Here's my summary of the key news overnight to keep you up-to-date over these holidays.

Stocks are weaker on Wall Street today. Commodities are lower.

According to the IMF, global economic growth will be disappointing next year and the outlook for the medium-term has also deteriorated. The IMF's Christine Lagarde said in a guest article in a German newspaper that the prospect of rising interest rates in the US and the slowdown in China were adding uncertainty and a higher risk of vulnerability worldwide. She said growth in global trade has slowed considerably and a decline in commodity prices are posing problems for economies based on these, she said. She also sees weakness in the financial sector in many countries and financial risks are rising in emerging markets.

In the US, home sales volumes fell 'modestly' in November from October but they were still +2.7% higher than the same month a year ago. The median price is US$220,700, a +6% rise year-on-year.

China has suspended at least two foreign banks from conducting some cross-border yuan business until late March, limiting their scope to profit from a widening gap between the currency's exchange rates inside and outside the country.

Portuguese authorities have been shifting assets around to 'fix' one of their banks. This has involved Novo Banco SA, the bank that is at the heart of the NZ Super Fund's legal stoush with Oak Finance and the Portuguese Central Bank. Things just got worse and more complicated for the NZSF in this matter, it seems.

Coal and iron ore might be the poster-ores of a retreating commodities market - one that affects Australia significantly - but there is one mining product that is in hot demand: yellowcake uranium. Asia's fast-growing nuclear energy industry is fueling demand for the radioactive metal. Despite reactor closures in Europe and the US, the global outlook for uranium is bright, with significant demand coming from China, India, Korea and Russia.

There is still no price difference between the US WTI benchmark and the Brent benchmark but both have given up more than US$1 today to trade at US$36.50/bbl. A surprise buildup in stocks of petroleum products in the US is behind the fall.

Gold is lower in New York, now at US$1,060/oz and having shed all yesterday's gains and more. This is near its low for the year (US$1,046) and -18% below its high for the year of US$1,296/oz which it reached on January 22, 2015. It's basically been downhill since then.

UST benchmark 10yr bond yields is rising in New York today and are now at 2.31%. This is a rise of +4 bps since yesterday and +7 bps in the past two days. Bond prices are falling. At the start of the year the rate for this key benchmark was 2.17% and during the year it fell as low as 1.68% and rose as high as 2.50%.

The NZ dollar starts is ending the year -7.5% lower than where it started. Today it opens at 68.3 USc -13% lower than the 78.3 USc it was on New Year's eve in 2014. It is at 93.8 AUc,-2% lower than a year ago, 62.2 euro cents which is -3% lower. Against the British pound were are 46.1p and -8% lower. (We are -9% lower against the Chinese Yuan.) The TWI is at 73.5 and while this near a six-month high, it is -7.5% lower than on New Year's eve in 2014.

The easiest place to stay up with event risk over the holiday period is by following our Economic Calendar here »

Daily exchange rates

Select chart tabs

30 Comments

http://blogs.worldbank.org/voices/year-review-2015-12-charts

The share of the world’s population living in extreme poverty is projected to hit a historic low of 9.6% of in 2015 – falling from 37.1% in 1990.

The number of forcibly displaced people now stands at more than 60 million -- the highest number since the Second World War. More than half of the some 20 million refugees worldwide come from Syria, Afghanistan, and Somalia, and the majority find refuge in countries close to their own.

Between 1990 and 2015, the under-5 and maternal mortality rates fell 53% and 44% respectively. This means the number of children dying before age 5 has fallen dramatically - from 12.7 million in 1990 to 5.9 million in 2015.

Portuguese authorities have been shifting assets around to 'fix' one of their banks. This has involved Novo Banco SA, the bank that is at the heart of the NZ Super Fund's legal stoush with Oak Finance and the Portuguese Central Bank. Things just got worse and more complicated for the NZSF in this matter, it seems.

Here it is necessary to back up and address the “reason” (excuse) behind this newest form of systemic bank crime. The “bail-in” is the ultra-insane culmination of the “too big to fail” doctrine. By this doctrine, any and all assets, public or private, in our financial system can and will be sacrificed (stolen by the Big Banks) to prevent any of the Big Banks from “failing” – that is, going bankrupt as a consequence of their own reckless gambling . Read More

Good luck is all that stands between under capitalised Aussie banks and their unsecured creditors, and that includes depositors. Read more

Depositors are investors and no investment is without risk or cost to someone if it goes wrong. So its perfectly acceptable for depositors to take a hair cut. Its also perfectly acceptable for investors not to invest in a bank, it is their choice to take the income.

That is a defensible retort if depositors received the same return on capital as bank shareholders. I believe from past experience ~16% p.a is the target.

