The Reserve Bank does not see rising international interest rates as a major concern for households in New Zealand, as long as there are no “abrupt changes” in the international market.

In its twice-yearly Financial Stability Report, the central bank again outlined the high level of household debt in New Zealand as the “largest single vulnerability of the financial system.”

Although, in part thanks to loan-to-value ratio (LVR) restrictions on home loans household debt has moderated recently, it remains at an all-time high.

The Reserve Bank has previously outlined this as an issue, citing issues of homes being highly leveraged and vulnerable to any increases in interest rates.

Speaking to reporters on Wednesday Bernard Hodgetts , the Head of the Reserve Bank’s Macro-Financial Department, said households could probably cope with an increase in interest rates.

“The issue really comes about if we get an abrupt change in interest rates,” Hodgetts says.

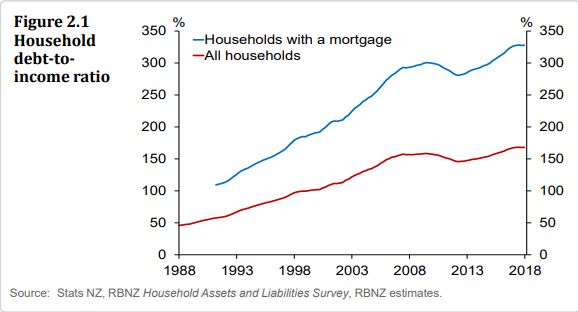

He says there are still a lot of households with high debt to income ratios (see graph.)

“Those are the sort of borrowers that could struggle if interest rates were to move up abruptly.”

Reserve Bank Governor Adrian Orr says the central bank is “positively pursuing” adding debt-to-income (DTI) restrictions to its macroprudential toolbox, through the RBNZ Act Review currently taking place.

Hodgetts says the Reserve Bank is “very conscious” of the risk to highly leveraged households if markets react negatively to “dramatic tightening of monetary policy that we’re seeing around the globe.”

In its March forecasts, the US Federal Open Market Committee was split on whether to lift rates two or three additional times this year amid an improving economic outlook and rising inflation.

As long as things go according to plan, Hodgetts says “the household sector generally can cope with it.”

Good and bad tightening

Orr followed Hodgetts’ comments by outlining the difference between good, and bad interest rate tightening.

“Good tightening is if central banks are gradually raising interest rates because economic activity in those countries is behaving as they currently project,” he says.

This could be due to improving economic growth, for example.

“Good tightening” is well signalled in the Reserve Bank’s central projections.

“Bad tightening,” on the other hand, is more of a concern.

Orr gives the example of what happened overnight with the Italian elections, where suddenly markets got spooked and risk premiums rose.

But, he says the risks of this happening on a much wider scale are “very small – they’re not part of central projections.”

Speaking to MPs during the Finance and Expenditure select committee, Orr said he was pleased to see an improvement in the banking sector around how banks are funding themselves.

“They are borrowing more internally long-term, rather than short-term and they are funding themselves more from domestic deposits, rather than more international borrowing.”

He says this is a “fantastic movement” that makes the Reserve Bank feel more comfortable about the ability of the banks to weather unanticipated events.

Meanwhile, Orr says the BNZ’s major service loss over the weekend – caused by the power loss at its parent bank National Australia Bank in Australia – is an “excellent example of the operational vulnerability of banks.”

“It is one of those trade-offs of efficiency vs certainty,” he said when asked about BNZ's implementation of the Reserve Bank's outsourcing policy.

“In this case, were they aware and ready enough to have independent business continuity plans that could manage for that particular risks?

“But we have got a very, very big work programme ahead of us, around making sure that large, important banks are operationally capable on their own within New Zealand.”

68 Comments

Can they handle a recession?

They can - they have safe high paying jobs with the government!

The rest of us - unlikely.

how many of these so called safe Govn jobs? National spent 9 years "cleaning them out" so really the few left? wont matter.

On the contrary...many of these jobs still needed doing, but - if MBIE was anything to go by - were apparently converted into contractor roles rather than permanent. So they ended up costing far more than permanent employees but the desired reporting was achieved.

Isnt that a good Q. For me a recession or even a depression are far more likely than significant inflation which in fact I see as zero chance.

Who? Ecobird, Tothepoint, Double-GZ, Zach? No I wouldn't have thought so, that is why they're not here today. Too busy meeting RE agents to get their portfolios on the market...

Who? Ecobird, Tothepoint, Double-GZ, Zach? No I wouldn't have thought so, that is why they're not here today. Too busy meeting RE agents to get their portfolios on the market...

