Here's my summary of the key events from overnight that affect New Zealand.

Peer-to-peer lenders in China warn they risk going bust if the Chinese Government goes ahead with plans to up its regulation of the burgeoning industry, as competition heats up and the economy slows. Citing credit risk and potential new restrictions on their abilities to accept public deposits, P2P executives say firms that aren’t adaptable and lack proper risk controls are likely to fail. This is a huge concern given there are a whopping 2,595 P2P platforms in China - up from just 880 in 2014. The number of outstanding loans within the sector has increased 14-fold in this time.

Another Fed president has come out in a support of a rate hike as early as next month. St Louis Fed President James Bullard says inflation expectations have started "moving in the right direction". Bullard is one of a hand-full of Fed presidents who have spoken out in defiance of Fed Chair Janet Yellen on the issue this week.

A governing council member of the European Central Bank says the bank's latest expansion of stimulus measures went too far. Jens Weidmann, who also heads Germany's Bundesbank, says the ECB should be flexible about the time it takes to lift inflation back to target and should worry about low bank profits as they could reduce the effectiveness of its policies.

The pause button's been pushed on the strengthening US housing market. Data out overnight shows new home sales rose 2% in February. Yet the increase was concentrated in the west of the country, where sales surged 39%. A separate report released by the Mortgage Bankers Association also shows some weakness in housing activity, with its Purchase Index decreasing 1% last week. Yet with the index up 25% from a year ago, the sector's still at a high point.

In New York the benchmark UST 10yr yield is up to 1.91%.

The US crude oil price has eased overnight to US$40/bbl, while Brent has been knocked back to just under US$41/bbl. The stronger US dollar has helped dampen demand for oil, yet a preliminary report from an industry group shows a higher-than-expected build up of stock.

The gold price has plummeted US$33 overnight to US$1,219/oz. Gold had spiked off the back of the Brussels attacks yesterday, as investors rushed to "safe havens".

Talk among Fed presidents of another rate hike soon has seen the US dollar strengthen. It's at 67.2 USc against the kiwi. The NZ dollar has bounced back to 89.0 AUc, following a speech by the Reserve Bank of Australia's governor talking up the economy's ability to deal with a potential economic shock yesterday. The dollar is stable at 60.0 euro cents. The TWI-5 is slightly lower at 70.8.

If you'd like to catch up with all the local changes from yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

21 Comments

How did the futile fight to find CPI inflation reveal a landscape of over leveraged finance companies masquerading as banks, and in desperate need of bail-in legislation?

It's Official: Canadian Bank Depositors Are Now At Risk Of Bail-Ins

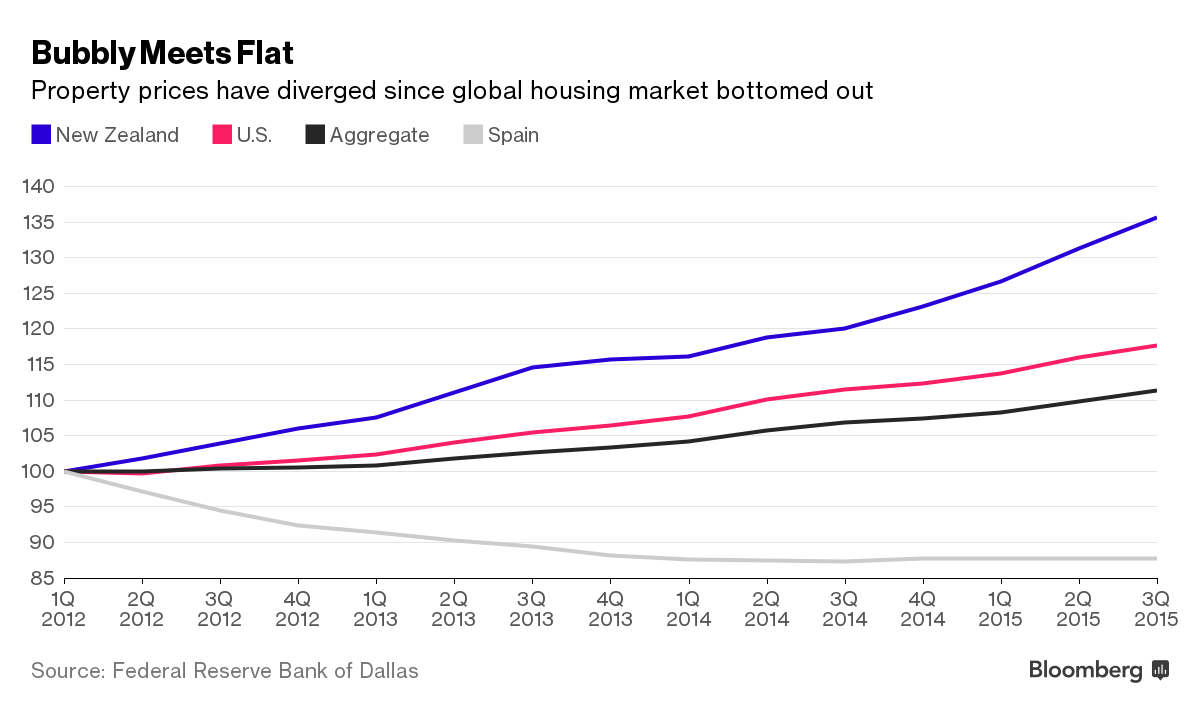

How did the resultant false prosperity of a mortgage fueled property speculation boom find New Zealand ahead of the pack?

