershocks are likely to have added to nominal insurance costs, but the costs of the rebuilding in real terms may not be significantly affected (i.e., you only rebuild a house once). In addition, the longer the delays to rebuilding, the greater the human cost and the risk of leakage of businesses and residents from Christchurch to other centres. Delays could also mean the rebuild is done more quickly, albeit starting later, so exacerbating inflationary pressures."

Yesterday the Reserve Bank held the Official Cash Rate at 2.5%, as expected, and said inflationary pressures were reassuringly low. Economists said the Reserve Bank's relaxed stance on inflation and a slow domestic economy, caused partly by quake rebuilding delays, meant the Reserve Bank was likely to hold the OCR until the final quarter of this year. See our article on the RBNZ decision.

Rebuild delays

Bollard said the Reserve Bank had continuously updated its reviews of the Official Cash Rate to take into account the impact on economic activity and inflationary pressures of the earthquakes.

"We cut the OCR in March 2011 as an “insurance cut” following the February 2011 aftershock. The deepening Euro crisis and ongoing aftershocks in Christchurch have led us to leave the OCR unchanged over seven successive reviews," Bollard said.

"Reconstruction, is projected to eventually provide a boost to demand similar to the mid-2000s housing boom. Residential and non-residential investment will lift growth sharply. Spare capacity and labour will be absorbed rapidly, and inflation pressures will pick up from current low levels. We will need to keep monitoring this to judge whether the level of the OCR continues to be appropriate," Bollard said.

"The outlook for rebuilding in Canterbury remains subject to a high degree of uncertainty. In the January OCR Review, we took account of the latest aftershocks and pushed out our assumption of the rebuild by a few months, with a gradual lift in activity over 2012, consistent with demolition and repairs to housing and infrastructure getting underway, with reconstruction getting underway in earnest in 2013," he said.

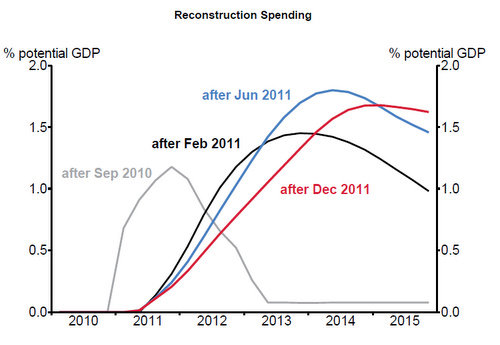

See here a chart published in the speech showing the Reserve Bank's projections of earthquake rebuild spending over time.

34 Comments

And are residents the only ones expected to feed the govt the GST on the rebuilding..?

Gee - he should have consulted Chris_J ages ago if he'd wanted to get these cost predictions/forecasts right first time around.

Went and visited elderly family in Cashmere on the weekend whose house has significant damage. They still haven't been assessed for damage done last February and they said most of thier surrounding area hasn't. They are on the Port Hills. The $30bln 'estimate' may still be found to be short.

PDK/Walter/scarfie - you may be interested (but not surprised?) to hear that a house across the street from the rellies, was built on a sustainable/eco friendly building basis by a young European couple, bout 3 years ago. It was the only house in the street untouched. The house in front of it collapsed, and those that are still living in their houses in the street are living in reduced living space.

I said $30b back in March.

The truth is that the RBNZ nor even the insurers have a grasp of what the likely cost will be.

I know for a fact that the insurers are continuing to be stunned at what quantity surveyors are bringing back to them for the rebuild cost of full replacement (uncapped) residential policies.

One of the most damaged types of residential buildings are the large pre 1940 2 storey dwellings. These are coming in at $3500 to $4000 plus per square metre to rebuild.

Whole streets of these types of properties in Merivale, Fendalton and the City are being written off and on average they can have replacement cost of $1m plus for a modest size house which may have only had a market value not much more than half of that including land.

Even typical large bungalows and villas with high studs which are write offs (making up much of Richmond, St Albans, City and Linwood and other badly affected areas) are coming back at $350,000 cost for a smaller house and half a million plus for larger ones.

These are all miles above the actual market value. But that is irrelevant, because the insurance policies for full replacement clearly state if the building cannot be repaired then they must build new, like for like.

I actually think that the insurers did not know what they were insuring, and were only too happy to take the premiums without taking adequate consideration for the total value of assets they insured.

