Here's our summary of key events overnight that affect New Zealand, with news all about China today.

But first, American housing starts fell more than expected in December, recording their biggest drop in just over a year. Markets were expecting starts on new housing to run at an annual rate of 1.275 mln units but the data showed a rate of only only 1.192 mln units. The construction of single-family housing units had an especially steep decline although the December numbers follow two months of hefty gains. The saving grace in this data is that building consents issued are holding steady.

As expected in China, they announced a strong GDP growth of +6.8% for 2017, and well above Beijing's target for the year of +6.5%. There may be sceptcism about Chinese numbers, but not that 2017 was an improvement.

Housing sales in China hit a new record in 2017, both in terms of area and transaction value. 1.7 bln square meters of residential properties, worth NZ$2.9 tln were sold in the year. The figures are +7.7% and +13.7% higher, respectively, than in 2016, giving an indication of how strong the price rises were. But the data also shows a clear cooling by the end of the year.

Also cooling a little in December were Chinese retail sales. But for all of 2017 they totaled NZ$7.8 tln in the year and that compares to US retail sales of NZ$7.9 tln. Chinese retail grew +9.4% in 2017 while American retail grew +4.2% so it is clear that the size and importance of the Chinese consumer will be greater in 2018. The world clearly has two major drivers of growth and trade now. This is an important change and transition.

Another important shift in China is that per capita income is growing at different rates between 'average' and 'median', indicating a strong rise inequality. The Average growth was +9.0% in 2017 and a faster pace, but the Median growth was +7.3% and a slower pace. Unless reversed, this tension will catch up with them. What is striking is the speed of the change.

And finally, among the data was an indication of how tough their environmental challenges are. Electricity production was up a strong +6.0% in 2017 and much of that was because they burned more thermal coal. They may be making green power progress, but it isn't turning the tide. And if 2018 brings higher growth as seems likely, the consumption of coal isn't going to decrease.

In Australia they have been hit with an unwelcome surprise. Their already stratospheric household-debt-to-income ratio was thought to be 195%, but a recent change to include self-managed super funds properly has seen it balloon to 199.7%. SMSFs are a debt magnet so I hope we don't adopt that option here. By the way, the equivalent NZ ratio is 167%, which is high enough thank you. Fortunately, ours has been stable for all of 2017.

Back on Wall Street, the UST 10yr yield is up +4 bps at 2.61% today, and that is approaching a four year high. The UST 2yr is near a ten year high. Bond investors will be sweating on losses. The equivalent 10yr China sovereign bond is up another +1 bp at 4.04%. The equivalent NZ 10yr sovereign bond is up +5 bps at 2.94%. And there was a another fall in the premium investors need for NZ Govt credit default swaps, and that is now just +12.9 bps and a new record low.

Oil prices are little changed again today with the US benchmark now just over US$64 a barrel, while the Brent benchmark is now under US$69.50.

Gold is down -US$7 today to US$1,329/oz.

The Kiwi dollar is marking time this morning and is now at 73.1 USc. On the cross rates it is at 91.5 AUc, and against the euro at 59.7 euro cents. That puts the TWI-5 at 74.5 and little changed from this time yesterday.

There were more big movements in cryptocurrency markets. Bitcoin has risen strongly over the past 24 hours after its crash yesterday. Today it is at US$11,770 and up +US$1770 or +17.8% in the past 24 hours.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

13 Comments

NZ and AU miss out - suckers

Apple takes advantage of the new tax code that President Trump signed into law last month. A provision allows for a one-time repatriation of corporate cash held abroad at a lower tax rate than what would have been paid under the previous tax plan. Apple, which has 94% of its total stash of $269 billion of tax-haven profits held outside the United States, said it would make a one-time tax payment of $38 billion on the repatriated cash

https://www.nytimes.com/2018/01/17/technology/apple-tax-bill-repatriate…

A tax rate of 14% going off those numbers. Their employees paid much more.

