Here's my summary of the key events from overnight that affect New Zealand, with news Chinese debt distortions are spreading.

But first in the US, data on their labour market, retail sales and industrial production all suggest their economy regained momentum at the start of the second quarter. But expectations of a sharp rebound seem unlikely as their goods trade deficit rose +3.8% to US$68 bln in April amid a drop in exports. Rising inventories in both the retail and wholesale sectors are also weighing on growth.

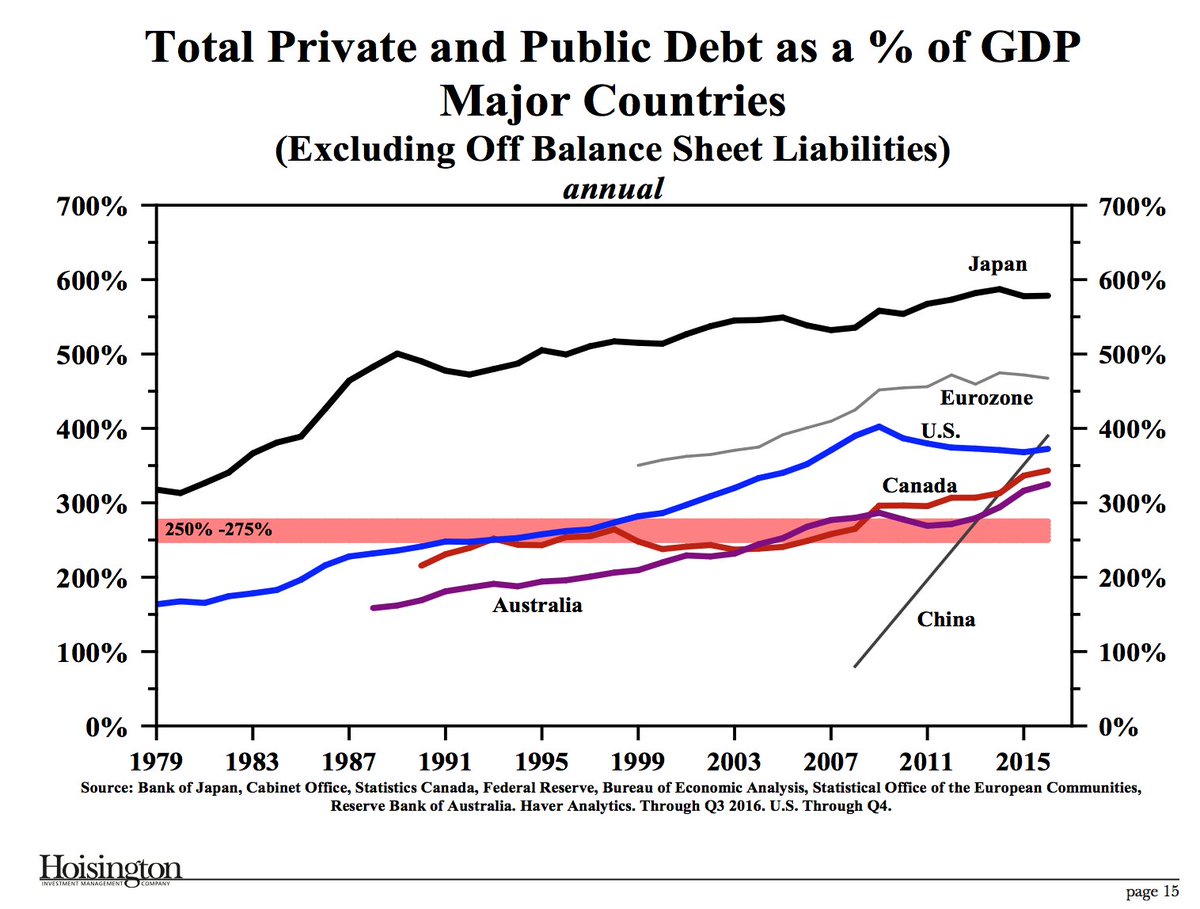

In China, the number of companies issuing US dollar debt is rising and the values are ballooning. Chinese companies pay higher yields which attracts bond investors, but the sheer size and sudden rush into this is 'impressive', and not necessarily in a good way. This Chinese debt suddenly now exceeds a quarter of all emerging market corporate dollar debt.

