This Top 5 COVID-19 Alert Level 3 special comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Following the Prime Minister's announcement on Monday afternoon, this should be the last Top 5 Alert Level 3 special. Certainly in my house the parents are really looking forward to the kids going back to school, and the kids are even looking forward to going back. Hopefully we'll then be free from the type of home schooling special demonstrated below...

1) Pandemics depress the economy, public health interventions do not: Evidence from the 1918 Flu.

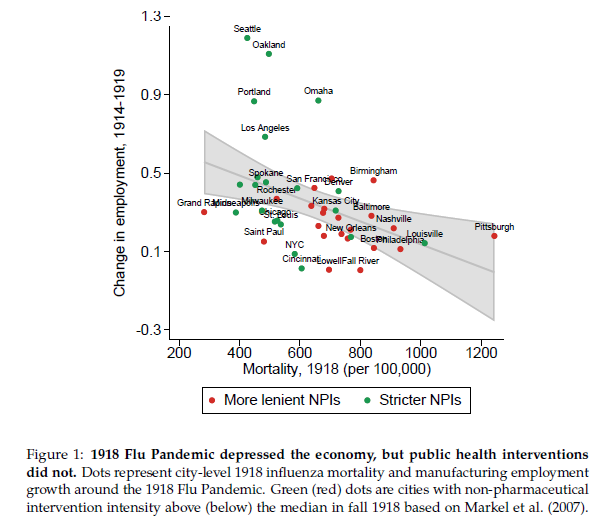

This academic paper probes the impact of pandemics and the associated public health responses on the real economy, looking at evidence from the 1918 Flu Pandemic in the United States. The authors find cities that intervened earlier and more aggressively do not perform worse and, if anything, grow faster after

the pandemic is over. The findings therefore suggest non-pharmaceutical interventions not only lower mortality, they might also mitigate the adverse economic consequences of a pandemic.

The paper is obviously interesting against the backdrop of what's going on across much of the world right now, and also in terms of the tough lockdown implemented here in New Zealand. The authors are Sergio Correia from the Board of Governors of the Federal Reserve System, Stephen Luck from the Federal Reserve Bank of New York, and Emil Verner from the Massachusetts Institute of Technology - Sloan School of Management.

Our analysis yields two main insights. First, we find that areas that were more severely affected by the 1918 Flu Pandemic see a sharp and persistent decline in real economic activity. Second, we find that early and extensive NPIs [non-pharmaceutical interventions] have no adverse effect on local economic outcomes. On the contrary, cities that intervened earlier and more aggressively experience a relative increase in real economic activity after the pandemic. Altogether, our findings suggest that pandemics can have substantial economic costs, and NPIs cannot only be means to lower mortality but may also have economic merits by mitigating the adverse impact of the pandemic.

Our two main findings are summarized in Figure 1, which shows the city-level correlation between 1918 Flu mortality and the growth in manufacturing employment from 1914 to 1919 census years.1 As the figure reveals, higher mortality during the 1918 Flu is associated with a relative decline in economic activity. The figure further splits cities into those that were more and less aggressive in their use of NPIs. Cities that implemented stricter NPIs (green dots) tend to be clustered in the upper-left region (low mortality, high growth), while cities with more lenient NPIs (red dots) are clustered in the lower-right region (high mortality, low growth). This suggests that NPIs play a role in attenuating mortality, but without reducing economic activity. If anything, cities with stricter NPIs during the pandemic perform better in the year after the pandemic.

Altogether, our evidence implies that pandemics are highly disruptive for economic activity. However, timely measures that mitigate the severity of the pandemic may also reduce the severity of the persistent economic downturn. That is, NPIs can reduce mortality while at the same time being economically beneficial.

When interpreting our findings, there are several important caveats to keep in mind. First, our analysis is limited to data on 30 states and 43 to 66 cities. Second, data on manufacturing activity is not available in all years, so we cannot carefully examine pre-trends between 1914 and 1919 for the manufacturing activity outcomes. Third, the economic environment toward the end of 1918 was unusual due to the end of WWI. Fourth, our cross-regional analysis does not allow us to capture aggregate general equilibrium effects.

