Here's my summary of the key events overnight that affect New Zealand, with news the Chinese have revealed the massive scale and growth in "off balance sheet Wealth Management Products".

But first, this morning, all eyes are on the release of the US Fed minutes from the February 2nd meeting, seeking out clues about the next benchmark rate rise. Update: These minutes show the Fed is expecting to raise rates "fairly soon" (see p16). The NZD has risen on the news against most currencies.

Meanwhile, American existing home sales rose strongly in January to a 10-year high as confident buyers seemed unworried about the combination of higher prices and higher mortgage rates.

South of the border, Mexico’s economy slowed down a bit in the fourth quarter, but broadly as expected. Mexican GDP growth was +2.1% higher in 2016 than the previous year. Interestingly, the growth rate in the December quarter was higher than this annual rate, although lower than Q3. In 2015, the Mexican economy grew +2.4%.

Also today, we have had a lesson in how long it can take for large trade agreements to become effective. Earlier in the day, the WTO's Trade Facilitation Agreement was finally ratified by the 110 countries needed, and it should usher in an era of reduced border restrictions to trade. The general claim is that it will be more important that any tariff reductions. New Zealand signed up in September 2015. But the original Agreement was concluded in December 2013 in Bali. Of course, all this is slightly ironic in the age of Trump. But the US is also a signatory - one of the first - and there is no recent suggestion that they will back out.

In China, more indications of their wild west financial system - from their central bank. The PBoC is reporting that Chinese banks have more than NZ$5.3 tln of wealth-management products held off their balance sheets at the end of 2016. That is +30% more than a year earlier, and far faster growth than normal lending. This type of financial system leveraging seems out of control in China. No-one is safe if it explodes.

In New York, the UST 10yr yield is currently rising at 2.45%.

Oil prices are lower today by almost -US$1, now just over US$53.50 for the US benchmark, while the Brent benchmark is just under US$56 a barrel.

The gold price is also lower at US$1,232/oz.

And the New Zealand dollar will also start today essentially unchanged at 71.6 USc. On the cross rates we are at 93.2 AU¢, and against the euro at 67.8 euro cents. The NZ TWI-5 index is still at 77.2 and is now the 13th days we have been in this tight range.

If you want to catch up with all the changes yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

37 Comments

china will go to war in the south china sea if their banking bubble bursts. they will use it to instill national pride and cover what they allowed to happen.

and who will NZ side with

Interesting idea. A collapsing regime often uses just such a war as a means of distracting the masses whilst the regime furthers it's control over the populace.

General Galtieri in Argentina used the invasion of the Falklands to distract the masses whilst throwing students out of helicopters over the sea. The parents didn't dare report their children as missing.

Arguably Putin has used the same strategy in Ukraine and Syria, he seems to be popular in Russia despite the mess the country is in.

Which collapsing regime do you refer... US or China? The US has a motivation to bring any miltiary date fwd...before the gap closes further.

http://www.businessinsider.com.au/chinas-military-near-parity-west-2017…

We will be on the winning side. America.

If there is ever a full scale conflict between China and the US - even if no nuclear weapons are involved - there will be no winning side.

http://www.stuff.co.nz/world/americas/89711029/unskilled-and-unable-why…

This is a very good piece on why Trump and the Rust Belt are dreaming if they think lost jobs will return to the US. The infrastructure, skills and knowledge are lost, not to mention the technology that has taken over on a large scale. There has been extensive research done which I'm sure the deluded president will dismiss.

Very true - he cant possibly make America great again. The reason world manufacturing moved to China was cheap coal, cheap labour and lower environmental standards.

ON top of this America's abundant cheap energy resources are gone.

Alternative facts eh? The US is swimming in cheap energy. A war with China and America will be top dog again for the next 100 years.

Yes.

Lets not apply any economic/financial common sense to the problem or pay any attention to the recorded reserves.

You might want to try and picture it like milk ...

The reason the price collapsed when it was high is ... there was a lack of demand for high priced milk! But you cant just turn off the supply like that ... hence a glut....

Similarly ... there is no lack of demand for Oil ... but there IS a lack of demand for HIGH PRICED Oil .. what you are seeing now is the glut before the ugly correction.

The problem is, we can skip our milk on cornies .. we cant skip our Oil

Nymad - heres one for you ... this is what low price does to Oil reserves

https://qz.com/917178/exxon-wiped-19-3-of-its-oil-reserves-off-its-book…

H&E is definitely a victim of alternative facts when it comes to the case of energy resources.

