Here's my summary of the key events overnight that affect New Zealand, with news - unusually - from Peru.

But first from China, their central bank is expanding an unconventional easing program to boost bank lending, stepping up its repertoire of monetary-stimulus measures to arrest the country’s economic slowdown, but also taking on more risk itself.

The PBoC will let more commercial lenders use loans as collateral to borrow cheap funds from the central bank. The commercial banks are then supposed to use the money to steer loans to parts of the economy deemed crucial for China’s growth, such as small and private businesses. It's a variation of the Western QE programs, and like them it will expose the central bank to commercial risk.

Local markets like the initiative with Shanghai stocks up strongly on the announcement. Their index was up +3.3% yesterday.

In Peru, the annual meeting of the IMF and World Bank has revealed an interesting frustration with the US Fed. Finance ministers there have told their American counterparts that they should just get on and raise interest rates if it is justified by US conditions. The Malaysians even said, if EM countries have borrowed too much, the Fed waiting so as to ease their burden won't solve anything. It seemed like a unanimous message - just get on with an increase.

In New York, the UST 10yr yield benchmark is unchanged at 2.09% however.

The US benchmark oil price is lower today at US$47.50/barrel, and the Brent is lower as well at US$50.50/barrel. It seems the US shale industry has reshaped the global oil market permanently.

The gold price has continued its strong run in New York, gaining another $10 to US$1,167/oz.

The New Zealand dollar starts higher again today. It is now at 67.3 US¢, at 91.3 AU¢, and 59.2 euro cents. The TWI-5 is at 71.2 in what is now a three week continuous rise and we are at our highest level in three months.

If you want to catch up with all the local changes yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here »

Daily exchange rates

Select chart tabs

14 Comments

In New York, the UST 10yr yield benchmark is unchanged at 2.09% however.

In Peru, the annual meeting of the IMF and World Bank has revealed an interesting frustration with the US Fed.

They have company.

We start with several suppositions that in an academic setting are perfectly reasonable and complimentary: the Fed can “print money”; money printing amounts to “more money chasing fewer goods”; “more money chasing fewer goods” means rising prices; rising prices mean workers ask for wage increases; wage increases are inflation; inflation is a recovery and fully functioning economic growth period. Not only is the 2% inflation target indicative of that on the upside, it is also suggesting that the Fed can, by turning off or fine-tuning the “money printing”, stop inflation at or around their 2% threshold should it have been all so workable.

But none of that actually takes place, especially the money printing part. In fact, all of that is a fairy tale that the “market” simply believes can be the case if the Fed is ever so challenged. As long as the Fed holds out such credulity that if it was forced to do so it could, the “market” should do the Fed’s work in a manner consistent with the 2% inflation target. It really does hinge upon that and nothing else. Read Part 1 and Part 2

Stephen,

The papers you have linked to are not an easy read, but seem to be saying, correctly in my view, that QE as practiced by both the Fed and Europe, has achieved very little positive outcomes, and certainly not its stated intended outcomes, but has caused distortions that are somewhat negative (although the indebted property owning class may think otherwise). It is unclear to me what the authors are proposing instead; whether a different more direct form of money printing- as I would advocate when necessary, even at interest rates somewhere above zero, as it is the very low interest rates causing the distortions-or for the central banks to do nothing at all, although if so, at what interest rate level would be interesting.

It seems interesting to me that the Bank of America is forecasting a change in policy towards more fiscal stimulus in the US.

http://www.cnbc.com/2015/10/12/inequality-to-drive-massive-policy-shift…

This seems a very obvious play for the US, especially given fairly dated infrastructure, and assuming it does come about, how it will be funded will be interesting. Will it be direct Fed printing, or will it be issuing of bonds?

There is an argument that QE merely moves bank reserve money from the equivalent of an interest paying savings account (ie government long term debt) to the equivalent of a non interest bearing current account. So it actually reduces the money flowing from government to the banking sector- ie - it reduces bank income and thus lending ability. It seems a more plausible argument than the self serving nonsense we get from the would be central planners. Their primary concern is that we think they are very important.

My guess is we are at a point in time when everyone realises the central planners have no clothes.

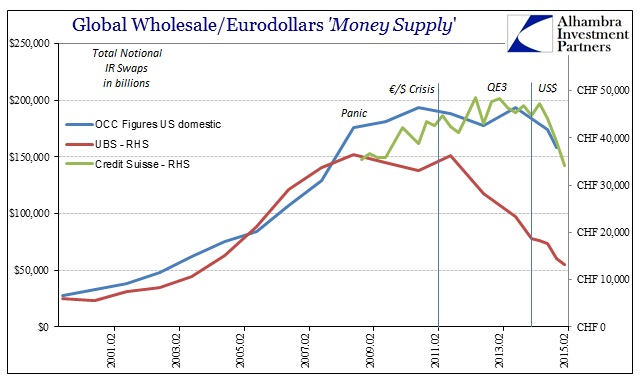

I particularly liked this graph (and note the figures are $200 trillion dollars and counting - ie real money not loose change):

http://www.alhambrapartners.com/wp-content/uploads/2015/09/ABOOK-Sept-2…

{kind=link}

I don't get that Roger...

A Central Bank buys Bonds off a Bank it pays for those bonds by depositing the money into the Banks acct. at the Central Bank ( ie. Bank reserves held at the FED... it creates bank reserves ).