Finally, while there are important economic lessons from the 1918 Flu for today’s COVID-19 pandemic, we stress the limits of external validity. Estimates suggest that 1918 Flu was more deadly than COVID-19, especially for prime-age workers, which also suggests more severe economic impacts of the 1918 Flu. The complex nature of modern global supply chains, the larger role of services, and improvements in communication technology are mechanisms we cannot capture in our analysis, but these are important factors for understanding the macroeconomic effects of COVID-19.

2) The threat of enfeebled great powers.

Writing for Project Syndicate, Arvind Subramanian sees three watershed events coming out of the COVID-19 crisis. These are the end of Europe’s integration project, the end of a united, functional America, and the end of the implicit social compact between the Chinese state and its citizens. This means all three major powers will emerge from the pandemic internally weakened, undermining their ability to provide global leadership.

In an excellent article Subramanian has some tough language for Europe.

The continent’s leaders have faltered and dithered, from European Central Bank President Christine Lagarde’s apparent gaffe in March – when she said that the ECB was “not here to close spreads” between member states’ borrowing costs – to the bickering over debt mutualization and COVID-19 rescue funds and the reluctant, grudging incrementalism of the latest agreement.

And:

Suppose, as seems likely, that the successful economies of the EU core recover from the crisis while those on the bloc’s periphery falter. No political integration project can survive a narrative featuring a permanent underclass of countries that do not share their neighbors’ prosperity in good times and are left to their own devices when calamity strikes.

The US cops it too.

But so far, the world’s richest country has been by far the worst at coping with the pandemic. Although the US has less than 5% of the world’s population, it currently accounts for about 24% of total confirmed COVID-19 deaths and 32% of all cases.

In rapid succession, therefore, America’s credibility and global leadership have been buffeted by imperial overreach (the Iraq war), a rigged economic system (the global financial crisis), political dysfunction (the Trump presidency), and now staggering incompetence in tackling COVID-19. The cumulative blow is devastating, even if it is not yet fatal.

And then there's China. He argues the crisis will probably hurt China’s long-term economic prospects.

First, the Chinese authorities’ terrible initial handling of the pandemic, and in particular their catastrophic suppression of the truth about the COVID-19 outbreak in Wuhan, has called the regime’s legitimacy and competence into question. After all, the social contract looks less attractive if the state cannot guarantee citizens’ basic wellbeing, including life itself. China’s true COVID-19 death toll, which is almost certainly higher than the authorities are admitting, will eventually come to light. So, too, will the stark contrast with the exemplary response to the pandemic by the freer societies of Taiwan and Hong Kong.

Second, the pandemic could lead to an external squeeze on trade, investment, and finance. If the world deglobalizes as a result of COVID-19, other countries will almost certainly look to reduce their reliance on China, thus shrinking the country’s trading opportunities. Similarly, more Chinese companies will be blocked from investing abroad, and not just on security grounds – as India has recently signaled, for example. And China’s Belt and Road Initiative – its laudable effort to boost its soft power by building trade and communications infrastructure from Asia to Europe – is at risk of unraveling as its pandemic-ravaged poorer participants start defaulting on onerous loans.

Subramanian argues by further weakening the internal cohesion of the world’s leading powers, the COVID-19 crisis threatens to leave the world even more rudderless, unstable, and conflict-prone than it was before the virus came along.

The sense of three endings in Europe, America, and China is pregnant with such grim geopolitical possibilities.

There's an interesting take on getting COVID-19 here from virologist Peter Piot. He's director of the London School of Hygiene & Tropical Medicine. He got COVID-19 in mid-March, spent a week in hospital, and has been recovering at home in London since. Piot, 71, was one of the discoverers of the Ebola virus in 1976, headed up the Joint United Nations Programme on HIV/AIDS between 1995 and 2008, and is currently a coronavirus adviser to European Commission President Ursula von der Leyen.

