The Tax Working Group (TWG) recommends the Government extends the taxation of capital gains and reduces income tax.

The 11-member group, chaired by former Labour Finance Minister Michael Cullen, has delivered its final report detailing a suite of ways the Government could do this.

As a starting point, the TWG suggests gains and losses from all types of land and improvements, shares, intangible property and business assets be taxed.

It recommends the “family home” and personal use assets like cars, boats and other household durables be excluded.

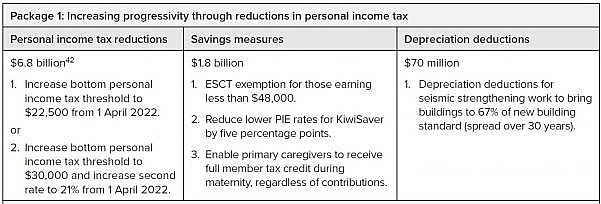

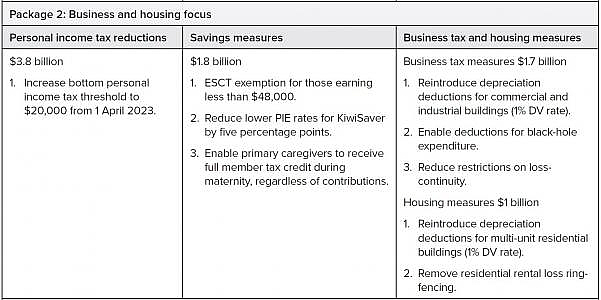

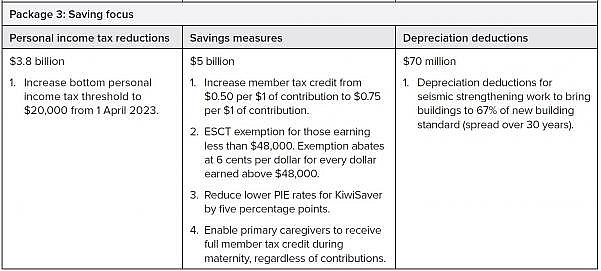

Recognising that broadly taxing more income from capital gains would raise about $8.3 billion of tax revenue over five years, it has put four packages on the table suggesting ways to offset this. These packages (detailed below) are broadly revenue-neutral and include income tax cuts but focus on different themes.

Coming back to the extension of capital gains taxation, these are the characteristics the TWG suggests this has:

- Taxing gains and losses after a set implementation date or ‘Valuation Day’, so gains will only be considered from the time a law change comes in.

- Imposing the tax on a realisation basis in most cases. IE imposing the tax when an asset is sold.

- Having a rollover treatment for certain life events (IE death and relationship separations), business reorganisations and small business reinvestment.

- Taxing gains within the current income tax system at a person’s marginal rate.

- Having no adjustments for inflation.

- Ringfencing capital losses for portfolio investments in listed shares (other than when they are trading stock), associated party transitions and losses from Valuation Day assets.

- Giving taxpayers five years from Valuation Day to value their assets.

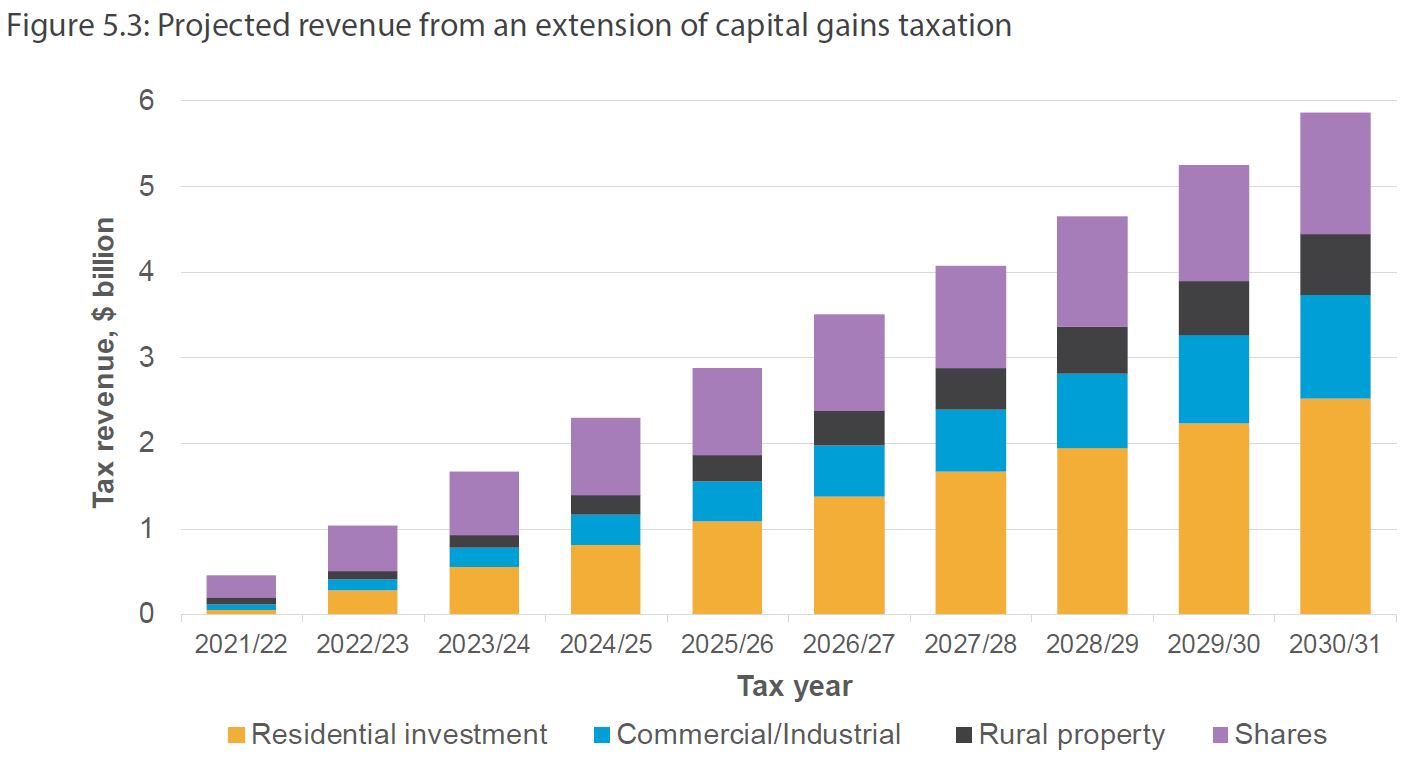

Extending capital gains taxation is projected to generate between 1% and 4% of total yearly tax revenue in the first 10 years.

It is expected to hit residential property investors the hardest, followed by those invested in shares.

The TWG doesn't believe the extension of capital gains taxation would have a huge effect on housing affordability.

It believes it would lead to some "small upward pressure on rents and downward pressure on house prices". See this story for more on this.

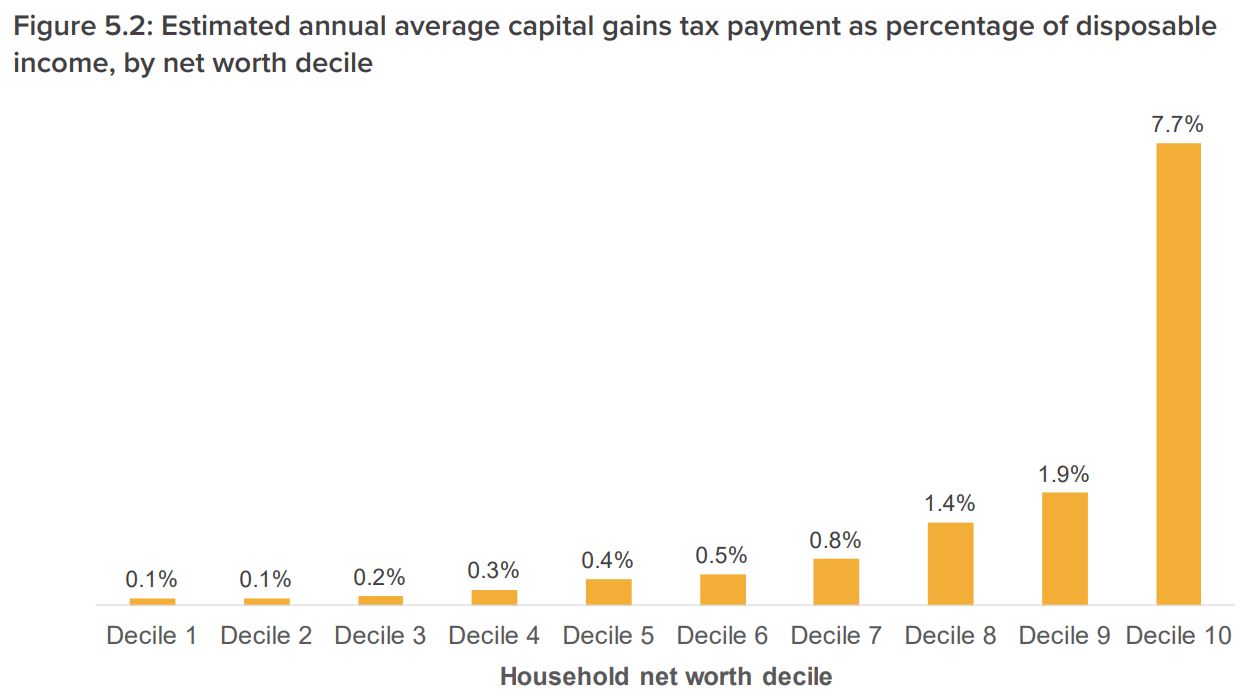

It's likely an extension of capital gains taxation would however be "highly progressive". The TWG expects that on average, households with higher net worth would pay a higher amount in tax as a percentage of disposable income than lower net-worth households.