Hi Nic Johnson,

You're wrong on two counts:

i) I don't ever meet with real estate agents. I always avoid them.

ii) In the current market, I'd much rather buy property than sell property.

I guess you're getting used to being corrected.

TTP

TTP - shall we replay some of our previous discussions, or have you forgotten them again??/ you old folk do get grumpy when you get things wrong don't you or forget the details...

.....( Alzheimers is a bugger for these babyboomers and I do feel a bit sorry for them, they get so easily mislead into bad decisions)

Okay TTP.. here's what happened, You bought another house, do you remember TTP that nice man Andrew King said it would be a good idea??? Okay its not really a house, more like a drafty shed in Auckland, but you liked the nice man, do you remember???? You re-mortgaged your home, yes Agnes is in a nursing home now .... and it seemed like a good idea but ANZ now want their money back because it's all gone wrong in Australia and they're not lending 7 times income anymore... I know its not your fault you didn't have any income but that's their new rules..... Where's Andrew?? No sorry Andrew left after he got his commission for the re-mortgage.. don't know where he is now... but, you have a choice now TTP. Go and live in the shed? or join Agnes in the nursing home? ANZ want the house! I'm sorry

Thankfully the alzheimers should kick in again..

Any time you want a replay TTP - I'll put it on tape for you, so you remember.

Goodnight TTP.

Nic Johnson,

The real question is that do they understand the article and the potential ramifications of issues raised in the Financial Stability Report by the RBNZ? It requires an understanding of macro-economics, and most residential property investors do not have an understanding of macro-economics - most may have chosen to not understand macro-economics, or may not have the time to learn and understand macro-economics.

If they understood the issues raised by the Financial Stability Report of the RBNZ, then perhaps they could discuss their viewpoints and address the issues that the report raises in an intelligent and informed manner.

My observations are that most of the Auckland property price bulls comment frequently on articles regarding property prices, property auctions, etc, yet infrequently make informed comments on macro-economic related articles.

Meanwhile those that have an understanding of the macro-economic issues raised in the Financial Stability Report and an understanding of a credit bubble have a much more cautious outlook on future property prices in Auckland.

Good.Bring on higher interest rates for the savers!

Being forced to sell because of something to do with the loan is a sign of a borrower not coping!

Not necessarily, alot of those might have high incomes.

Its the people who have some how been allowed to have a DTI of 7 or more that are in the danger zone and given that the median house in Auckland is somewhere around 8x the median household income, there could be a few of them

"As long as things go according to plan, Hodgetts says “the household sector generally can cope with it.”

So, things need to go according to "plan". If things do go according to "plan" the household sector "generally" will cope. Ok ...............................

Haha.

I'm not at all convinced either. Its so waffley and lightweight that I'm actually more worried than I was!

Sounds a bit flimsy from the governor. Good and bad interest rate rises are all the same to a borrower who's got too much debt Would also be good to know the DTIs of the worst 20th percentile are. Medians and averages are almost meaningless.

Yeah, I didn’t find the distinction a particularly compelling one

Translated

Good rate rises - ones controlled from the RBNZ

Bad rate rises - from market forces, the RBNZ will not be held responsible

In short a proactive deflection of blame

I strongly disagree with the title:

"RBNZ Governor Adrian Orr is confident NZ’s highly indebted households can withstand interest rate rises"

I believe a 2% rise in retail interest rates would lead to 20% of borrowers being insolvent and another 40% having to drastically tighten spending to meet mortgage payments. This would of course lead to mortgagee sales and much lower spending so people can meet their interest payment obligations. A bit down the line a proper recession would follow

Sheesh, and you’re a permabull. Do you realise what you have just said? A 2% rise in rates seems to me relatively modest over the medium term. And if this happens, you’re are predicting a meltdown?! Wow

If you have a million dollar mortgage a 2% increase costs you an additional $20,000. If you don’t have $20,000 you default. How many of these million dollar mortgage households do you imagine are carrying a spare $20k.

Hardly any, would be my pick

You make it sound like they just need to find $20K.. It would be a bit more serious than that having to find it every year.. A slow bleed. What you'd probably find if that was the case is that those heavily indebted folks would end up selling out and moving back in with their paretns (or the babyboomers who created the mess in the first place) bit more density of household use with three generations in one house but more houses freed up to ease the housing shortage. The market always reverts back to balance eventually even if it is painful getting there.

So its in balance now with people living in uninsulated garages with no loos?

