This week’s Top 5 comes from Infometrics senior economist Brad Olsen.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Housing looks set to continue dominating headlines in 2020, as house prices look to rally again and rent pressures grow. Who’s got property, who’s paying for property, and how many need property will all be key issues through the year as we build towards another election. But separate from that, the spotlight will keep shining on the housing market as New Zealand’s primary method of wealth creation. With so much money and interest wrapped up in property, here are some of the components to watch in 2020.

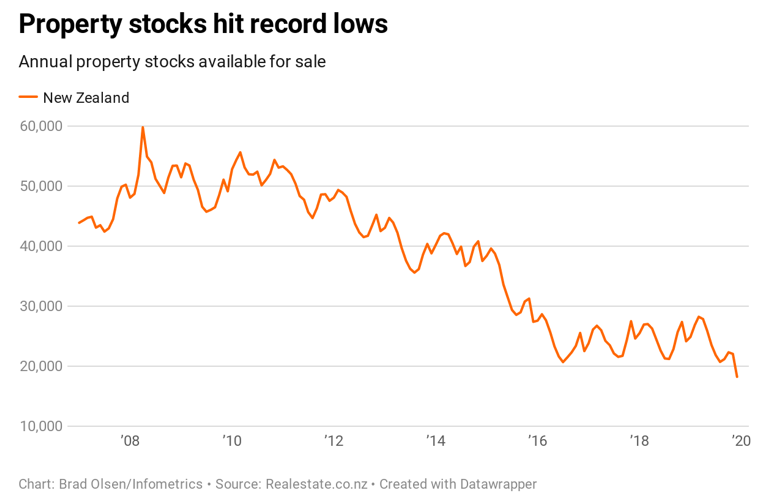

Year-end figures from realestate.co.nz paint a picture of renewed house price growth in 2020, driven by low stock numbers available. With less stock available for purchase, prices are heading higher as buyers bid up prices to secure a piece of the small amount of remaining stock. Stocks are at their lowest since realestate.co.nz records began in 2007, with just over 18,000 houses on the market in 2019.

“Taylor said that in times of shortage, people also tended to buy before they sold.

"Given the limited choice of homes available, people are often reluctant to sell without having somewhere to go – especially if the rental market in their area is cramped. This then has a flow-on effect with homes coming off the market before new ones go up for sale."

Low stocks will continue to push house prices higher, with stronger than expected population growth also contributing to higher demand, even as supply remains constrained. It looks like 2020 will see strong gains again in the housing market, with low interest rates also enabling more buyer action.

2. Mum and dad investors dominate property investment

New analysis from Herald journalist Kirsty Johnson and Ramifier has provided a fresh and comprehensive view of house ownership in New Zealand. The results show the importance of “mum and dad” investors who own between two and seven properties, with this group making up 40% of ownership across the country.

“[The analysis] shows 30 per cent of homes are owned by people who only own one home.

Another 13 per cent is owned by people who have two homes. Six per cent is owned by people who have three homes. Ten per cent is owned by people who have between four and six homes.

And another 10 per cent is owned by those who have between seven and 20 homes.”

Given the sustained commentary on New Zealand’s rental market, I suspect that the key ‘battle’ in the housing sector remains between landlords and renters. Often, conversations around landlords view them as all professional landlords, whereas this analysis shows that many are part-time. In 2020, with increased rental reforms seeing higher costs imposed on landlords, and with rents heading higher as a consequence, this battle of landlords vs renters will only heat up further. In designing and implementing changes to new Zealand’s rental market, it will be increasingly important to understand who landlords actually are to ensure that proposals will see the actions they expect.

3. Rents are continuing to rise, as interest rises but listings remains flat.

Rents continue to rise across New Zealand, with rental inflation over the 2019 calendar year running at 5.3%pa. Certain parts of the country are bracing for the usual spike in rental market activity as students flock back to their studies and interest levels eclipse the number of rentals available.

“Trade Me Property’s Aaron Clancy said the number of properties available to rent was fairly flat compared to last year while demand, on the other hand, was up 17 per cent.

“The pace of rent growth across the country will be alarming for a lot of tenants and the trend we’re seeing now suggests the peak season in summer is going to deliver some new price records. Demand for rentals has increased enormously year-on-year and until there’s a spike in supply high rents will be the new normal.”

December’s Trade Me Rental Price Index release sets the tone for the rental market in early 2020 and is worth watching over coming months. The question from everyone is where the rental market is going from here. The answer is, still up. Sustained population growth, lower home ownership rates, and increased rental costs (due to stricter standards) will keep the pressure on rents in 2020. Without a change in supply, this trend will likely continue.

