ANZ has announced its rate reduction for floating rate borrowers following today's OCR rate cut of -0.25%.

But it is passing on only a -0.10% reduction.

It is keeping the balance.

A spokesperson issued a statement which said: "Over the last 18 months, offshore wholesale funding costs have increased significantly. Until now, and unlike some other banks, ANZ has passed on all the recent OCR rate cuts in full. But international volatility has proved to be more than temporary so these extra costs now need to be reflected in our lending rates."

"It’s important to also bear in mind that changes to floating and flexible rates won’t impact most ANZ home loan customers because around 76 per cent of ANZ home lending is fixed rate, compared to only 36 per cent four years ago."

ANZ's floating rate will drop to 5.64% for floating rate home loans and 5.75% for their revolving credit facilities.

These changes will take effect on Tuesday, March 29 for existing customers, and immediately for customers which take out a new loan today onward.

The RBNZ said today it expects banks to pass on the whole reduction.

The Cooperative Bank has already announced that it will pass on the full -0.25% reduction. The Cooperative Bank floating rate has become 5.45%.

Wholesale swap rates fell sharply today.

The 90 day bank bill rate fell even more than swap rates, being down -32 bps since the January OCR review when no change occurred.

Sine the last OCR reduction in December 2015, the 90 day bank bill rate is -36 bps lower.

The 90 day bank bill rate is important because this is the key benchmark floating rate lending, especially for mortgages, is based on.

Some bank officials have pointed out that the run-up in CDS swap spreads adds to their funding costs. But while these did peak at 170 in February, they have siubsequently fallen back to 143 today. And the last time the OCR was reduced this spread index was at 127. It is important to note that this index is only a proxy for Australasian and debt risk. And that includes more than just banks; it includes the Aussie miners who have suffered far more credit stress and that has pumped the CDS spread index. Further, that index reflects the Australian debt indications much more than the New Zealand components. Reading the CDS spread index is only a very rough proxy for NZ risk costs and probably overstates it significantly.

ANZ NZ made a tax-paid profit of NZ$1.7 bln in 2015.

Mortgage rates

Select chart tabs

28 Comments

A spokesperson issued a statement which said: "Over the last 18 months, offshore wholesale funding costs have increased significantly. Until now, and unlike some other banks, ANZ has passed on all the recent OCR rate cuts in full. But international volatility has proved to be more than temporary so these extra costs now need to be reflected in our lending rates."

What about a reflection of the inherent rising risk factors showing up in higher domestic deposit rates? It's not as as if the cross currency swapped foreign lenders have any OBR risk from banks' previous poor lending decisions and still they hike rates.

Mouthful

What about a reflection of the inherent rising risk factors showing up in higher domestic deposit rates?

Would you care to deconstruct that please - not sure it says what I think you mean

Foreign wholesale lenders have moved their risk adjusted NZ bank lending rates higher- in a free non-state controlled market domestic lenders would normally execute their right to do the same based off the better informed foreign wholesale metric. Why hasn't the RBNZ taken these factors into account given depositors are now considered risk averse investors, in need of higher risk offsetting interest rate returns?

Motive.......Stephen H, I genuinely believe Wheeler is responding to an IMF call to arms......do read that piece on 90 at 9 yesterday on the IMF going all bold on plain speak for once.

Japan geesus what can you say really cept maybe .................meanwhile back at the ranch..!

Sure, share and share alike

Central banks' attempts to kick-start advanced economies following the financial crisis have made the gap between the rich and poor wider, suggests the Bank for International Settlements. Read more

interesting they rank shareholders first whom would have thunk

Well I hope they at least move deposit rates by the full the 25bps

The pathetic response from the banks tends to indicate that they are of the belief that the average Kiwi is pretty happy with mortgage rates in the mid 4% territory - the huge volume of mortgage approvals over recent weeks indicates that is the case. So they can probably get away with stretching their margins further and making even bigger billions. The average Kiwi borrower needs to start putting pressure on the banks and not take this lying down. They were offering punters 4.15% for two years fixed ie well below carded rates when the swap rates were half a percent higher than they are now so they should be able to and can offer 2 years fixed at 3.65% - they really are taking the piss right now!

The free market economy at work. Obviously these Ockers reckon the competition ain't too flash and they can keep creaming it for all its worth. Sheep shaggers?