Nymad - Please post some background information that proves your point ... preferably which excludes the technically feasible sources of oil on Mars courtesy of Telsa's new jetpack...

Theres plenty of info out there arguing the opposite. The point you continually miss is ...

The economy needs ever lower prices to prevent collapse ... the Oil companies need higher prices to avoid collapse.

The apparent glut is actually weak demand for Oil at the current price ...

http://www.businessinsider.com.au/breakeven-costs-for-us-oil-production…

http://energyskeptic.com/2017/book-review-of-failing-states-collapsing-…

No one (apart from the Chinese) buys a BMW made in China, though. It is possible to manufacture elsewhere profitably. Heck, BMW themselves started manufacturing in Spartanburg, North Carolina, in 1994. If you drive an X5 you probably drive a car made in the USA.

Not to say that manufacturing isn't usually cheaper in a place without human rights, minimum wages etc. but merely that countries are managing to manufacture various goods quite viably.

Not to mention, when it becomes robots vs robots...how different will the manufacturing costs be then?

My mate in California purchased a new X5, sold it as it kept breaking down on the motorway and he has sworn never to buy another German car.

I know someone who had a similar experience with a Toyota. Toyota ended up buying it back from her, it was so bad.

Lemons seem to happen with any brand. (And on the topic of manufacturing...very few are keen to buy Chinese cars, as of yet.)

They have a lemon law in the states

Lemon Law Presumption*

Within the Song-Beverly Act, there is a presumption guideline

wherein it is presumed that a vehicle is a “lemon” if the following

criteria are met within 18 months of delivery to the buyer or

lessee or 18,000 miles on the vehicle’s odometer, whichever

comes first:

• The manufacturer or its agents have made two or more

attempts to repair a warranty problem that results in a

condition that is likely to cause death or serious bodily

injury if the vehicle is driven;

• The manufacturer or its agents have made four or more

attempts to repair the same warranty problem; or

• The vehicle has been out of service for more than 30

days (not necessarily all at the same time) while being

repaired for any number of warranty problems; or

• The problems are covered by the warranty, substantially

reduce the vehicle’s use, value, or safety to the consumer

and are not caused by abuse of the vehicle;

• If required by the warranty materials or by the owner’s

manual, the consumer has to directly notify the

manufacturer about the problem(s), preferably in writing.

The notice must be sent to the address shown in the

warranty or owner’s manual (for bullets 1 and 2).

If these criteria are met, the Lemon Law presumes that the buyer

or lessee is entitled to a replacement vehicle or a refund of the

purchase price. However, this presumption is rebuttable. The

manufacturer may show that the criteria has not been met (for

example, because the problems are minor) and therefore, the

buyer or lessee is not entitled to a replacement vehicle or refund.

You will have caught up with Andrew Newman's "resignation" today. Rex Graham is passing it off as differences over Ruataniwha. But the timing and some of Graham's comments on RNZ this morning strongly suggest Newman was fired (with lots of face saving words).

http://roadsratsrates.blogspot.co.nz/2017/02/first-and-probably-only-ca…

I think he was fired, may be some conflict in his joint role. I think there are more to follow.

The CEO of HBRIC has already gone? And I noted that, even after the Inquiry bollocksed HBRC for withholding evidence about the Mangateretere Pond, Stephen Schwabey was still giving sworn evidence claiming failures in HDC's bore. (The independent scientific caucus have now poured cold water on that idea). I can't see him lasting much longer either unless he gives it up.

Rick ... have a read down here and note China's coal usage boom during the last 10 years ...this cheap coal is what drove the shift to China in manufacturing in general.

https://ourfiniteworld.com/2017/02/20/oops-the-economy-is-like-a-self-d…

This is a good article worthy of discussion, but it is a long bow he is drawing to state that it is too expensive re-establish industries.

The article clearly identifies the downside of globalisation and the free market - in that in the greed for easy money, multinational conglomerates will always take their business to the environ were the cost of business is least, thus costing jobs in their markets. Yes technology does cause lost jobs, but who is making the robots?

Nations still face the dilemma of how to employ the majority of averagely educated and skilled population. The alternatives are rising crime, and bigger prisons - a huge waste of taxpayer funds. But caused by failed socio-economic policies. None of our political parties have an answer, Trump will at least cause the conversation to begin, but at what cost?

This type of financial system leveraging seems out of control in China. No-one is safe if it explodes.

