By David Chaston

I am looking forward to learning how much bank pressure has moved the RBNZ objective to get banks to hold more equity. Hopefully not much.

It is an issue I have been writing about for more than eight years.

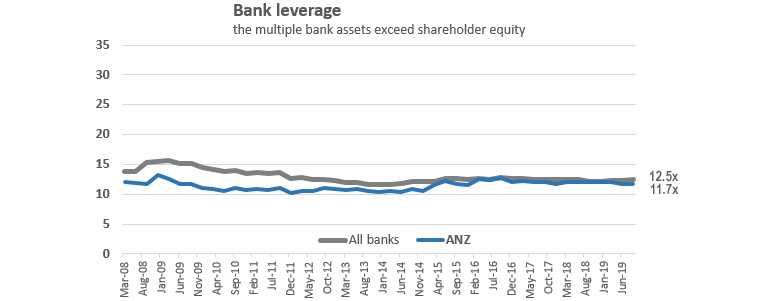

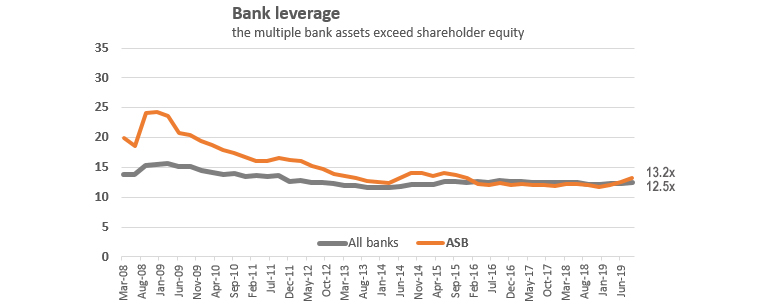

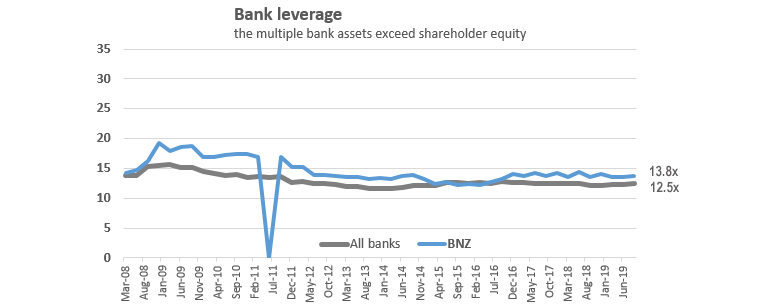

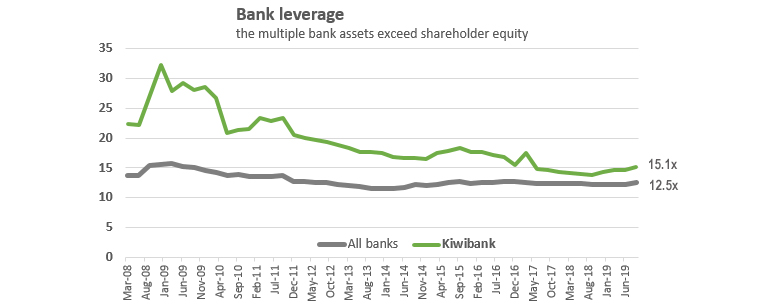

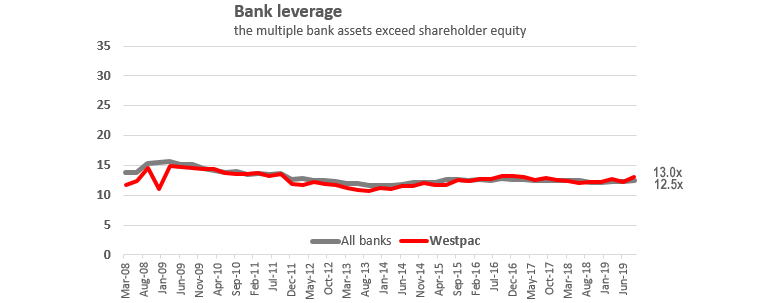

The lack of shareholder support for banks got to extreme levels in 2010, but they have not been adequate for more than 20 years. And the issue actually goes back further. Historical RBNZ data goes back to 1992 and nowhere in that time have bank shareholders stumped up adequate support for their businesses. The worst leverage was in December 1996 when it reached an industry average exceeding 26 times. That is, bank assets exceeded shareholder funds by 26.7 times. The 'best' was in March 2014 when it was 11.6 times.