{kind=link}

Property Bubble Ghost Haunts Central Bankers Trying to Boost Prices

And a Happy Easter to you as well Mr Wheeler.

Years of excess domestic asset appreciation will be much harder to fix in New Zealand. Wheelers focus on the exchange rate will see a balance sheet depression in New Zealand before decades end. I was surprised that the new flag designs have not a real estate company or bank adorned upon them.

Pat, for you.

http://www.theaustralian.com.au/business/property/kidman-empires-suitor…

Now its a fund or partner thereof. Reportings all different now.if it ever was.

Henry , cannot access site.although Hunan dakang announced new CEO yesterday , speaks Chinese unlike Romano.

"I like the smell of cattle in the yards,”

And other quotable quotes...

‘I’ve always had an interest in agriculture, cattle and the land,’ says James Jackson of Australian Rural Capital. James Jackson is a man with a fight on his hands. As chairman of Australian Rural Capital, Jackson has emerged as a key player in the drawn-out bidding war for the S Kidman & Co pastoral empire. But it wasn’t always this way.

The expansive outback properties are a world away from the rarefied world of London and New York stockbroking, where Jackson spent many years. But they aren’t all that far from western Queensland, where Jackson’s family had cattle interests — alongside a number of butcher shops in Brisbane, where Jackson boarded as a young student.

“I’ve always had an interest in agriculture, cattle and the land, I worked on farms as a youngster, did agriculture as a subject at school and worked as jackaroo and agent prior to university, I like the smell of cattle in the yards,” Jackson says. “What I like about it is that it’s a very dynamic process which obviously relies on the weather, the farming or animal husbandry practices, skills and game plan you can bring to the table. “It has a very tangible product at the end of it and I feel as though over time you can witness the tangible benefits of your own input and work in improving and creating a better outcome.”

After a short stint working as a livestock agent for Dalgety Winchcombe, Jackson returned to Brisbane to study commerce, and began working at the venerable firm JBWere. He jumped ship, moving to Britain where he took up a position at Potter Warburg, now part of UBS, before spending the rest of the decade in New York. “My recollection is that the long lunch was still in play in London at that time. I was fairly young and when I moved to New York. It was a very different environment,” he says.

“The people involved in the financial world in New York were a lot younger, the workload was significantly higher, but the rewards were significantly greater. “Their capital markets are the most sophisticated in the world with the greatest amount of technology being employed as well, so it was seeing the world from the cutting edge.”

It was this experience that pushed Jackson, on his return to Australia, to take a small stake in Maryborough Sugar. “I felt there was an opportunity in agribusiness and agriculture in Australia which at that time was fairly under researched and under-represented on the stock market,” he says. “I felt that Australian agriculture, from what I had seen elsewhere, was actually a competitive business and Australian farmers were globally very efficient.” Maryborough began to expand, scaling the business substantially before becoming MSF Sugar and eventually being acquired by Thailand and Asia’s largest sugar producer Mitr Phol.

That led to Jackson moving on, and with the help of Stephen Chapman of Barron Partners, moving to listed the investment firm Tidewater, which has now become ARC. ARC’s biggest investment has been in Namoi Cotton, but its biggest target is Kidman. The fund has partnered with Shanghai Pengxin, the presumed frontrunner in the $370 million race for more than 11 million hectares of cattle properties.

A decision is expected next month. “The thing about investing in agriculture is that it’s a long-term game. We’re long-term committed,” Jackson says. “We’ll be raising long-term committed capital that will be primarily equity-based — and we see that being a good fit for something like Kidman.”

Fund of funds

King of kings...

They should have a word to Boone Pickens

https://books.google.co.nz/books?id=MrjHQ90O-nYC&pg=PA96&lpg=PA96&dq=Bo…

Bloomberg with some nice things to say about innovation in NZ.

"As for the technology, well, bless the New Zealanders and their willingness to go after seemingly daft—some would argue impossible—ideas. Just in Auckland, there’s a professor named Mark Sagar who has built the world’s most realistic computer-generated faces, making them think and talk, too. There’s Rex Bionics, which has made exoskeletons that let paralyzed people walk again. There’s a gentleman named Ray Avery, who wears all-white and creates low-cost baby incubators and protein formulas for the malnourished from his garage lab. And there’s Rocket Lab—an honest-to-God rocket company that is on the verge of lowering the cost of sending things to space by the most dramatic margin in history. It tests these rockets near a farm on the outskirts of Auckland, and the cows and sheep barely seem to mind."

http://www.bloomberg.com/features/2016-hello-world-new-zealand/

Sadly, from personal experience, to get funding you have to have a lot of funding to start with.