That pricing seems crazy....but there was a shortage of builders before Chch.....so right now I assume they can charge anything they want....

regards

We have just finished building a house in Auckland and I was amased at how little help, either from the builders, designers or council, is given to make houses earth quake proof and eco-friendly. It was all down to us and didn't make things cheaper. We do have a house that will wobble nicely and is capable of being independant in the event of a disaster but it's no thanks to anybody but us!

Chris's prices on the building look pretty acurate to me too - without any frills!

I think the idea is you use a professional or do the work yourself.....so in some form you pay for it.

The EQ bit is adequately shown in the regualtions and guides available at low cost, even in the library.....its all there....in some cases you odnt even have to think, house frames come ready made to those standards...........

"Builders" know diddly for the most part.....they can hammer a nail....

"designers", well dont know who you talked to but it couldnt have been someone with my background for instance....I have a Beng (Hons) in Building services with an speciality of energy efficiency/passive techniques.......

Council, well again most are ex-builders or tradesmen.....they install they cant do much more....also the council wouldnt want the liability of something not performing....

Most architects are similar and a decade ago it was awful trying to tell them how to do passive desing, they didnt want to listen.....really they were the lead professional in a design and actually that was a mistake....egos ruled...I got out.

btw, now do IT because I earn twice as much and have better job security....ppl expected to pay a tradesman's or less rate for specialist advice.....which they ignored mostly..

regards

A friend has 3 insurance policies spread across 2 insurance companies. One of them www.racv.com.au (for vehicle and house contents) is one of the smaller independants with no presence in New Zealand, and is equivalent to AMI in that it concentrates on one market. Friend has just been notified by racv that their contents insurance will be increased from $240 pa to $1750 pa on a $70,000 sum insured. Reason for 600% increase is the re-insurers have upped their costs substantially due to the number of adverse events in Australasia.

wow........time to get new quotes......I shopped around recently and the house is threatening to go up quite a bit, but nothing else seems much impacted.

regards

I don't think anyone has a real grasp on the numbers. If we try to calculate the FULL REPLACEMENT cost of properties that have been lost it becomes extraordinary:

The vast majority of the large expensive houses in the city are write offs.

I would estimate that there could be as many as 500 houses with rebuild (full replacement) costs over $2m each which are write offs. (say $1.5b)

There could be thousands perhaps 2 or 3 thousand that have rebuild costs above $1m (we have one and 4 others that are very close). (say $4b)

A good 10,000 probably have rebuild costs at between $500k and a million (say $7b).

I would say there's 20,000 at $300k-$500k (say $8b).

And a few smaller properties at under $300k say 5,000. (say $1b).

So that's say $22b just for written off houses. Now not all will have full replacement, and not all will battle to get their full replacement and will give in to insurer and Government offers at discounted amounts.

Now let's look at repairs.

I would say 40,000 repairs over $100k repairs at an average $150,000. (say $6b)

Perhaps 60,000 repairs $40-100k. (say $4b)

Perhaps 30,000 at under $10,000 (say $200m)

A total about $10b. $32b so far.

Total chattels (mostly from written off houses) say $2b.

Land damage through EQC, say $1.5b in red zones. $1.5b elsewhere.

Infrastructure damage. Mostly uninsured I imagine, but would be many many billions in real cost I assume there was $2 or 3b in insured amounts? (Probably another $10b if you wanted to repair everything to prequake standards, which will never happen (ie not insured and won't be spent - there are too many roads still barely passable to worry about a few bumps in virtually every road in town).

Business interruption must be at least $2b plus? (depending on levels of insurance).

Running total about $42b

Churches, schools etc, that must be $2-3b plus in insured amounts (Ansvar alone lost $700m)

Loss of commercial contents/stock, must be $2b plus given the scale of "dirty" demolition with contents.

Commercial property. Certainly 100ha of commercial space is written off. But it's hard to judge as a lot of buildings are still being used that ultimately will be demolished because they are sloping, could it be double or triple that?

So if it is 250ha (2,500,000m2) with an average replacement of $2500/m2. That's $6b. But this one is just a pretty rough guessimate. My gut feeling is that it could be higher, when you consider the number of $50-100m+ claims that there must be.

FINAL TOTAL $53b.

And I've probably missed something? But who knows what the exact number will be. But I am fairly confident, given the scale of demolition that it is significantly above my original estimate.

Of course much of that amount will be bargained away in negotiation between the insured and insurers, but the total amount will stilll be astonomical.

EQC are likely on for $12-14billion (based on my previous guessimates).