Even $500k mortgages. 2% increase = $150 - $200 additional per week. Earning enough money to withstand that increase is one thing, but seeing those extra interest dollars going out every week/month would be very hard to stomach.

That's always been my view Bobster. It's also why I believe interest rates are NOT going to rise in the future. Humans (and governments) generally don't like to self-harm. Rising interest rates by 2% and precipitaing the country into recession is a bit like sticking a knife in your own hand, not likely to happen

"Humans generally don't like to self-harm." Have you ever worked for a Multi-National Corporate?

Yvil,

If the inflation rate rises, then the RBNZ is mandated to raise interest rates to keep inflation in the 1-3% target range. Recall the period when CPI rose from 2004-2006 and went above 3% in September 2005 and resulted in interest rate rises from 2006 -2007.

Sounds more like wishful thinking to me, bit concerned by the prospect of interest rises Yvil? Maybe you shouldn't have bought things you can't afford ;)

Yvil - I’ll call that wishing thinking or even naive. Remember that the majority of Kiwis aren’t borrowers and when the equity markets ultimately correct and investors are having to live off interest rates, understand that there is pain. Also understand that if inflation gets away, pain is required to put it back in place, and you don’t want to be one of those especially if its for an extend period which will be a death knell for the over-leveraged. Thats not the forecast but if you rely on forecasts youre a far bigger risk taker than me and clearly not an observer of forecasts reliability - some people do not understand risk, and for many that’s what ultimately makes them, or kills them.

Yvil, it's not simply about OCR and headline bank rates.

When banks assess risk more thoroughly, many more borrowers will discover that they can no longer access the headline rates.

This is what I think will be much more likely than serious RBNZ tightening.

It very much looks like banks are going to be required to demonstrate more restrained lending practices and more vigorous borrower affordability evaluations. This has already been happening since 2017 but the pressure is going to increase.

Now if you have a good income and low outgoings, you should be fine. You'll get the great rates. But how many FHB's and late-to-the-game-specuvestors took on huge mortgages 9 or 10 times their exaggerated income in 2015/16? And when their fixed rate periods end, and they need to apply for another loan, but now the banks have tightened and are assessing more thoroughly, suddenly they can't get away with exaggerating their income, suddenly they can no longer access the headline rate and are stuck on the variable rate. These are the kinds of people who will struggle.

This could can also lead to price falls, even without the above stretched borrowers needing to sell up or being forced to sell....because the maximum lending is reduced, so some of the froth evaporates and there are less people who can match the high prices.

When prices fall you will also see investors who have relied on cross collaterisation of equity gains to leverage up and buy more property running into problems with LVRs. So it’s not just a servicing issue.

And yes I agree, when there is a reduction in aggregate mortgage credit prices will fall. This is happening already in Aussie.

Reminds me of so many hubristic central banker quotes before. Mr Bernanke was very confident that the real estate crash in the US was contained and wouldn't pose any major systemic problems.

Mr Greenspan did not believe in the dotcom bubble at all and assured everyone on numerous occasions that it wouldn't blow up.

Both of them ascertain that if they hadn't done what they had done the world would have ended. Something I would dispute and something that is conveniently impossible to prove. It is only their opinion.

"Bad tightening", in Italy not having wider implications, is absurd. This is the 7th or 8th largest economy in the world. It is too big to fail and too big to bail out. It will collapse the Euro and throw the entire global economy into chaos. It is already being bailed out via the backdoor to the tune of hundreds of millions of euros a month...and it is still failing. It's debt is too high to service and the Italians, rightly or wrongly are sick of Europe and sick of trying to service it.

"Bad tightening" as a term is ridiculous. How can tightening by the market, which is lead by real views on the credit risk of a country be bad? It is actually correct. Italian bonds are crashing because they cannot pay back their debt. Ever. It is impossible. they can't even pay the interest, and that is with the help of the ECB (another hubristic arrogant central bank) forcing their interest rates artificially low. So if their already poor situation deteriorates further why is it "bad" that their rates go up? It is absolutely logical and correct.

Bad tightening is the politically skewed mumbo jumbo, voodoo economic machinations of central bankers. They talk in riddles and spend hours debating the use of a single word in minute of a meeting. Do they really believe that this is the best way to define the cost of money? Or to measure credit risk? As if what they say about something changes the fundamental mathematics of the situation?! Do they really believe if they pull lever a they will get result b? As if the economy is a perfect machine that they can manage with one lever. Am I the only person who thinks this is ridiculous and clearly not the case?!