Think about that for a moment; the time banks had the most support from their owners was when they only had 8.6% of their assets (loans, advances and other banking assets) supported by their shareholders. The heavy lifting has been done by depositors and other creditors. But the profits have been taken by the one party that has the least skin in the game.

And that high leverage allows out sized returns in institutions that are essentially regulated utilities.

It is an excess leverage situation that has been going on for so long, that long term extreme levels have been normalised. Even today, average leverage exceeds 12 times.

High leverage equates to high risk. But the risk isn't being faced by the shareholders. It is the depositors who are taking the risk, and because they are so disbursed and so numerous just about everyone understands that for the large institutions, ultimately it will be the taxpayer who will assume the risk of failure.

It should be an unacceptable trap that our economy has fallen into.

Things must change.

There are ironies aplenty here.

First is the obvious fact that bankers themselves would never lend to any other borrower with such extreme leverage.

Second is the equally obvious fact that this situation and its high risk environment only works with active government regulation. The regulators are enablers of low support by shareholders.

And thirdly, it only works because of the implicit guarantee from taxpayers. It's parasitic in that regard.

But even though it has been going on in a twisted version of 'normal' for more than a generation, finally our regulators are pushing back.

Shareholders need to expect lower returns, and invest more in their businesses.

It won't be hard for them to invest more. They are highly profitable and foregoing dividends for just a few years would bolster their investment quickly. The four big banks paid about $3.8 bln in dividends in the past year*, so they could reduce their leverage by 1.0x each year. In less than four years, overall bank leverage could be down to about 9x. In six years it could be reduced to under 8x. That is not an impossible standard - Rabobank NZ is already at that level and so is Heartland Bank. Yes, that would involve profitability without dividends (in other words, bank profitability wouldn't be degraded) and returns would fall from 13% tax paid to just under 9% after tax, and still high for a regulated utility. Dividends could then resume at the historical dollar level. (Or they could just add capital.) Of course investors would squawk. They would threaten, they would pressure, they would warn the-world-will-end. But I doubt there would be capital flight, or even an internal pause in enterprise capital investment, because these banks would still be returning out sized results that investors can't get in any other industry for the low risks they are taking.

Banks have tried to instil a fear among customers that the cost of debt will rise if they have to hold more capital. Of course, that is on the basis that they can continue to impose their currently high return on equity on their clients. This is weaponising fear on customers who are naive. If risk falls when more capital is retained, there is no need to extract such high returns. Bankers and investors need to revisit Investment 101. And regulators need to ensure normal competitive forces apply so that rent-seeking from an imbalance of pricing power doesn't happen.

That imbalance is longstanding, and another public policy challenge. Banks are, or should be, enabling utilities. They have social obligations to ensure our economy is lubricated efficiently. Their behaviour needs to respond to the social licence they have to operate at this choke point. Any kidnapping of economic efficiency is unacceptable. But operating in this space without sufficient equity investment is a form of economic kidnapping. Which is why I am hoping the Reserve Bank capital review is the start of a new effort to re-balance something that has been out of balance for far too long.

Better capitalised banks will more likely result in a better credit ratings. Better credit ratings bring expanded access to funding and lower funding costs.

Here is how the main banks have changed their leverage. One takeaway is that none of them have been reducing it in the year or so that the RBNZ capital review has been underway. That is the type of attitude the regulator is up against.