Cullen says: “There’s a fear [extending the taxation of capital] may discourage investment, but if you look offshore at countries with capital gains taxes – for example Denmark with a rate of 42%, UK, US, Australia – in fact almost every developed economy, there is no relationship between capital gains taxation and their levels of investment and their levels of productivity. Indeed there is a relationship between their overall levels of taxation and their levels of productivity and incomes."

Cullen does however recognise it could be problematic in encouraging people not to sell their assets when they should, which would affect economic efficiency.

Importantly, the TWG says the Government could choose to extend the taxation of capital gains to some asset classes only.

“The Government also has options about how to stage the timing of introduction, whether to phase in asset classes, whether to grandparent some or all asset classes and whether to apply the deemed return method,” the TWG says.

Here are some examples the TWG has provided of how it could work:

Property

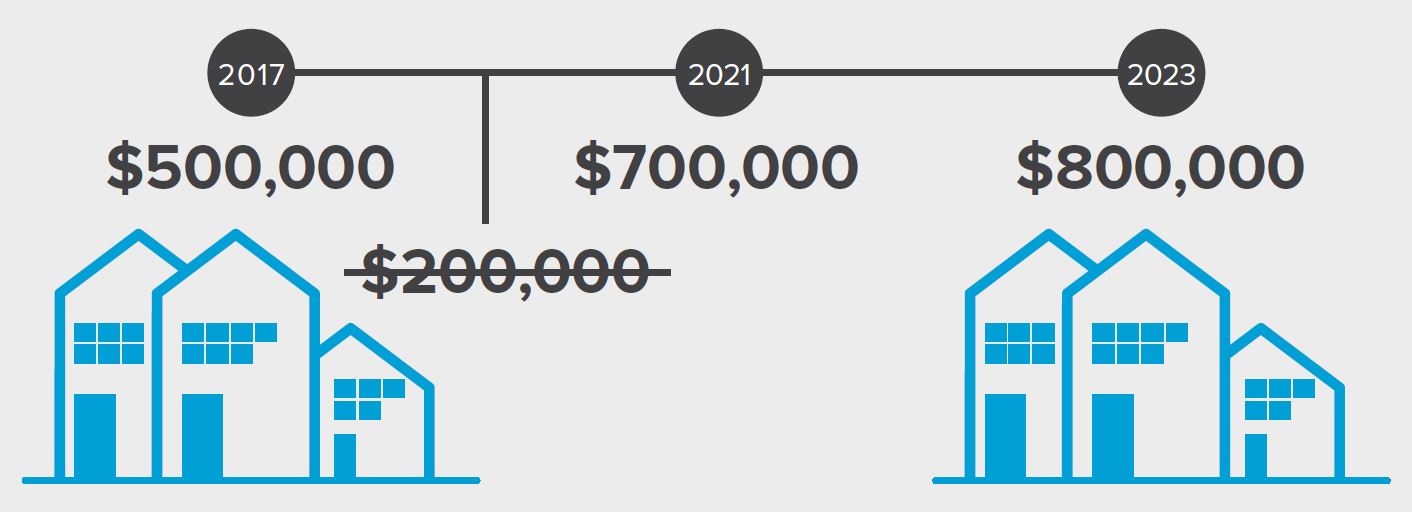

Mary owns a few rental properties. She bought one for $500,000 in 2017 and sells it for $800,000 in 2023.

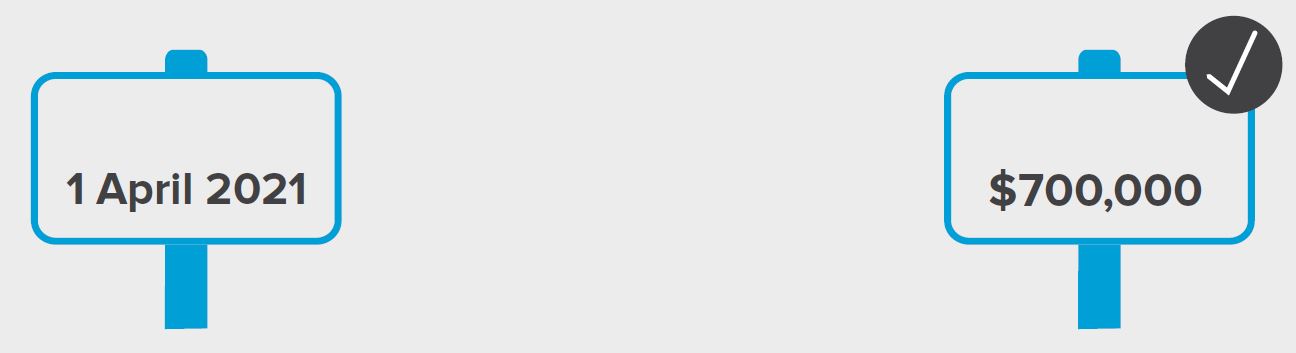

Let’s say new tax rules come into force on 1 April 2021 and Mary decides to accept the next Council Valuation of $700,000 as the value of her house.

Mary won’t be taxed on $200,000 gain that occurred before 2021. It’s only the $100,000 gain after 1 April 2021 that matters.

Mary spent $70,000 on renovations after the date of the council valuation, but ahead of the sale so her net gain is $30,000. Mary doesn’t earn any wages, but she receives $60,000 each year from her rental income.

So how much tax does Mary need to pay in 2023 when she sells the property?

Under the current rules, Mary is only taxed on her $60,000 of rental income and not the $30,000 she earns from selling the property, meaning she pays $11,020 in tax.

Under the new proposal, Mary would be taxed on $90,000 of income, because her net gain from selling her property is included. This means she pays $20,620 in tax – exactly the same as the amount of tax paid by someone who earns $90,000 in wages.

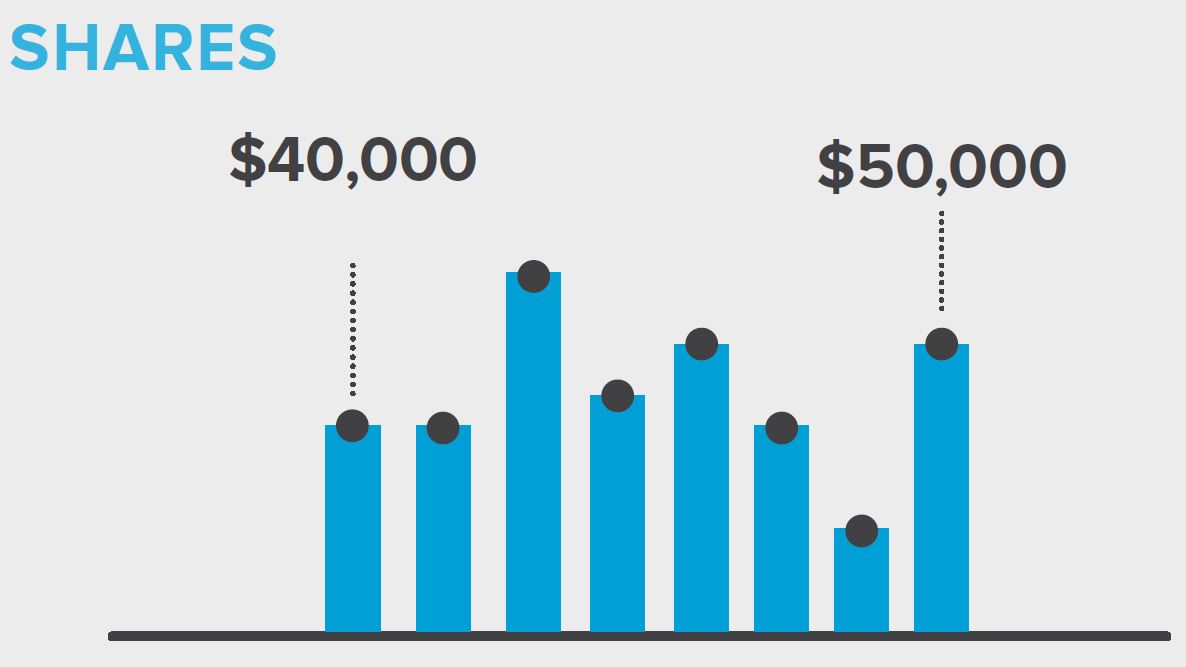

Shares

Wiremu bought some shares for $40,000 after the new rules had been introduced. A few years later, he sold them for $50,000. That’s a capital gain of $10,000. Wiremu also earns $48,000 in wages, so his total income in the year he sold the shares is $58,000. Wiremu’s employer would have already sorted the tax on his wages, paying $7,420 to Inland Revenue.