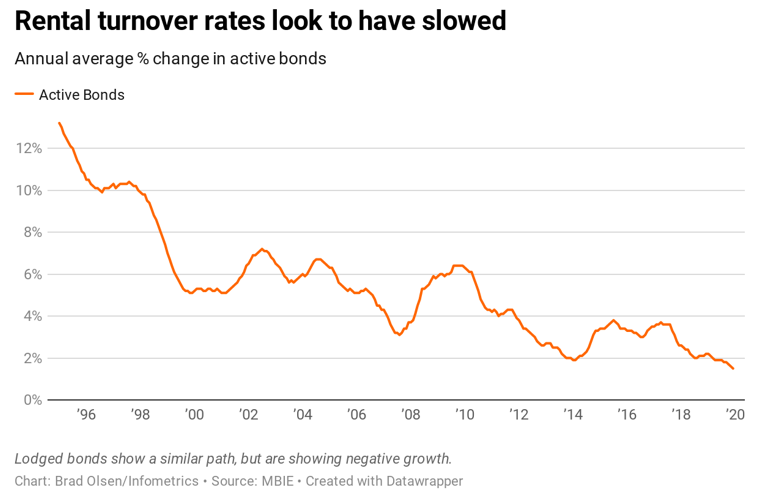

It’s important to note that, across the country, rental turnover rates look to be low. This lower turnover suggests both that more people are staying in their current rentals to ensure they keep a roof over their head, and that landlords are staying in the market even as costs are rising, as rental investment gains remain better than other investments out there.

4. More people needing housing assistance as the squeeze continues

Housing pressures for those unable to afford housing themselves will remain in the spotlight in 2020, even as the high build rate starts to drill into the housing shortage across the country. Some parts of New Zealand are seeing rapidly accelerating housing stress as urban centres become too expensive to buy or rent. As a result, commuter areas become a focus area for living, which is making those at the lower end of the housing spectrum are becoming increasingly vulnerable as they are priced out of commuter areas too. This trend is well evidenced by the rise in the social housing register in the Wellington region outside of Wellington City.

“Lower Hutt's social housing wait list has jumped 42 per cent in just one month highlighting mounting pressure on the Wellington region's market.

Those who are most vulnerable are being priced out as people look further afield from the capital to buy properties and secure rentals.

…

Nationally, MSD social housing wait lists have quadrupled over the past four years.

Wellington City's waiting list is in line with that trend but Lower Hutt's is growing at twice the national increase.”

Ensuring development capacity is available for construction will be key to unlocking new housing areas. Work by various councils around New Zealand in 2020/21 to examine and review their District Plans will be vital to properly zone and resource new areas. This work is particularly critical for areas outside the main urban centres who will continue to experience the spill over of higher urban housing prices.

5. What next after the Decade of Housing?

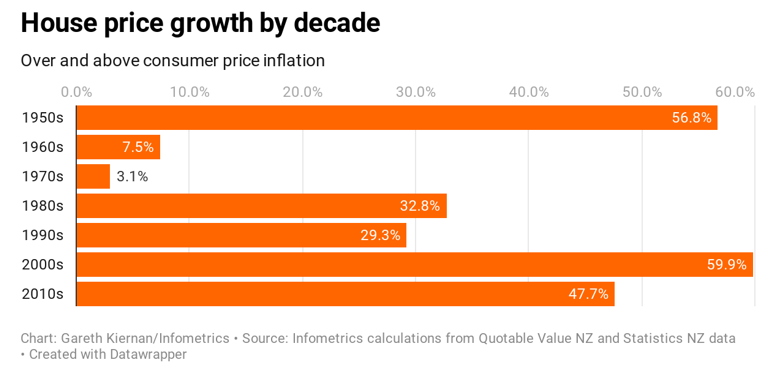

In my mind, the 2010s can be looked back on in New Zealand’s history as the Decade of Housing. Not because it saw the highest house price growth (although it was still high), but because of the rapid and sustained growth in prices at the same time as housing pressures pervaded New Zealand’s consciousness. A housing ‘crisis’, higher house prices, rising rental costs, housing shortages, investment gains on property, and a significant rise in unmet need for housing have all contributed in our fixation on the roof above our heads. But what’s next? Infometrics Chief Forecaster Gareth Kiernan, in a recent opinion piece, reckons that we are making headway on our housing supply:

“It is improbable that the housing undersupply issues that developed throughout the last decade will persist for another 10 years. The residential build rate is at its highest since 1974, and our analysis suggests it has started to reduce the undersupply of housing in key areas such as Auckland. Historically, New Zealand’s construction cycle has typically been very boom-bust, meaning that residential development could continue at high levels until there is a clear oversupply of housing. This cyclical pattern looks likely to place downward pressure on property prices within the next 3-5 years.”