There's a long way to go. Let's hope the RBNZ makes a clear start on Thursday, December 5, 2019.

* This total excludes the dividends that ANZ and BNZ declared which were simply converted into shares in the New Zealand subsidiary in 2019. The comparative dividend total for 2018 was $3.6 bln.

48 Comments

maybe you will get your wish with our new governor.looks like he wants the banks to clean up their act.

I think you've hit the nail on the head, he "looks like he wanths the banks to clean up" but what has our directionless Orr done so far ?

Hmmhh he's dropped the OCR down to record levels, indicated he's happy to destroy the Bond market and go negative.

So at every turn he has done what he can to benefit well the BANKS and GOVT.

I know what my money is on......

A good article, and excellent thoughts.

For mine, the encouragement needed to make any intransigent bank recapitalisation is to let the RBNZ offer a savings account to any tax paying New Zealanders. Let them know that at the drop of a hat the banks' on-call depositor base could move to the safety of the sovereign. Leave the banks' (shareholders) with the risk of the loan book etc and competing for longer-term depositor funds based on price. At some stage, the message will get through.

RBNZ is proactive so should and will act.

This is new RBNZ........Hopefully.

Waiting for 5th December to hail the RBNZ governor....hopefully.

You reckon we should take him a garland :)

... if he's successful in his crusade to shake up the banks , place a garland of a red and a black dildo on his head ....

If he's unsuccessful , smack him in the face with it ...

... rejoice .. .

Great article, thanks David.

Most bank shareholders probably wouldn't have a problem with higher capital levels provided these are factored into the share price they pay. They might not want to be shareholders during the transition period however. To be honest, I wonder who exactly holds bank shares at the moment because it's not been a good time for them.

... if the government took a 51 % stake in the subsidiary of any overseas bank who operates in NZ , roundabout half of the $ 5 Billion of profits that leaves these shores annually would stay ...

Our you could just bank with Kiwibank...or other NZ bank....save the tax payer some mula.

Seems that a lot of people are already doing just that. Article from The Guardian: Not happy Westpac: how customers can show their discontent over banking scandals. https://www.theguardian.com/australia-news/2019/dec/01/not-happy-westpa…

The tough talking and threats coming back from the banks in response to RBNZ position will make the reserve bank think twice about whether it wants to proceed. I am picking there will be a small acknowledgement of the bank rhetoric. Oh Adrian Orr will have plenty to say to pad out his position come Thursday. It will be essentially 'we hear you, but....'. If the banks dont raise some interest rates in retaliation I will be surprised but that will be shortlived because of competition between the banks.

Agree that any blackmailing by bank to increase interest rate will not last because of competition and RBNZ should do what it should be doing though all banks and so called expers/ media with vested interest may cry foul a little but at the end everything will fall in place.

The bank's 'blackmailing' hand has been substantially weakened by the recent debacle at Westpac in Australia. (and CBA and NAB before that)

Does any local bank want the scrutiny of a Royal Commission here, as happened in their home country?

The Chairman/CEO of any local subsidiary should be taking whatever the RBNZ come out with without challenge. The last thing they'll want is 'someone' ferreting about in their accounts. There are highly paid jobs on the line, after all!

"Don't poke it, and it won't bite you"

"A long overdue rebalancing is required"

Will RBNZ be bold and do what is required for them to do in current challenging environment.

Also low / falling interest rate is a blunt knife and RBNZ if serious can try to control/give direction to undesired consequence of low interest rate ( Debt bubble in which average Kiwi specially FHB are being caught due to FOMO).

Wait and Watch : How RBNZ acts on 5th Dec.

I sincerely hope common sense prevails, at long last. Aussie Banks and anyone who is skimming off the rest of us is stupid.

Banks used to be the Safe place to put your money, now it is a nightmare...Cannot put your trust in em.

It is now a rort.

David the below statement is the most sensible that I have read this year, it's logical and factual..