Why don't the Government wake up and realise that they can't afford CERA going around demolishing fixable or relocatable buildings in either the red zone or the CBD?

If we accept $3500 to $4000 per sqm as a typical build cost for what are very average properties, we're accepting that residential building is uneconomic in the New Zealand. Good news for Australian real estate agents and landlords, not so good for the rebuild Pollyannas.

$3,500 to $4000 per sqm is for a substantial quality building with high stud. I am talking about rebuilding Fendalton/Remuera style pre war high end housing.

You can build to a reasonable standard at $1500/m2 for a conventional modern house.

Of course prices will only rise for existing stock when the reality of replacement cost flows through to the market.

Yes indeed 4k is really high end. I imagine 1500 would very basic low end fitting Chris and single storey?

Word is Marryatt is rejecting $68,000 pay increase. So good of the poor fellow.

Most of the settlements so far are not being spent on rebuilds and won't be.

For investors like ourselves it makes no sense building new dwellings to rent out. We may invest some money back in ChCh but I know many are seeing the insurance settlements as an opportunity for early retirement and justifiably so with so many obstacles and obstructions provided by the CCC, CERA and the Govt.

It's hard work for ChCh to recover from where it's sunk to now.

I would agree with you totally, Hugh, that the cost of building in New Zealand is divorced from all economic reality. And that's not just in Christchurch, but is up and down the country too. But how can we bring the cost down, which is another way of saying what is making it so expensive?While the price of land is a big component of that expense, there's got to be more behind it than just that.

My worry is that once the rebuild gets underway in Christchurch this is going to have major cost ramifications for new builds and renovations up and down the rest of the country. Will housing construction inflation be so severe that it will actually depress new builds and renovations been done in other parts of the country? Will this shortage of new housing stock actually drive the price of existing houses even higher, especially in high demand areas like Auckland?

I’m also very curious to get both your opinion, Hugh, and Chris-J’s, on what effect the rebuild in Christchurch will have on the profitability of the construction sector in New Zealand. The popular view is that they are on the cusp of a bonanza to rival a gold rush. But is the popular view correct? Well Fletcher’s for example make the large profits everybody expects them to, or not? If construction in the rest of the country actually falls due to Christchurch, will the amount of building activity in Christchurch be sufficient to make up for that and more?

So to be clear you are saying too high house land pricing is the major / primary driver of our "problems"?

regards

In many countries Real Estate/ property isn’t a major sector of the economy. Here it is – one of the reasons why prices are inflated. I think the government doesn’t do enough and therefore we are becoming increasingly a nation of tenants in competition with foreign investors.

Please read more: 24 01.12 – 4:00pm

As you may discerne, Hugh doesn't believe the monetary system is debt based, or that increasing aggregate debt drives inflation (including house price inflation).

The following is a good discussion of housing market influences, including some discussion of things which property sprukers tend to point to...

http://www.debtdeflation.com/blogs/2011/02/10/a-motley-crew-interview-on-australian-house-prices/

As to if or not the Christchurch rebuild will drive a boom, that demends how much new debt is being taken on. I don't think this will be huge, as many people who lost homes in the earthquake would have had a mortgage already.

If ppl stay around to build.....what happens overall if (only) 10% of ppl take their insurance payouts and leave? Bear in mind those 10% are probably the most mobile and good earners.....I think such a effect will be serious.....if those ppl are also young families thats a longer term impact....

Actually what options do they have? ie if they have lost their house, can they get re-insured to build new right now? or insured if they buy an existing? my understanding is right now that isnt the case? hows the job situtaion for them?

If that is the case, to me that is the death knell of Chch....

regards

What options? My generalised observations from the residential red zone:

1. Retirees are using an option from their insurer to buy an existing house outside Chch, and in many cases outside Canterbury, often to be nearer family. If you HAVE to move, it makes sense, and you can leave the EQs behind.

2. Working age people are buying existing houses in "safer" areas of Chch, or outlying towns, or leaving Canterbury altogether for Akld or Oz where they are not limited in their options by insurance, e,g,tenants and those taking Govt Option 1.

3. People on western side are taking advantage of strong property prices to sell to eastsiders, and leaving NZ for perceived better prospects in Oz.

4. Generally an existing property can be sold with its insurance to the buyer, no additional risk to the insurer. A new build (e.g. us) is a bit of a gamble, our building firm carries its own contract works cover, and insurance for the finished house is an issue dealt with when the house is finished. Insurers will not write such a policy until then, so you have to have a bit of faith in the future, as does your banker if he/she has much skin in the game. That bit of uncertainty is a big problem for most people.