At today’s rates, his extra $10,000 would be taxed at 30%. Wiremu will have $3,000 more tax to pay, because of the gain from the shares, for a total tax bill of $10,420.

That’s exactly the same as someone who earned $58,000 just in wages.

Managed funds

Alex‘s KiwiSaver account increased by $5,000 during the year to $105,000. Her scheme provider took care of the tax she owed, according to the PIR tax rate she selected earlier.

Her tax depends on the kind of assets her fund is invested in.

Let’s say the value of the parcel of Australian and New Zealand shares in her KiwiSaver increased by $1,000 over the year and her tax rate for KiwiSaver was 28%. Her scheme provider would pay $280 from her account to Inland Revenue. If those shares had a bad year and dropped in value by $1,000, then Alex would get $280 back from Inland Revenue.

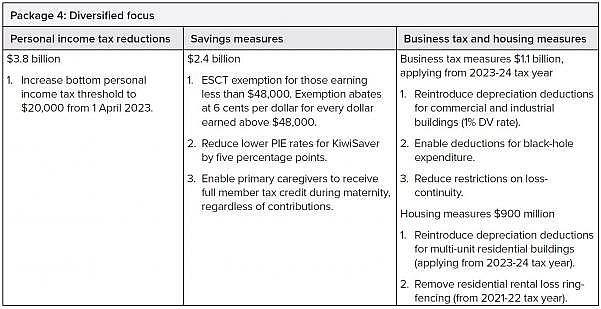

Looking at the bigger picture, here is a summary of the four packages the TWG suggests complement the extension of a tax on capital:

The Government, which has had the report for a few weeks, will release its full response in April.

The hurdle it's expected to face is getting NZ First to support a capital gains tax, as it has previously spoken out against it.

The Government had committed to passing legislation to implement policy changes arising from the report before the end of the Parliamentary term. However no policy measures will come into force until April 1 2021, meaning people will be able to vote on any decisions the Government makes on tax.

See the full media statement from the TWG here, and the Government's response here.

227 Comments

No surprises really, but I am relieved they didn’t go with the wealth tax style lunacy that their interim report suggested they were considering.

All comes down to Winston now. If he backs this, he’ll be completely stuffing his party’s prospects of getting over 5% at the next election. Not only would he be backtracking on his previous opposition to CGT, but he would be unambiguously shafting his base. That said, his base is probably accustomed to it by now. And he lost his Northland electorate seat at the last election, so they would probably be out of parliament.

Huge disincentive to sell rental property under this regime.

Winston will do the dance of 100 faces and no-one will quite be sure what he stands for until the next election campaign.

Does someone know, are commercial properties subject to cgt? I guess so but commercial property is not under the brightline regime. And what happens to the brightline regime, does it stay even when there is a CGT?

If the family home is exempt is it possible to avoid cgt by moving in to the rental and making it your home. I probably wouldn't do that I am just asking a question.

There is a change of use recorded and any gain while the house was renter is taxable on sale. This example is from the report (volume 2 page 38):

Example 50: Rental to residential Wang Fang purchases a property in 2030 for $400,000. She uses the property as a residential rental property. In 2034, Wang Fang decides to move into the property and uses it as her main residence. At the time of the change of use, the property is valued at $550,000. In 2037, Wang

Fang sells the property for $675,000. When Wang Fang sells the property, she has a net gain of $275,000.

Wang Fang can choose to pay tax on 4/7 of the net gain ($157,143), because she used the property as a rental property for four of the seven years she owned it.

Alternatively, Wang Fang can pay tax on the actual gain relating to the time the property was used as a rental property, being $150,000 (i.e. $550,000 – $400,000).

The remaining net gain will not be taxable because it relates to the period when Wang Fang used the property as her excluded home.

Errr, how about the rental property worth $600,000 in 2023.

Will IRD pay back the tax on capital losses?

Capital Gains Tax, the keyword here is "Gains"

And if the market turns, and no one makes any gains, how much revenue does a Capital Gain Tax make?

And if the economy tanks, and people get made redundant, how much do income tax /company tax bring in? Oh, it varies.

The government would reduce income taxes to ensure that the CGT is revenue neutral. Incomes reduce during a recession, but capital gains disappear. The revenue hit with CGT would very likely be more than the reduction in income tax revenue that one would otherwise expect during a slowdown.

In the short run, perhaps.

If you prescribe to the notion that economic growth has a drift component (i.e. it goes up over time), this is inconsequential.

If you prescribe to the notion that economic growth has a drift component (i.e. it goes up over time), this is inconsequential.

The old everything must go up...

Can you point to a time that it hasn't over the long term?

Plus if you prescribe to that Keynesian notion, a tax cut today is a tax increase tomorrow, again, it doesn't matter in the long run.

Depends on definition of long term. But yes I agree.

The post was more a dig at all those that bemoan housing/share/insert asset here is a crock because they can't always go up.

Haha. Yea. I figured.

Noncents,

Apologies for being pedantic,but the word is ascribe,not prescribe.

Yep but if you recall the Lange/Douglas introduced and increased GST with fair compensation to income tax payers. But the Clark/Cullen government (hiding behind Anderton) simply banged income tax up again next time round. Who is to say history will not repeat. Income tax is just such an easy target. Bit like Californian electricity prices.

Given that income taxes would've been reduced proportionally, the government would presumably take a significant revenue hit.

At the moment IRD probably makes zilt in CGT so can't be worst than current situation!

Yes, but the government would reduce the income tax rate so that the CGT is revenue neutral. I'm basically saying that during a recession they would be taking in less income tax due to the lower tax rate and lower level of income being taxed due to the downturn. My intuition is that capital gains dry up almost entirely during a recession, whereas incomes just reduce, so the loss in tax revenue would likely be more than one would expect from just a reduction the level of income being taxed during a recession.

That said, I don't have any fundamental objection to a CGT as proposed here.

In some years its going to be much more than the average and others it will be much lower, not zero though, as over time the gains will be from decades and at that point sales will still have gains even in down markets. Never the less you borrow in the lean years and pay down debt in the plump years and it all comes out in the wash.

"gains will be from decades and at that point sales will still have gains" - yes, this is a good point, should even things out. In the last recession property sales volumes dropped by 70% though, so I still think that the lean times are likely to be leaner.

it's a good argument for a wealth/land tax over CGT

Yes, in the same way that expediency is a good argument for jumping out of a tenth story window over taking the stairs. You'd have to ignore so many major issues with a wealth tax to say that it is preferable to CGT.

You should

...You mean like they do in any recession?

It's about the long run. No the short run.

In the long run, there is no alternative to permanent recession.

I think history has categorically proven you wrong on that one.

I am very pleased that you finally prescribe to asymptotic growth paths, though!

So that's a win!

Your comment can only make sense in the case that zero limit is never reached - by the same token, the maximum limit can never be reached! So, growth can, in theory be negative or positive for any period approaching infinity!

Well done, PDK! I'm impressed at your new found understanding!

Nit one growh-aspiring empire has continued to grow - all have collapsed.

This time - the first and only possible - we're running the experiment at global level.

An beyond peak, there is only recession, for something based on extraction from a finite reserve.

Don't mistake oscillations for ups and downs from here on in - it's just the dying spasms. They'll tail off.

"Nit one growh-aspiring empire has continued to grow - all have collapsed."

That doesn't imply permanent recession. I think we are probably a bit more wealthy that those cave dwellers 100k years ago.

Then you're accounting incorrectly.

They had all the fossil energy untapped. They had no exhaust/pollutive issues. They had every resource opportunity ahead of them

And their per-head possibilities were near-unlimited.

But they did tend to discount the future - just as we are doing. The difference is, they had one.

What tosh! Cave dwellers lived to 35 if they were lucky. We are better off now than at any time in history, and live longer, too. But there's little doubt that something like an asteroid strike or pandemic will spoil that, as it has in the past. And as to accounting, what about the untapped wealth of the sun, the stars, space and other planets?