{kind=link}

In Australia, Moody's is reporting that default rate for securitised car loans is rising. In fact one Liberty tranche has a weighted-average 30+ day delinquency rate of 9.02% at March, up from 7.74% at December. However, the average was much less at 1.72% but up from 1.43% in the prior quarter.

And staying in Australia, one of their leaders in the export education industry has close collapsed. Classes have also been cancelled for 15,000 students at 13 campuses across the country. The event is sure to sour the reputation of this sector and affect New Zealand in the primary markets from where students are recruited.

And there is big trouble in the Melbourne apartment market. Chinese investors are pulling out accentuating the downturn. Around 5,000 new apartments are expected to be completed and up for sale this year. But 80% of Chinese buyers will not be able to settle because they can no longer get finance. They either forfeit their deposits and abandon the sale or sell at a loss.

In New York, the UST 10yr yield is still at 2.25%. The yield inversions in China have unwound today with the yields for their government 2, 5 and 10 yr debt all now at 3.69%.

The price of oil fell sharply today. The US crude benchmark is now back under US$49 a barrel, while the Brent benchmark is just under US$51.50. OPEC has extended its agreement on output cuts until March 2018 but markets are highly sceptical this move will be effective.

Gold is basically unchanged at US$1,256/oz.

Meanwhile, the Kiwi dollar is been holding its own, supported by positive views of the NZ budget and fiscal situation and is now at 70.3 USc. On the cross rates the Kiwi is at 94.3 AU¢, and 62.7 euro cents. The TWI-5 index is still at 74.6.

And bitcoin is higher again, but only marginally today at US$2,501.

If you want to catch up with all the changes yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

7 Comments

China entered the party late but its catching up fast

https://pbs.twimg.com/media/DAl1Tb9XYAEWXLk.jpg

{kind=link}

Ozz car loans could be interesting. Because of the way leasing and novated leasing is sold to everybody (some Australian firms are here doing it now).

Its sold as car and ute payments & fuel running costs coming from before tax income. But for salary & wage earners and the newly sub contracting? Aside from Drs and lawyers - always done it.

Course everything has to be new.

Course big assumption is the resudual value - and in the future.

"Wallets shutting across the country - Belt tightening causes heartburn in retail and auto"

http://www.afr.com/business/retail/belt-tightening-causes-heartburn-in-…

Welcome to debt-serfdom, the only possible output of the soaring cost of living for the unprotected many who are ruled by a hubris-soaked, subsidized Protected Elite.

The Consumer Price Index (CPI) measure of inflation is bogus on a number of fronts, a reality I've covered a number of times: though the heavily gamed official CPI is under 2% for the past four years, the real rate is 7% to 12%, depending on whether you happen to live in locales with soaring rents/housing and healthcare costs. Read more

Foreign investment in the Australian housing market and lots of Australians with crushing mortgage payments taking 50%+ of their monthly income is going to hit their economy hard. It sounds like debt deflation is in full swing over there.

In China, the number of companies issuing US dollar debt is rising and the values are ballooning. Chinese companies pay higher yields which attracts bond investors, but the sheer size and sudden rush into this is 'impressive', and not necessarily in a good way. This Chinese debt suddenly now exceeds a quarter of all emerging market corporate dollar debt.

The national offset/hedge might present itself in data revealing the PBOC has been replenishing it's foreign reserves with significant US Treasury purchases over recent months. Read more

But first in the US, data on their labour market, retail sales and industrial production all suggest their economy regained momentum at the start of the second quarter. But expectations of a sharp rebound seem unlikely as their goods trade deficit rose +3.8% to US$68 bln in April amid a drop in exports. Rising inventories in both the retail and wholesale sectors are also weighing on growth.

Hmmmmm....

This is why the Fed is currently seeking to “raise rates” and maybe even runoff its balance sheet while its models tell policymakers the expected growth rate isn’t even 2%. They currently figure a trajectory of just 1.8% that is very likely, given the latest drop in the unemployment rate without any uptick in wages, about to be downgraded still further at the next statistical update. From that view of the world as it really is, a pitiful state by any standard, let alone that it has happened following the worst economic contraction since the Great Depression, a 3% economy just might sound laughably insane. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.