No and no,

a) They can move any time they want, they are not forced to be a depositor in a bank, ergo they are free to leave if they do not like the risk.

b) So then the depositors if they had any sense would buy bank shares which is also tax free?.

So they must be stupid then?

c) Also the % is immaterial.

d) even 16% tax free probably does not cover the size of the potential loss.

Wrong. People are forced to be a depositor in a Bank.

That way both the Bank and Govt can stick their beak in your business, take their unearned cut and track the hell out of you.

You ever tried buying a house with folding cash?

Rubbish, no they are not forced at all to have a deposit account. If there is an OBR that is not on the chequing account but savings.

Otherwise that is a specific point and even then no you dont have to have the deposit in a bank.

tracking is a moot point to the argument of loss.

Try spending over 10K in cash via a single purchase ( Where the reporting limit kicks in) and then get back to me on how you get on.

We are arguing different points here. A deposit is a long term deposit, if you wanted to buy something and you had to use the bank then you transfer the money into and then out of.

Are you saying that an OBR wouldn't apply to money held in a cheque account ???

My understanding (and I maybe wrong) is the chequing and investor parts of the bank are treated as separate entities for OBR purposes. So the idea is if an OBR event occurs all investments/deposits are frozen over a weekend? for some weeks? until a haircut % is determined? but the chequing part opens on the Monday as normal.

Now like I said I maybe wrong?? or maybe the Govn/RB/Banks might decide to confiscate your "cash" in the cheque account anyway?

As a PAYE if say my bank goes into an OBR well I just tell my employer to deposit my pay into another bank. of course that assumes the other banks are OK, which I doubt.

So one of my protections is I hold a CC from a different bank to my main one so if my main bank does an OBR I should still be able to eat.

You ever tried buying a house with folding cash?

True story - I have witnessed that very act

In 1998 just after Hong Kong was ceded back to China, when numbers of people were fleeing the place, a friend in Mt Roskill was door-knocked by a Honkers refugee who wanted to buy their house and offered CASH and placed a briefcase full of bricks of high denomination bank-notes on the dining-room table

b) So then the depositors if they had any sense would buy bank shares which is also tax free?.

Exactly - setup a low cost bank share ETF and allow the depositors to arbitrage the equity and deposit saving rate returns. This would necessitate the expulsion of the egregious state sponsored central bank acting in concert with an expedient political overseer dictating what unrepresented depositors should earn for risks undertaken. The freedom of market determined price discovery would be a revelation for all to behold.

Thanks, you never cease to amaze me on your extremist views as they slowly come to light, Ann Rynd by your bedside I take it? Free market, yeah like all the bankruptcies and financial disasters etc were before the Fed was created? no thanks.

Name them - the US Federal Reserve was set up in 1913 - and let's not forget more recent financial debacles engineered under the purview of Fed type connivance.

Just as interesting is "who" the founders of Federal Reserve were, the fact it is privately owned and operated, and not a government owned and controlled organisation, and the identity of the founders and shareholders

Name them

From memory, this book addresses most of your purported concerns. As to ownership, the 12 regional reserve banks have private shareholders, but nonetheless are subject to official oversight by the Board of Governors of the Federal Reserve System, hence the recent, unprecedented transfer of cash to the US Treasury. Read more

and the de-regulation? the non-prosecution / pathetic fines of the few that were? To me many for the financial parasites should be in jail, that includes the last President Bush.

It is okay to commit war crimes if you win, it seems. Unfortunately, it seems that under No Change At All Obama that more people have died violent deaths in the Middle East and North Africa than under his precedessor. Not sure where I read that, but it was somewhere reputable, er, I think.

No I think that is probably true. Some policy wonks examined Obama's policies and concluded he had governed like a mild republican (say Ike) rather than a democrat and certianly it has not striked me he has pulled punches in killng ppl.

I agree, or am at least inclined toward, most of your opinions and comments Steven but not this point. You are applying your own level of knowledge and sophistication to the average person, this is simply not the case. Intelligence is also a part but I have those close to me that are at least as intelligent as you but, despite being informed of the OBR by me, they still can't grasp the concept. The apparent safety of a bank deposit is deeply ingrained in the psyche of the general population.

This is the same principle that underpins my claim that money would fulfill the requirements for a criminal fraud, it simply isn't what people believe it is.

and commentary from gold bugs, hardly un-interested parties are they.

Comments on chinese buyers,

http://economyandmarkets.com/markets/housing-market-markets/chinas-unpr…

"The Chinese make the Japanese look prudent!

Chinese buyers are bidding up the high end of the top coastal cities in English-speaking countries like they’ll never go down and like they can’t get enough.

We’re talking Sydney, Melbourne, Brisbane, Auckland, Singapore, San Francisco, L.A., Vancouver, Toronto, New York, London…

These markets are considered “Teflon-proof.” They’re not! In fact, they’re some of the greatest bubbles that exist today. China’s leading cities – like Shanghai, Beijing and Shenzhen – are up 700% or more since 2000!