Yes, humans are living longer, but with our modern crap diets it has been suggested that we looking at the real possibility of that going into reverse. And while the human race might have done ok out of it all for now, the same cannot be said for other species we share the planet with. #itsnotallaboutus

Hi GV

My understanding is that is one makes a capital loss; then that loss will be likely ring fenced, can not be applied against other income but can be applied against any future capital gain.

As for capital gains on investment properties, I recall John Key once saying that the time to introduce a capital gains tax is prior to a boom in the market and not after and hence his reluctance to introduce a capital gains tax on property in his later term in government. I agree with you; the 2021 timing will be after the property investment capital gains have long past when the horse bolted at least for this round of the property cycle.

But of course - "capital gains are no different from other income " is the catch cry of the left - but they are not like other income in cases where it would lead to less tax on you.

The timing is a bit more diffuse... one could do your property evaluation in 2026 as you have up to five years to get a property evaluation. In essence, there is likely to be nearly zero property gains tax collected until after this date. Well, other than the current CGT under the existing bright-line rules.

Wrong. Did you even read the article? Capital losses result in a tax refund. The report even provides an example of your KiwiSaver share portfolio losing value one year, resulting in a tax refund.

GK, starting a post with "wrong" doesn't earn you any friends.

I have read the article and yes Kiwisaver capital losses will results in refunds but losses from property or shares will not, these losses will be ring-fenced and will only be allowed to be offset against future gains

Deductible against other income is the recommendation.

Where did you see that ZP?

On Stuff or NZ Herald, perhaps I misread.

Seems crazy that property losses would be deductible but share losses ring-fenced. I hope we're not going to end up with a situation which further discouraged productive investment and promotes property.

No deduction for capital losses on privately used land (recommendation 2L)

What if you have no other income to deduct it from???

No superannuation, no benefit, no share dividend income, no job? Well, you're a bit of a wally then aren't ya. All your eggs in one basket..

?

That loss will be ring fenced and only be able to be used against other capital gains in the future. The article states:

"- Ringfencing capital losses for portfolio investments in listed shares (other than when they are trading stock), associated party transitions and losses from Valuation Day assets."

The rental will be a "Valuation Day" asset.

Wow, just dragging up the bottom bracket, no higher level changes and presumably no indexing or adjustment of the top current bracket. In short, net tax consumers pay less, net taxpayers pay more? It could only be Cullen.

Only an incredibly stupid person would propose a CGT that is more punitive than Australia's. No discount for inflation? No tax free threshold for low income earners? No negative gearing? Why would anyone with significant assets even bother staying in the country when they can pack up and move to Australia, and make more money and take advantage of tax breaks like CGT discounts, and superannuation exemptions? Plus there should be some nice discounted properties in Sydney and Melbourne in a few years for the real estate investors.

Or Singapore for the really filthy rich. Even the US taxes CGT at half the normal tax rate. So plenty of options for rich people to take their money and go live elsewhere.

Australia does have a zero tax for the first 10,000 or so, but they pay much higher tax rates above a certain level than we do. Australia is looking to remove negative gearing if Labour get in next election. There is already big discounts on property in Sydney, some suburbs that were selling at 1.5 million one year ago, are now listed and trying to sell at $895,000. That is a massive price reduction. All the while, vendors who have purchased off the plan, can no longer settle, as their banks are re-assessing the values at much lower prices. Australians are in a world of pain right now. As far as super annuation discounts, I am pretty sure that only applies to Australian born citizens. You will need to check this though.

What is to stop lank bankers plonking little "family home" tin cottages on their holdings? The land bankers' teenage children will have their own "family home" as well I suppose.

It also encourages the property flippers to flip every year so they can fit more taxable gains into the lower income brackets... or wait until National get in and remove the CGT.

It would be a good thing to encourage more productive use of empty land. Building houses for family members also reduces demand in other area's such as rental properties. The more people that are housed the more productive they are and the more tax they pay.

How is it equitable to include only capital items that generally appreciate in this new tax? If houses are included why not cars, boats, computers, televisions, cell phones, cameras, etc ( which will generally contribute capital losses ) ?

"It recommends the “family home” and personal use assets like cars, boats and other household durables be excluded."

You already pay tax on personal items at the point of sale. These items depreciate anyway and therefore CGT is pointless.

'average hard-working Kiwi', hmm...

Wishful thinking on the property appreciation in the example!! :)

So losses on Kiwisaver can be deducted from income, is that also the case for shares and property (and businesses) ? I imagine it will be since Kiwisaver invests in property and shares, otherwise it's blatantly unfair

"As a starting point, it suggests gains and losses from all types of land and improvements, shares, intangible property and business assets be taxed"

Does that mean that if you sell an investment house, or shares or business you will get a tax refund?

Intangible assets sounds intriguing. My reputation and goodwill are worth 100,000,000 loosing 500,000 per annum...

Ring fenced to be used against future capital gain income i.e. no refunds.

Also, given this now excludes cars, boats, and fine art, why don't we just go the direct surgical strike and implement a stamp duty, which has all of the property-targeting upsides and none of the negatives that impact on Kiwisaver or business sales?

Then again, that would be actually solving the problem, not making a political point.

Stamp duties hand a massive financial advantage to the rentier classes of super-rich family trusts and businesses and corporates that can hold onto assets for generations - if you never have to sell you never get hit by it.

I'm not seeing the difference between a Capital Gains Tax on realisation and what you're suggesting here.

Same with CGT, (if you never sell you never have to pay)

Very true. If you can hold onto your assets and have no need to sell, that would be a good decision.

mmm, wont they enjoy the exact same advantage under the proposed realisation basis CGT?

Stamp duty is a terrible idea - adding a cost to any move discourages people from moving for opportunities.

What do you think is going to happen to house prices when boomers who are cashing out can sell in a market with low interest rates and chronic supply issues? Who do you think is going to cover the cost of the capital gains tax? I'll give you a hint: it won't be the vendor.

If they all cash out at the same time Gains won't be the issue.

I'll ignore your hint - it will be the vendor. It will only apply to investment properties, which is the minority of sales. Do you seriously think that those unfortunate enough to be paying this tax will be able to price their properties ~10-20% higher than the market to compensate themselves for their CGT?

Funniest thing I have read for a long time .

U have 5 years to get your property valued!

U would get it valued when just before dale confirmation therefore u would be paying no CGT.

CGT is dead in the water

People are going to luv paying tax on their shares as well I know what I would rather have between property and shares, and it isn’t shares.

It will make more people want property lol

Valuation day would be 1 April 2021. It wouldn't matter when you got your valuation done e.g. 1 day before or 5 years after, the valuation would be a estimate of the 1 April 2021 value.

Volume 2 of the report states:

"3. The rules for Valuation Day should provide taxpayers a choice between simplicity and accuracy and provide different options for different types of assets. The Group is not proposing that all assets need to be valued by valuers on Valuation Day, as this would impose an unmanageable burden on valuers and unreasonable compliance costs on taxpayers. Instead, taxpayers should have five years from Valuation Day (or to the time of sale if that is earlier) to determine a value for their included assets as at Valuation Day. If no valuation is determined, then a default rule should apply. "

I'm sure that there will be "valuers" who will put an extra $200k on the valuation if you send a lot of business their way. They will just have to make sure they have a good disclaimer e.g. "Not suitable for bank lending purposes, or anything else really except CGT".

I agree

This package makes me tend to consider property investment. This goes against every principle that I have previously held as I believe that the occupier is the best owner of a property. I would have thought it wiser to tilt the playing field in favour or equity investments which after all create employment and real income for the country, IE it has a real social benefit. Property investment is quite the opposite and impoverishes a wide section of society. So I am asking myself why take all the risks associated with share investment when the government will treat me no worse with lower risk property investments held over a very long period.

On the basis of this Labour will loose our vote

Under the new proposal, Mary would be taxed on $90,000 of income, because her net gain from selling her property is included. This means she pays $20,620 in tax – exactly the same as the amount of tax paid by someone who earns $90,000 in wages.

How could anyone argue that this would be unfair?

Seems like a perfectly fair approach to earned and unearned income.

How much money has Mary made after allowing for inflation over the time period, assuming she is buying and selling in the same market? Is Mary worse off in Real Terms once she pays her CGT? Is Mary better off not selling the property at all and simply deriving the income at $60K ad inifnium?

You really love the word "unearned". Even the TWG report never refers to "unearned" income. I dont know how a capital gain from selling an intangible asset or a successful company is "unearned". Income from risking your capital by investing in a business venture is "unearned". While using loaded words such as unearned (instead of call it what it is a capital gain) may emotionally charge your message (thus gaining additional support for it) it does little to improve the quality of the discussion

If you don't work with a shovel, your income is unearned ; )

In physics terms, Yvll is quite correct.:)

It's actually just an economic/accounting term:

https://www.investopedia.com/terms/u/unearnedincome.asp

https://en.wikipedia.org/wiki/Unearned_income

If you experience a negative emotional reaction to it, that's a completely different matter.