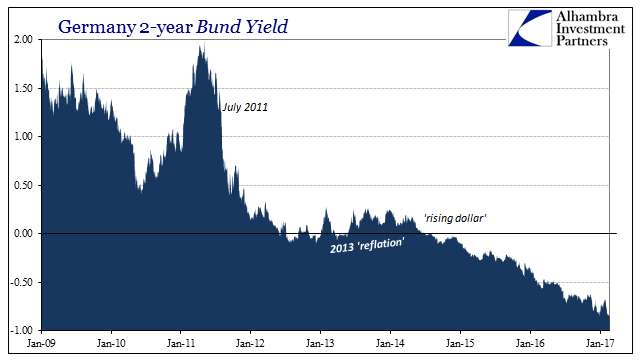

Is all well in Europe, I think not?

Despite “reflation” of late, German 2-year federal paper has kept marching along in nearly a straight line down that goes back in time to the middle of 2014. It is all the more compelling since nothing in finance no matter how well-established and intense ever moves in such a regular fashion. As such, there is absolutely no value in receiving -0.92% in “yield” for holding this instrument, the record low “yield” achieved at yesterday’s close. The value or motive for doing so is derived from other considerations (and not the ECB buying them in QE), considerations put right out in the open on the post-crisis chart for the German 2s.

{kind=link}

As I wrote this morning (subscription required):

What you see above is pure liquidity preferences being carried out in a most extreme manner. Financial participants, mostly banks, are buying shorter bunds not because the ECB is or because they are worried about populism, but rather because they know all-too-well why populism has taken root. It is all right there in that chart, going back to July 2011 when everything changed. It is practically the same chart, if obverse, as the pattern we find in eurodollar futures that shows us exactly the same behavior with slightly different proportions and irregularity along the way.

If the euro breaks up it won’t be because of Marine Le Pen in France or Brexit spreading to other nations. The risks to the euro are risks because the global economy has failed, and further authorities have displayed only a determined unwillingness to do anything (of substance) about it. Banks hoard liquidity, driving up its price long past fundamental value, because they are faced with a paradigm of all risk and no opportunity. This perception was driven home in the middle of 2014 in a way that should have been universally recognizable, but still to this day remains obscured by politics most of all (including the politics of Economics).

The possible breakup of the euro is a symptom of the same cause as the growing appeal of populism, which is the same as you see in Chinese money rates. The global economy doesn’t work, the prime element behind those, as a symptom of the still larger cause of an unstable global currency regime that is more unstable and illiquid today than last year. Read more

Dealers scrambling to acquire the premier currency of US shadow banking at 49.5 bps yesterday, below the the Fed's most recently declared official rate corridor for unsecured funding, is hardly edifying. View Table.

NZ Trade Minister seems pretty happy on that WTO result:

Trade Minister Todd McClay has welcomed the entry into force of the WTO Trade Facilitation Agreement (TFA) saying it is a big win for New Zealand exporters.

“The TFA will benefit all New Zealand exporters and is particularly good for small and medium sized enterprises. The TFA reduces the cost, administration and time burden associated with getting products across borders and into the marketplace,” Mr McClay says.

“New Zealand’s agricultural exporters will also benefit significantly from a provision to hasten the release of perishable goods within the shortest possible time.”

The TFA works by simplifying and streamlining customs and border processes as well as addressing some key barriers that exporters face when doing business abroad. It was ratified by New Zealand in 2015.

“This is a win for trade liberalisation, and the WTO, in the face of growing concerns around protectionism,” Mr McClay says.

“A credible and effective WTO is important for New Zealand. The Government is committed to pushing for better access and great fairness for all New Zealand exporters and the TFA is an important part of this.”

“This is a win for trade liberalisation, and the WTO, in the face of growing concerns around protectionism,” Mr McClay says.

I think Mr McClay needs to widen his understanding that free trade was/is a function of financialisation, in so much that banks created excessive trade funding at the outset for the right price for them to facilitate that which has since withered dramatically in global harmony under the weight of costs attached to such initial largesse.