It is a perfect example of the arrogance of central bankers and the inherent fallacy of our central bank lead system, that they believe they can understand credit risk better than the people who actually own / trade it.

Numerous studies have shown that financial instability has increased since the introduction of the federal reserve. The price of money is possibly the most important price in our society. Why do we leave it to a bunch of pseudo science "intellects" who have no real world experience and who are quite clearly politically pressured. Why is it we don't have a central bank for the price of cars, or planes or houses? Because price controls do not work. So why would we believe they work in this case when again and again they are shown to get it completely wrong?

The way I see it the terms "good" and "bad" are being used by someone who is over simplifying things to the extent that if certain things happen, it is actually wrong. Oversimplification like this is often done by those who like to think of themselves as being extraordinary communicators. But in reality they are going way too far (whether they know it or not) and it could well end up being very embarrassing.

Boom. Powerful post.

Do they really believe if they pull lever a they will get result b? As if the economy is a perfect machine that they can manage with one lever. Am I the only person who thinks this is ridiculous and clearly not the case?!

Yes, and if the economy is a closed box that dances to the beat of the price of money, why do we need humans to run it anyway? Surely, mathematical computation and machine learning would be more appropriate.

It is a perfect example of the arrogance of central bankers and the inherent fallacy of our central bank lead system, that they believe they can understand credit risk better than the people who actually own / trade it.

Like Dunning Kruger for Smart People (or should I say institutionally adept people with good educations)

So why would we believe they work in this case when again and again they are shown to get it completely wrong?

We shouldn't. But change means wholesale changes to the status quo. Too many reputations and egos are at threat.

You are right JC, I let my exasperation with this get the better of me.

But we don't need machine learning, we just need to let the market decide how much a NZD is worth. Not a central banker. The market does not fail, it is merely a mechanism for deciding a price. It is people that fail. So we should get them out of the equation, when ever possible. And I recognise it is not always possible.

Alan Greenspan was treated like some sort of superstar God of economics and money. But all he did was flood the world with credit when things looked bad. That was it, his only trick. And it did nothing but kick the can down the road. No one called him on it then and it still seems no one can call him on it now.

I guess he spoke in an obscure enough fashion that he could never be blamed for anything. But covering your arse is hardly a marker of success. And it does not make for good decisions.

Change is tough. Tough for me too. I have kids and people I care about. Do I want to see bloodshed and revolution, homelessness, poverty, a great depression a world war? Not at all. I like to think I have empathy. But it seems like it's the only way things change. They get so bad......until people can't handle it anymore and they rise up. It is the ultimate, repeating pattern of human history.

We all know this is bullshit. We all know the Western economy has become a sham. But what do we do? What can we do? Me ranting on here isn't helping anything for sure.

Hope for the best and prepare of the worst I guess.

Good luck everyone.

The assumption that human behaviour is rational is itself irrational - that if we do A, the people will do B, when in reality they will do C or ....Z.

Totally.

Efficient market, my ass.

I'm curious as to why the statement places such high relevance on 'abruptness'.

Most of those who are at highest risk of default are in fixed-income roles. If/When Interest rates go up, and they start to go backwards (Expenses > Income), is there a real distinction between it happening over a week, or a year?

A long slow drag would help avoid panic in the streets, but if people are over-leveraged and rates go up, it will get them eventually!

Death by a thousand cuts or a bullet to the head?

At least there is hope up to the 999th cut

The Chinese would give opium to the victim as well so it wasn't all bad.

This is ridiculously optimistic. If interest rates go up 2% there are going to be a lot of people who will be crushed. And the impact on consumer spending and therefore GDP will be significant.

Arnt we led to believe lenders are stress tested up to 7% mortgage rates???

Hardly is referring to borrowers, not lenders

Most servicing calculators from the banks add 2% or so to current rates. The point is that if you cannot afford to pay that, you shouldnt borrow. Rates went down by a larger delta, so what prevents the reverse? Most interest rate drivers are global anyway and RBNZ is generally powerless against them - up or down

In theory maybe but then again there are brokers involved and there are one or two liars out there.

Hardly - Correct there will be real hurt - but its happened so many times in the past and will again, the question is, when it eventually happens again will you be one of those, as in the past, still claiming it cant happen as they go under weather ? This time is different right ? read the book

325% DTI for households with mortgages...risk No 1.

“But we have got a very, very big work programme ahead of us, around making sure that large, important banks are operationally capable on their own within New Zealand.”.....The Oz banks are over exposed. Risk no. 2.

