Here's our summary of key events over the weekend that affect New Zealand, with news investors have been jolted by more capricious policy stances.

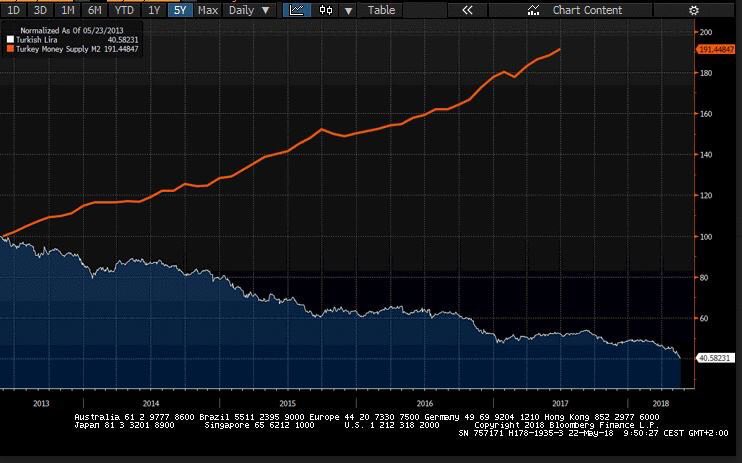

Wall Street ended last week down sharply as investors reacted negatively to the way the American Administration is dealing with its relations with Turkey. The Turkish lira is being pressed lower, quicker, by a culture war spat. That is undermining investment in the country, especially by some large European banks, and that in turn is unnerving investors in other systemically important banks. Wall Street was down -0.8%. US bank stocks were down as much as -2.5%.

Meanwhile US inflation rose +2.9% in the year to July. This is the largest annual increase since September 2008. Even though the US Fed prefers the PCE inflation measure, today's CPI data is sure to be reflected there too showing US inflation is rising quite quickly now. Even without food and energy, US inflation is up +2.4%.The US Fed will likely raise rates sooner and probably next in September.

But their inflation is now rising faster than wages as new 'real income' data shows, take-home pay buys less than it did a year ago. The cost of petrol actually rose an eye-popping +25.4% in the past year. Fuel oil rose more than a third. These are serious jumps and will impact how households allocate their spending.

And the US Federal deficit came in slightly worse than analysts expected. The July deficit was -US$76.9 bln, making the full deficit for the past twelve months an eye-popping -US$784 bln. In fiscal 2017 the deficit was -US$665.8, so this current year is running -18% worse and will reach -3.9% of GDP. That will make it the highest ever for a non-recessionary period.

In contrast, Canada reported strong employment growth in July (+54,100) and well above analyst forecasts. Their jobless rate dipped as well. Pay rose +3.0%, a little less than in June, but well above their inflation rate of +2.5%.

In China, their car market shrank in July, the first drop in fourteen months as consumers shifted away from American cars due to the escalating trade spat.

Japan's economy returned to growth in the April-June quarter after having contracted in the first three months of the year. The turnaround was due to a rise in household spending and an increase in corporate investment.

Locally, the big news is the sharp re-calibration of the wholesale interest rate market. Friday brought sharp falls across the whole curve on top of those on Thursday. That takes the two year rate back to levels we last saw in August 2016. The five year swap rate is now back to levels last seen in October 2016, and the ten year is back to November 2016 levels. One thing that hasn't reverted however is the curve; we are now just under +90 bps for the 2-10 curve and it has been like that for more than a year.

Meanwhile, international rates are on the move lower for their separate reasons. The UST 10yr is weaker and now at 2.87%, down -6 bps from the previous day and pushing their 2-10 curve lower, now under +26 bps and erasing the steepening of the past month. Remember this curve was positive +120 bps at the start of 2017 so its been basically downhill since then. The Aussie Govt 10yr is at 2.59% (down another -4 bps), the China Govt 10yr is at 3.57% down -1 bp, while the NZ Govt 10 yr is at 2.61%, dropping -2 bps on top of the previous day's -6 bps and the day before's -9 bps. That is a major reset.

Gold is down another -US$1 and now a just on US$1,211/oz in New York.

US oil prices are higher and now just over US$67.50/bbl. The Brent benchmark is now just over US$72.50/bbl. The US rig count is sharply higher this week chasing those higher oil prices.

The IEA is warning that even though oil markets seem to be in a period of relative calm, a storm might be looming later this year when new American sanctions work to slash supplies of Iranian oil.

The Kiwi dollar is starting the week very much weaker at 65.8 USc, after a -5% fall last week. On the cross rates we are now just under 90 AUc again, and at 57.6 euro cents. That puts the TWI-5 at 69.8 and a three year low.

Bitcoin is now at US$6,299 which is -1.7% lower than where we left it on Saturday. In the past two weeks bitcoin has lost more than a fifth of its value (-22.1%).

This chart is animated here. For previous users, the animation process has been updated and works better now.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

21 Comments

http://www.abc.net.au/news/2018-08-06/banking-royal-commission-not-to-b…

"There is no doubt credit is tighter and pressure is building on interest rates.

The most immediate cause is that those who lend to our banks from offshore have discovered a few concerning weaknesses in our financial system.

Having for years been assured of the rock-solid foundations of Australian lending standards, global wholesale markets have been keenly watching revelations from the royal commission. They now see increased risk. And they are charging accordingly.

