Content sourced from the World Gold Council*

Gold is becoming more mainstream.

Since 2001, investment demand for gold worldwide has grown 18% per year, on average. This has been driven in part by the advent of new ways to access the market, such as physical gold-backed exchange-traded funds (ETFs), but also by the expansion of the middle class in Asia, and a renewed focus on effective risk management following the 2008–2009 financial crisis in the US and Europe.

Today, gold is more relevant than ever for institutional investors. While central banks in developed markets are starting to normalise monetary policies – leading to higher interest rates – we believe the effect of quantitative easing and the prolonged period of low interest rates can have a long-term effect.

These policies may have fundamentally altered what it means to manage portfolio risk and could extend the time needed to meet investment objectives.

In response, institutional investors have embraced alternatives to traditional assets such as stocks and bonds. The share of non-traditional assets among US pension funds has increased from 17% in 2006 to 27% in 2016.

Many investors are drawn to gold’s role as a diversifier – due to its low correlation to most mainstream assets – and as a hedge against systemic risk and strong stock market pullbacks. Some use it as a store of wealth and as an inflation and currency hedge.

As a strategic asset, gold has historically improved the riskadjusted returns of portfolios, providing returns while reducing losses and providing liquidity to meet liabilities in times of market stress.

A source of returns

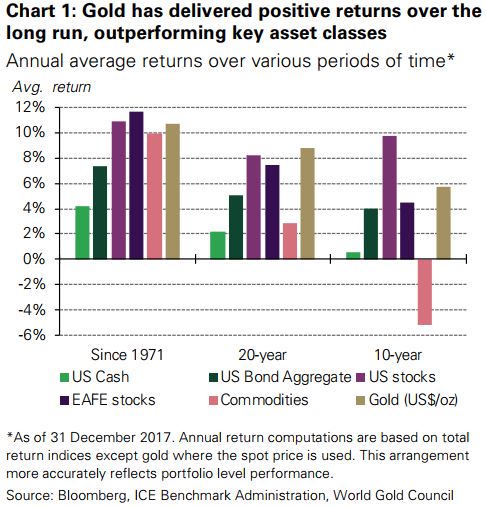

Gold is not only useful in periods of higher uncertainty. Its price has increased by an average of 10% per year since 1971, when gold began to be freely traded following the collapse of Bretton Woods.

And gold’s long-term returns have been comparable to stocks and higher than bonds or commodities (Chart 1).

There is a good reason behind gold’s price performance: it trades in a large and liquid market, yet it is scarce.

Mine production has increased by an average of 1.6% per year for the past 20 years. At the same time, consumers, investors and central banks have all contributed to higher demand.

On the consumer side, the combined share of global gold demand from India and China grew from 25% in the early 1990s to more than 50% in recent years.

Our research shows that expansion of wealth is one of the most important drivers of gold demand over the long run. It has had a positive effect on jewellery, technology, and bar and coin demand – the latter in the form of long-term savings.

Gold-backed ETFs and similar products have amassed more than 2,000 tonnes (t) of gold worth almost US$100 billion since they were first launched in 2003. And central banks have been net buyers of gold since 2010 as a means of diversifying their expanding foreign reserves.

Well above inflation

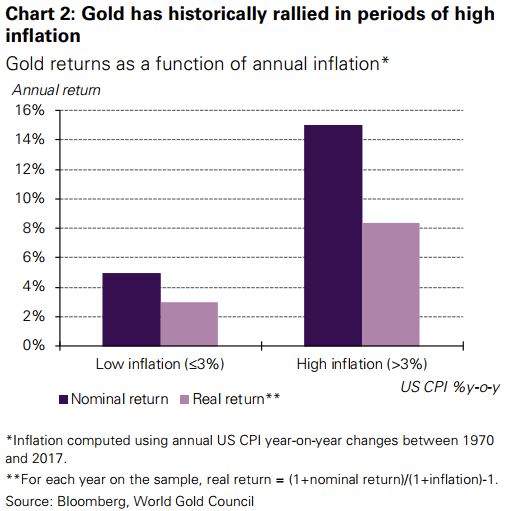

During the Gold Standard and subsequently the Bretton Woods system, when the US dollar was backed by and pegged to the price of gold, there was a close link between gold and US inflation. But once gold became free floating, US inflation was not its main price driver. Sure enough, gold returns have outpaced the US consumer price index (CPI) over the long run, due to its many sources of demand. Gold has not just preserved capital, it has helped it grow.