International economic shock exposing our over leveraged position eg italy, trade war, brexit you name it. Big risk no 3

Low interest rates heading into a recession...risk no. 4. The list is long.

This was all very obvious and foreseeable years ago as we binged on banks throwing cheap money around.The RBNZ, banks, govt and we as the irrational exuberatants are all at fault.

Maybe we should consider the moments of the distribution here.

Figure 2.1 is completely ignorant to regional and demographic factors.

Essentially the older generation with (relatively) pittance mortgages dragging down the average DTI ratio will be fine.

The younger generation with astronomical mortgages will be stuffed.

But don't worry because as we use a broad average as validation, everything will be fine.

caveat emptor

The buyer should be aware of of the possibilities of rate changes to their mortgages.

To take on astronomical mortgages is foolish, and a fool and their money are soon parted!

You can have cheap money, and you can have tight regulation of the banks by the RBNZ (via macro-prudential measures) which then restricts bank lending, particularly to high risk sectors of the economy.

We still have cheap money, however we have had credit tightening due to the tightening of debt servicing criteria to mortgage borrowers and property investors, and bank loan growth limits to certain borrower types. This tightening of loan underwriting criteria was by APRA in Australia which they applied to the Australian banks and they in turn applied them to their NZ owned banking subsidiaries.

This concentration of 40% of mortgages by 8% of households is very concerning.

If this small proportion of borrowers faces financial stress, then there could be a mass sale of the underlying investment properties at the same time causing property prices to decline due to large number of properties sold under distress and desperation or as a mortgagee sale - there is your supply of properties coming onto the market (you don't need newly built supply in this scenario), overwhelming market demand.

It could also put the financial system at risk if the bank loan losses are sufficient to erode bank capital, which then might result in an injection of capital by the Australian parent banks. However if the Australian parent banks are also capital constrained (due to their own credit bubble), then the NZ banks may be sold off to another buyer who can inject capital, or the NZ government may need to inject capital into the NZ banks (which means more government borrowing to finance the bank recapitalisation like the case in Ireland in the GFC), or at worse, the open bank resolution (OBR) is put into place which means that bank deposit holders, lose a portion of their deposits and get shares in their bank as compensation. A whiff of an OBR might even cause a run by deposit holders - especially large corporate treasurers ...

If the debt to income (DTI) measures had been previously implemented by regulators and finance ministers on the NZ banks (and enforced by regulators), getting to this precarious and fragile situation, and hence risk to the financial system in NZ may have been avoided.

To restore confidence in the banking system, there should be the results of stress tests on the bank capital and liquidity ratios which are made publicly. The key test variables would be a recession, with a high unemployment rate and a fall in property prices to see if bank capital is adequate in such a scenario.

In the late 1980's, early 1990's banks in NZ had problems loans in the commercial property sector and look at the recession and impact of that. The BNZ needed capital from the NZ government which then sold it to the Australian parent. The housing sector is a much bigger part of bank loan books today than the commercial property sector loans were back then.

The safety of the entire financial system should be the primary concern of the bank regulator and never be secondary to bank profits or the vested interests of politicians who wish to get re-elected and want a booming economy (which requires bank lending) to stay in favour with the voting population (a recession causes financial pain and resentment by the voting population with the incumbent and typically results in a change of government).

Too late now. DTI ratios should have been put in place in the Southern Hemisphere post 2008/2009. They weren't and the issue has been magnified beyond belief.. Its like RBS and Northern Rock on speed and generally they stopped at 5 and 6 six DTI. Introducing them now however would merely speed up the inevitable collapse. Far better to gradually introduce them year on year as the market naturally deflates its excesses. A period of time on life support with the chance of recovery is a preferable to just switching off the machine.

Aug. 15 (BusinessDesk) - Prime Minister Bill English ruled out giving the Reserve Bank authority to use a debt-to-income ratio tool as part of a suite of macro prudential tools to prevent a housing market crash and said it should look at removing some of the curbs that are already in place as some of the heat comes out of the market.

http://www.scoop.co.nz/stories/BU1708/S00501/pm-says-theres-no-need-for…

This month Finance Minister Steven Joyce said he wanted a full cost-benefit analysis of the proposal and was cautious about giving the Reserve Bank more tools to address the risks it identified in the financial system.

https://www.stuff.co.nz/business/89506431/Banks-say-Reserve-Bank-has-mi…

Yea and abolish interest only mortgages.

"This concentration of 40% of mortgages by 8% of households is very concerning"

I'm not so sure about that. This just means that there are few people at the top who own the majority of assets, hence also a large chunk of mortgages.