It’s clear that we’re starting to address issues in the New Zealand housing market – the question now is the pace at which they are solved. Key work ongoing to funded increased infrastructure spending and speed up developments, alongside zoning changes and strengthening the building sector itself, will all continue to assist additional housing supply. But it will still take a while before any success can be claimed.

54 Comments

We need a huge increase in public housing to solve the issue, unfortunately the incumbent and any potential government has not the appetite to do anything about it

Exactly.

The rhetoric is around regulation. While important, it conveniently ignores the fact that the crisis won't be properly addressed unless the govt ups its delivery big time

Or reduces immigration

I agree. Plus an urban growth reform agenda.

"With less stock available for purchase, prices are heading higher as buyers bid up". Really though we're certainly not seeing those bid up price results in the auction listings and we're past mid January now....?

So far only 2 properties have been shown as being sold at auction this year and they're both in Tauranga.

Perhaps we'll see the flood homes on the market soon brandishing their 'SOLD' signs!

People are just starting up the marketing plan after the Xmas break now, Auctions wont get going for another 4-6 weeks. And lots of sellers aren't doing auctions, Deadline sales seem to be very popular at the moment.

Yep no doubt though property listing do appear to be up in the expensive areas like Remuera (Currently at 104) and AKL City Centre (616 listings) could it be that they're over priced?

Housing to dominate 2020 headlines.... That is just fantastic, look forward to it!

So long as we never.. never ever mention the rate of population growth.

I suggest two problem solvers. Firstly cut immigration in half this year & then in half again next year. Second discourage those that cannot afford children (& thereby afford housing) to stop breeding. The government could pay for a maximum of three children per family on benefits. They can have more, but no more money.

LJM You'll only get that demographic responsible for having excessive children at the expense of the taxpayer to curtail this activity by ensuring they use contraception; unfortunately the males of this demographic just don't want to do this and the solo mothers go along with this. The question is why won't the females of this demographic use contraception when it is available free of charge? Is it because they want to make a life-style choice of having more and more children (at the expense of the taxpayer), or are they somehow desperately not wanting to upset the males who possibly see it as very manly (macho) to have children to multiple mothers. I don't know what the answer is myself.

When the youngest child turns 2 the solo mums have seeking employment obligations. So the idea is to have another child before that happens.

Yes, that sounds right. It should be noted that since October 2019 the mothers have been absolved (by the Labour Government) from having to name the fathers. The fathers can now continue their irresponsible behaviour without having to contribute a cent to the child's upbringing.

The mothers will be relieved as they don't want to face repercussions from the male for naming him as the father.

Meanwhile some of these mothers have cottoned on to the idea that the prior sanctions were wrong, therefore they may be entitled to recompense for their lost benefit payments often resulting in thousands of dollars of payouts. All under section 70a.

Irrespective of who own the houses (if they are not professional landlords, then what are they?) landlords are pretty predatory for rents. I continue to believe the real solution to the crisis on affordable housing is rent controls, despite the denials of vested interest. Yes there needs to be many more houses built but i don't believe that will impact the affordability issue. Even the 'mum and dad investors' made a business decision to buy a residential property to rent. So if they then paid too much for that property to be able to charge an affordable rent, then that is on them. They should not be able to expect their rents to be subsidised by the tax payer through accommodation supplements.

An immigration still seems to be having an impact on this issue, with an ever growing, but undiscussed elephant in the room - just how much population can a town/city/region/the country support without a negative impact on the environment or available resources?

I lived under rent controls (London early seventies) and do not recommend them at least not if draconian. We had the most empty houses in Europe and the worst homelessness and there was a positive preference for shared tenancies to foreign students. Admittedly there is much in devil in the detail. Best solution is more houses and maybe some reward to tenants & landlords when a tenancy lasts for more than say 3 years.

After some push back from a few a couple of years ago, I did a little research into the international experience with rent controls, and found that as you suggest the devil was in the details. Landlords were given scope to push back against the legislation, essentially holding their communities to ransom, and of course they did this. Hence the mess you refer to. Housing, especially housing for rent needs to be fully and thoroughly regulated, including how much is charged for rents. An analogy is cars - imaging if you will there was only one law to govern all traffic. it might be speed or condition, but not both. what kind of state do you think our road traffic would be in? Apply this same principle to housing - landlords limited only in the amount of rent they could charge. This is what happened in all cases I could identify, just one rule of significance. Thus it turned into a mess.