Time to buy a new mattress to stuff.

Great to see the NZD move closer to the PM's goldilocks rate - but does that mean the bears will be back soon?

Inflation expectations, fears, are rising and markets are responding. Markets are not infallible and it could be that these moves are quickly reversed as the deflationary fears of the last few years return. But I have my doubts. It has always seemed inevitable that the aggressive monetary policies of the world’s central banks would end in inflation. We may have finally reached the point where everyone looks askance at fiat currencies, preferring to hold their capital in real assets rather than ones that depend on confidence in economists and politicians. Considering the track record of economists and their models and the current crop of Presidential candidates the only wonder is that it has taken so long.

http://www.alhambrapartners.com/2016/03/09/is-inflation-about-to-make-a…

Just proves that with out some form of regulation, unrestrained gred will win out over client base and common sense. These guys will continue fleecing us while RBNZ and JK do a Nero

It is like this however with many aspects of "retail". I will accept some of it is simply overhead costs spread across too few sales, but I think much of it is simply monopolistic behavior.

So correct Aj. I can cope with inflation, deflation, but it's subducation that concerns me.

Wheeler should put the ocr back up in kind. Just for a laugh.

Is that sort of like laughing at the firing squad sort of laugh?

Smells a bit like U.S rate increases being transmitted to New Zealand. Should be interesting times when a few more come through.

Friday 11th Prime Minister Key announces investigation into the bank cartel and unfair pricing.

Wednesday 16th. All allegations found proved (Well it's been obvious for years)

Friday 18th. Break up of banks announced. Twenty new banks. Only NZ citizes can be shareholders.

Saturday 19th. Pigs do formation flypast

more like PM announces retirement, following day announces taking a board seat at Westpac and to be future chairmen