The red line in the graph below charts the premium that wholesale lending markets are charging Australian banks. It's now at its highest in more than a decade. The other factor making offshore lenders twitchy is the drop in our housing prices.

Given our banks are glorified building societies with up to 60 per cent of their loan books devoted to mortgages over residential real estate, a sustained drop in housing prices would unsettle foreign lenders.Our real estate obsession has created another problem. Household debt now is at world-record levels. Combine that with record-low wages growth, and the only way Australians can maintain themselves is by running down savings.

The blue line shows just that; the widening gap between deposits and loans. Put the red and blue lines together and the supply of credit certainly is tightening. Less supply, ultimately, usually results in higher prices. In this case, that means rate hikes."

https://ci4.googleusercontent.com/proxy/MU0Nm9it7WeuW93caeynYKzXEoTC17U…

{kind=link}

Isn't this a bit like Turkey, but with a well run country (yes, I know it's the Aussies, but compared to Turkey)? In both cases there is a chunk of foreign debt that is going up in value and in cost at a rapid rate. This has to be sorted out as the 90 day Eurodollar loans roll off, assuming that's where the wholesale lending came from. At this point the preferred option is to repay the Eurodollar loan and replace it with a local currency loan. This creates downward pressure on the exchange rate and upward pressure on local deposit rates, presumably.

Now, this may not be the mechanism, but if it is, then is there any reason for it to cause a break in the chain of payments rather than a steady adjustment? This is clearly where Aussie and Turkey differ. In Turkey the dictator's supporters get lent Turkish lira, his enemies go bust and bought by his mates. Standard purge tactics as perfected by Vlad next door. Thanks for your link yesterday for that bit of the pussle.

Breaks in the chain of payments in Aussie? In the UK they had Carillion, here we had a couple of near misses with Fonterra and Fletchers where the breaks were manageable, and a direct hit with two major builders. So who is overindebted and losing money? Are Fonterra and Fletchers fatally weakened, so that they cannot take the next blow?

Less supply of offshore borrowing for banks will results in higher interest rates for mortgage borrowers, who would then have to dip further into their savings to fund the extra borrowing costs leading to a wider funding gap.

This self-sustaining vicious cycle will result in a financial crisis, unless higher wage growth kicks in. RBA has written off wage growth as unlikely in the near term as the slack in workforce is on an upward trend with continued record migration and a larger share of employment creation coming from new part-time jobs amid the rise of gig economy.

Not necessarily. It could be cheaper rates for some mortgage borrowers and higher rates for others. As far as I can tell that is what has happened in the UK, where someone on a high salary can borrow at 1.2% and most people pay around 4%, others pay more. Totally unlike here. You would have to check my figures but that's the impression I got when I was over there. We have a weak version of it here where HSBC offer much lower rates for high income earners borrowing $500,000 or more, they don't lend to anyone else (ie, on yer bike mate, we don't want your types here).

According to David Chaston, NZ sources only 16% of its mortgage funding from offshore, so I can't see rising rates overseas having a major effect on NZ interest rates

You don't think the rising cost of living in Auckland (the wealthiest and most populous major centre) is going to decrease the locally available funds?

On the other hand, a lot of our banks are owned by Australian parent banks and are a nice wee source of revenue for them. What are the chances the parents don't seek to squeeze the NZ banks for a bit more to shore things up?

Aren't rates set by the cost of the banks' most expensive source of funding? So if the cost of that final % of funding does indeed increase then rates will have to go up. Unless a cheaper alternative source of funds is available.

Well the governor said they would be readily available. I guess it's either cheaper currency or cheaper houses. The governor seems to strongly favour the former. I wonder, will markets test his resolve?

Turkish lira. Early opening above 7 against USD.This morning will see continued flight to JPY

{kind=link}

Unbelievable what successive governments the world over have ignored in terms of multinationals and tax.

One from www.economist.com/graphic-detail/2018/02/09/the-economist-house-price-i… the Economist

That is scary, HK is about the only place where house prices are dafter than here. It's as if it's been a competition to see who can get deepest in debt.

Thanks for the great charts, Cowpat

Great piece of analysis. Thanks for sharing!

I wonder if all the economic activity driven by speculative house flipping and the activity from involvement of associated industries such as construction, mortgage lending, professional services etc. were to be ignored, how much the economies of NZ, Canada and Australia would have grown from real value addition to the world and its people in the past decade or so.

You'll never know but it's irrelevant anyway

Time to wake TM2 from his slumber... taking bets on on how soon he works himself up to an aneurysm?

And there will be plenty of time to put together your application, view the available KiwiBuild homes and make an informed decision about becoming a homeowner. The ballot for the first limited release of homes in Papakura will open in September.

Remember, this is the first ballot and KiwiBuild is a 10-year programme. More ballots will be announced as the programme scales up, and we'll give you enough time to organise your documentation.

Extremely sad state of affairs in our public services as successive governments fail to reduce immigration numbers to a level where our welfare infrastructure growth can catch up.

Two articles on the sorry state of public affairs in NZ just this morning caught my attention:

Schools in Auckland quickly approach peak capacity - https://www.radionz.co.nz/news/national/363420/auckland-schools-struggl…

New Zealanders dialysis patients at-risk of improper attention as ineligible immigrants are being serviced at public hospitals - https://www.radionz.co.nz/news/national/363933/dialysis-for-nz-patients…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.