Gold has also protected investors against extreme inflation. In years when inflation has been higher than 3%, gold’s price has increased by more than 14%, on average (Chart 2). Additionally, research by Oxford Economics shows that gold should do well in periods of deflation.

A high-quality, hard currency

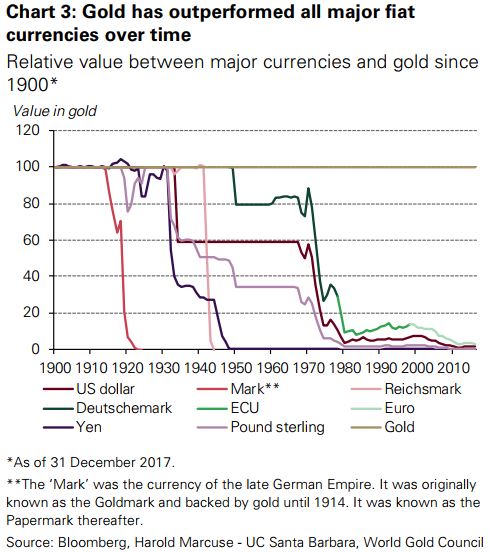

Over the past century, gold has greatly outperformed all major currencies as a means of exchange (Chart 3). This includes instances when major economies defaulted, sending their currencies spiralling down, and after the end of the Gold Standard. One of the reasons for this robust performance is that the available supply of gold has changed little over time – growing less than 2% per year through mine production for the past two decades. In contrast, fiat money can be printed in unlimited quantities to support monetary policies.

Diversification that works

Most investors agree about the relevance of diversification, but effective diversifiers are not easy to find. Correlations tend to increase as market uncertainty (and volatility) rises, driven in part by risk-on/risk-off investment decisions. Consequently, many so-called diversifiers fail to protect portfolios when investors most need it.

For example, during the 2008–2009 financial crisis, hedge funds, broad commodities and real estate, long deemed portfolio diversifiers, sold off alongside stocks and other risk assets. This was not the case with gold.

Gold historically benefits from flight-to-quality inflows during periods of heightened risk. By providing positive returns and reducing portfolio losses, gold has been especially effective during times of systemic crisis, when investors tend to withdraw from stocks (see Appendix II). Gold has also allowed investors to meet liabilities while less liquid assets in their portfolio were undervalued and possibly mispriced.

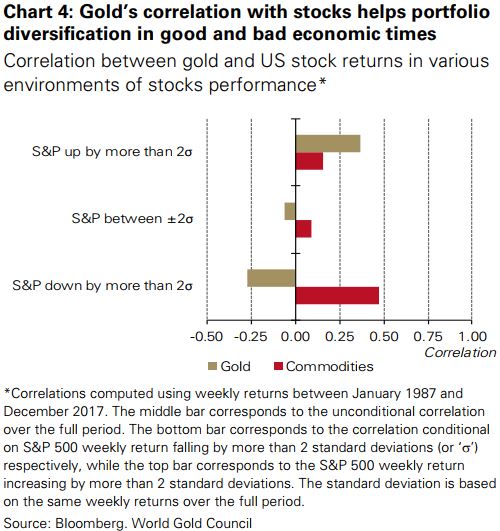

The greater a downturn in stocks and other risk assets, the more negative gold’s correlation to these assets becomes (Chart 4). But gold’s correlation doesn’t only work for investors during periods of turmoil.

Due to its dual nature as a luxury good and an investment, gold’s long-term price trend is supported by income growth. As such, our research shows that when stocks rally strongly, their correlation to gold can increase driven by the wealth effect and, sometimes, by higher inflation expectations.