I was concerned I would be put on a ventilator immediately because I had seen publications showing it increases your chance of dying. I was pretty scared, but fortunately, they just gave me an oxygen mask first and that turned out to work. So, I ended up in an isolation room in the antechamber of the intensive care department. You’re tired, so you’re resigned to your fate. You completely surrender to the nursing staff. You live in a routine from syringe to infusion and you hope you make it. I am usually quite proactive in the way I operate, but here I was 100% patient.

I shared a room with a homeless person, a Colombian cleaner, and a man from Bangladesh—all three diabetics, incidentally, which is consistent with the known picture of the disease. The days and nights were lonely because no one had the energy to talk. I could only whisper for weeks; even now, my voice loses power in the evening. But I always had that question going around in my head: How will I be when I get out of this?

And he talks about the long-term health issues some COVID-19 survivors will face.

Many people think COVID-19 kills 1% of patients, and the rest get away with some flulike symptoms. But the story gets more complicated. Many people will be left with chronic kidney and heart problems. Even their neural system is disrupted. There will be hundreds of thousands of people worldwide, possibly more, who will need treatments such as renal dialysis for the rest of their lives. The more we learn about the coronavirus, the more questions arise. We are learning while we are sailing. That’s why I get so annoyed by the many commentators on the sidelines who, without much insight, criticize the scientists and policymakers trying hard to get the epidemic under control. That’s very unfair.

NHK conducted an experiment to see how germs spread at a cruise buffet.

— Spoon & Tamago (@Johnny_suputama) May 8, 2020

They applied fluorescent paint to the hands of 1 person and then had a group of 10 people dine.

In 30 min the paint had transferred to every individual and was on the faces of 3.

pic.twitter.com/1Ieb9ffehp

4) Printing and devaluing money the easiest way out of a debt crisis.

Ray Dalio, founder of investment management firm Bridgewater Associates, has published an appendix to chapter two of his upcoming book The Changing World Order. In it Dalio looks at four levers policy makers can pull to bring debt and debt-service levels down relative to the income and cash-flow levels required to service debts. In a COVID-19 ravaged world, governments, corporates and households will be looking to do this.

The four levers Dalio cites are austerity, or spending less, debt defaults and restructurings, transfers of money and credit from those who have more than they need to those who have less than they need (e.g. raising taxes), and printing money and devaluing it.

In comparison to the other options, he argues printing money is the most expedient, least well-understood, and most common big way of restructuring debts.

In fact it seems good rather than bad to most people because it helps to relieve debt squeezes, it’s tough to identify any harmed parties that the wealth was taken away from to provide this financial wealth (though they are the holders of money and debt assets), and in most cases it causes assets to go up in the depreciating currency that people use to measure their wealth in so that it appears that people are getting richer.

You are seeing these things happen now in response to the announcements of the sending out of large amounts of money and credit by central governments and central banks.

Note that you don’t hear anyone complaining about the money and credit creation; in fact you hear cries for a lot more with accusations that the government would be cheap and cruel if it didn’t provide more. There isn’t any acknowledging that the government doesn’t have this money that it is giving out, that the government is just us collectively rather than some rich entity, and that someone has to pay for this. Now imagine what it would have been like if government officials cut expenses to balance their budgets and asked people to do the same, allowing lots of defaults and debt restructurings, and/or they sought to redistribute wealth from those who have more of it to those who have less of it through taxing and redistributing the money. This money and credit producing path is much more acceptable. It’s like playing Monopoly in a way where the banker can make more money and redistribute it to everyone when too many of the players are going broke and getting angry. You can understand why in the Old Testament they called the year that it’s done “the year of Jubilee.”

In the article Dalio also writes extensively about currencies.

Bloomberg has the story of Toronto day trader Syed Shah who, having started April 20 with $77,000 in his account, ended up owing his broker $9 million at the end of the day after trading oil on the day the price sank below zero for the first time ever.

What he didn’t know was oil’s first trip into negative pricing had broken Interactive Brokers Group Inc. Its software couldn’t cope with that pesky minus sign, even though it was always technically possible -- though this was an outlandish idea before the pandemic -- for the crude market to go upside down. Crude was actually around negative $3.70 a barrel when Shah’s screen had it at 1 cent. Interactive Brokers never displayed a subzero price to him as oil kept diving to end the day at minus $37.63 a barrel.