Guess what happens when the bubble wealth in real estate that has built up in China finally collapses?"

The problem I can see is that we have virtually done away with money and replaced it with IOUs. Bank deposits become unsecured debt, and yet banks require security on loans. How do we get back to inflation when there is no money? The only things that inflate are assets that banks choose to provide cheap loans for. Gold is a form of money and yet it 's price is falling, so no one wants money? I wonder if where we are heading at this rate is a complete change in our financial system? How can we value our possessions, houses, labour by an unlimited supply of bank credits? It's basic economics 101. Money must be a store of value, by which we value everything, a means of exchange and a standard of deffered payment. But if all money is becoming unsecured debt or only secured by overvalued assets is it any longer a store of value?

tim12, the reality of that which you note is revealing itself in a none to subtle manner.

In other words, for years now “people” have been leading with the ephemeral and dismissing the real because that seemed to be the path of least resistance; to consciously set aside what is actually happening because it can only be temporary in favor of what isn’t evident now but should occur because Janet Yellen (as Ben Bernanke) says not just that it will, but that it must. The backwards placement of this kind of intuition is the only way to explain these divergences as they continue for years. Read more

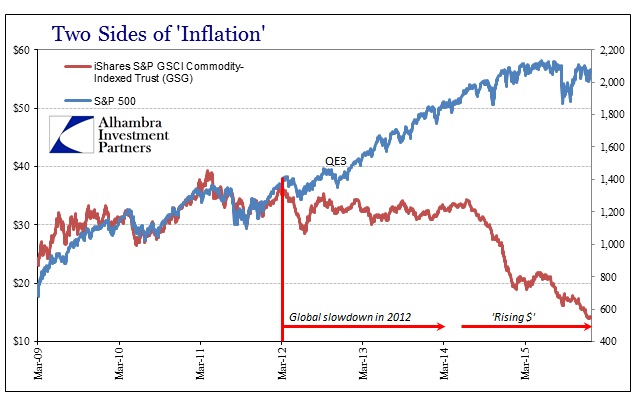

The two sides of inflation charts are really interesting. Real stuff getting inexorably cheaper, financial fantasy products getting more expensive. Commodities take real work and the creation of real physical capital like railways, roads and ports and ships. Financial fantasy products, in this case US shares, are pumped up in price by corporate borrowing to buy back shares using record profits created by not increasing wages and not spending on real capital investment.

http://www.alhambrapartners.com/wp-content/uploads/2015/12/ABOOK-Dec-20…

{kind=link}

Wages in the US have not increased since 1970, in France they have gone up 2.8 times in real terms:

Page 18 https://www.gmo.com/docs/default-source/public-commentary/gmo-quarterly…

We live in interesting times. When did financial "capital" somehow come to be seen as real capital whereas real physical capital became seen as an expense? 1984 (by George Orwell) presumably.

Nice...

"Dhaval Joshi, an economist at BCA, a London-based research company, said: “A commodity bubble has deflated three times in the past 100 years: the first was after world war one; the second was after the 1980s oil shock; the third is happening right now.”

http://www.theguardian.com/business/2015/dec/30/oil-iran-saudi-arabia-r…

hmmmm

"Slide 4 suggests that the world economy is heading into recession, because recent growth in the use of energy supplies is very low recently. Another sign that we are headed into recession is that fact that CO2 emissions fell in 2015. They usually don’t fall unless a global crisis exists. Emissions fell when the Soviet Union collapsed in 1991, and they fell during the economic crisis in 2008. Perhaps the world economy is hitting headwinds that are not being picked up well in conventional calculations of GDP growth."

http://ourfiniteworld.com/2015/12/21/we-are-at-peak-oil-now-we-need-ver…

More from the IMF,

"For years, Saudi Arabia has used its oil wealth to support friends and allies around the world, including media organisations, thinktanks, academic institutions, religious schools and charities. Countries that have traditionally benefited from Saudi largesse include Jordan, Lebanon, Bahrain, Palestine and Egypt.

But now the IMF has raised the prospect that Saudi Arabia could go bankrupt in five years without changes to its economic policy, cuts in support to foreign allies seem inevitable.

Egypt’s black-hole economy is potentially the kingdom’s most expensive foreign policy commitment. In recent years, Saudi Arabia has donated billions in cash and oil products but, despite this, the Egyptian economy, battered by war, terrorism and political instability, is facing an acute foreign currency shortage.

Analysis Saudi Arabia's $640bn question: when to turn off the taps?

Speculation is mounting that Saudi financial support to Egypt is starting to dry up – something the Egyptian authorities have denied – and that this is damaging the bilateral relationship."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.