As mentioned before, you cannot call capital gains from producing items such as patent or other intellectual properties (as an example) "unearned income". You really use the word out of context and for its emotive properties. The wiki link you have included clearly demonstrate this point. You do not have to be an academic to deduce that labeling gain from discovering something new as "unearned income" is unlikely to be an accurate way of describing it.

Unearned income is income from investments and other sources which is unrelated to employment. Examples of unearned income include interest from savings accounts, bond interest, alimony, and dividends from stock. Unearned income, known as a "passive source of income," is income not acquired through work.

And

In economics 'unearned income' has different meanings and implications depending on the theoretical framework used. To classical economists, with their emphasis on dynamic competition, income not subject to competition, mainly income from land titles, are 'rents' or unearned income. According to certain conceptions of the Labor Theory of Value, it may refer to all income that is not an immediate result of labor. In a neoclassical frame, it may mean income not attributed to the normal or expected returns to a factor of production. Generally it may be used to refer to windfall profits, such as when population growth increases the value of a plot of land.

It's pretty clear how it is used, and in the NZ context where most discussion is of income of windfall gains from property is clearly a suitable term.

The problem here is not the term's accuracy but more seems to be people's happiness or unhappiness with it.

Ask ACC about assessable income and what income is charged the levy. Passive, unearned income from rents is exempt because it does not depend on the landlord and it just happens.

Say inflation increases at 2% a year. After 10 years your asset is worth 20% more (ignore compounding for sake of argument). How is this money you have "earned" when its simply the price of an item increasing to reflect the cost of living increase? In terms of relative buying power, your asset is worth exactly the same as it is today.

Unless your asset price falls and in this case there would be no CGT applied.

It's what I expected, though I thought they'd suggest inflation adjusted tax brackets.

Might look into a Ferrari or art collection of there is going to be a loophole.

Agreed CGT should be inflation adjusted

The loophole is moving to Australia. Or Singapore.

Cullen is a crafty bugger, not as crafty as Ulyanov himself, but addicted to the same intellectual kool-aid.. Most of the supposed "gains" are really just inflation due to a buggered monetary system that pumps up asset prices by devalueing the currency over time. There be monsters.

Keynes put it better than I could:

Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security but [also] at confidence in the equity of the existing distribution of wealth.

Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become "profiteers," who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

https://www.pbs.org/wgbh/commandingheights/shared/minitext/ess_inflatio…

This is the only economics lesson you ever need. Read it over and over and over until you understand what it's telling you.

I seriously doubt that introduction of CGT will be accompanied by any real drop in income taxes or GST. The reason is unlike the latter, CGT is both unreliable and unpredictable exposing government revenue to a serious level of risk.

Overall, other than disallowing adjustment for inflation, and the unprecedented rate for taxing capital gains (at personal margin rates) the recommendations for CGT are reasonable provided that they also allow all relevant expenditure to be fully deductible from the gain (e.g. for a property allow maintenance, interest, rates, insurance, etc to be deducted).

The high rate for taxing capital gains will have a significant impact over capital formation. I see that they have provisions for reinvestment for SMEs but I wonder if enough. In principle, and notwithstanding all the implementation complications, as long as the gain is reinvested in productive activities, and not consumed, it should be exempt from taxation. That is why taxing savings (e.g. Kiwisaver) is simply wrong and a very bad idea. Tax it when they are distributed for consumption, not when they continue to be reinvested.

This is a big disincentive to workers with Kiwisaver. The tax being paid each year will have a massive compounding loss over a lifetime of savings. Optimal retirement savings are external to Kiwisaver as the CGT only gets paid when a gain is realised. Kiwisaver is still worth it for the minimum contribution of $87 per month to obtain the Member Tax Credit, despite the annual CGT.

The amount the Government is taxing from Kiwisaver is greedier than some of the Wall Street hedge funds. Some of the better performing hedge funds only charge 20% on the gains.

e: In the long run Kiwisaver accounts will perform worse and the Government will collect less tax in the long term as a result.

Yea. 'F' Kiwisaver when there is a family home exemption.

Draw everything out for your first property, ditch KS and reinvest everything in that home for the next 40 years.

Agglomerate contiguous titles, McMansion the hell out of that property and lobby the council for favorable zoning laws, amongst other things.

Agreed nymad.

We tend to have a mentality of minimising our tax liability.

For this reason, rightly or wrongly, many will be influence into putting more into their home for a tax free capital gain rather than in an investment property.

This is especially so when the yield on rental properties is only around 4% (interest.co) less expenses.

One of the critical things I would have liked to have seen discouraged is people using retirement savings to buy a house. Now the CGT on Kiwisaver is going to encourage it. You will pay less tax by buying a house and zeroing your Kiwisaver account. Then only put the $87/month into Kiwisaver while holding all retirement savings outside of the scheme.

Michael Cullen's dream taxation scheme of Kiwisaver won't be the ATM the Government is hoping for.

It isn't a gain if you don't intend to sell. Some people improve their properties to improve their own living standards and enjoyment of life and have no intention to sell. A house isn't an investment if you are living in it, it is merely a consumption item and a roof over your head that provides security against ever increasing rents. Not much more than that really. In fact, it is a liability, as you still need to paint it every few years, replace the roof etc....

Yes, Kiwisaver should be exempt from this if they want people to save for their own retirement.

Not that anyone cares, but a way to generate property based inflation, is to depreciate the NZD, now they can freely engage in FX depreciation to generate taxable inflation. I don't think they've thought of that yet, but that's where this is heading. The path of most effect least resistance, is to engage in currency depreciation.

It's not about taxing capital gains, its about taxing inflation at the average joe's expense.

Not sure I fully understand you, do you mean because the CGT is not adjusted for inflation (which I think is very wrong)

Yes exactly. And due to the nominal gains being high, but real gains being low. Inflation in NZ is actually very high, but you only see it in downturns.

The correlation between the property cycle and the NZD is around 90%, you can depreciate the currency to push up nominal prices of property (the real gains are a different story)

Across the board, all taxes are now not subject to inflation, there is a reason for this, the Government knows its a great way to be able to depreciate the currency to generate tax revenue.

It is now in the Governments best interest to generate large amounts of inflation

Ok, and how do you think the government will "generate large amounts of inflation"?

Two words.

Fannie and Freddie

All currencies are being devalued and have been since QE started after the GFC. Have you ever wondered why you now need up to 8 times double income earning household to purchase a house these days? You need that much more, because fiat currencies are being de-valued when money is created to keep the global economy ticking over. Our super-annuation savings won't buy much when we cash in our savings for the same reason, unless they stop printing money and start increasing interest rates. Low interest rates over the long term is actually a function of low growth and an economy on life support, not the other way around.

From a property investment perspective.

Rental property investment has just become a hell of a lot less attractive for landlords and and the anti-landlord renters will be celebrating doing a dance of unbridled glee.

For rental properties to be viable for private investors, rents will need to increase considerably and renters will then be moaning and doing dances of unbridled anger.

I think the government will be forced to become a landlord on a large scale in a few year's time, as there just won't be enough rental houses

They've already been forced to take up that mantle more because of soaring housing costs and abandonment of earlier policies that helped make home ownership accessible to the previous generations. See the declining home ownership rate in NZ.

Once the self licking icecream cone generation are dribbling into their pajamas at the Summerset retirement village, I think only then can sustainable and wise policy be implemented. In the interim, its a race to the bottom to see who can generate maximum paperwealth with disregard to future generations.

Your posts are becoming more and more negative and envious. Raise a drink and cheer up

Your posts are becoming more and more negative and envious. Raise a drink and cheer up

Raising a drink at present regarding CGT and the future of another term of the coalition of liberty (CoL). Cheers!

Totally agree Yvil, but unfortunately our current socialist government cant see or comprehend this through their red tinted spectacles.

We are in for interesting times as any CGT on investment properties - along with the numerous other recent changes affecting the viability of investment properties - plays out.

so property prices will drop and the number of owner occupiers increase? Good outcome in my books.

Socialists...aren't you on the pension?

Oh my god, will a cgt lead to disappearing houses ? Is this an unintended outcome ? Burn the witches !!

I don't see why, a capital gain on property is never a guarantee so I don't see why it would affect the rent. Property investors should be looking towards an income from rent (investment) rather than a capital gain (speculation). When there is a capital gain, it should be a bonus and losing some to tax is a cost of being in business..

Hi Anacoda: If you can't see why, talk to some long term landlords .

"For rental properties to be viable for private investors, rents will need to increase considerably" - or rental properties will need to become considerably cheaper...