"That imbalance is longstanding, and another public policy challenge. Banks are, or should be, enabling utilities. They have social obligations to ensure our economy is lubricated efficiently. Their behaviour needs to respond to the social licence they have to operate at this choke point. Any kidnapping of economic efficiency is unacceptable. But operating in this space without sufficient equity investment is a form of economic kidnapping. Which is why I am hoping the Reserve Bank capital review is the start of a new effort to re-balance something that has been out of balance for far too long."

Agree Dgm.

Accepting and highlighting itself is a good start.

.. if , ultimately it is the taxpayer via the government guarantee that will bail out a bank , should it fail ... should've each bank be required to pay an annual fee directly to the government .... a recompense for this guarantee ...

If they opt out ... no taxpayer backstop....

What is the break up of the shareholding of the Big 4 Aussie Banks which own the NZ subsidiaries ? That would give an idea as to who will or will not be ready and able to contribute to the increase in capital.

Also high time RBNZ also stipulates a ceiling on profit repatriation at say 60% or so maximum.

That will take care of future capital growth needed.

The time and psychology is right at present to push through these important measures in the national interest of Aotearoa.

It is a good first step. So far the banks have retaliated against the tightening of regulations by drastically cutting credit to business, eg going from 60% max loan to value ratio for commercial property (where it has been for years and years) to max 40%. Banks can lend 3 or 4 times as much against housing for a given amount of capital as they can if they lent to business, due to the smoke and mirrors weighting system.

Why does the RBNZ prioritise rising house prices over business lending? To what extent is our distorted banking system the result of international regulators turning them into regulated utilities that lend against housing assets and wage income? They are now no banks that lend primarily to small and medium sized businesses. Is over regulation coming out of Basle the cause of the problem? Banks just follow the incentives that society places before them.

Retaliation is about revenge. I wouldn’t expect professional boards to tolerate that. It’s more likely that banks will react to the new parameters and ratio business credit unless it gives the required return.

The times of socially conscious bankers is long gone. The only rationale they have now is profits and bonuses and perks. Their least concern is for the customers. Wonder why they still trot out customers as another stakeholder. In many countries it is the Government's stake and participation in the management of banks (by directors, etc) that result in socially beneficial business practices of banks. Left to themselves you know which businesses they will support, which is evident in all these scandals coming out. To give an example, Anti Money Laundering control/compliance is also a Government initiative, not a self regulatory act by the Banks.

There is more quid pro quo in banking than in any other industry/business.

It appears that RBNZ under previous managements has been complicit in several ways (slack regulation, allowing self certification, not thinking of adequate capital/reserves, implicit guarantee without any cost to the banks, etc) which have allowed the Aussie banks now to threaten and attempt to blackmail publicly our regulator/ government with rate rise, withdrawal of business, etc.

I still wish the Government would come out strongly in a more public way to support Orr in his moves to reign in the power of these trading banks, in the national interest. JA and GR too have roles to play and they should without further delay.

... and ... what is the downside of the RBNZ being tougher on those Aussie banks ? ... higher fees , higher mortgage rates ...

Maybe the downside would've meant less borrowing to buy houses ... ergo , lower current house prices .... I reckon we could've coped with that ...

Awesome article! Of course banks are licencenced public utilities operated at the grace of the public they are sposed to serve.

Another huge question is WHY simple concepts such as this are not taught in our schools? Anyone who can pass school c english... tbh I failed it.. can understand concepts like this.

Too many people understanding the hidden transfers that alway happen in times of crisis and otherwise would change the politics of money and power.

It might significantly reduce the number of people willing swap their life time for subsitance hourly wages in the service of their more informed betters.

Perhaps that would be a very good thing as society must inevitably adjust to the decoupling of wages, employment and productivity due to the rise of AI.