At midnight, Shah got the devastating news: he owed Interactive Brokers $9 million. He’d started the day with $77,000 in his account.

“I was in shock,” the 30-year-old said in a phone interview. “I felt like everything was going to be taken from me, all my assets.”

Thomas Peterffy, chairman and founder of Interactive Brokers, told Bloomberg the dramatic fall in the price of oil futures exposed bugs in his company’s software. Peterffy described this as "a $113 million mistake on our part”.

Customers will be made whole, Peterffy said. “We will rebate from our own funds to our customers who were locked in with a long position during the time the price was negative any losses they suffered below zero.”

That could help Shah. The day trader in Mississauga, Canada, bought his first five contracts for $3.30 each at 1:19 p.m. that historic Monday. Over the next 40 minutes or so he bought 21 more, the last for 50 cents. He tried to put an order in for a negative price, but the Interactive Brokers system rejected it, so he became more convinced that it wasn’t possible for oil to go below zero. At 2:11 p.m., he placed that dream-turned-nightmare trade at a penny.

Hairdressers and barber shops will be in hot demand once they reopen from Thursday. Epsom MP David Seymour might be among their customers...

26 Comments

I hope all those in here saying it was a waste of money having a lockdown just to "save a few old people" read item 3) by Peter Piot above about the ongoing major health issues for a large swathe of the population who catch the virus.Remembering we already feature highly in global statistics for diabetes before this came along.Our health system would be paying for this for many years if we didn't intervene.

I saw a surgeon on the news the other day, practicality in tears, talking about how terrified the medical profession had been about the prospect of Covid taking off here.

Don't forget in an outbreak we'd be expecting our doctors and nurses to be on the front line, risking the health of themselves and their families, and suffering the trauma of being powerless to stop large numbers of fatalities.

There are more dangerous jobs out there than healthcare - even in a pandemic. "...the data does not clearly show that healthcare workers are dying at rates proportionately higher than other employed individuals or even the population as a whole."

https://www.hsj.co.uk/exclusive-deaths-of-nhs-staff-from-covid-19-analy…

They may read it and a hundred more like it but I doubt it will lead to any changing of minds.

Seems the jig’s up !

https://sorendreier.com/washington-times-coronavirus-hype-biggest-polit…

Dalio is a very accomplished man. But to say :

"... you don’t hear anyone complaining about the money and credit creation" isn't quite right.

Many complain that it's the wrong thing to do, (even John Key, to his credit, did!) but they get swept away by the illusions created by MMT and the like.

As was noted earlier "It's going to end badly".

(Roubini, for instance)

MMT Has Become Mainstream.....But as people say, you can fool some of the people all of the time and all of the people some of the time, but you cannot fool all of the people all of the time.

https://thesoundingline.com/nouriel-roubini-mmt-has-become-mainstream-s…

And it's not like he didn't see what was coming! ( from 2018)

NOURIEL ROUBINI PREDICTS A CRISIS BY 2020 : WHAT TO MAKE OF IT?

https://www.goldbroker.com/news/nouriel-roubini-predicts-crisis-by-2020…

#2 is very concerning - historically threatened nation leaderships have used wars to distract their populations. Every country mentioned here has strongly patriotic citizenry, even while admitting the faults of their leaders. The late 20th, and post millennial belief that globalisation will reduce the threat of a global war may be undermined by the pandemic. Can we make sure someone keeps Trump away from his buttons, especially the big ones?

Agree. I think the world is closer to the brink than we have been in a long time. A lot of events could trigger it too. I've been watching the oil price saga as one potential trigger, OPEC+ falling apart lead to a sharp fall in oil prices prior to the fall in demand from Covid. This badly hurts the US oil industry, if it continues I would not at all be surprised to see them intervening further in the middle east to destabilise the region and drive oil prices back up. Lots of saber rattling with Iran this year and last.

It's not 'to drive oil prices back up' - it's to get energy. The US, ex lockdown, consumes 18-plus million barrels a day. It extracts 12, 2/3rds of that from fracking.