Minimum tenancy lengths wouldn’t really work for people posted somewhere for work for a year or students studying for 1-3 years. If you make it so that the tenant chooses the length of tenancy then you get that “strong preference for foreign students” reappearing.

Capital gains controls would be more effective

If there was enough of a push on public housing, and the government carried on renting based on 25 - 30% of income, the drive downward in the private market would be inevitable. Obviously this would take many years to normalise.

Expect the crisis to just get worse. The current govt are nearly as bad as the last lot on this issue, and that is saying something.

I propose a 200% capital gains tax on politicians houses. Every dollar they go up in value costs them a dollar.

Once properly incentivised they might choose doing something about our real problems instead of just pulling sad face and signalling their faux empathy at each photo-op.

Perhaps they could also be personally responsible for housing a good portion of the non-kiwis they insist on overwhelming our country with. We might find they are no longer so keen on shoving mass immigration down our throats.

Ha ha

Funny.

And sadly true.

Its definitely going to be a big year for the topic!

Has anyone done the maths (in a rough way perhaps) to invert the Herald's recent statistics on home ownership - to let us see how many people in NZ own a single home?

I can see it is not a simple inversion since some people invest on their own, whereas some are effectively a family of 2 adults and 4 kids that own properties between them.

Not much support in this article for those who are predicting a bubble burst.

That's so "last decade"

Historically low and ever declining interest rates favor the incumbents. Lower interest rates favor higher asset prices. For the first time ever a half million mortgage is required to purchase the median priced New Zealand home , with a twenty percent deposit. Higher house prices almost by default equate to higher rents .Higher rents , more difficulty in growing a deposit. Lower and slower household formation , lower home ownership rates, lower housing turnover. A classic ponzi scheme.

Cowpat

Re: "A ponzi scheme"

Sounds similar to the bitter comment when dropped by a bird that you really do fancy - "She’s a sl*g".

The success of Japan's public housing only really occured in the aftermath of WWII and the national goal of becoming an economic powerhouse as opposed to being an imperialist tyrant. They realized it was better to be inclusive as opposed to exclusive and affordable housing was necessary to meet their goals. Compare that to the Anglosphere where the only option left seems to be competing for the rents of a perennial underclass subsidized by the govt. Somehow I cannot see this ending well.

Anyway, the NZ bubble seems to be just part of a global master plan to jack the price of every conceivable asset owned by the boomer generation. And there seems to be an expectation that the next generations are going to pay absurd prices for everything to keep the charade humming along. Funny thing is (even though you won't read it in Granny Herald or see it on the idiot box) that incomes appear to going nowhere while govts are doing their utmost to suppress labor costs.

Yes. The west is wedded to a neoliberal paradigm in housing.

But it's not "neoliberal" in my sense of the word (except for the banks to do what they want enabled by the central banks and a dysfunctional bureaucratic class). It seems to be closer to a scoiopathic "planned economy". Now Japan is not perfect but they have done far better to ensure that people can have shelter that's within their economic means regardless of where one sits on the socio-economic ladder.

It's neoliberal in the sense that western governments have relieved themselves of housing duties, relying instead on 'enabling the market's through smaller govt. Its trickle down bullshit

To some extent I agree, but what do you think would happen in NZ and Australia if you removed all the middle-class welfare? Its existence has nothing to do with neoliberalism.

Remember that neo-liberalism is not classical liberalism. It's an amalgam of intervention and free market notions, but which ultimately aims to reduce government without going as far as classical liberalism (which is simply a theory, it would never be achievable). And has the side effect (intentional?) of feathering the caps of the wealthy, and disempowering the poor. Some centre-left governments have been among the greatest proponents of neoliberalism eg. Clinton.

Providing welfare benefits is quite compatible with neoliberalism. Much more than building and managing houses.

@Fritz. The gov hasn’t relieved themselves of housing duties at all. In fact the do a great job in making sure it continually goes up. There’s no real “market” unfortunately. It’s more planned economy than free market.

Every politican promises a solution and none deliver. I reckon every commentator on this site could solve our housing problem so it is merely a matter of determination by our govt.

My solution - a referendum requiring all MPs to sell all investment properties owned by them or their family by public auction within say a month of being elected. If there was no self interest in parliament solutions would be found. My prediction such a referendum would gain overwhelming support and once it passed our housing bubble would burst long before the new law actually took effect.

Not sure I agree. But I do think that Bill English should have been fired when it was discovered he was double-dipping on his housing allowances. In the private sector, there would have been far more scrutiny (unless you sit atop the food chain in a commercial bank).