The TWG says: "If those shares (in Kiwisaver) had a bad year and dropped in value by $1,000, then Alex would get $280 back from Inland Revenue"

Why can Alex get a refund if his Kiwisaver, which invests in property and shares, goes down, yet if you own property or shares directly, and they go down in value, you cannot get a refund?

The Government is planning on using Kiwisaver as an ATM so the tax refund is just to encourage people to stick with the scheme in bad years, and the Government knows it can draw the money back out later when times are good.

Those in Kiwisaver are locked in until retirement age.

Err, the govt doesn't hold the kiwisaver funds.. So how exactly are they going to do that?

See my comment above about CGT application to Kiwisaver.

All those "kiwi" savers just got shafted....... i mean plucked......

so what about gold and bitcoin?

Those are personal possessions.

Who has two thumbs and will look into moving his investments off-shore? This guy.

Don't worry though tax spruikers, I'm sure the government will track me down. Right after they make sure all those immigrant bakery workers are being paid minimum wage and paying income tax. Maybe around the time they build all those affordable houses.

So... has the working group said anything about the impact on FIF? With a GCT, there should no longer be any rationale to tax the paper profits of overseas investments, right?

11. The FDR method should be retained as the main method for taxing income from FIF interests of less than 10%.

12. Under an extension of the taxation of capital gains, there are three options for taxing interests of less than 10% in foreign companies that are currently excluded from the FIF regime, i.e. interests in Australian resident listed companies and for portfolios costing less than $50,000:[16]

•they could be taxed on a realisation basis, in the same way as other New Zealand assets

•they could be taxed under the FIF rules like other foreign shares (with the main method of taxation being the FDR method)

•taxpayers could make one-off elections to tax these interests either on a realisation basis or under the FIF rules, i.e. the FDR method.

'Family home run business' looks to get a boost with all this: as long as one has quiet work habits and high fences and paid-off neighbours.....

KiwiSaver is the fly in the ointment here. So most will get a few hundred extra a year, but most are in KS and will pay 28-33% on their gains. On $100,000 invested, returning an average 5%, that is $1400 to $1700 extra tax a year. On $50,000, $700 to $850. That more than wipes out tax cut. Or am I missing something? A lot of Labour voters will be disadvantaged, I think.

Correct, now compound the lower gain over 20-30 years… a monumental reduction in final KS payout

No you're bang on. In the highest tax bracket the reduction in income tax is around $595. So at 5% return on capital gains you would end up better off if your Kiwisaver balance is below $36,000. Until the balance eventually rises until you pay more tax.

Art, boats, cars, bikes, jewellery, personal household items and the family home to be exempt.

So instead of houses, best bet is few bars of gold. Melt them down to a big fat heavy ugly ring and pay no CGT on that!

it is strange that ART and gold/Sliver are not included

Included assets

1. The taxation of capital gains should be extended to a list of ‘included assets', being:

•land, including improvements to land (other than the excluded home)

•shares

•intangible property, and

•business assets.

2. Those assets, as well as the assets that should be excluded from an extension of the taxation of capital gains, are discussed in this chapter.

10 years too late. CGT and foreign buyers ban should have been implemented 10 years ago.

NZ would be much 'norma', affordable. Banks would not make their billions though....

This is worth repeating from Printer8 above ......" I recall John Key once saying that the time to introduce a capital gains tax is prior to a boom in the market and not after and hence his reluctance to introduce a capital gains tax on property in his later term in government....."

And it seems to me the boom is past and we are on the slide down eg. capital loss.

If prices are about to stagnate at the end of this business cycle/credit expasion phase - why the long faces about a capital gains tax?

.- because it is a nightmare to administer and comply with , benefiting tax accountants mostly ( Terry Boucher, take a bow ..)

- because it is a thin edge of the wedge - as soon as the revenue from CGT proves negligible it will be used as justification to extend it to the family home or a wealth tax ( which I think is exactly what you would like to see - do correct me if I am wrong )

Capital gains tax will cause the value of your family home ot fall so please don't worry about that....

nonsense again - even if property prices are affected negatively by CGT in real terms they will certainly not go down in nominal terms in the longer run

It depends entirely at what price point and part of the cycle that one entered into the market.

What is long run for you?

The Kiwisaver idea's are just weird. If you are looking for the dumb nitpicking from the Cullen group. Here it is. Like a different graduated tax for Kiwisaver. Continuing government contributions for non contributors on maternity.

Long story short. Kiwisaver should not be taxed at all. Government should not be making any contributions.

CGT tax will apply to any property above 4500m² - so screw the rural voters and lifestyle blockers eh? Never mind that their properties are worth way less than the untaxed urban family homes or waterfront apartments in Wellington and Auckland.

And no inflation indexing!!! Hold your asset through a period of high inflation or a few decades with no real growth and the government gets a huge cut - leaving you far behind where you were in real terms, and rewarding bad govt economic management with more tax.

"30. The excluded home should include the land under the house and the land around the house

up to the lesser of 4,500m2 or the amount required for the reasonable occupation and

enjoyment of the house. However, this land area allowance should be monitored and reduced

if necessary."

More reason to do away with the family home exemption.

Foyle, where did you hear or read about "CGT tax will apply to any property above 4500m²"?

The documents are at https://taxworkinggroup.govt.nz/

See page 11

https://taxworkinggroup.govt.nz/sites/default/files/2019-02/twg-final-r…

wow that will capture a lot of farms, I can see our next farm shareholder meeting and the panic it will cause about selling up now before it comes BUT its only 30-33% of the GC so what is the big deal we just will make a third less. and over 20 years we will still make enough to be happy, not to count the dividends along the way.

They may lose more than a third as the CGT makes the property less desirable to buyers. Much like a discount cash flow model they'll factor capital gains tax into their own valuation.

I thought Farms were excluded as they are an integral part of this countries GDP? This needs to be checked.

Example 20: Land under an excluded

home

The Farmers own a 100-acre sheep farm.

Approximately 4,000m2

of the land comprises the

Farmers’ house and gardens.

...

The valuation

confirms that the house and gardens make up

approximately 15% of the value of the whole farm.

On that basis, only 15% of the total gain on sale

can be allocated to the excluded home.

Bureaucratic valuers cost a fortune to pull numbers out of their bum. Yet again the politicians boost the unproductive economy.

Even though the capital gain (income) was accumulated over say 10 years it's only recognised in the one tax year so the gains will almost certainly be taxed in the top bracket(s) which is totally unfair. Where as the property flipper selling every year might only pay tax on a middle bracket. Much better to just go with a flat middle bracket rate.

Make sure you separate from your partner before buying another house in a rising market, reconcile after 3 years and pay no CGT.

Also will lead to people living in unnecessarily large/valuable houses as a way of avoiding the tax. Highly inefficient use of a scarce (land) resource.

Then if you are a bloke, you could declare yourself a female, change your birth certificate accordingly, then enter female toilets and sit down with your legs spread apart and give everyone a good gawk at your tackle while you perv on all the women in there. Too easy.

Shouldn't we be celebrating the concept of falling income taxes? Or people so self absorbed with the valuation of their house that they don't care about the paid income they receive each week?

The $595 tax break per year is a lot less than the CGT that people will end up paying. Remember this is increasing the Government tax take, not decreasing it. Who is paying that tax?

Dictator - what rate of capital appreciation of assets are you assuming?

It is kind of the point - on the whole assets are owned by the wealthier in society, currently they make money from these and pay no tax increasing the gap between the haves and the have nots. This is more about an attempt to level the field by taxing all income irrespective of how you come about it. It should include the family home too.

IO, It insnaive to think we will actually get lower income taxes. By the time the CGT is in force (if at all) the government will realise they are not taking as much tax as expected and lots of it is going to administration cost, they will reduce the income tax credits.

Make no mistake, the headline that "THE TAX CHANGES WILL BE REVENUE NEUTRAL" are as true as "WE WILL BUILD 100'000 AFFORDABLE HOUSES IN 10 YEARS"

Guess they'll need to make the CGT even higher then I suppose if they need more tax income.

IO - If you seriously believe that.....well....

My take

- Akl could be in for 10 years of capital losses on property = no CGT for a long long time

- the provinces that are showing capital appreciation on housing may well be hit.

- Kiwisavers will get hammered, meaning the retirement nest egg will take a lot longer to accumulate

- farmers will get hit very hard.

- small businesses won't on-sell, but liquidate

- fundamentally middle nz will get hit the hardest

- Bridges is right, many Kiwis will move to Australia as the CGT regime there is less

so...

- pile all your wealth into the family home by selling investment properties

- get out of kiwisaver, pies, and any other funds that primarily invests in NZ or Australia, and pile into other overseas markets (FDR regime)

- transfer business assets to new vehicle prior to 2021 at inflated rate to realise capital gain.

- anything else?

Accountants, and tax advisors will cream it.