A modern 'economy' (which is nothing more than the extraction, processing, consumption and excretion of parts of the planet) needs compact energy; energy which doesn't need a high proportion of itself to extract itself. Fracking is below that line, but it is still energy. My guess is that nobody gets EROEI and that they bail out fracking, adding to their already unrepayable debt. Reminds one of The Big Short. The high-EROEI energy is mostly in the ME, and yes, we will see continued US presence there. Indeed, their withdrawal will signal the end of their Empire more clearly than anything else.

But there isn't the high-EROEI energy nor the concentrated resource-stocks left, for China to take over (not at that scale anyway; presumably anyone can rule the planet whatever size their 'economy').

And yet Trump was nearly overthrown on the basis he wanted better relations with Russia? And North Korea, and, yes, even China and Iran in the early days.

I'll suggest he's been as far away from The Button as any of his predecessors - especially Bush(s)!

Even after all these years, the US public want nothing to do with the Kremlin and more recently, the CCP.

He possibly has, even though he publicly made it very clear to Kim Jong Un that he considered his button to be bigger than Kim's. But amongst America's political class there is a status with being a 'wartime' president, and Trump is just as likely to seek that. This was part of Bush junior's attitude, following in daddy's footsteps but also finishing a job that many saw as unfinished.

Also, congratulations Fart Face Gareth on your reportedly rambunctious and voluminous achievements.

Gareth Vaughan are you my soul mate?

I jest. I'm happily married but I agree with you HARD and I like the cut of your jib. I have tried making similar points on the economy in a pandemic but I just sound like another key board warrior with an axe to grind. Whereas you have laid it out marvellously, so thank you.

Plus my husband and I just bellied laughed for the Disco Stu reference, thanks for that too.

The study was done at a time when the world had just been through war, which has question marks over the health of the population. It was also rebuilding, the USA in particular was still a growing empire, there was plenty of growth left in the tank. There was less intrustion by the state in peoples lives, government was much cheaper to run by a factor of about 15, so less demand on free enterprise. It is a very different ball game now.

What I've noticed is that anyone with any sort of medical background is jumping at the chance to get a moment in the sun. From a psychological point of view I see this as a retreat to a safe place, a backstop to something they know to give them meaning in life in a troubled time. I don't think medicine is equipped to understand the complex and dynamic nature of the overall problem because of bias. There is also the arrogance that nature can be controlled. My guess is nature is going to kick a*** no matter much intervention is wasted on trying to stop it. I am talking multi year here, not just the next year or two.

One of the most interesting perspectives out there is that a professor of risk management, Nicholas Taleb, has vey little regard for epidemiologists.

I agree scarfie, there are multiple complex factors that make this pandemic and recession unique. We really have no idea what this level of debt and stimulus will do to our societies and cultures moving forward in this type of crisis, let alone fractured supply chains.

Some suggest that paternalistic government is something society tends to want during difficult times and this is a proposed phenomena in the lead up to and during WW2. To infer that onto the current era, paternalistic or even autocratic government might be something many want. That doesn't suit everyone obviously, but much of the desire and lean towards that might be subconscious rather than actively chosen. There has definitely been a huge uptake in paternalism around the globe. If that kind of government action is successful both practically and psychologically, then the theory goes that they cultural perception of fear is less traumatic, people return more readily to a positive mindset and there is renewed economic vigour. Historians have suggested this to explain why Churchill was booted out again so soon after the war. The worry of course, is that after the crisis, the paternalistic leaders remain, intruding further on our privacy and freedoms (most revolutions seem to end this way).

I agree that there huge psychological processes going on for all of us and I have no doubt that this will play out politically in some way. As for the medically trained getting a moment in the sun... considering the idolisation of sports stars, social media celebrities, loveisland contestants, is it not natural that people who we have ignored and underpaid for decades and who we have suddenly been reminded are valuable, might get a little time in sun? In a health crisis, I would think that was pretty natural.