Just my 10c worth. Always interested to hear others' perspectives.

Nic, if there was no mortgage credit facilities at all, but urban planning was rationing the supply of land for development, prices would still rise faster than most young people could save money, and almost exactly the same cohort of the population would be locked out of home ownership. South Korea is an example of conditions close to this, in the 1980's.

The difference is that national savings increased rather than debt, as young people worked and saved frantically, delaying marriage and childbearing, with consequences for demographics that will last decades.

On the flip side of this, it doesn't matter how low the Fed made interest rates, or how easy credit got, or how much mortgage securitisation was done by Wall Street, the housing markets in MOST cities in the USA did NOT bubble, because they had no urban growth constraints. An absence of urban growth constraints "proofs" a housing market against bubbles and unaffordability and intergenerational inequity. Bubbles in about 6 States, did ALL the damage to the US economy that we have seen. These bubbles also provided ALL the "money go round" revenue and fat fees for Wall Street. Michael Lewis points this out in "The Big Short" - all the activity was focused on mortgage markets in less than 6 States.

Also worth noting is that Britain, since their 1947 Town and Country Planning Act, had the most cyclically volatile house prices in the world, through decades of widely varying fiscal and monetary conditions. Each cycle involved a bigger "price" response and a weaker "building" response, and the latest cycle involved a "building" response about a quarter of the level of a typical 1960's building response, although actual SHORTAGE of housing is a national crisis.

NZ is simply going the same way, without the excuse that a U-Boat peril once exposed an inability to feed our population unless we preserved most of our fertile land from urban encroachment. Of course Britain has about 20 times as many people as us and slightly less land.

Hugh Pavletich is RIGHT. And there is no lack of academic support (links to be posted in a follow up comment).

Check out THESE collations of lists of people and research that “GETS IT”, and ask yourself if the problem is not entrenched bureaucratic iron triangles that simply will not listen, will not learn, feathers its own nest, and follows ideology rather than facts and reason.

http://demographia.com/db-dhi-econ.pdf

That's not academic support. That's HughP trying to pust his sad little barrow. Cherry-picking numbers which were just a temporary phase on the continuum.

How old's the planet PB?

Just askin.

You're just a straight out eco-Nazi.

If that's not "academic support", you're Joe Goebbels reincarnated.

I am not going to waste time debating you any more, eco-Nazi maniac.

You make a lot of statements of supposed 'facts' but offer absolutely no sources. Some of these claims are frankly ridiculus, like that there is a shortage of housing.

Who was the last homeless person you met with more than even $2000 in financial assets? There was a program on TV recently highlighting the number of properties sitting empty in the UK, and how they might be reported to council housing schemes attempting to use utilise them. I think this typifies how credible your claims are about nearly anything.

Is there any justification for the logic that anything which can't be explained by a Michael Lewis can be explained by Hughs theory of planning. Thats a pretty incredible claim. Why did the crisis in six US states demolish the finance company sector in NZ if this is true? Especially how did this happen if debt is not relevant? Was there some sudden change in planning regulations around 2008? What caused the finance company sector in NZ to collapse if not. I doubt Michael Lewis is even claiming this in his book. Its certainly not Keens analysis, which looks at the whole US finance system.

I am not actually claiming that urban planning is irrelevant, but it has a far smaller influence than finance. This is supported by evidence of the correlation between various statistical quantities by Keen, but I don't expect to see any similar approach from Hugh. Just more cherry picking examples and pointing, so his approach can not in any way rationally motivated, its purely political and exactly the same approach as any housing spruker.

I personally favour only one kind of planning regulation, regulations which have democratic support from the constituants in the region. I hope Hugh has the sense to allow others a voice during the public meetings. Even those people he doesn't agree with.

I have spent a lot of time actually reading most of THIS stuff:

http://www.performanceurbanplanning.org/academics.html

A lot of it, I had already read before that page was created anyway.

I am sick and tired of know-it-alls with certainties that are nothing more than opinions formed by themselves and ignorant chattering classes, based on their own biases and preconceived notions re "class" guilt etc.

I have made dozens of comments on interest.co.nz stating sources. If you want to actually learn something, start by reading everything on the linked page above, by Alan Evans, then everything by Paul Cheshire.