Fairly certain he was using the green party’s model and that he paid it all back despite not being required to? He likely had legal and tax advise regarding it.

If you thought that about Bill English then Simon Bridges will not be pleasing to you:

MPs' property loophole 'stings taxpayers'

It appears that he is still using that Private Superannuation Scheme where the loophole has been closed for their own properties held in a Trust. It's still on the pecuniary interests register, last time I looked. Seems awfully like what folk described as "Double Dipping" in Bill English's case.

Does Simon have genuine concern for NZ's taxpayers not being stung too hard?

If you thought that about Bill English then Simon Bridges will not be pleasing to you:

Correct. Bridges accepts the status quo of entitlement. Then again, I can't really think of any NZ politician that doesn't have a peculiar sense of entitlement. Perhaps Nandor Tanczos was the last with any real integrity.

I do not believe failure to get house prices down and/or immigration under control is deliberate and purposeful corruption by MPs (many would be financially better off out of parliament) but I do think it influences MPs into listening to those who are interested (real estate investors, etc) rather than those who are sleeping in garages. My proposal is similar to ministers putting businesses they own into limbo while they are making decisions relevant to their businesses. The simple act of selling investment property (for those who own it) would focus their minds.

""social housing wait lists have quadrupled over the past four years"" - that could cost Labour the next election.

Agree. They will try to blame the previous govt, but there is a limit to the credibility of that assertion.

In my opinion, Twyford's incompetence is a big part of this government's failure, and Ardern is culpable with regard to that.

Twyford's incompetence

Bit harsh don't you think? Twyford is only the product of a system. Perhaps NZ as a society is "incompetent."

I don't think its harsh. I know for a fact what he was advised, and what he ignored - wrongly.

But you do make a valid point, that collectively NZ doesn't seem to have a clue. Lots of people who call themselves 'experts', and some have good ideas, but it's not brought together as an integrated whole.

I could tell you within 5 brief points what could be done to make a meaningful difference. It's not rocket science, at all, yet it is made out to be.

Phil Twyford is certainly part of a Cabinet which has collective responsibility. Also Jacinda as the PM is responsible for portfolio allocation and oversight. Grant Robertson is in charge of finances. In any government the PM and the Finance Minister are usually the two main characters. David Parker as Minister of the Environment is responsible for reforming the RMA (panel in progress). Jenny Salesa construction and building materials. Megan Woods took over the housing portfolio in May. Kris Faafoi is in charge social housing...

Don't forget that git in charge of immigration....

There are limits to that, but the previous government as doing the same after 8 years of their own governance. So the limit may be a little more than 3 years, especially on such a large mess as housing.

The graph "House Price Growth by Decade" is interesting.

A couple of takeaways:

- After the past decade of rapid growth and issues of affordability coming to the fore, it shows that since the 1950's, the past decade has seen only the third most rapid period of housing growth above the inflation.

- Over the past seven decades, and especially so over the past four decades, house prices increases have been greater than inflation so have provided actual capital gains; it is no wonder Kiwis have a love of home ownership and property investment.

Meh. Needs proper context such as an adjustment for h'hold income.

JC

Agreed - however it is related to inflation so should be reasonably consistent with wages.

To me the biggie is the 1950s with considerable house price inflation; socially single income so potentially less disposal and savings income.

Would be interested in seeing the graph as a basis for an article.

I remain concerned that homeownership (from memory) for 24 to 35 year olds has dropped from 65% in 1988 to 35% in 2018. A socioeconomic issue that needs to be confronted and not piecemeal politicking as currently.

I think the bigger question is the 30-40 year old demographic.

In the last 30 years there's been a move to young peoepl wanting to be less committed in their 20s, ie. work and travel overseas.

But from my own experience, many people are starting to think of settling down once they hit late 20s / 30, so I think that is the more relevant age group

Fritz

Agreed.

Also other issues such as student loans which didn't exist in 1988; student loan repayments at 12% on top of income tax on $65,000 is over $19,000 pa.

Indeed, referencing it against CPI is rubbish for several reasons.

1) CPI already includes a cost of housing component, so its self-correlated to a degree.

2) Nothing to do with buying a house is inflation adjusted, everything is in nominal dollars.

3) Most peoples income isn't CPI-adjusted, and that what pays the mortgage.

House prices vs incomes (post tax preferably) makes sense, you pay for your house from your income. And the effect of interest rates needs to be accounted for. And it would be good to do it for at least three income bands, say 20th percentile, median, and 80th percentile?

..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.