‘Shareholders need to expect lower returns and invest more in their business’

The first part is already happening as bank share prices continue to soften. The second part is problematic as long as banks remain the prime whipping boy of politicians and media. David makes the case well that shareholders have enjoyed strong dividends ( although glosses over that on a total return basis bank shares have been at best very average performers) but does not much consider the negative impact of future shareholder support reduction and withdrawal. I’m a long term bank shareholder but have been steadily reducing my exposure relative to the rest of my portfolio over the last 5 years. I’d have bailed completely several years ago if not for the elevated dividends David identifies and and may yet do so while I’m still ahead. I note with interest the increasingly downbeat position of analysts on banks and there is a similar trend in share forum chat. David’s advocacy for a kinder and fairer banking world ignores the reality of the more attractive investment options than banks for any new money.

So you're threatening to withdraw your bank investment and move that money into investment in something that actually produces something other than increasing levels of debt?

Oh well, so be it.

And if bank share prices, say, halved as a result of any change, what would you do?

Answer: It depends on the level of dividend payment at that new share price. Exactly! Maybe you'd reinvest down there, or buy more if you'd 'got caught' with a holding?

It's like the old Telecom, that was paying 12% dividend, then 'the rules' were changed by the Government, and the share price fell from about $12 to $6. The dividend was slashed, but so was the share price. Eventually, the share price went to $4 odd ( and Chorus was spun out) but that's how it's supposed to work.

Nothing stays the same forever.

Obviously share prices reflect projected return on capital and as an equity investor I’m well used to and accept price fluctuations. But I react to significant downside risk not just by repositioning my holdings but also by not supporting capital raises. Which is a risk in respect of banks that I think is real but which David rather lightly dismisses.

Good article. Banks are sucking the financial life out NZ. High rents, people living in garages, both parents working, and the stupid house prices are all drive the extraction of money via leveraged debt. It is quite parasitic in nature, a parasite that is at the tipping point of the parasite being heavier that the host. Global printing and low rates is the banking parasite fighting to keep its position suck all that is good from its host. In another financial shock are we going to see negative interest rates?

Bring on the 5th of Dec and stay the course. Banks will react. Picking those that just leveraged up again on cheap money will regret it. Bull Trap.

Everyone is expecting too much from RBNZ governor (For a change RBNZ governor is generating confidence in average Kiwi).

Will it be Orr...or will it be Err.....

Wait till 5th December .....Will he be a Hero or Zero.....

Very good article David. In light of what's been happening with the Australian banks and recently with the Westpac fiasco, will the RBNZ finally put a "Saver Deposit Guarantee Scheme" in place, since we're the only Western country in the world not to have one, There's been a lot of talk on this but so far not action?

Agree excellent well thought and meaningfull article.

As you may recall from a previous article, (and here) I hope they don't. It's a dreadful 'moral hazard' and will be paid for by lower bank interest offer rates. You only have to look at other countries that have it to see how that discount will be applied. Safer banks should make a deposit guarantee unnecessary. But I fear, given it is election year next year, that one will come here soon. Sadly when it is in place, most savers will regret it (big time) and whine louder about low returns. Be careful what you wish for.

Agree with you on that, David, I hope we do not go there. And yes, safer banks should make it unnecessary. Hopefully, that's also Orr's thinking with these proposals.

'look at other countries"? I presume you are referring to the rest of developed and not so develpoed countries have decided that the moral hazard of deposit insurance you speak of is irrelevant....either that or they are simply not as morally superior to you David?

I would be interested if you could give me the numbers to back up your assertion that a deposit guarantee would make any significant difference to the interest paid to depositors. The spreads are so fantastic between what the banks borrow at and what they charge that it will be absorbed without much fanfare. The Govt. must have produced some numbers as to how it will be funded? And why do think interest paid to depositors would be any less under deposit guarantee funding than increased capital requirements. Not against either, just wondering where you are getting your numbers to back such a statement?