There are plenty of ideas sat idle as the people have golden handcuffs or/and are unwilling to take 5c/hr from an incubator and/or don't have a fortune to show Callaghan to get matched funding.

Fanatic projects with a talented team I have had to put it mothballs (H&S, Bee Keeping Software etc.).

I just ran out of money... lots of clients waiting.. just lack of funds...

Sigh...

Lloyd’s of London reported a 30 percent drop of full-year profit as the world’s largest insurance market was hurt by continued pressure on pricing and the lowest investment returns since at least 2001.

Earnings declined to 2.1 billion pounds ($3 billion) for 2015 as income from investments, primarily in fixed income, sank 60 percent to 400 million pounds with the majority earned in the first half of the year, according to the company’s annual report Wednesday. Weaker insurance pricing in 2015 is expected to continue this year, hurting profitability. Read more

A problem too obvious to ignore and yet, it was. Read more

9.1% return on capital (combined underwriting margin and investment) - where is the problem ? Premium rates will rise to address falling investment returns - over time.

Read this: The rational people are coming up with to go so into debt is going to bite so many in the butt over these next few years.

http://www.stuff.co.nz/life-style/home-property/78087706/first-home-for…

Good on them for giving it a go Justice.......some people wait their whole life-time looking for the right time!!! Life is too damn short to sit back and not give things a go.

I agree notaneconomist that life is too damn short. However that is precisely why no one should spend their entire life burdened with unnecessary debt working like bloody slaves to pay off overpriced properties.

There's a time to be brave and a time to be cautious. We're at the end (or nearing the end) of this cycle, so it is extremely unwise to be brave at this point.

B&T auctions results this week under the hammer:

Central/Bays 20 sold from 36 = 58% success

Manukau 20 sold from 35 = 57% success

These numbers are well down on the 75%+ success rates of mid last year.

Bull markets do not die of old age. They are murdered by central banks. How far away we are from that old adage. The last six weeks have seen yet again central banks responding to further weakness in the world economy, by lowering or at least not raising interest rates and continuing to subsidise the weakest. Wherever they see any sign of distress as with the CDS market in Europe, their response is to believe that risk premiums are unfairly rising and immediately to take action to cancel the effect.

However, several years of watching central banks responding to ever falling productivity numbers by reducing interest rates have shown that they can effect asset prices with their actions, but that not only do they have almost no effect on economic activity, but they positively damage it.

The reason is simple. Banks work, like everyone else, off profit margins and the lower and longer interest rates remain close to zero, the more that net interest margins shrink and the less inclined, because profits are falling, are they to countenance new lending.

http://www.zerohedge.com/news/2016-03-23/why-crispin-odeys-11-billion-f…

So what is the underlying problem? I disagree on your assertion that banks are "like everyone else" as they are solely dependent on "growth" to supply their margin, without growth no one borrows and pays interest in order to benefit now from the future. The underlying problem is that the western economies are in overshoot, importing cheap goods to sustain their habit and the banks are the in the middle, quite firmly the instututions of the status quo when the future aint what it used to be.

I think Western economies can no longer handle the competition from what were once trading partners, now competitors. Left with high cost structures from better times, an inability to adapt due to regulation and existing commitments on over priced assets.

http://www.ibtimes.com/international-wheat-market-russia-set-become-lar…

Andrew, They never could "handle the competition", I said western but really I mean the US lead west, post WWII the US had essentially no competition and in the subsequent decades they have bolstered the head start with a mixture of military and political maneuvers using allies, wars and cold wars to capitalise on it and the oil they once had. Since 1973 the US economy has been in the repetitive cycle of reality checks and denial. To quote James Kunstler this is the long emergenc, its been how long now? seven years?

Hey Neven911, where have you been the past little while? Missed you commenting here, hope you are back.

What are your thoughts on the oil industry today?

I've been watching but only choose to respond to the more interesting posts. Re the oil industry US shale gas moved the wall down the road but did you notice that the recent price drop had a negative rather than positive effect on the US economy, EROEI making itself felt, where the drop in drilling has a bigger effect on US manufacturing (pipe etc) than the plus of lower energy costs to the rest of it. At what point does this collapse?

Some insight into the plight of G-SIBs

If Ben Bernanke and Janet Yellen had the foresight to stop trying to fool the world via “stimulus” that 2005 could be rebuilt and instead worked on removing the wholesale finance burden in favor of more traditional banking, the prospects for a less violent paradigm shift would have been somewhat better – not completely, as systemic resets are going to be messy even under the best of circumstances, but much more hopeful than a eurodollar that decays into who knows what. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.