Tax returns that are currently 4 pages, will blow out to 20

kane02. Re yr comment about exiting nz equities; I agree. The risk/return calculation tilts significantly away from NZ equities if a third of the gain is expropriated by the state. The proposition that because other jurisdictions have CGT NZ equities will continue to be just as attractive if we also enact one, is nonsense. Our tiny, narrow economy presents inherently higher risk, with the tax advantage one of the few things going for it. With the total return for kiwi investors savagely cut, you'd be crazy not to take the knife to your NZX allocation.

correct.

and buy gold and art both exempt from what I have read so far on the tax working groups website

Invest in dividend generating shares. You pay tax on the income anyway, but people may want to look offshore for better returns. I'll have to reassess my holdings, perhaps save for early retirement and then leave NZ once I'm there.

How long do you need to live in your rental house before it becomes your home?

Average Joe/Josephine is just plain confused and angry as they think it is already passed into law.

Accountants and Lawyers everywhere are hopeful. If it goes ahead then everyone will need them to prepare their tax return.

Real estate agents are against it - as private sales will be the way forward. A lot easier to hide from the tax man that way.

The opportunistic are already working out the pros/cons of using Kiwisaver as a tax reduction system rather than a retirement saving scheme.

Me - Can't see it going anywhere, it is political suicide.

A flat tax with no dedutions is my cure for everyone.

Thank you.

Not a word that I can find on bracket creep, only tax brackets at the low end. The end result tis the middle being crammed into a small group. Is that appropriate?

The same middle reliant on inheritances to help manage massive mortgages on family homes and small business sales and Kiwisaver to get them through their retirement? Nah, those guys apparently have it way to easy, to hell with them!

He's got the Robin Hood bit all mixed up; he's going rob from the working poor to give to the poor who don't want to work.

No real surprises. Farming debt on property for sole purpose of tax free capital appreciation just took another blow. See whats happens next. For me its too complex. Id favor a flat % land tax like rates (higher for offshore owners) and a lowering of income tax. Simple and easy to enforce.

I guess to swap houses will become more popular then sell and buy with CGT:

If Mary owns house1 (bought for 500k) which costs 1m now and she wants to upgrade (let's say to 1.2m house2 which was bought for 600k )

then with sell/buy operation:

1)Marry pays CGT from 500k gain after selling house1 (~160k)

2)Owner of house2 pays CGT from 600k gain after selling house1 (~190k)

with swap operation

1)Marry pays nothing as CGT as she did not gain any capital

2)Owher of house2 pays Income tax from 200k (~66k) that Marry paid him on top of house1

The problem would be to find those owners happy to swap though .

Yeah CGT looks fair from the first glance , it won't allow buy the same sort of house on the same market in reality, so I would expect :

1) people won't sell houses just for simple upgrade (e.g. +100k-300k ) so the NUMBER OF LISTINGS WILL GO DOWN drastically

2)The housing prices will go DOWN because of less speculation level on the market , but still will have upward pressure generated by listing shortage (but this will hugely depend on the number of new-builds coming to the market)

You're onto something, I can build you a "Swapmyhouse" app

More fiddling while we consume our seed capital. Keynesian delusions abound. There are four functions of govt.

1.A parliament to uphold the rights of citizens. 2 An independant judiciary to uphold those rights. 3 An internal police force to enforce those rights. 4 A defence force to stop those not entitled to be in this country.

Everything else is a construct of politicians to gather votes. Democracy ends when the voters realise they can vote themselves all they want from the treasury. This latest tax is justified by the politics of envy. Tic Toc.

I quite enjoy my roads and hospitals

Spot on. “Ask not what your country can do for you” has turned into “who will offer me the most at the expense of someone else.” Time to go back to basics.

CG should not be a part of Income tax but should have flat rate of say 20% or can have short term tax of 30% if accrued by selling within 2 yeads and long term capital gain of 20% if accrued by selling after 2 years.

It should be inflation adjusted.

Capital gain should be allowed to offset with capital loss in same financial year.

If sold and bought (Reinvested) of similar amount or more should not be taxed so that investment is generated.

Small business could be exempted or charged much less - can have lower bracket.

Excusion of family home is already accepted by all and Income Tax bracket should be extended as advised in the report.

Some sort of tax is required and must to be fair to everyone and percentage of CG does not have to be high.

Labour government can pull it off by giving concession in Income Tax and relief to small business.

Don’t worry it won’t come in!

Absolute waste of time having a TWG as this lot will be out and National will repeal it anyway!

TM2. I'd like to be as confident. Remember that around 50% of NZ households pay no income tax (after transfers) so have no skin in this game. It's not only a chance to grab more of the tax paid by others but also to stick it to the rich pricks.

As soon as National is back in itvwill be repealed so there is no point!

Everyone will be worse off but then some people are just not that financially intelligent, especially the COL government.

Robertson can not even answer any question put to him and him and Twyford together are just so cute!

Brain between them ?

Just like all conservative governments over seas have repealed any capital gains taxes in place?

Just like how National didn't set any bright line test for a CGT?

Just like National repealed the "communism by stealth" increases to WFF?

Nah, I think you will be wrong.

Its a dangerous path to start down. Sure for now it doesn't include the "Family Home" that will just come with stealth further down the track. More fiddling with the tax system, accountants are going to love it, more work for them. I don't own multiple house but still cannot see the upside for me. Just more reasons not to bother owing a rental property. Those people renting are going to get shafted.

The positive news for you there Carlos67 is that if property investors all start selling up, it will add more supply available to owner occupiers and prices will fall. So this will be great because the capital value of you're house will go down and you won't have to worry about a captial gains tax either way.

Also if interest rates ever go up, house prices will fall and again you won't have ot worry about capital gains tax on your family home. So either way, its good news for you. Must be stoked?

Why do you care about Carlos67's affairs?

Why do you care that I (don't really) care about Carlos67's affairs? Um...

Gosh you're a child

Ironic that the inventor of Kiwisaver is the one who will shaft it.

The share tax will put people off it, and in to bigger family homes, offshore investment, term deposits with no or negative return, gold xc.

Hard to see that as anything but diverting money from productive investment in NZ. Such as building up a business, or even continuing one.

Why get locked into a long term deal when the Govt can change the terms and conditions: think taxes: change lump sum to annuity; raise age of eligibility???

From Kim.com!!

Get ready for the biggest asset sell off in New Zealand history. Real estate, stocks, everything will go before a new capital gains tax becomes law. If you’re planning to buy a home you’re in luck. The real estate market may drop 30% or more. The NZ stock market will crash too

If a capital gains tax is introduced, capital gains oriented property investors might start selling (remember, home ownership rate is about 65%, so non home ownership is about 35%)

1) NZ residents who are capital gains oriented property investors might start selling ...

2) Non residents who are capital gains oriented property investors might start selling ...

A capital gains tax might also result in land prices falling as land speculators sell. This could lead to lower the cost of sections and the cost of construction of houses.

If ring fencing of losses is passed, this may cause many loss making property investors to start selling (particularly those owned in tax structures which allowed losses to be deducted against personal income)

This could make houses more affordable for owner occupiers ...

How does a potential price fall impact the banks and bank depositors?

Hot investment tip.

If you can, invest in a property valuation company. They are going to be rushed off their feet 1 April 2021 with the flood of requests for valuations.

There is an upside after all. :)

Does Wiremu have a heap of kids. If he does accounting all that income in one year is going to mean a way bigger tax bill on it.

I totally want the tax system redone but can't see this being anything but a dog's breakfast.

Do I understand it correctly you pay tax on your kiwisaver every year? So that will materially reduce the amount of money in your fund over a life time, and materially reduces the effect of compounding interest.

So what would be the effective tax rate for let's say a teacher? That could be 50% or more I'm guessing.

Yes you are understanding this correctly. In one of my other comments I have pointed out that the Government is planning on taking a larger cut that a hedge fund manager each year on any capital gains in Kiwisaver.

This is primarily a tax on workers. Those that run businesses or only have investment income there is only a benefit from putting in $87 per month to obtain the tax credit. No doubt this will hit some high income households until they renegotiate any Kiwisaver benefits from their employer to salary instead.

In fact everyone should now switch to minimum contributions to Kiwisaver as they will be better off.

Indeed, I see later others had mentioned that as well. To advance the discussion, I created a quick spreadsheet: given a $400 monthly contribution, and a fund return of 7%, the difference between these two regimes is over $150,000!!!

Financial wizards: please checkout my spreadsheet, I can easily have made a mistake.

It's close enough, it assumes the full percentage return even on the recent monthly contributions. However it's sufficient for the purpose.

Think about people starting working at 20 and working to 65 or 67, etc. Over 40-50 years the loss of compounding gains will get even worse.