{kind=link}

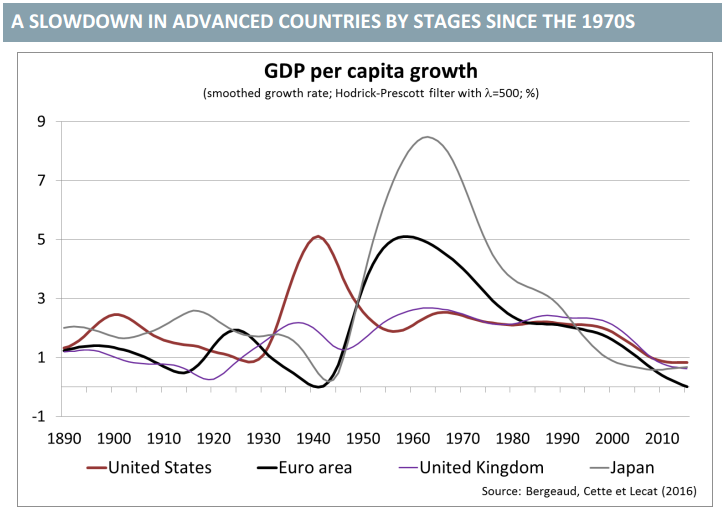

For the first time in modern world history, GDP per capita growth has become synchronized in the worst possible way. There have been economic problems before, but never before so sharp and uniform. Economists and policymakers have no answers for this, which isn’t surprising since it already by its existence questions the competence of these economists and policymakers. Read more

Mr McClay just repeats what his advisors tell him, not sure he understands that capital flows must balance trade flows. For that matter, and much more worrying, I'm not sure his advisors do either. They probably studied economics and think a balance sheet is an obscure accounting term.

I'm afraid that any time you talk with an MP you discover that you are talking to an empty vessel. There is only ever a minority of MPs that have the capability to form a thought, let alone understand anything.

I somehow think the intellectual rigour required to get his head around it could well be beyond Mr McClay. And besides, he'd likely see his job to merely convince a constituency to keep faith with the status quo.

But what does really frustrate me with respect to the situation we find ourselves in, is that those with the intellectual rigour that I know seemingly refuse to entertain, let alone study, Marxian economics as a means to pursue possibilities and seek answers to today's problems. It is such an un-academic response not to seek to inquire or to entertain the possibility for the need for paradigm change.

I just don't get it.

thats because it isnt a problem. Its a predicament.

https://ourfiniteworld.com/2017/02/20/oops-the-economy-is-like-a-self-d…

Studying Marxist economics sounds somehow naughty these days. I have a problem with most of it as it seems to be mainly people sticking to outdated ideas about how things work, rather than about how things actually work (eg, a Frenchman concludes that capitalism is unequal. Who would have thought?). I do like Michael Hudson, particularly his insight that the Finance, Insurance, Real Estate and Legal economy functions differently from the Production/Consumption economy and differently again from the Government economy.

To me it's more about interest groups and their relative power at any one time. I just cannot see the interests of a factory owner as opposed to the interests of the factory workers, most of their interests are shared.

LOL "naughty". Point is, Marxian political economy is an historical framework for the analyses of crises in capitalism - and historically of course, this is not the first crisis, nor the first/only change in the nature of capitalism since it replaced mercantilism;

Marxist political economy typically recognizes three great periods: laissez-faire capitalism around the middle of the 19th century, monopoly capitalism toward the end of the 19th century and imperialism that lasted perhaps until the Second World War. The 70 years since the war have been very difficult to categorize, not least because of the extraordinary Long Boom that lasted until the early 1970s, with unprecedented growth rates, rising incomes and greater equality. The Long Boom has been followed by four decades of indifferent growth, often stagnant incomes and rising inequality. In my view, financialization is a term that adequately characterizes this period. Its dominant feature has been the extraordinary rise of finance, which has come to penetrate areas of economic and social activity previously relatively distant to it.

Hardly scary stuff :-)

http://www.truth-out.org/news/item/21383-costas-lapavitsas-discusses-th…

Overshoot and finite resources is where its gets scary. Not to mention we are all totally trapped into dependence on an industrial machine which is totally reliant on ongoing supply of Oil Coal and gas.

Thinking and sharing nicely wont solve anything when overshoot really comes into play

https://medium.com/@End_of_More/an-infinity-of-futility-ecb8c4edc887#.q…

China has been a real worry for some time , and I have my doubts about how long it can carry on doing as it pleases without consequence

So long as their population doesn't murder them then the Chinese government can keep doing what they are doing forever. They don't need permission from anybody to print their own money.

But they cant keep printing for long

1) without causing (further) massive capital flight ....

2) because their overseas denominated debt would become impossible to service and

3) among other things they need OIL .. which is priced and traded in US$$.

"money is a function of energy

energy is not a function of money

using printed money without the relevant increase in raw energy supply does not increase gdp

if it did, we could all repair each other’s shoes and take in each other’s washing, pay each other with helicopter money as much as we wanted and all become billionaires. this is obviously ridiculous.

there is a complete absence of awareness of the link between energy and money-flow."

You might want to read up about the petrodollar before suggesting Zimbabwe type monetary reform

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.