"The New Zealand Dollar: Compilation of Major Bank Forecasts, Currency Views for 2018"

Some very interesting comments from the international banks on New Zealand.

https://www.poundsterlinglive.com/nzd/8237-the-new-zealand-dollar-compi…

I think those 'analysts' just show how shallow their view is. They couldn't be further away from here if they tried. Their perspective is once-over, very lightly and I would be suspicious. They still think NZ has some relationship with Europe. But years ago, NZ's economy moved on to an Asia/AU/US focus. Someone forgot to tell them ...

David, so you don't think currency traders are influenced by the views of Morgan Stanley, JP Morgan etc?

Shallow indeed but that article doesn't talk about links to Europe at all - what were you referring too?

And tourism is a slightly larger export than dairy these days.

Interesting.

"Over the next 3 years, the minimum wage is expected to increase 20%. Higher wages should lead to more spending, growth and price pressures that should drive the New Zealand dollar higher."

And yet:

The conference delegates also examined why growth in German wages remains so weak -- a key concern for the ECB as it tries to the generate the sustained inflation that will allow it to end its emergency stimulus measures for the region.

Weidmann said migration from other European Union member states is partially responsible for muted wage pressures, and that labor unions are playing a part by insisting on reduced working hours and more training instead of higher pay. But he also noted that low pay growth is a widespread phenomenon, affecting countries including the U.S., the U.K. and Japan.

“When it comes to modest wage growth in the face of tight labor-market conditions, Germany is by no means unique,” Weidmann said. “This suggests that the factors responsible for holding back wage growth are not only idiosyncratic, but at least partly international as well.” Read more

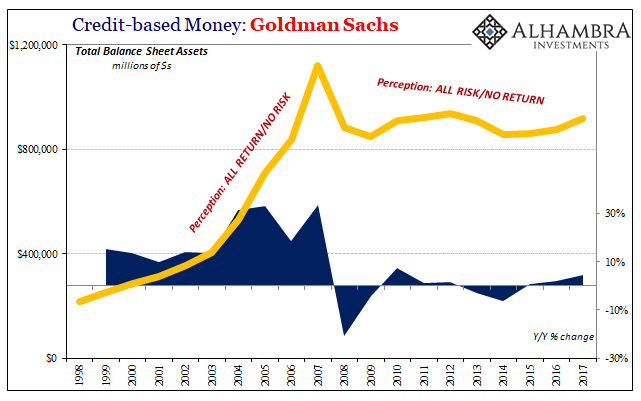

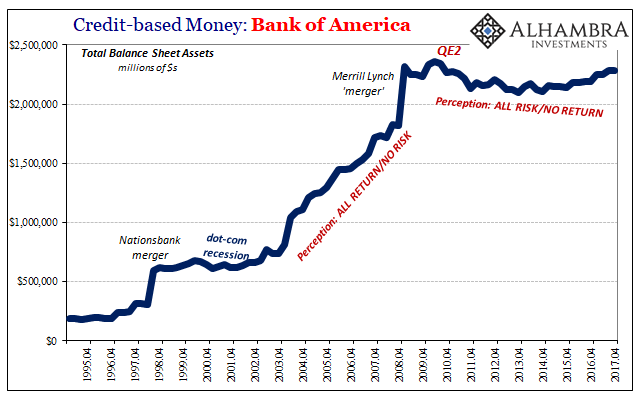

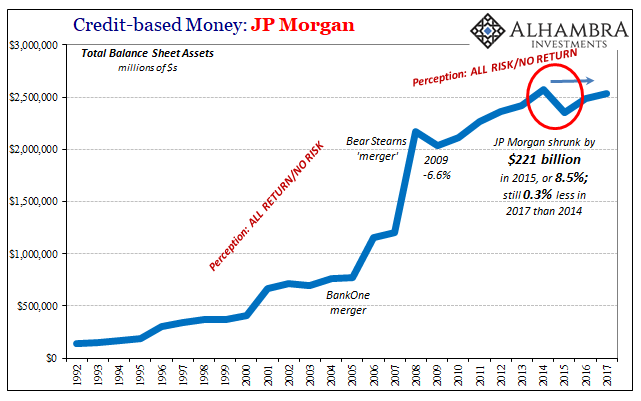

If inflation is considered a monetary phenomenon are large US banks part of the problem rather than the solution? View total balance sheet assets of Goldman Sachs, Bank of America and JP Morgan Read more