The whole 'Moral Hazard' thing is irrelevant...all the mum and pop depositors can never hope be as financially educated or morally superior as you David...what you are therefore saying is hardly anyone should be depositing their money in any bank because they don't understand the intricacies of that particular banks lending portfolio. And that is precisely where deposit Insurance comes into play as a safety net for us ignoramus's. If people don't deposit, the banks don't loan and the country fails financially, so it is in a governments interest (government being the people!), to have a secure financial system to protect against bank failures, just like insuring your house. Is it worth insuring your house...yes, it costs you a small percentage of the value of the house...is it worth it?...ask 99% of house owners and they will say yes...same with deposit insurance....the only criminal part about house insurance is that it is taxed (GST)..now, will the gov tax deposit insurance as well...stay tuned

Tui Wai Smith,

Well put. The moral hazard argument is rubbish, or at least much less relevant than giving ordinary depositors peace of mind. Even if the RB's capital proposals are fully implemented, it still leaves depositors potentially exposed. If a major bank were to be seen as vulnerable, then not only could there be a 'run on the bank', but much worse, 'contagion'. And what would happen then? as sure as night follows day, the government would have no choice but to step in with a full deposit guarantee. Sounds familiar?

We need a Deposit Guarantee scheme and the sooner the better.

The OBR deals with the issue of a run on the bank, but to my mind its shareholders alone that should take the haircut.

maybe you're right...hence deposit insurance would be in the best interest of the depositor.

What about the 'moral hazard' in the TBTF that is pervading the western banking ?

Even South Canterbury Finance investors were saved with tax payers money, right ? Why no one talked about moral hazard then ? Because it was beneficial to the rich mostly ?

TBTF is costing and will cost the tax payers (including bank customers) more than the 'moral hazard' of some deposit insurance for smaller depositors, say up to $100k.

We can't give into the banks' threats to raise rates/fees/withdraw business at the drop of the hat.

Good article, but there is one thing that perplexes me.

"Bank shareholders" are often portrayed as a privileged group.

Their shares are available on the open market, and my understanding of markets is that over time, the market will price in any known advantages/disadvantages as a premium/discount.

Am I missing something?

Ideas and views expressed on interest.co.nz reflects the sentiment of the nation.

Normally media and experts toe the line of rich and powerfull lobby but not this time.

Congrats.

Best article I've seen on interest. Pretty much sums up who's responsible for our current housing debacle

Realisation is good but just acceptance will not help without Action (though acceptance of crisis/disease is first step and equally important).

It is long overdue and RBNZ should take strong step to control.

I was going to write a different comment about why bank shareholders should support this but then I realised why the status quo is optimal for them.

There are essentially two scenarios for banks:

A) make a lot of money without using your equity to bail yourself out

B) lose a lot of money bailing (or trying to bail) yourself out.

In scenario A you want enough equity to ride out the day to day stuff and your run of the mill recession.

In scenario B you want the minimum possible equity.

Why? Let’s consider three scenarios:

(A) Bank has equity common today among Australian banks, gets wiped out, debt greater than equity.

(B) Bank has double equity today, gets wiped out, debt greater than equity.

(C) Bank has triple equity today, loses two thirds, lives to fight another day.

For arguments sake let’s assume these are the only possibilities. Let’s also assume no government bailout.

The way I see it the bank shareholder is choosing from three options (where they set equity reserves not government regulation):

(A) Lose 1x, profits the same

(B) Lose 2x, profits the same

(C) Lose 2x, profits the same.

So, if you accept my game theory, it’s always worth minimising the equity in the bank. Because you harvest the gains while the going is good and in the 100 year event you shut up shop and take the hit. Trying to build a reserve to survive a 1 in 100 year financial loss only increases the loss you take. Plus it encumbers you in the interim. Keep things lean to minimise your loses.

Too long, didn’t read - we need regulation because the incentives mean banks will set themselves up to lose in very low probability events.

It is long overdue David - but don't put your hope too high, addiction to profit is already the norm. The RBNZ independence now days, influence largely by market sentiments. All those significant regulatory measures, will only crystallised after the major economic event.

For what it's worth, I think he will give some ground on the implementation period, raising it from 5 to say 7 years and possibly on what constitutes allowable Tier 1 capital, but will largely stick to his guns. I certainly hope so. Bank leverage must come down.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.