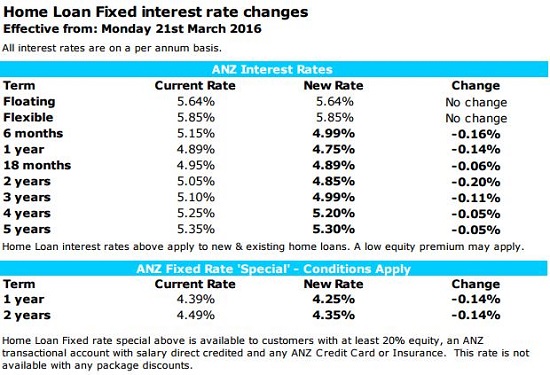

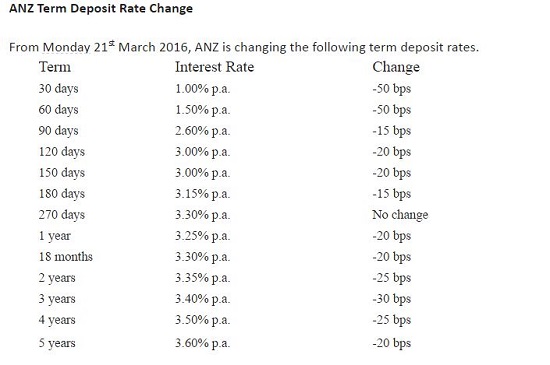

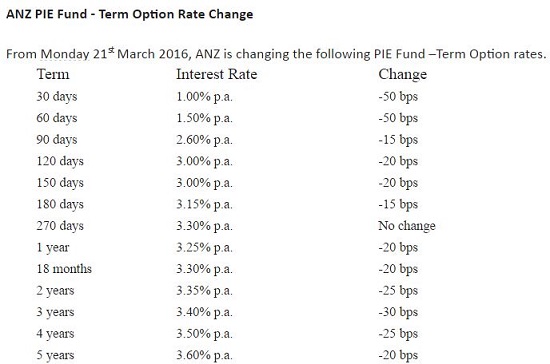

ANZ is slashing up to 50 basis points off its PIE and term deposit rates, yet it's only cutting its fixed-term interest rates on home loans by between 5 and 20 basis points.

The announcement comes further to the Reserve Bank cutting the Official Cash Rate by 25 basis points on March 10.

The bank has announced the following changes – none of which are market-leading – today:

Note ANZ cut its floating and flexible homes loan rates by 10 basis points straight after the OCR cut. These changes took effect immediately for new customers and will take effect on March 29 for existing customers.

See all banks' carded, or advertised, home loan rates here.

This is the second time ANZ's cut its 30-day term deposit rate by 50bps since the latest OCR cut. It's now half of what it was before the RBNZ made its move. ANZ also cut its online savings and cash PIE interest rates by 25 basis points to 0.75% on March 14.

See all banks' carded, or advertised term deposit rates for one to nine months here. And all banks' carded term deposit rates for one to five years here.

6 Comments

Why , when the Banks Cost of funds has dropped so may times , is the floating mortgage rate unchanged ?

This is another example of what Bernard Hickey highlighted on the weekend as an oligopoly at work

Kicking the can down the road at NZ citizen's expense - Taxes fall on savers incomes as does the tax take from tax deductible high rate risky business loans - Aussie banks repatriate the higher net interest margin back home.

While RBNZ invoked under rewarded NZ depositors are expected to risk all underwriting the higher default risk profile determined by the RBNZ dictated OBR racket. Life is certainly stranger than fiction.

Economists at the country's biggest bank ANZ are expressing concern at the blow-out of household debt levels, which has seen household debt-to-disposable income rising to a record high of over 167% Read more

Banks know that ZIRP and NIRP is coming soon, so getting all prepared with lower longer term deposit rates. Otherwise they'll be locked in while OCR is .5

Not for foreign wholesale debt, it will rise until these banks are bankrupted and taken over by their larger Northern Hemisphere peers. We will be just EM rated and subject to whatever Brazil pays.

Note most 2 year rates start @ 4.3?% now....anyone experiencing discounts on this - my bank refused when I asked for 3.95 for 2 yrs considering both personal & biz lending of $400k and less than 30% borrowed on equity / income to support ?? perhaps I'm not a great risk?

NZ Aussie bank subsidiaries are going to demand higher rates of interest to cover the cost of borrowing rising capital demands on top of funding dividend payments to disgruntled shareholders. APRA has lent on the parents after being lent on by foreign wholesale lenders - unforgiving professional taskmasters. They will end up as debt ridden hollowed out shells - this is just the beginning.

APRA urged banks in December 2014 to limit their annual growth in investor mortgages to 10 percent. From July this year, lenders will need to hold more capital against mortgages and the regulator asked them to change the way they assess borrowers’ capacity and ability to repay the loans. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.