Example, if I have 20 Mill mortgage with 50 Mill worth of assets, I'd probably be in that 8% but I wouldn't be considered high risk, being geared at only 40%

Yvil,

Do you have any statistics on the LVR on that group of households as a whole? For the entire group, it is likely to be higher than 40%.

There are many stories of property investors engaging in deposit recycling / equity release (as taught by many property mentors) - which is basically a euphemism for borrowing more money on their existing property which has risen in market value (usually to max out to maximum allowable LVR levels) to use as an initial deposit for another investment property. So together with that deposit (which itself was borrowed ) and a mortgage on the newly purchased property, they have purchased the property with 100% bank financing thereby increasing their whole combined LVR ....

From the RBNZ Financial Stability report

1) Household indebtedness remains high

Indebtedness is particularly high for new homeowners and for property investors

Household sector indebtedness has increased since 2011, coinciding with significant growth in house prices, and debt is now at a record high (figure 1.1). Indebtedness is particularly high for new homeowners and for property investors. These borrowers are particularly vulnerable to rising interest rates or a change in financial circumstances. A significant deterioration in households’ debt servicing capacity, particularly accompanied by a fall in house prices, could cause significant loan losses for the banking system

2) the RBNZ is concerned about a self-reinforcing cycle in property prices both on the upside and downside in Auckland

The rise in household debt since 2012 has coincided with a sharp rise in house prices, particularly in Auckland.

The simultaneous rise in household debt and house prices could partly reflect a self-reinforcing cycle, where bank lending has boosted house prices and, in turn, higher house prices have supported more bank lending, by increasing the value of homeowners’ collateral.

But this cycle can also operate in reverse, driving down bank lending and house prices. This negative interaction can amplify the financial stability impact of a household income shock, by lowering collateral values and reducing households’ ability to service their existing debts by increasing their borrowing

You mean there are a few people who that have been duped into the responsibility of servicing the banks debt. The big question really is, how many of that 8% who own 40% of the debt have been using negative gearing to service the debt? What happens when they can't?

Anyone who has overleveraged themselves are at great risk and they will bite the dust if trouble arises. My point was that 8% owing 40% of the debt sounds like they must be overleveradged but it's not necessarily the case. It's well known that the 5% of richest people own 90% of assets, therefore it's also likely they own a large chunck of debt. This debt is large comapred to the overall debt, say 40% but it may not be that large compared to the assets owned, maybe under 50%, therefore they are not as high risk as originally assumed.

Is that clearer?

One thing we know with certainty from history after you strip aside all the noise is that projections and forecasts are only projections and forecasts. Unpredictable shocks have always been the cause of major recessions and delinquencies. They have happened in the past and will continue with certainty to happen without warning in the future. Lets not forget 2008. I reiterate my past comments and continue to chime the alarm on high indebted businesses and individuals. Be wary of unpredictable shocks not the warnings that can easily be predicted and hide behind the blanket of comforting words like.....'don't worry folks you'll be fine...., BUT only if things happen the way they should.....".

^^ exactly PatrickW ^^ the issue should not be constantly looking for signs on the horizon of bearish or bullish sentiments, but making sure that whatever the weather, households, corporations and banks are in good enough shape to survive the shocks that will undoubtedly happen at some point or another.

Households, as indebted as they are now, and with 40% of lending concentrated in only 8% of households, is not an example of good shape.

I actually like that statistic of 40% of debt in 8% of households in that when things go badly, it will be a small minority of households that are completely screwed. This gives me hope that the majority of households will fare well when we have the proverbial unpredicted shock to the system.

8% of households is still quite a few households so I imagine there won’t be a shortage of sob stories on stuff.

Nowadays, stuff reminds me of the old US rag national enquirer, as the journalistic integrity appears to be similar.

I believe Stuff hire journalism school drop outs as a sort of “second chance initiative”. They’re paid a commission based on clicks.

Again, 8% owing 40% of debt sounds like they will be in trouble but they may well not be. We have to comapre debt with overall assets (LVR), not debt to overall debt. Example:

John owes 4 Million and has 10 Million of assets

11 other people each owe $545k and each have $600k of assets

Well John has 40% of the overall debt but he won't be in trouble cause his leverage is only 40%

The other 11 people on the other hand will be in trouble being leveraged at 90%

I hope that's clearer

The OBN is alive and kicking to keep the sham prosperity going strong.

Every one plays their part at the right time with the right pronouncements.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.