(It is akin to a chq acct that u or I might have....)

A bank can spend it at any time it wants.... It is still a Banks "income"..

In regards to money supply.... I guess the transaction is neutral.. ( thou it is an exchange of "inside money" for "outside money"..... of " credit money" for " real fiat money".

http://www.pragcap.com/understanding-inside-money-and-outside-money/

BUT... Reserves are high powered money...AND if there should be another "credit Boom".... then Banks will be able to create huge amounts of credit...

I think one of the purposes of QE was to repair Banks Balance sheets... ( It would be nice if a central bank might be so gracious to you and I )

This is just my view.... and I find I have to simplify everything, in order to understand.... so I'm no rocket scientist..

A clearer money flow understanding maybe gleaned from a read of this document

I admit a certain amount of Google time will be necessary to come to terms with the mechanics of some of the terminology.

Took me a while Roelof. The bank that previously owned the government bonds now has a cash balance at the Federal reserve. Same as closing a savings account in Auckland and putting the money in a current account in Wellington. The banks apparent capital gain that the clever clogs talk about is offset by the loss of ongoing income. The banks do not lend the money because they do not see credit worthy borrowers, that has nothing to do with how much money they have sitting in reserve. Banks are not stupid, if they see opportunity they will get more money to lend. The Bank of England is quite clear on this.

Government intervention has run it's failed course. A serious attempt to reinvigorate a less regulatory constrained private wholesale credit creating global bank sector needs urgent investigation. Read more

I think they feel they have a tiger on a lead, whereas they really have a tiger by it's tail.

A shrinking tiger if the disclosures are to be believed.

Big banks always like to tidy up their balance sheets ahead of their quarterly earnings reports, the Wall Street equivalent of putting on makeup before a big date. But the latest go-round was more than a vanity exercise for the debt market, and more ominous, it could turn garish at the end of the year.

The banks were especially aggressive about primping and pruning at the end of September. Dealers sold a net $5.6 billion in just one week, leaving them with the smallest pool of corporate-debt holdings on their books in recent history. The 22 primary dealers that trade with the Federal Reserve reported just $13.1 billion of the debt at the end of last month, 71 percent below the amount in March 2014, according to Fed data compiled by Scott Buchta at Brean Capital LLC. Read more

" the Fed can “print money”; money printing amounts to “more money chasing fewer goods”; “more money chasing fewer goods” means rising prices; rising prices mean workers ask for wage increases; wage increases are inflation; inflation is a recovery and fully functioning economic growth period. Not only is the 2% inflation target indicative of that on the upside, it is also suggesting that the Fed can, by turning off or fine-tuning the “money printing”, stop inflation at or around their 2% threshold should it have been all so workable."

Sounds like a fairy tale...!!

Rising prices mean worker ask for wage increases...???? yeah..they can ask for it..

Globalization and Free trade sound like wonderful things .... especially so when we think about comparative advantage..

BUT...when free Trade gets turned on its' head and, mainly, becomes a mechanism for corporates/businesses to reduce their labour costs, by shifting to low cost countries...

AND... when Free trade agreements and Govts. have made the power of corporates vs Labour so one sided....

How on earth do average wages increase...???

How on earth are meaningful jobs created... that pay well...??

How on earth does real... grassroots consumption ever increase...?? ( ie. without credit growth )

In a world of overcapacity... how on earth does more money end up chasing fewer goods..??

Unfettered money supply growth.... looking for that 2% inflation... with out looking at the big picture...is like filling up a bucket with water.... but it never fills because it is full of holes..

( the full bucket being that 2% inflation.... )

AND... the biggest hole is that most of that new quantity of money goes into assets...( like a game of monopoly )...

Another hole is that with more money we simply import more goods....

Another hole is that with ultra low interest rates ( Nestle had a bond issue for -ve yields ) ...it is so easy to build new capacity... in low cost countries... ie. investment... and then we end up with even cheaper goods...

etc..etc..

A Central Bank looks rather limited.... in the scheme of things.... playing with money supply does not solve underlying problems....

Having a fixation on the CPI...and 2% inflation... in what is a very dynamic , fluid and complex system ( economy )...that is continually evolving..... seems wrong to me... seems like dogma....

Maybe 2% CPI inflation will just squeeze consumers and lower living standards..???

This is where I like George Soros' idea about "reflexivity"..... that we get trapped into belief systems.

The mkt gets caught up in a belief system...and there is an inflection point when it suddenly realizes that what it believed in is no longer valid..... and then...whamo... a shift happens..

Thats why Open Societies and transparency are such good things.... these shifts can happen more fluidly ...

Why did TPP have to be sooooo secret..???

to cut a long story short... Central Banks can't solve real economic problems.... at best they give us quick fixes.... and then bigger quick fixes....

The way I see it, modern money and banking is so complex that no-one can really understand it. Some people understand bits of it, but clearly even the very clever chaps at Lehman Brothers (for instance) thought they did, but in fact, didn't. I can't see why the not so bright academics should do any better, except in their own eyes.

they wont raise this year if anything they have now got themselves into a position where there economy will slow and they will need to pump up QE4 anyone

DC

Please, either do not highlight articles that are behind a paywall or include enough of the text to cover your quote.

The oil price is a worry for Shale Oil Producers , they need at least $50 to break -even , so $47 is a problem for the industry

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.