{kind=link}

{kind=link}

{kind=link}

The downward trend on GDT as shown in the graph on gingerninja' link saw an upward movement in the last 2 GDT results.

https://www.globaldairytrade.info/en/product-results/

"SMSFs are a debt magnet so I hope we don't adopt that option here." Apart from the compulsory acquisition of funds from wage and salary income it is exactly what we have here. All those mum and dad speculators have just done it themselves. That is their super fund, they are managing it and doing it, mostly with debt.

They [China] may be making green power progress, but it isn't turning the tide. And if 2018 brings higher growth as seems likely, the consumption of coal isn't going to decrease. [my emphasis]

Elements of Fonterra's energy use policy exhibit the same coal consumption trend.

Bathurst Coal has successfully appealed in the Environment Court against a Selwyn District Council order to reduce the number of truck movements at a mine at Coalgate, inland from Christchurch.

The company supplies Fonterra's milk processing factory at Darfield with about 65,000 tonnes of coal a year and may increase the amount over coming years. Read more

By the way, I'm liking your move away from more sombre business attire, David. The 'shirt aesthetic index' is at all-time highs, and trending up!

Taxpayers will be forced to hand over nearly £200bn to contractors under private finance deals for at least 25 years, according to a report by Whitehall’s spending watchdog.

In the wake of the collapse of public service provider Carillion, the National Audit Office found little evidence that government investment in more than 700 existing public-private projects has delivered financial benefits.

The cost of privately financing public projects can be 40% higher than relying solely upon government money, auditors found. [my emphasis] Read more

Is there evidence that New Zealand's flirtation with off-balance sheet PPP financing of public works offers better outcomes than those revealed in the UK, beyond diverting public scrutiny away from the government's actual cash outflow exposures?

As expected in China, they announced a strong GDP growth of +6.8% for 2017, and well above Beijing's target for the year of +6.5%. There may be sceptcism about Chinese numbers, but not that 2017 was an improvement.

Hmmmm...

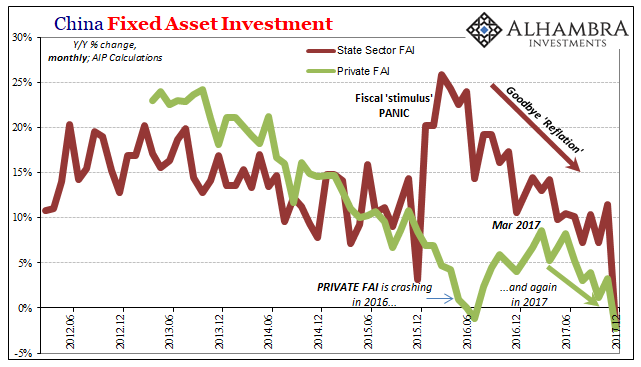

How much China imports sets the agenda for the rest of the global economy beneath it on the supply chain. Which potentially means: no acceleration in top level global growth (despite it being, purportedly, synchronized for the first time since 2007), lower Chinese exports, less manufacturing growth, reduced need for additional ghost cities, lower FAI as fewer will be constructed, leaving less of a need to import material.

The link in the economic chain immediately before imports is Fixed Asset Investment. FAI drives everything in China, and is driven by Chinese perceptions of the global economy. It is for China’s internal economy what China’s economy is for the worldwide system. Read more

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.