Wednesday's sudden drop in swap rates could well suggest that sub 4% mortgage rates could reappear.

Of course, that depends on whether that fall is sustained.

But today, we have another drop on Wall Street and a decline in the benchmark US Treasury yields.

And that is flowing through to local swap rates this morning.

A drop in fixed mortgage rates is therefore a live possibility.

But by how much?

Current mortgage rates are low by historical standards.

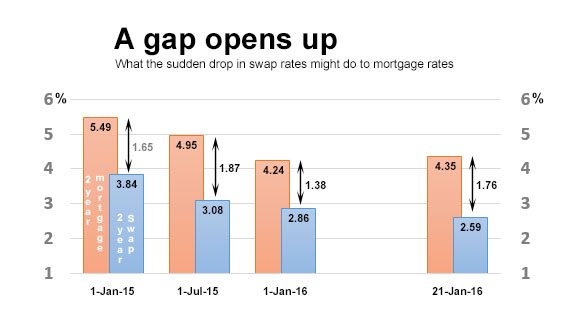

But margins-to-swap are not.

It was only a few weeks ago we saw one local bank pitch carded rates at a margin-to-swap of +1.4%.

After Wednesday's fall in swap rates, these margins seem to be back to - even slightly above - normal levels.

The chart above compares the lowest carded two-year fixed mortgage rate on offer from any bank with the two-year swap rate on the dates shown.

It is 'easy' to extrapolate a 2.58% swap rate (today) with a 1.40% margin to give a 3.98% two-year mortgage rate offer.

One thing missing from this back-of-the-envelope pricing approach is the risk premium. We see Credit Default Swap (CDS) spreads rising, and that will restrain the bank pricing officers.

But it is still possible.

And it is probably more likely given that the volumes of new mortgage business is tailing off. Bank marketing folks will be highly motivated to win share (and hold on to their sales bonuses that are dependent on volume).

Who will be the next to slip below 4% (remembering that SBS Bank has already broken the ice with a 3.99% rate for a number of weeks in late 2015)?

18 Comments

Late November banks were negotiating well below carded rates to as low as 4% to 4.2% for 1 and 2 years fixed. Swaps have since taken a dive that was never predicted by any bank economist. To keep the money rolling as demand drops, due to fear of a GFC2 and Chinese desert the NZ housing market, the banks will almost certainly offer carded rates in the 3.5% to 3.75% territory within a matter of weeks. Elderly with finds on deposit are going to do it tough.

The optimistic Liam Dann has it all wrong http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=115…

There is no US recovery - it's all smoke and mirrors and as for Europe - well that is a basket case. GFC2 is going to be a severe correction as the amount of debt out there is massive compared with 2007 and trillions of it will never be paid back. The US were too generous with the bailouts - they should have permitted failure to enable a reset of the world economy to take place - all they have done is postpone the inevitable and created a worse problem.

Anyone else agree?

How low will 1 and 2 year fixed mortgages go - 3%?

Will the OCR be cut another 0.5 over the next 8 weeks?

Just been offered 2yr fixed at 4.25% + 1k cash.

Over the past 3 months I have changed over to kiwibank, they have offered lower than other banks with an incentive of 1% of the mortgage rate. Ive been fixing all at the 6 month rate. Lowest rate has been 4.25%.

Renegotiate

What sort of deal do you think should be realistically achievable?

Yes your right i forecast the 6 month fixed rate at 3.50% it may well go lower as the crash and deflation progress which is doing now.

I would not be concerned with long term fixed rates go short term go low until inflation takes hold which it wont do until 2023

There is no recovery in the USA or Europe the only thing that is happening is money printing and policy esing as to try and stop the 2016 depression worse than 1929.

The crash will happen 2016 so they can blame the coming depression on Barry Obama his term ends Nov 2016 new president in office Jan 20 2017.

This crash is Barry Obama's farewell present to the markets.

Barry will retire to Hawaii and play golf the John Key.

Therefore both their futures are looking quite bright and will be much better off.

Doesn't bad debt and economic turmoil make the cost of borrowing for the banks increase? Do mortgage rates not disconnect from base rates if things get messy in housing market and prices drop?

Macbet - interest rates sunk to historical lows during the economic turmoil of 2009 to 2016 - that's all the evidence you need.

Bigblue - Macbet makes a fair point - during the GFC bank funding cost blew out to above 150bps which went into the level of interest rates. However, it was nicely masked by the 575bps fall in the OCR. I'm not saying the next crisis will necessarily have the same impact upon bank funding costs (they are much more longer-term funded since the GFC), but one thing I am certain of, there won't be another 575bps fall in the OCR to cushion it if we do.

So many big calls that are impossible to make with any accuracy.. but i will pick a holes in a couple.

1. Quite a few bank economists saw this coming, albeit the timing is a little off. Both Westpac and ASB have been saying for quite some time the OCR goes to 2% and with it short term swap rates.

2. I would bet my lifes savings on major banks NOT offering a carded rate of 3.5 -3.75% within weeks. IF, and that is a massive IF, we saw an OCR of 2% in the next 3 months, the carded rates may get to 3.75 at one or two banks. Given cash and broker incentives on offer, along with the cost of raising funds mentioned in the article, a margin of 140 points over swap is very hard to move below while at the same time covering the cost of capital.

Could we get to 3% mortgage rates.. maybe, but that would require an OCR of close to 1%, with no corresponding rise in funding cost. Would be pretty tough but maybe if things get really bad in 2017 onwards.

1. as in some months 6?, not 12+....?

2. Agree, the commercial wholesale borrowing rate is in effect from private offshore investors. Who if the effects that have caused us to have to drop to 2% OCR will not be keen to lend to us at that same 2%. In fact we might find like Greece the NZ banks have to accept higher costs. Always a huge risk when you borrow short to lend long.

Yep.. was referring to Bigblues comments that the moves since late november hadnt been predicted by any bank economist. First to admit that most/all got it wrong when looking back a bit further.

So if the two year swap over next two weeks goes to 2.2 plus 1.4 margin = 3.6% two year fixed mortgage rate even if OCR stays where it is. A matter of weeks away I reckon.

Offered 4.09% on 2 years with 8k cash back on a refinance > 1M. Looks like better to stay put on floating @ 4.85% for few more weeks!

Which bank?

I am looking for home loan first time and I have to confirm the bank next week. after reading this hope I have to go for floating instead fixed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.