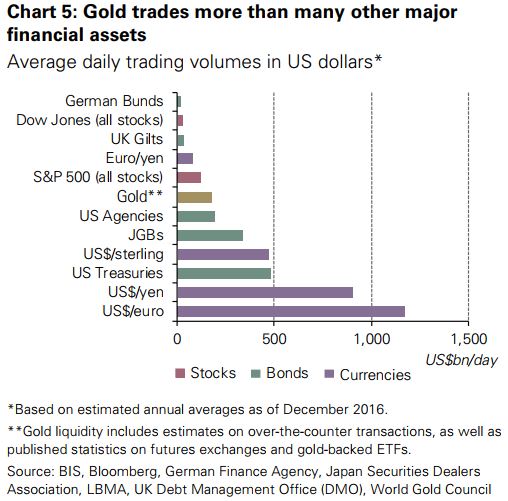

A deep and liquid market

For large buy-and-hold institutional investors, size and liquidity are important factors when establishing a strategic holding.

Gold benefits from its large, global market. We estimate that physical gold holdings by investors and central banks are worth approximately US$2.9 trillion, with an additional US$400 billion in open interest through derivatives traded on exchanges or over-the-counter.

In addition, the gold market is liquid (Chart 5). Gold trades between US$150 billion and US$220 billion per day through spot and derivatives contracts over-the-counter. Gold futures trade US$35–60 billion per day across various global exchanges. Gold-backed ETFs offer an additional source of liquidity, with the largest US-listed fund trading an average of US$1.2 billion per day.

Enhancing portfolio performance

The combination of all these factors means that adding gold to a portfolio can enhance risk-adjusted returns.

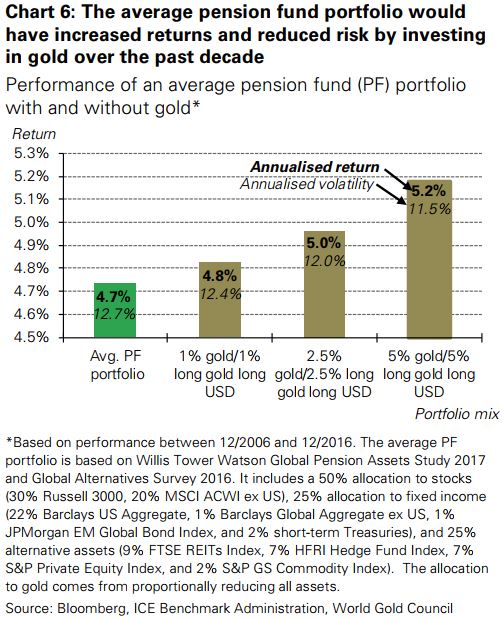

Over the past decade, institutional investors with an asset allocation equivalent to the average US pension fund would have benefitted from including gold in their portfolio. Adding 2%, 5% or 10% in gold would have both increased returns and reduced volatility, resulting in higher riskadjusted returns.

But looking at the past performance of an average portfolio alone is not enough to answer how much gold investors should add to achieve the maximum benefit to a portfolio.