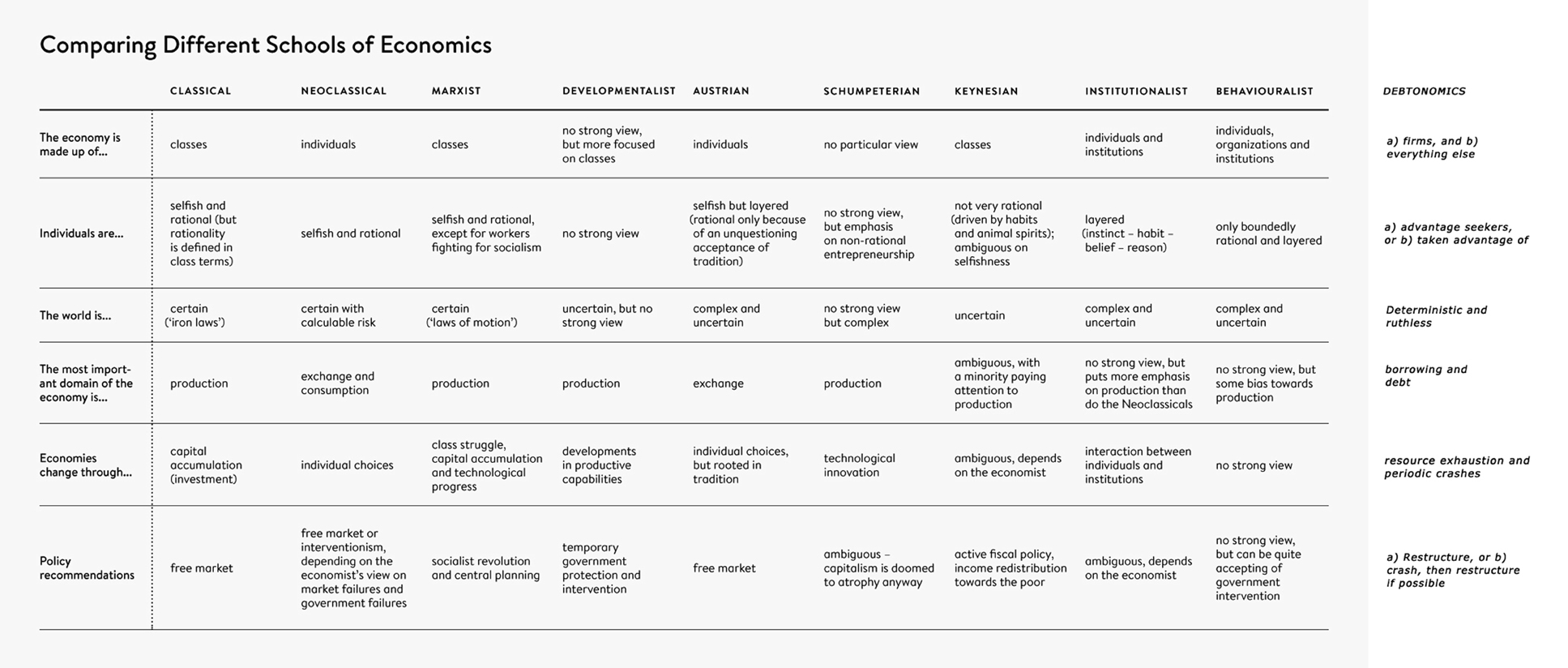

Comparing different 'Schools of Economics' ..a great chart. Economics is a behavioural science after all, thats why the words of the speech and the intentions are studied so intently, as were the tea leaves of the past.

http://www.economic-undertow.com/wp-content/uploads/2014/07/comparing-d…

{kind=link}

Unfair practice when ANZ send out letters to refix your mortgage. It should be saying stay on floating. Poor people being manipulated so that banks keep margins high.. 76% fixed is just truly sad.

Unfair practice when ANZ send out letters to refix your mortgage. It should be saying stay on floating. Poor people being manipulated so that banks keep margins high.. 76% fixed is just truly sad.

Unfortunately, floating rate is very high, forcing borrowers to fixed.

6 months or 1 year is best compromise.

Wonder how other banks will react. Great time here for other banks to drop rates the ful 25, point the finger at ANZ and grab some new customers.

As an ANZ customer I'm pretty amazed by this and will be moving my accounts somewhere else, offshore wholesale funding cost, p|ss off. Does that mean you were contemplating raising your fixed rate by 15bps last week? Talk about money for nothing.

Kiwis are so happy with mid 4% rates that the banks can get away with pocketing the reduction, boosting their margins to record levels and making even more billions. Kiwis really are suckers as evidenced by all the people that fixed mortgage rates a year ago for 3 years at significantly higher rates than are available today.

Suckers is a bit harsh, I'd rather say that there are still a lot around who can remember 18 - 23% rates, and they are really happy at 4%. This is more about a lack of education on the power of the free market, a move by the banks to charge if you want to move every thing, and just how difficult it will be. Banks fees put a cost on that can make moving seem not worth it. One way though would be to have accounts across all the banks, and be able to move money at short notice. Minimum action at any one bank will minimise fees, but deprive the bank of any of your savings.

The poor old ANZ has got it's back against the wall. All those dairy farmers running at a loss.

EU predicts 'further milk price falls', as output growth continues

The European Union, forecasting further milk price falls, flagged a "need for supply increase to slow down" in dairy – even as the bloc estimated its own output rising further both this year and 2017.

"Further milk price declines can be expected," the European Commission said, singling out in particular early 2016 as a vulnerable period, given relative values of fluid milk in the EU compared with those abroad, and in dairy commodity markets.'Significant increases in Ireland'

The comments came as the commission forecast EU milk output, which rose by 2.3% to 163.5m tonnes last year, rising by a further 1.4% to 165.7m tonnes in 2016.

However, the commission said that the rise in world supply was "not only due to EU quota expiry".

From 2007-15, US milk production rose by 12% and New Zealand output by 36%, well ahead of the EU increase of 10% over the same period.

http://www.agrimoney.com/news/eu-predicts-further-milk-price-falls-as-o…

And benefit of an alternative headline, rather than:

http://m.smh.com.au/business/banking-and-finance/rate-rigging-case-a-cr…

Hang on who is paying for this...

The corporate watchdog's pursuit of ANZ Banking Group over potential interest rate rigging weakens the bank's credit-worthiness because of the damage to its reputation and the threat of class actions, says Moody's.

The ratings agency warned of "significant" damages from related class actions if the Australian Securities and Investments Commission (ASIC) succeeds in its civil case. ASIC is pursuing the bank for unconscionable conduct and manipulation of the bank bill swap rate, a key interest rate benchmark in the Australian money market.

If we went to custodial sentences instead of fines, it might make a difference.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.