Yes, there can be empty homes in Britain, for which the prices remain out of reach to most of the buyers who SHOULD be occupying them, such as the disporortionate number of people under about 40 who do not own a home. One of the classic symptoms of an urban land price bubble due to regulatory interference, is empty properties, both housing and commercial, for which the prices simply refuse to drop to meet the market.

In markets with low, stable land prices due to low regulatory interference, the market "clears" a lot more rapidly.

The crisis in US States had nothing to do with the finance sector in NZ falling over, that was already happening due to our own economy's distortions.

The changed planning regulations have been incrementally building up in their effects since the 1990's.

Look, I need to be sympathetic with people who have not yet made the effort to look into the whole picture. Mainstream economics is NOWHERE regarding land economics and planning. They can't even see China and India having a massive bubble right now, which will be "Asian Crisis 2' when it bursts, only bigger. These bubbles relate to "planning gain" being excessive as the result of corruption. In the 1st world we call it "urban planning".

Alan W. Evans says this in "Economics, Real Estate and the Supply of land" (2004):

".....few economists have any interest whatsoever in planning. Their whole training leads them to ignore matters related to land and location, so they tend to consider only those factors conventionally considered "economic" - investment, training, labour relations, management, etc....."

Evans should be a celebrity now, as having written 2 books in 2004 that set all the shortcomings of the econ profession on land issues straight.

I certainly got a bit burned near the end of my last major DIY project, the costs for materials have made me stop any future signficant plans.

Hmmm...yet owning forrestry seems a poor investment....so there appears to be no money in growing wood....certainly what I buy is also of poor quality.....so I assume NZers get the rejects no one else wants at prices no one outside NZ would pay.

I notice that powertools are hugely cheaper in the USA....$450USD for something I paid $1150NZ for and that was on special from $1580....new blades, $45USD, here $300NZ....like WTF?

Same with finishing (paints, taps etc).....its way expensive...too expensive.......then taking my in-laws bad experience with a recent house build and I can see labour is over-chargeing and doing a poor quality job.........so land prices are wrong? sure its over the top but the entire industry I think has got indolent....

Kitchen units.....I am making a bamboo kitchen, the bamboo is cheaper to buy per sq m than to buy a "cheap" Bunnings/mitre10 kit....so I can make a unit for say $400 from bamboo for the same cost or less cost as buying a kit made....this stirkes me as odd...

So I conclude that what we see is ppl/companies pricing on what they believe the market will stand and not at a fair price.....

"gold rush" I dont believe so....when I can get and see significant discounts off tools, that I would have expected to see being bought up for the forth coming work I really wonder......I suspect that Placemekers etc bought wholesale expecting a boom and it just had not happened....I dont think it will.

regards

I have noticed (as a DIYer) that there is an increasing discrepency between the price of mass produced junk products and 'traditional' products (like raw material parts). Prices really add up when you look at the price (for example) of small metal brackets at the hardware store that might cost $2-$3 retail, but they're just stamped metal. Likewise the pack of four plastic GIB 'gorilla grips' that let you hang things on your wall - these typically cost about $8. No connection between production cost and retail cost there whatsoever.

It's like people are becoming accustomed to paying Chinese junk prices (like a complete power drill with battery and wall charger for $28, or a violin bow and case for $40) when other things are so overpriced by comparison.

Need a straight edge? You can pay $20 for about 1.2m of box aluminium tubing, or you can pay LESS and get a 1m long aluminium Chinese spirit level of the same size complete with storage pouch.

I don't think chch will have much effect on rest of nz. There won't be a boom, there will be a moderately paced recovery which won't have major inflationary impacts elsewhere.

Development is already largely unfeasible in auckland, so it doesn't matter what happens in chch building in akld is going to be anemic for years unless auckland land prices corrected by 20% plus.

And the state isn't building houses.

Who knows how many architects, surveyors and builders will be able to survive the next few years

How does this sit with what really plays out here...who is looking after the publics interest...is the property bubble in the public interest...the banks think so!

The Treasury will on Friday publish plans for a radical overhaul of financial regulation that will hand the Chancellor new powers to take charge in a crisis, rein in the might of the Bank of England, and provide extra protection for consumers.

deleted

Rant removed.

Bloomberg reported Bollard later told reporters this:

“The market thinks rates are going to be unchanged right through this year,” Bollard said. “We’re not uncomfortable with that. As we see the numbers at the minute, it seems to be a reasonable deduction to take from that.”

http://mobile.bloomberg.com/news/2012-01-27/bollard-sees-slower-new-zea…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.