There is an additional problem of people leaving money in Kiwisaver. Part of retirement fund benefits are keeping the money invested for the estimated mean of 30 years of retirement. The loss on compounding gains during retirement creates a higher risk of running out of money during retirement. So what is going to happen is everyone will have to cash out on the day they hit retirement age, which will create havoc.

One comment I received is that apparently you already pay taxes on kiwisaver? Not according to the example on this page, which I used as my source of information. So if PIE is applicable, that needs to be added for a correct comparison.

Maximum PIR rate is 28%. However there are ETFs that are PIEs and you do not have to buy them through Kiwisaver. So you can compare 28% on income to 28% on income and 33% on capital gains annually.

Another part is on the last year the person could take all the money out and pay capital gains at the end of the 30-40 years. The person paying at the end (outside of kiwisaver) will pay a substantial amount of tax but will also have more in the end.

Right, so I should add a 28% taxation rate for the current situation? That compared to 33% under the proposed CGT regime? Or is 28% too much?

No the 28% is only on interest earned. Most funds will have a mix of income and capital gains.

So 28% PIR on income, and 0% on capital gains right now.

It would become 28% PIR on income and up to 33% on capital gains under the TWG.

thanks so much @dictator! But another thing I've seen is that 0% on capital gains is only for Australia/NZ shares. So if that's true, we currently have CGT on some shares isn't it? And I'm assuming most funds have overseas shares.

Most Kiwisaver investments fall under the FIF regime so a higher rate tax payer would spend 1.4% on tax every year on the value of the investment regardless of market movements.

Also, you won't realise the gains every year, only on sale. During your accumulation phase, you are predominantly buying rather than selling. Most selling occurs when drawing funds down.

A CGT would actually cost less in tax over the course of ownership - better to pay 28% tax on the final gain than 1.4% tax every year.

Side note: tax loss harvesting is also an option to reduce capital gains tax over time

Check the Kiwisaver portion of the TWG video. If it's in Kiwisaver any capital gains (unrealised or not) will pay CGT. You need to be outside of Kiwisaver for CGT to only apply when selling.

So you could end up with FIF and CGT with the proposed tax changes.

Yup, and then factor in the forgone interest and compounding income over an entire working career that you're also no longer getting. It works out to be a much higher portion of the final amount than 33% because you've lost the chance to earn compounding revenue on it.

It's theft from the pockets of workers and straight back into the non-means tested pensions of the baby boomers and totally flies in the face of the logic of a retirement savings scheme.

According to my spreadsheet, even if you only add $100 a month to your kiwisaver fund, and assuming you have this in an aggressive fund, over 30 years you end up with $105,000 less!

I think the recommendation for a broad base CGT (specially including retirement saving and businesses) is to have ground to give so the actual target (residential properties) is saved. I think that any real proposal for CGT will only focus on residential properties and that at a lower rate. But starting from where they started, everyone will simply be a lot more amenable to the idea when the time come.

So as Kiwisaver is my biggest asset, under the above scenarios Im best to now buy a house to live in using my kiwisaver?

Always thought the previous governments use of peoples own kiwisaver money to bribe them was a slick/sick move, worked so damn well.

You would have a massive tax advantage in depleting your Kiwisaver account completely. You get the benefit of any capital gain tax free instead of the Government getting the money. Usually I've been recommending that people don't ever touch Kiwisaver money until retirement so you don't lose compounding gains, but in this case it's foolish to leave any substantial sum in Kiwisaver.

Only if your Kiwisaver is invested only in non-Fif NZ and AU shares. Any global funds are already subject to the wealth tax called FIF

Also, if the CGT is successful in dropping house values, and in the process increase the rental yield, does it not mean that people with money (and expensive "family houses" to leverage with) will be better off buying rental properties as a retirement plan thus reducing market access of first home buyers (the alternative being paying taxes on their savings every year)? this way they receive a rental income, and will only need to pay tax if they ever need to sell the property (at a minimum they defer payment of this tax until much later).

End result won’t change.

Another massive waste of resources and attention redirection...

Is a thoroughbred an asset?

Only if it's Pretty. Otherwise it's dog food-in-waiting: COGS.

"The 11-member group, chaired by former Labour Finance Minister Michael Cullen".

How to force hard working New Zealander investors to vote for someone else in the next election.

How to kill off several classes of productive investments in NZ and motivate foreign investment.

In future history this will be remembered as one of the biggest and most expensive mistakes the current government creates.

Do we see large amounts of capital leaving NZ in the next few years as investors cash their chips in and divert their investment overseas ?

I see the usual suspects are tilting at windmills as usual. Awfulizing abounds - truth is the world is not going to end. I think a lot of people suffer from offended dysfunctional disorder.

Person A purchases a property for 500K and spends 100K on renovations including 15k GST (note one cannot claim on improvements), and the entity is not registered for GST. When the house is sold for 600K, would my interpretation of paying 30% on 100k (30k) be correct, if this is so then isn’t one paying a tax on tax? Wouldn’t this make the tax on 100k of improvements in the order of 45% ?

Weren't the national party voters getting super excited about the prospects of income tax cuts not long ago? And now when they are offered them again they think it's the worst thing in the world. Should the National Party change its name to the Crony Capitalist Party?

Probably because the main beneficiaries will be the people who already pay no net tax and it transfers more of the burden onto anyone who has the audacity to earn over $70K.

Maybe Labour can change its name to the Anti-Middle Class Rich Pricks Party? Hurr durr.

I earn over $70k...no winging from me? Have paid income plus benefits from share/bond/commercial property/cash investing. Happy to pay capital gains tax where needed to level the playing field. Not sure where the issue is?

Mr "Scumbag" and "Rich Prick" Cullen's last insult. Last time Cullen screwed the country's economy up we were able to vote him out as he left us with a massive structural deficit predicted by treasury in the PREFU to balloon Govt debt to levels even higher than what National eventually managed to hold them down to. He has always been a nasty embittered, jealous and resentful man. Even in his maiden speech in 1981:

"And to my old school, Christ’s College. I am proud of the fact that my secondary education was not paid for by the taxpayers of New Zealand but by the farmers of Canterbury and Hawke’s Bay. I ripped them off for 5 years then, and I shall get stuck into them again in the next few years"

Then in 2008 as their fortunes waned he took to delighting in the crappy state he was leaving thing in: "Mr Key may find it difficult to give the tax cuts he wanted: "He'll find there isn't a lot of room left after Thursday afternoon." he was delighting in sabotaging the NZ economy to further his agenda and hurt his political opponents. Amongst all of their expensive lolly-scrambling to try and boost support 2008 saw a further Cullen bomb in the form of an appalling $0.7 billion dollar gift to Toll holdings to buy back a train system they sold to them for $1 dollar 5 years earlier, that cost ballooned to something like 1.5 billion with all the maintenance the govt then had to pay for.

So how the hell did he end up back here attempting to mangle the economy again when he made such an appalling mess of things last time? Stacking a Tax Working Group with an ideologically vetted group of embittered old socialists, left wing academics, union reps and ex bureaucrats with a couple of token voices for the productive parts of the economy and then declaring that 8 out of 11 voted for CGT is supposed to serve as some kind of veneer of legitimacy to sell this lemon? Never mind that majority of NZ oppose it. "Yes Minister" revealed as a documentary once more.

All the TWG members who weren’t flunkies or political appointees who had real world tax and legal experience voted against it seeing it for the mess it is.

https://taxworkinggroup.govt.nz/sites/default/files/2019-02/twg-bg-4050…

Amazing - a topic that has generated more comments than the housing market. Unique!

This is a tax on peoples savings for the future ie those who are taking personal responsibility for funding their retirements are being punished. Amy Adams ran circles around Nash and Robertson on this.

"so you want to buy my rental house and my car?, well you can have the house for same as I payed for it... however I'm very attached to my Corolla so wouldn't take anything less than $250,000 for it."

The policies seem to favour those who are salaried workers who invest only in Kiwisaver. It discourages investments or retirement planning. So I guess being stuck working for some companies and jumping straight into WINZ office at 65 is what the policies expects everyone to do.

As opposed to having to go to WINZ at 40 because you can't afford the rent and children like it is for many at present? And those are the people working for the companies and paying into kiwisaver (mostly..).... Instead of benefiting those who don't want to work for companies and insteand speculate on the price of houses?

How big is the black economy? Is cgt just a tool to try push more cashies onto the books (for investment/do up properties)?

... what a big yawn , wasn't it .... from the moment back when Sir Micky Cullen was installed as head of this latest tax working group ( anyone remember McLeod , and all the others ! ) we knew the outcome :

Sir Micky's frustrated ambition to blanket New Zealand in a CGT from his years as Helen Clark's finance minister, came bubbling back to the surface of the primeval ooze of his socialist ideological agenda ....

Leopard's don't change their spots , do they ....

... this tax working group was a complete waste of taxpayers money .... right down there with the referendum to change the flag ....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.