As for arrogance, we have been trying to control nature since the beginning...we mastered fire, made flint tools, dug trenches. We have manipulated nature to increase our chances of survival since before we were homo sapien. Nature has kicked our asses plenty and we always find a way to adapt eventually but I do agree that it could be a multi year issue. I will be very surprised if this is over in a few months and we are all dancing on the other end of a the recovery V.

Nice reply. Just a response on the time in the sun. No problem with those who derive their satisfaction in life from caring for others and I totally agree we've warped our priorities. I'd suspect most of those don't really need time in the sun, they just get on with it. I am with you on the warped world of media, I mean we also give guys narcissists like Mike Hosking air time. Why is he listened to at all when his only area of expertise is his own ego.

The problem I am seeing with a few very vocal friends is that they can't separate their bias and thus also lose consistency in their thinking. I'd extend what I say about medicine to those with any sort of scienct bent. They are viewing this is a purely science problem when it is clearly much more than that.

As for paternalism, do you think that is about wanting someone else to solve our problems? In regard to my own health I take the opposite position, it is all up to me.

An interesting article on Taiwan's Vice President Chen Chien-jen, who is also an epidemiologist, here https://www.nytimes.com/2020/05/09/world/asia/taiwan-vice-president-coronavirus.html?smid=fb-nytimes&smtyp=cur&fbclid=IwAR3h_Hhv5s5aq_FEUnEUEZFRxsp_AJcSYJnV5icN5nx9s_7Pp983dBg5XR0

#3 and i have thought this for a while. There is already enough information to indicate that if you catch this, even if you survive, the effects will be with you perhaps forever. Those selfish individuals who refuse to self-isolate or quarantine should face significant punishment.

Good top 5, the guy losing $9m was very lucky there was a glitch.

It sounds like it may be time for us to take our household budgets in a couple of notches as recession gets baked in and we all ask if it will be a depression scenario.

An intra-day trader, I used Interactive Brokers for 11 years. Good platform. Had (what I called) a Taxi Meter on the screen that showed a running profit or loss on any position. One day the market was particularly thin and some outfit hit the market with a large sweep order that cleaned out the order-book, sweeping it up 400 points until it ran out of depth. In 3 seconds the taxi-meter flashed bright red showing me down $7000. Jaw-droppingly fast. Luckily there was enough in the account to cover without tipping me out. Market came back into profit within the hour. One person that day went short on the way down and covered with a profit well in the money. The exchange then cancelled all trades above a set figure which included his entry. Not good. He lost $400,000

Ouch!!! My goodness your body must have been burning through Adrenalin doing that job!

1957 Asian flu an economic comparison? Similar amount of death in the US, 2 million globally. Or 2018 with 80,000 influenza deaths - even with a vaccine. Similar number of deaths in US but no lockdown - and no depression.

"The 1957 Asian Flu Pandemic killed around 70 to 100 thousand people in the United States (the 57 flu was not as infectious or deadly as COVID-19). In the last quarter of 1957 the growth rate (on an annualized basis) was -4% and in the first quarter of 1958, -10%, the largest such decline in post WWII history, bigger even than in the financial crisis. By the third and fourth quarters of 1958, however, the growth rate had surged back up to nearly 10% and for the year as a whole GDP declined by less than 1%–a bad recession, 3rd worst by depth in post WWII history, but not unprecedented.

Many sources don’t even list the pandemic as a cause of the recession (Wikipedia lists it as one among several causes). Indeed, the pandemic was soon forgotten. James Patterson’s Grand Expectations: The United States, 1945-1974 doesn’t even mention the pandemic or the recession, just the boom years of the 1950s."

https://marginalrevolution.com/marginalrevolution/2020/03/the-forgotten…

Funnily enough, for the sheer number of deaths that the 1918 flu pandemic caused and the economic disruption that followed, it also has a very low profile (or did before Covid-19) compared to the two wars and many other events of the 20th century. Many folk seem to have no idea it killed so many.

Yes, medically SF was a much bigger event but economically a fizzer. Stock market wobbled 8% but 6 months later was up 50% (Dow).

Difference now is the debt taken on over the last decade or so. C19 has just been the proverbial straw that has brought on what was probably inevitable.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.