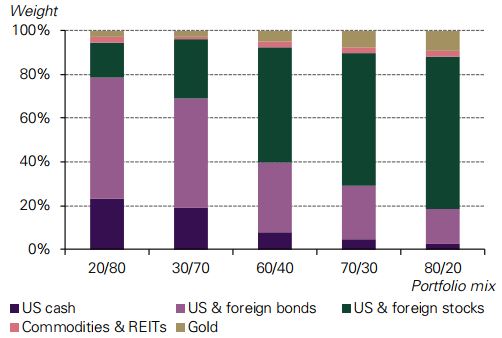

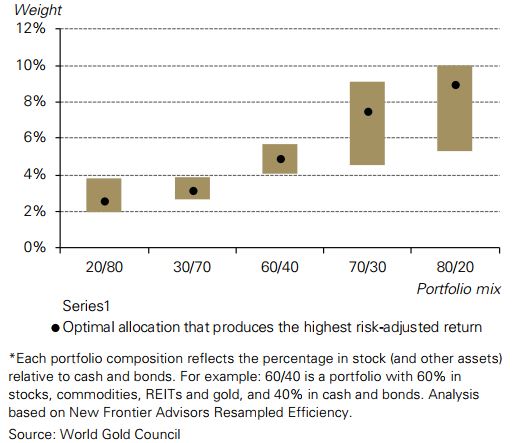

Portfolio allocation analysis indicates that, for most US dollar investors, holding 2% to 10% of their portfolio in gold can improve performance even more (Chart 7). Broadly speaking, the higher the risk in the portfolio – whether in terms of volatility, illiquidity or concentration of assets – the larger the required allocation to gold to offset that risk.

The analysis shows that gold’s optimal weight in a portfolio is statistically significant even if investors assume an annual return for gold between 2% and 4% – well below its actual, long-term historical performance.

This is also the case for investors who already hold other inflation-hedging assets, such as inflation-linked bonds, as well as for investors who hold other alternative assets (e.g., real estate and hedge funds).

Gold goes beyond commodities

Gold is often lumped together with the commodity complex by investors and investment practitioners alike. Whether as a component in a commodity index (e.g., S&P Goldman Sachs Commodity Index, Dow Jones UBS Commodity Index), one of the securities in an ETF, or as a future trading on a commodity exchange, gold is viewed as a part of this complex.

Gold undoubtedly shares some similarities with commodities. But a detailed look at the make-up of supply and demand highlights that the differences outnumber the similarities:

• The supply of gold is balanced, deep and broad, helping to quell uncertainty and volatility

• Because gold is not consumed, its above-ground stocks dwarf the stock levels of other commodities

• Gold demand comes from a wide range of segments and regions

• Gold has a lower correlation with the global business cycle.

Gold’s unique attributes set it apart from the commodity complex. From an empirical perspective, including a distinct allocation to gold has improved the performance of portfolios with passive commodity exposures.

Chart 7: Gold can significantly improve risk-adjusted returns for portfolios across various levels of risk

(a) Long-run optimal allocations based on asset mix*

(b) Range of gold allocations and the allocation that delivers the maximum risk-adjusted return for each portfolio mix*

This article is a re-post from here. The original article also hase detailed Notes, and an Appendix of further information.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

4 Comments

Where can I get a bitcoin kiwisaver fund? Adding bitcoin to your pension fund over the last decade would have increased volatility and sent your retirement to the moon. It has out performed all fiat currencies since it's inception.

If the World Gold Council is suggesting pension funds keep "paper" gold options on their books then one must ask how much of this bullion is actually in the vaults anyway? Sure HSBC say it's in their vault, but would you really trust them? Supposedly there are more ounces in gold options than there are in actual gold.

Maybe you need to learn about risk, volatility, legal regulations, and investing. You are not going to find a gambling on horses kiwisaver fund for the same reason,... wait no major horse races normally have better standards than most of the cryptocurrency market right now.

Not even Bitcoin faithful would consider any cryptocurrency risk instead of their retirement fund other investments, because speculating all in wildly on unregulated markets is not the smart long term option.

https://www.reddit.com/r/Bitcoin/comments/7s8kyh/vanguard_ceo_just_said…

After all the frauds, scams, hacks, crashes, volatility, whales diving, technical issues, lack of scalability, high fees etc you would be lucky in a decade to remain unscathed by any of them. Even miners have not had a good time of it, and the GPU market (while good but potentially risky for the Nvidia and AMD co.) has been terrible for the customers.

I dunno, my brother swears by the NZ lotto kiwisaver option.. he "invests" $30 a week..

Lotto is far more accessible & glitzy to NZders and far less complex, (which is probably also the appeal). It is not what you win but the potential to win that keeps people going back to it. If it required more technical research or had returns based on the invested amount then it would definitely lose the gloss.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.